444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Vietnam oil and gas upstream market represents a critical component of Southeast Asia’s energy landscape, characterized by significant offshore exploration activities and strategic government initiatives. Vietnam’s upstream sector encompasses exploration, development, and production activities across both onshore and offshore fields, with the majority of operations concentrated in the South China Sea region. The market demonstrates robust growth potential driven by increasing domestic energy demand, foreign investment partnerships, and technological advancement in deepwater drilling capabilities.

Market dynamics indicate that Vietnam’s upstream oil and gas sector is experiencing a transformative period, with enhanced recovery techniques contributing to 15-20% improvement in extraction efficiency across mature fields. The country’s strategic location along major shipping routes and its established infrastructure make it an attractive destination for international oil companies seeking expansion opportunities in Southeast Asian markets.

Government policies continue to play a pivotal role in shaping market development, with recent regulatory reforms aimed at attracting foreign direct investment and modernizing the legal framework governing upstream activities. The sector benefits from Vietnam’s commitment to energy security and economic diversification, positioning the upstream market as a cornerstone of national energy strategy.

The Vietnam oil and gas upstream market refers to the comprehensive ecosystem of exploration, drilling, and production activities conducted within Vietnamese territorial waters and onshore regions for the extraction of crude oil and natural gas resources. This market encompasses all activities from initial geological surveys and seismic studies to well completion and early-stage production operations.

Upstream operations in Vietnam involve sophisticated technological processes including offshore platform development, subsea infrastructure installation, and advanced drilling techniques designed to access hydrocarbon reserves in challenging deepwater environments. The market includes both state-owned enterprises and international joint ventures working under production sharing contracts and technical service agreements.

Key characteristics of Vietnam’s upstream market include its heavy reliance on offshore production, with approximately 85% of total production originating from offshore fields, advanced technological requirements for deepwater exploration, and strategic partnerships between Vietnamese national oil companies and international operators bringing expertise and capital investment to complex projects.

Vietnam’s oil and gas upstream market stands as a dynamic sector experiencing steady growth driven by technological innovation, strategic partnerships, and government support for energy sector development. The market demonstrates resilience through diversified production portfolios and continuous investment in exploration activities across promising geological formations.

Key market drivers include increasing domestic energy consumption, which has grown at 6-8% annually over recent years, strategic government initiatives promoting foreign investment, and technological advancements enabling access to previously uneconomical reserves. The sector benefits from Vietnam’s established position as a regional energy hub and its commitment to maintaining energy security through domestic production enhancement.

Market challenges encompass regulatory complexity, environmental compliance requirements, and the technical difficulties associated with deepwater exploration in the South China Sea. However, these challenges are being addressed through international collaboration, technology transfer programs, and continuous improvement in operational efficiency.

Future prospects remain positive, with multiple exploration blocks under development and significant potential for discovering new reserves through advanced seismic technologies and enhanced exploration techniques. The market is positioned for sustained growth supported by favorable government policies and increasing international investment interest.

Strategic insights reveal that Vietnam’s upstream oil and gas market operates within a complex framework of international partnerships, technological innovation, and regulatory evolution. The market demonstrates several critical characteristics that define its current trajectory and future potential.

Primary market drivers propelling Vietnam’s oil and gas upstream sector include robust domestic energy demand growth, strategic government policies supporting sector development, and increasing international investment in exploration and production activities. These drivers create a favorable environment for sustained market expansion and technological advancement.

Energy demand growth represents the most significant driver, with Vietnam’s rapidly expanding economy requiring increased energy supply to support industrial development, urbanization, and rising living standards. The country’s energy consumption has demonstrated consistent growth patterns, creating strong market fundamentals for upstream development.

Government initiatives play a crucial role in market development through policy reforms, investment incentives, and infrastructure development programs. Recent regulatory changes have simplified licensing procedures and improved terms for international investors, making Vietnam an increasingly attractive destination for upstream investment.

Technological advancement enables access to previously uneconomical reserves and improves operational efficiency across existing fields. Advanced drilling techniques, enhanced recovery methods, and digital technologies are transforming operational capabilities and extending field life cycles.

International partnerships bring essential expertise, technology, and capital investment to Vietnam’s upstream sector. These collaborations facilitate knowledge transfer, risk sharing, and access to global markets, accelerating sector development and improving competitive positioning.

Market restraints affecting Vietnam’s oil and gas upstream sector include regulatory complexity, environmental compliance requirements, technical challenges associated with deepwater operations, and geopolitical considerations affecting regional development activities.

