Vietnam’s oil and gas midstream market plays a crucial role in the country’s energy sector. The midstream sector encompasses the transportation, storage, and wholesale marketing of petroleum products, natural gas, and crude oil. It acts as a bridge between upstream exploration and production activities and downstream refining and distribution processes. The midstream market is essential for ensuring a steady and reliable supply of energy resources to meet the demands of various industries and consumers.

Meaning

The term “oil and gas midstream” refers to the infrastructure and activities involved in transporting, storing, and distributing petroleum products, natural gas, and crude oil. It includes pipelines, storage facilities, terminals, liquefied natural gas (LNG) plants, and other necessary infrastructure. The midstream sector plays a pivotal role in the energy value chain by enabling the efficient and reliable movement of energy resources from production sites to refineries and end-users.

Executive Summary

The Vietnam oil and gas midstream market has witnessed significant growth in recent years. The country’s strategic location in Southeast Asia, coupled with its increasing energy demands, has contributed to the expansion of the midstream sector. The government’s focus on developing infrastructure and attracting foreign investments has further fueled the market’s growth. However, challenges such as regulatory complexities and environmental concerns need to be addressed for sustainable development.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Rising Energy Demand: Vietnam’s rapid industrialization, urbanization, and population growth have led to a substantial increase in energy consumption. This surge in demand has created opportunities for the expansion of the oil and gas midstream market.

Infrastructure Development: The Vietnamese government has initiated several infrastructure development projects to enhance the midstream sector. These projects aim to improve transportation networks, construct new pipelines, and expand storage capacities.

Foreign Investments: The government’s efforts to attract foreign investments have resulted in collaborations between international companies and Vietnamese counterparts. These partnerships have contributed to technology transfer, capital infusion, and knowledge sharing in the midstream sector.

Shift towards Natural Gas: With a focus on reducing greenhouse gas emissions and diversifying the energy mix, Vietnam has been shifting towards natural gas as a cleaner fuel source. This transition has increased the demand for natural gas infrastructure and midstream facilities.

Market Drivers

Economic Growth and Industrialization: Vietnam’s robust economic growth and expanding industrial sectors, such as manufacturing and petrochemicals, have driven the demand for energy resources. This has created a need for efficient midstream infrastructure to support the growing energy requirements.

Government Initiatives and Policies: The Vietnamese government has implemented policies and initiatives to promote energy development and attract investments in the midstream sector. These measures include tax incentives, regulatory reforms, and the establishment of special economic zones to encourage foreign direct investment.

Regional Energy Integration: Vietnam is actively participating in regional energy integration initiatives, such as the ASEAN Power Grid and the Greater Mekong Subregion Energy Cooperation. These initiatives aim to enhance energy connectivity, promote cross-border trade, and facilitate the development of regional midstream infrastructure.

Expanding LNG Infrastructure: The increasing demand for liquefied natural gas (LNG) has led to the development of LNG import terminals and regasification facilities in Vietnam. This infrastructure expansion supports the importation and distribution of LNG, thereby driving the growth of the midstream market.

Market Restraints

Regulatory Complexities: The oil and gas midstream sector in Vietnam faces regulatory complexities and bureaucratic hurdles. Streamlining the permitting and licensing processes, ensuring transparency, and providing a stable regulatory environment are essential for attracting investments and facilitating market growth.

Environmental Concerns: The development of midstream infrastructure can have environmental impacts, including land use changes, emissions, and potential risks to ecosystems. Balancing economic development with environmental sustainability is crucial for the long-term viability of the midstream market.

Capital Intensive Nature: The establishment of midstream infrastructure requires significant capital investments. Access to funding and securing long-term financing can be challenging, especially for smaller market participants. Limited financial resources may hinder the development of the midstream sector.

Market Opportunities

Expansion of Pipeline Networks: There is a significant opportunity to expand the pipeline network in Vietnam to improve connectivity between production areas, refineries, and consumption centers. Investments in pipeline infrastructure will enhance the efficiency and reliability of oil and gas transportation.

Integration of Renewable Energy: As the country aims to increase the share of renewable energy in its energy mix, there is an opportunity to integrate renewable energy sources with the midstream sector. This includes developing infrastructure for the transportation and storage of biofuels, biogas, and hydrogen.

International Cooperation: Collaboration with international companies and leveraging their expertise can bring technological advancements, capital investment, and knowledge transfer to the Vietnamese midstream market. Strategic partnerships and joint ventures can help accelerate market growth and enhance capabilities.