Regulatory challenges encompass complex licensing procedures, evolving environmental standards, and coordination requirements between multiple government agencies. These factors can create delays in project development and increase operational costs for upstream operators.

Technical difficulties associated with deepwater exploration and production present significant challenges, requiring specialized equipment, advanced technologies, and highly skilled personnel. The harsh marine environment and complex geological conditions increase operational risks and capital requirements.

Environmental considerations are becoming increasingly important, with stricter regulations governing offshore operations, waste management, and ecosystem protection. Compliance with these requirements necessitates additional investment in environmental technologies and monitoring systems.

Capital intensity of upstream projects requires substantial initial investment and long-term commitment, creating barriers for smaller operators and limiting market participation to well-capitalized companies with proven technical capabilities.

Significant opportunities exist within Vietnam’s oil and gas upstream market, driven by untapped reserves, technological innovation potential, and expanding regional energy integration initiatives. These opportunities position the market for substantial growth and development over the coming years.

Exploration potential remains substantial, with numerous unexplored blocks offering prospects for new discoveries. Advanced seismic technologies and improved geological understanding are revealing previously unknown hydrocarbon accumulations, creating opportunities for both established operators and new market entrants.

Enhanced recovery techniques present opportunities to increase production from existing fields, with potential for 20-30% improvement in recovery rates through implementation of advanced technologies. These techniques can extend field life and improve project economics significantly.

Natural gas development offers substantial opportunities as Vietnam seeks to diversify its energy mix and reduce dependence on coal-fired power generation. Growing demand for cleaner energy sources creates favorable conditions for gas field development and infrastructure expansion.

Regional integration projects provide opportunities for cross-border pipeline development, shared infrastructure utilization, and collaborative exploration programs. These initiatives can reduce costs and improve market access for Vietnamese upstream operators.

Technology partnerships offer opportunities for knowledge transfer, capability development, and access to cutting-edge technologies that can improve operational efficiency and reduce environmental impact across upstream operations.

Market dynamics within Vietnam’s oil and gas upstream sector reflect the complex interplay of domestic policy initiatives, international investment flows, technological advancement, and regional energy market developments. These dynamics create both challenges and opportunities for market participants.

Supply and demand dynamics are influenced by Vietnam’s growing energy consumption, regional market integration, and global commodity price fluctuations. Domestic production capabilities must balance against import requirements and export opportunities, creating complex market dynamics that affect investment decisions.

Investment patterns demonstrate increasing international interest in Vietnam’s upstream sector, with foreign direct investment contributing advanced technology and capital resources essential for deepwater development projects. According to MarkWide Research analysis, international partnerships account for approximately 70% of major upstream investments in Vietnam.

Competitive dynamics involve both state-owned enterprises and international oil companies competing for exploration blocks, development opportunities, and market share. This competition drives innovation, improves operational efficiency, and accelerates technology adoption across the sector.

Regulatory dynamics continue evolving as the government seeks to balance energy security objectives, environmental protection requirements, and economic development goals. Recent policy reforms have improved investment conditions while maintaining strategic control over critical energy resources.

Comprehensive research methodology employed in analyzing Vietnam’s oil and gas upstream market incorporates multiple data sources, analytical frameworks, and validation techniques to ensure accuracy and reliability of market insights and projections.

Primary research activities include structured interviews with industry executives, government officials, and technical experts involved in upstream operations. These interviews provide firsthand insights into market conditions, operational challenges, and future development plans across the sector.

Secondary research encompasses analysis of government publications, industry reports, company financial statements, and regulatory documents to establish comprehensive understanding of market structure, competitive landscape, and regulatory environment affecting upstream activities.

Data validation processes involve cross-referencing information from multiple sources, conducting expert reviews, and applying statistical analysis techniques to ensure data accuracy and consistency. This rigorous approach provides reliable foundation for market analysis and forecasting.

Analytical frameworks include market segmentation analysis, competitive positioning assessment, regulatory impact evaluation, and technology trend analysis. These frameworks enable comprehensive understanding of market dynamics and identification of key growth drivers and constraints.

Regional analysis of Vietnam’s oil and gas upstream market reveals distinct geographical patterns of activity, resource distribution, and development potential across different offshore and onshore areas. The market demonstrates significant regional variation in terms of production levels, exploration activity, and infrastructure development.

Southern offshore regions dominate Vietnam’s upstream production, accounting for approximately 75% of total hydrocarbon output. These areas benefit from established infrastructure, proven reserves, and favorable geological conditions that support continued development and expansion activities.

Northern offshore areas represent emerging opportunities with significant exploration potential and growing international interest. Recent discoveries in these regions have attracted substantial investment and indicate promising prospects for future development activities.

Central coastal regions offer opportunities for both offshore and onshore development, with particular potential for natural gas production and processing facilities. These areas benefit from proximity to major population centers and existing industrial infrastructure.

Onshore regions contribute a smaller portion of total production but offer opportunities for enhanced recovery projects and unconventional resource development. These areas benefit from lower operational costs and reduced technical complexity compared to offshore operations.

Infrastructure distribution varies significantly across regions, with southern areas benefiting from established pipeline networks, processing facilities, and support infrastructure, while northern and central regions require additional investment in infrastructure development to support expanded operations.

Competitive landscape within Vietnam’s oil and gas upstream market features a diverse mix of state-owned enterprises, international oil companies, and specialized service providers working together through various partnership structures and operational arrangements.

Partnership structures typically involve production sharing contracts, joint ventures, and technical service agreements that combine international expertise with local knowledge and regulatory compliance capabilities.

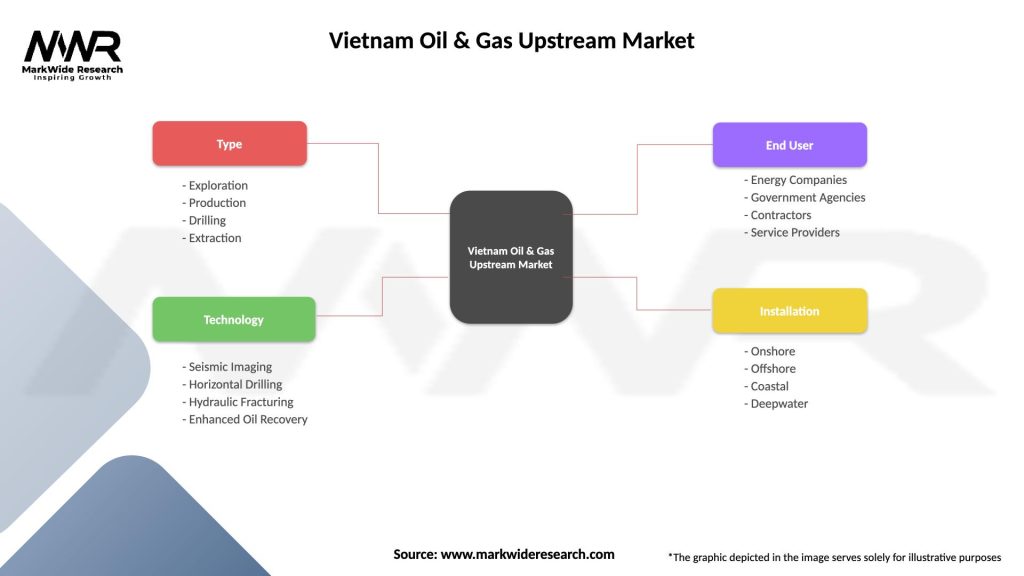

Market segmentation within Vietnam’s oil and gas upstream sector can be analyzed across multiple dimensions including operational type, geographical location, resource type, and development stage. This segmentation provides detailed understanding of market structure and growth opportunities.

By Operational Type:

By Location:

By Resource Type:

Category-wise analysis reveals distinct characteristics, growth patterns, and development opportunities across different segments of Vietnam’s oil and gas upstream market. Each category demonstrates unique operational requirements, investment patterns, and market dynamics.

Offshore Oil Production represents the dominant category, contributing the majority of Vietnam’s hydrocarbon output through established platforms and production facilities. This category benefits from proven reserves, established infrastructure, and continuous technology upgrades that improve operational efficiency and extend field life.

Natural Gas Development emerges as a rapidly growing category driven by increasing domestic demand and government policies promoting cleaner energy sources. This segment offers substantial growth potential with gas production increasing at rates exceeding overall hydrocarbon growth, supported by expanding pipeline infrastructure and processing capabilities.

Deepwater Exploration represents the frontier category with highest growth potential but also greatest technical challenges and capital requirements. Advanced drilling technologies and enhanced seismic capabilities are opening new opportunities in previously inaccessible areas.

Enhanced Recovery Operations provide opportunities for increasing production from existing fields through technological innovation and operational optimization. This category offers attractive returns on investment with lower risk profiles compared to greenfield exploration projects.

Onshore Development offers opportunities for cost-effective production and enhanced recovery projects, particularly in areas with existing infrastructure and established geological understanding.