LNG Infrastructure Development: Vietnam’s growing demand for LNG presents opportunities for further investment in LNG import terminals, storage facilities, and associated infrastructure. This infrastructure expansion will facilitate the importation, storage, and distribution of LNG to meet the country’s energy requirements.

Market Dynamics

The Vietnam oil and gas midstream market is characterized by intense competition, evolving regulations, and changing market dynamics. The market dynamics are influenced by factors such as geopolitical developments, global energy trends, technological advancements, and environmental considerations. Market participants need to adapt to these dynamics, innovate their offerings, and align their strategies with market requirements to stay competitive and capitalize on emerging opportunities.

Regional Analysis

Vietnam’s oil and gas midstream market exhibits regional variations in terms of infrastructure development, energy demand, and market dynamics. The northern region, including Hanoi and Hai Phong, is a significant hub for oil and gas activities, with several refineries and storage facilities. The southern region, particularly Ho Chi Minh City and Vung Tau, is home to major ports and plays a crucial role in the import and export of petroleum products. The central region is emerging as a potential location for new infrastructure development and oil and gas exploration activities.

Competitive Landscape

Leading Companies in Vietnam Oil and Gas Midstream Market:

Vietnam National Oil and Gas Group (PetroVietnam)

Vietnam Gas Corporation (PV GAS)

Binh Son Refining and Petrochemical Company Limited (BSR)

PetroVietnam Gas Joint Stock Corporation (PV GAS)

PV Oil Corporation

Vietnam Petroleum Institute (VPI)

Cửu Long Joint Operating Company (CLJOC)

Idemitsu Q8 Petroleum Limited Liability Company (IQ8)

Lam Son Joint Operating Company (LSJOC)

Thang Long Joint Operating Company (TLJOC)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

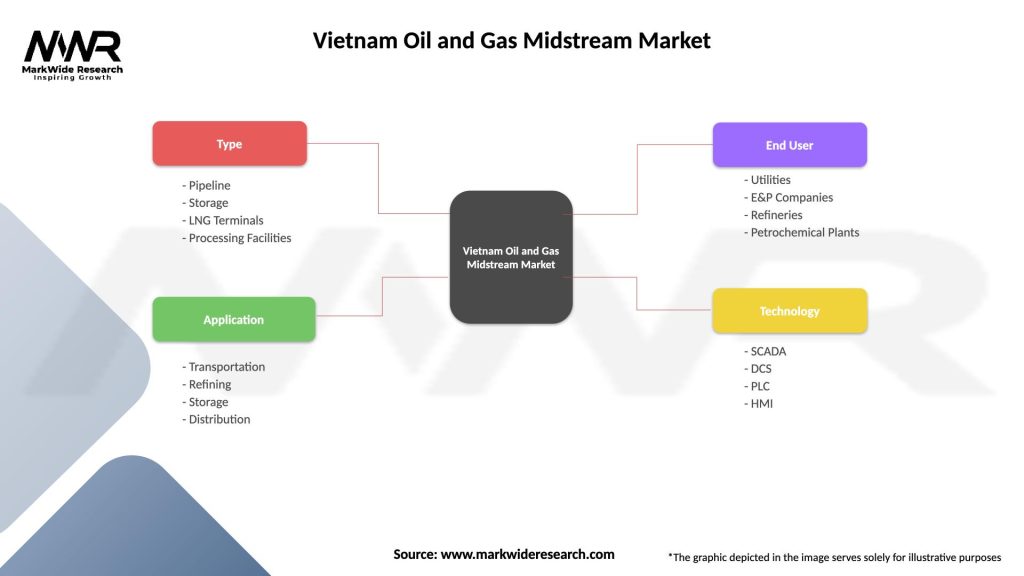

Segmentation

The Vietnam oil and gas midstream market can be segmented based on infrastructure type, product type, and end-use sectors.

Infrastructure Type:

Pipelines

Storage Facilities

LNG Terminals

Refining Facilities

Others

Product Type:

Crude Oil

Natural Gas

Petroleum Products

LNG

Others

End-use Sectors:

Power Generation

Industrial

Residential and Commercial

Transportation

Others

Category-wise Insights

Pipelines: Pipelines form a critical component of the midstream infrastructure, enabling the efficient transportation of oil, gas, and petroleum products across the country. The expansion and modernization of pipeline networks are essential to ensure a reliable supply of energy resources to various sectors.

Storage Facilities: Storage facilities play a vital role in maintaining an adequate inventory of oil, gas, and petroleum products. The construction of new storage tanks and terminals, along with the upgrade of existing facilities, is necessary to meet the growing demand and ensure energy security.