Industry participants in Vietnam’s oil and gas upstream market benefit from multiple advantages including access to proven reserves, established infrastructure, government support, and strategic geographical positioning within Southeast Asia’s energy corridor.

Operational benefits include access to experienced local workforce, established supply chain networks, and comprehensive support infrastructure that reduces operational costs and improves project efficiency. The mature regulatory framework provides clarity and predictability for long-term investment planning.

Strategic advantages encompass Vietnam’s position as a regional energy hub, access to growing domestic markets, and opportunities for regional export through established trade relationships. The country’s commitment to energy security creates stable demand conditions for upstream production.

Technology benefits arise from international partnerships that facilitate knowledge transfer, access to advanced technologies, and collaborative research and development initiatives. These partnerships accelerate capability development and improve competitive positioning.

Financial advantages include attractive fiscal terms, investment incentives, and access to regional capital markets. The government’s commitment to foreign investment creates favorable conditions for project financing and risk management.

Market access benefits provide opportunities for both domestic sales and regional export, supported by established infrastructure and trade relationships. The growing domestic market offers stable demand conditions while regional integration creates additional revenue opportunities.

Strengths:

Weaknesses:

Opportunities:

Threats:

Key market trends shaping Vietnam’s oil and gas upstream sector include technological digitalization, environmental sustainability focus, enhanced recovery adoption, and regional market integration initiatives. These trends are transforming operational practices and creating new opportunities for growth and development.

Digital transformation represents a major trend with operators implementing advanced analytics, artificial intelligence, and automated systems to improve operational efficiency and reduce costs. Digital technologies are enabling predictive maintenance, optimized drilling operations, and enhanced reservoir management across upstream operations.

Sustainability initiatives are becoming increasingly important as operators adopt cleaner technologies, reduce environmental impact, and implement carbon management strategies. This trend is driven by both regulatory requirements and corporate responsibility commitments from international partners.

Enhanced recovery techniques are gaining widespread adoption as operators seek to maximize production from existing fields. Advanced technologies including chemical flooding, gas injection, and thermal recovery are improving recovery rates by 15-25% in suitable applications.

Regional cooperation trends include cross-border pipeline projects, shared infrastructure development, and collaborative exploration programs that reduce costs and improve market access for Vietnamese upstream operators.

Technology partnerships are expanding as Vietnamese companies seek to develop domestic capabilities through collaboration with international technology providers, creating opportunities for knowledge transfer and capability building.

Recent industry developments in Vietnam’s oil and gas upstream sector demonstrate continued growth momentum, technological advancement, and strategic partnership expansion. These developments indicate positive market trajectory and increasing international confidence in Vietnam’s upstream potential.

Exploration successes in recent years have resulted in significant new discoveries, with several major finds confirming the continued potential for reserve additions. These discoveries have attracted additional international investment and exploration activity across multiple offshore blocks.

Infrastructure expansion projects include new pipeline connections, processing facility upgrades, and platform installations that increase production capacity and improve operational efficiency. These investments demonstrate long-term commitment to Vietnam’s upstream sector development.

Regulatory reforms have streamlined licensing procedures, improved investment terms, and enhanced environmental standards. Recent policy changes have created more favorable conditions for international investment while maintaining strategic control over energy resources.

Technology implementations include deployment of advanced drilling systems, enhanced recovery technologies, and digital monitoring systems that improve operational performance and reduce environmental impact across upstream operations.

Partnership agreements between Vietnamese companies and international operators continue expanding, bringing advanced technology, capital investment, and operational expertise to support sector development and capability building initiatives.

Strategic recommendations for stakeholders in Vietnam’s oil and gas upstream market emphasize the importance of technology adoption, partnership development, regulatory compliance, and sustainable operational practices to maximize growth opportunities and competitive positioning.

Investment priorities should focus on advanced technology acquisition, particularly in areas of enhanced recovery, digital operations, and environmental management. Companies should prioritize partnerships that provide access to cutting-edge technologies and operational expertise essential for complex offshore projects.

Regulatory engagement remains crucial as the policy environment continues evolving. Stakeholders should maintain active dialogue with government agencies, participate in policy development processes, and ensure compliance with emerging environmental and operational standards.

Operational excellence initiatives should emphasize safety, environmental protection, and efficiency improvement through technology adoption and best practice implementation. Companies should invest in workforce development and capability building to support long-term operational success.

Market positioning strategies should leverage Vietnam’s strategic location, growing domestic market, and regional integration opportunities. Companies should develop flexible business models that can adapt to changing market conditions and regulatory requirements.

Sustainability planning should integrate environmental considerations, carbon management, and social responsibility into operational strategies. This approach aligns with global trends and regulatory expectations while supporting long-term market positioning.

Future outlook for Vietnam’s oil and gas upstream market remains positive, supported by continued exploration success, technology advancement, government policy support, and growing regional energy demand. MWR analysis indicates the sector is positioned for sustained growth over the coming decade.

Production growth is expected to continue through development of discovered reserves, implementation of enhanced recovery techniques, and successful exploration in frontier areas. New field developments and production optimization initiatives are projected to maintain steady production growth despite natural field decline rates.

Technology evolution will continue driving operational improvements, cost reductions, and environmental performance enhancements. Advanced drilling techniques, digital technologies, and enhanced recovery methods will enable access to previously uneconomical resources and improve overall sector efficiency.

Investment flows are expected to remain strong, supported by favorable government policies, proven resource potential, and attractive project economics. International partnerships will continue providing essential technology and capital resources for complex upstream projects.

Market integration with regional energy systems will expand through infrastructure development, cross-border projects, and collaborative initiatives that improve market access and reduce operational costs for Vietnamese upstream operators.

Environmental standards will continue evolving, driving adoption of cleaner technologies and sustainable operational practices. Companies that proactively address environmental considerations will be better positioned for long-term success in Vietnam’s upstream market.

Vietnam’s oil and gas upstream market represents a dynamic and growing sector with substantial opportunities for continued development and expansion. The market benefits from proven reserves, established infrastructure, government support, and strategic partnerships with international operators that provide essential technology and expertise.

Key success factors include technological innovation, operational excellence, regulatory compliance, and sustainable development practices that align with evolving market expectations and environmental standards. Companies that effectively integrate these elements will be well-positioned to capitalize on growth opportunities and maintain competitive advantages.

Market fundamentals remain strong, supported by growing domestic energy demand, continued exploration success, and favorable government policies that encourage investment and development. The sector’s strategic importance to Vietnam’s energy security and economic development ensures continued policy support and investment priority.

Future growth prospects are enhanced by technological advancement, regional market integration, and expanding opportunities in natural gas development. The market’s evolution toward more sustainable and efficient operations positions it well for long-term success in the changing global energy landscape, making Vietnam’s upstream sector an attractive destination for continued investment and development activities.

What is Oil & Gas Upstream?

Oil & Gas Upstream refers to the exploration and production segment of the oil and gas industry, focusing on locating and extracting crude oil and natural gas from the earth. This includes activities such as drilling, well completion, and production operations.

What are the key players in the Vietnam Oil & Gas Upstream Market?

Key players in the Vietnam Oil & Gas Upstream Market include PetroVietnam, ExxonMobil, and Chevron, which are involved in exploration, production, and development of oil and gas resources in the region, among others.

What are the growth factors driving the Vietnam Oil & Gas Upstream Market?

The growth of the Vietnam Oil & Gas Upstream Market is driven by increasing energy demand, significant offshore reserves, and government initiatives to enhance exploration activities. Additionally, foreign investments are boosting technological advancements in extraction methods.

What challenges does the Vietnam Oil & Gas Upstream Market face?

The Vietnam Oil & Gas Upstream Market faces challenges such as regulatory hurdles, environmental concerns, and fluctuating global oil prices. These factors can impact investment decisions and operational costs for companies in the sector.

What opportunities exist in the Vietnam Oil & Gas Upstream Market?

Opportunities in the Vietnam Oil & Gas Upstream Market include the potential for new offshore discoveries, partnerships with international firms, and advancements in extraction technologies. These factors can enhance production efficiency and resource recovery.

What trends are shaping the Vietnam Oil & Gas Upstream Market?

Trends in the Vietnam Oil & Gas Upstream Market include a shift towards sustainable practices, increased use of digital technologies for exploration, and a focus on reducing carbon emissions. These trends are influencing how companies operate and invest in the sector.

Vietnam Oil & Gas Upstream Market

| Segmentation Details | Description |

|---|---|

| Type | Exploration, Production, Drilling, Extraction |

| Technology | Seismic Imaging, Horizontal Drilling, Hydraulic Fracturing, Enhanced Oil Recovery |

| End User | Energy Companies, Government Agencies, Contractors, Service Providers |

| Installation | Onshore, Offshore, Coastal, Deepwater |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Vietnam Oil & Gas Upstream Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.