LNG Terminals: With the increasing demand for natural gas and LNG, the development of LNG import terminals is crucial. These terminals receive, store, and regasify LNG for distribution to power plants, industrial facilities, and other consumers.

Refining Facilities: Refining facilities transform crude oil into various petroleum products, including gasoline, diesel, and jet fuel. The modernization and expansion of refining capacities are necessary to meet the domestic demand for petroleum products and reduce reliance on imports.

Key Benefits for Industry Participants and Stakeholders

Revenue Generation: The oil and gas midstream market presents revenue-generating opportunities for industry participants through transportation, storage, and wholesale marketing activities. Midstream companies can capitalize on the growing energy demand and leverage their infrastructure to generate profits.

Market Expansion: For stakeholders in the midstream sector, market expansion translates into increased business opportunities and a wider customer base. Expanding infrastructure networks and participating in new projects enable companies to tap into emerging markets and diversify their revenue streams.

Energy Security: A well-developed midstream infrastructure ensures a reliable supply of energy resources, contributing to energy security for the country. Industry participants and stakeholders play a crucial role in maintaining a resilient midstream sector to support uninterrupted energy supply.

Employment and Economic Growth: The development of the midstream sector creates job opportunities and stimulates economic growth. The expansion of infrastructure projects and the establishment of new facilities generate employment across various sectors, including engineering, construction, logistics, and operations.

SWOT Analysis

Strengths:

Strategic Location: Vietnam’s geographic location provides opportunities for energy trade and regional connectivity.

Growing Energy Demand: The country’s increasing energy consumption drives the need for midstream infrastructure development.

Government Support: The government’s initiatives and policies support market growth and attract investments in the midstream sector.

Weaknesses:

Regulatory Complexities: Complex regulatory processes and bureaucratic hurdles pose challenges for market participants.

Environmental Concerns: Balancing environmental sustainability with infrastructure development requires careful planning and mitigation measures.

Capital Intensive Nature: Establishing midstream infrastructure requires significant capital investments, which may pose financial challenges for some players.

Opportunities:

Regional Integration: Participation in regional energy integration initiatives opens up opportunities for cross-border energy trade and infrastructure development.

Renewable Energy Integration: Integrating renewable energy sources with the midstream sector can support the country’s sustainability goals.

Collaboration with International Players: Strategic partnerships with international companies can bring in expertise, capital, and technology transfer.

Threats:

Geopolitical Risks: Political instability, trade tensions, and geopolitical conflicts in the region can impact the midstream market.

Volatile Energy Prices: Fluctuating oil and gas prices can influence market dynamics and profitability.

Technological Disruptions: Rapid technological advancements and the emergence of alternative energy sources may disrupt traditional midstream operations.

Market Key Trends

Shift towards Clean Energy: Vietnam’s commitment to reducing greenhouse gas emissions and transitioning to a cleaner energy mix is driving the adoption of natural gas and renewable energy sources. This trend is reshaping the midstream market, with a focus on developing infrastructure for cleaner fuel sources.

Digitalization and Automation: The midstream sector is increasingly embracing digital technologies and automation to enhance operational efficiency, safety, and asset management. Implementation of technologies such as IoT sensors, data analytics, and predictive maintenance optimizes operations and reduces downtime.

Decentralized Energy Systems: The development of decentralized energy systems, such as mini-grids and off-grid solutions, presents opportunities for the midstream market. These systems require localized midstream infrastructure to connect distributed energy sources with end-users.

Circular Economy Practices: The adoption of circular economy practices in the energy sector promotes resource efficiency, waste reduction, and recycling. Midstream companies are exploring innovative solutions to minimize environmental impacts and optimize the use of resources.

Covid-19 Impact

The Covid-19 pandemic has had a significant impact on the Vietnam oil and gas midstream market. The temporary decline in economic activity and travel restrictions resulted in a decrease in energy demand. Reduced industrial production and transportation activities led to lower fuel consumption and storage capacity utilization. However, as the country gradually recovers and economic activities resume, the midstream sector is expected to rebound, driven by the resumption of energy-intensive industries and infrastructure development projects.

Key Industry Developments

Infrastructure Expansion: Several infrastructure development projects have been initiated to enhance the midstream sector. These projects include the construction of new pipelines, storage facilities, and LNG terminals to improve connectivity and meet growing energy demands.

Renewable Energy Integration: The integration of renewable energy sources, such as solar and wind, into the midstream sector has gained momentum. This involves the development of infrastructure for the transportation and storage of renewable energy-derived fuels and electricity.

International Collaborations: Vietnamese companies have forged partnerships with international players to leverage their expertise and technology in the midstream sector. These collaborations aim to enhance capabilities, improve operational efficiency, and promote knowledge transfer.

Regulatory Reforms: The Vietnamese government has undertaken regulatory reforms to attract investments and promote market competitiveness. Streamlining permitting processes, providing clearer guidelines, and ensuring a stable regulatory environment are some key developments in the sector.

Analyst Suggestions

Regulatory Streamlining: The government should continue efforts to streamline regulatory processes, reduce bureaucratic hurdles, and provide a transparent and stable regulatory environment. This will attract investments, expedite project implementation, and foster market growth.

Sustainability Focus: Balancing economic growth with environmental sustainability is crucial. Midstream companies should adopt sustainable practices, mitigate environmental impacts, and prioritize the development of infrastructure for cleaner energy sources.

Technology Adoption: Embracing digitalization, automation, and advanced technologies can enhance operational efficiency, asset management, and safety. Midstream companies should invest in technologies such as IoT, data analytics, and automation to optimize operations and reduce costs.

Collaborative Partnerships: Encouraging collaborations between domestic and international companies can facilitate technology transfer, capital infusion, and knowledge sharing. Joint ventures and partnerships can accelerate market development and enhance capabilities.

Future Outlook

The Vietnam oil and gas midstream market is poised for significant growth in the coming years. The government’s focus on infrastructure development, renewable energy integration, and attracting foreign investments will continue to drive market expansion. The shift towards cleaner energy sources, digitalization, and regional energy integration initiatives will shape the future of the midstream sector. However, addressing regulatory complexities, environmental concerns, and ensuring adequate financing will be crucial for sustained growth and long-term success.

Conclusion

The Vietnam oil and gas midstream market plays a vital role in supporting the country’s energy needs. The sector encompasses transportation, storage, and wholesale marketing of petroleum products, natural gas, and crude oil. The market has witnessed substantial growth driven by rising energy demand, government initiatives, and infrastructure development projects. However, challenges such as regulatory complexities, environmental concerns, and the capital-intensive nature of the sector need to be addressed. With opportunities in pipeline expansion, renewable energy integration, and international collaborations, the midstream market holds immense potential. The future outlook remains positive, but stakeholders must adapt to changing market dynamics and leverage technology advancements for sustainable growth in Vietnam’s oil and gas midstream market.

What is Oil and Gas Midstream?

Oil and Gas Midstream refers to the sector involved in the transportation, storage, and processing of oil and gas products. This includes pipelines, storage facilities, and processing plants that connect upstream production with downstream distribution.

What are the key players in the Vietnam Oil and Gas Midstream Market?

Key players in the Vietnam Oil and Gas Midstream Market include PetroVietnam, Vietsovpetro, and PV Gas, which are involved in various aspects of midstream operations such as transportation and storage of hydrocarbons, among others.

What are the growth factors driving the Vietnam Oil and Gas Midstream Market?

The growth of the Vietnam Oil and Gas Midstream Market is driven by increasing energy demand, the expansion of pipeline infrastructure, and investments in storage facilities. Additionally, the government’s focus on energy security and self-sufficiency plays a significant role.

What challenges does the Vietnam Oil and Gas Midstream Market face?

The Vietnam Oil and Gas Midstream Market faces challenges such as regulatory hurdles, environmental concerns, and the need for significant capital investment. Additionally, fluctuating global oil prices can impact project viability.

What opportunities exist in the Vietnam Oil and Gas Midstream Market?

Opportunities in the Vietnam Oil and Gas Midstream Market include the development of new pipeline projects, the integration of advanced technologies for efficiency, and the potential for partnerships with international firms. The shift towards renewable energy sources also presents avenues for innovation.

What trends are shaping the Vietnam Oil and Gas Midstream Market?

Trends in the Vietnam Oil and Gas Midstream Market include the adoption of digital technologies for monitoring and management, increased focus on sustainability practices, and the development of liquefied natural gas (LNG) infrastructure. These trends aim to enhance operational efficiency and reduce environmental impact.

Leading Companies in Vietnam Oil and Gas Midstream Market:

Vietnam National Oil and Gas Group (PetroVietnam)

Vietnam Gas Corporation (PV GAS)

Binh Son Refining and Petrochemical Company Limited (BSR)

PetroVietnam Gas Joint Stock Corporation (PV GAS)

PV Oil Corporation

Vietnam Petroleum Institute (VPI)

Cửu Long Joint Operating Company (CLJOC)

Idemitsu Q8 Petroleum Limited Liability Company (IQ8)

Lam Son Joint Operating Company (LSJOC)

Thang Long Joint Operating Company (TLJOC)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.