444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The US Transportation and Logistics Market represents one of the most critical and dynamic sectors of the American economy, serving as the backbone for commerce, trade, and economic growth across the nation. This comprehensive market encompasses a vast network of transportation modes, logistics services, and supply chain management solutions that facilitate the movement of goods and people throughout the United States and beyond.

Market dynamics indicate that the sector is experiencing unprecedented transformation driven by technological advancement, changing consumer expectations, and evolving business models. The market demonstrates robust growth potential with a projected compound annual growth rate (CAGR) of 6.2% through the forecast period, reflecting the increasing demand for efficient transportation and logistics solutions across various industries.

Digital transformation has emerged as a key catalyst, with approximately 78% of logistics companies investing in advanced technologies such as artificial intelligence, Internet of Things (IoT), and blockchain solutions to optimize operations and enhance service delivery. The integration of these technologies is revolutionizing traditional logistics practices and creating new opportunities for market expansion.

E-commerce growth continues to be a primary driver, with online retail penetration reaching 15.3% of total retail sales, necessitating sophisticated last-mile delivery solutions and warehouse automation systems. This trend has fundamentally altered the logistics landscape, requiring companies to adapt their strategies to meet evolving consumer demands for faster, more reliable delivery services.

The US Transportation and Logistics Market refers to the comprehensive ecosystem of services, infrastructure, and technologies that facilitate the movement, storage, and distribution of goods and people across the United States. This market encompasses multiple transportation modes including trucking, rail, air, maritime, and pipeline transportation, along with supporting logistics services such as warehousing, distribution, freight forwarding, and supply chain management.

Transportation services form the core component, involving the physical movement of cargo and passengers through various modes of transport. Each mode serves specific market segments and geographic regions, with trucking dominating domestic freight movement, accounting for approximately 72% of total freight tonnage transported within the United States.

Logistics services complement transportation by providing value-added solutions including inventory management, order fulfillment, packaging, labeling, and reverse logistics. These services have evolved from basic storage and handling functions to sophisticated supply chain orchestration platforms that optimize efficiency and reduce costs for businesses across industries.

Strategic positioning within the US Transportation and Logistics Market reveals a sector characterized by intense competition, technological innovation, and evolving customer expectations. The market demonstrates remarkable resilience and adaptability, having successfully navigated various economic challenges while maintaining consistent growth trajectories.

Key market segments include freight transportation, passenger transportation, logistics services, and supporting infrastructure. Freight transportation dominates market activity, driven by robust industrial production, manufacturing output, and consumer spending patterns. The sector benefits from America’s extensive transportation infrastructure, including highways, railways, airports, and ports that facilitate efficient goods movement.

Technology adoption has accelerated significantly, with 85% of major logistics providers implementing some form of automation or digital solution to enhance operational efficiency. This technological transformation is reshaping competitive dynamics and creating new business models that prioritize data-driven decision making and customer-centric service delivery.

Market consolidation trends indicate ongoing merger and acquisition activity as companies seek to expand geographic coverage, enhance service capabilities, and achieve economies of scale. This consolidation is particularly evident in the trucking and logistics services segments, where larger players are acquiring smaller regional operators to strengthen market position.

Market intelligence reveals several critical insights that define the current state and future trajectory of the US Transportation and Logistics Market:

According to MarkWide Research, these insights collectively indicate a market in transition, where traditional business models are being challenged by technological innovation and changing customer demands. Companies that successfully adapt to these trends are positioned to capture significant market opportunities.

Economic growth serves as the primary driver for the US Transportation and Logistics Market, with GDP expansion directly correlating to increased freight movement and transportation demand. Industrial production, manufacturing activity, and consumer spending patterns create sustained demand for logistics services across all market segments.

E-commerce expansion continues to drive market growth, with online retail sales growing at 12.4% annually, significantly outpacing traditional retail growth rates. This trend necessitates sophisticated fulfillment networks, last-mile delivery capabilities, and reverse logistics solutions to handle returns and exchanges.

Globalization and trade activities support market expansion through increased import and export volumes. International trade relationships, despite periodic disruptions, generate consistent demand for port services, intermodal transportation, and customs brokerage services that connect domestic markets with global supply chains.

Technological advancement acts as both a driver and enabler, with innovations in automation, artificial intelligence, and data analytics improving operational efficiency while creating new service opportunities. These technologies enable companies to offer enhanced visibility, predictive analytics, and optimized routing solutions that add value for customers.

Infrastructure development supports market growth through improved transportation networks, expanded port facilities, and enhanced intermodal connections. Government investment in infrastructure modernization creates opportunities for increased capacity and improved service reliability across all transportation modes.

Labor shortages represent a significant constraint, particularly in the trucking sector where driver availability has become a critical bottleneck. The American Trucking Associations estimates a shortage of qualified drivers that impacts service capacity and drives up operational costs across the industry.

Regulatory compliance requirements create operational complexity and cost burdens for transportation and logistics providers. Environmental regulations, safety standards, and hours-of-service rules, while necessary for public safety, require significant investment in compliance systems and monitoring technologies.

Infrastructure limitations in certain regions constrain market growth, with aging highways, congested urban areas, and capacity constraints at major ports creating bottlenecks that impact service reliability and increase costs. These limitations require coordinated public and private investment to address effectively.

Fuel price volatility creates ongoing operational challenges, with energy costs representing a significant portion of transportation expenses. Price fluctuations impact profitability and require sophisticated hedging strategies or fuel surcharge mechanisms to manage financial risk.

Cybersecurity threats pose increasing risks as the industry becomes more digitized and interconnected. Transportation and logistics companies must invest in robust cybersecurity measures to protect sensitive data and maintain operational continuity in the face of evolving cyber threats.

Technology adoption presents substantial opportunities for companies that successfully integrate advanced solutions into their operations. Artificial intelligence, machine learning, and predictive analytics offer potential for significant efficiency gains and service improvements that can differentiate market participants.

Sustainability initiatives create new market segments focused on environmentally responsible transportation and logistics solutions. Companies developing electric vehicle fleets, carbon-neutral shipping options, and sustainable packaging solutions are positioned to capture growing demand from environmentally conscious customers.

Last-mile delivery innovation offers opportunities for companies that can develop cost-effective solutions for urban delivery challenges. Autonomous vehicles, drone delivery systems, and micro-fulfillment centers represent emerging technologies that could transform final-mile logistics.

Supply chain visibility solutions present opportunities for technology providers and logistics companies that can offer real-time tracking, predictive analytics, and integrated supply chain management platforms. These solutions address growing customer demand for transparency and control over their supply chains.

Nearshoring trends create opportunities for domestic transportation and logistics providers as companies relocate production closer to end markets. This trend, driven by supply chain resilience considerations, increases demand for domestic transportation and warehousing services.

Competitive dynamics within the US Transportation and Logistics Market are characterized by intense competition across all segments, with companies competing on service quality, reliability, cost, and technological capabilities. Market leaders maintain competitive advantages through scale economies, extensive networks, and advanced technology platforms.

Customer relationships have evolved from transactional interactions to strategic partnerships, with logistics providers offering comprehensive supply chain solutions rather than individual transportation services. This shift requires companies to develop deeper industry expertise and integrated service capabilities.

Technology disruption continues to reshape competitive dynamics, with traditional transportation companies competing against technology-enabled startups and platform-based business models. This disruption creates both challenges and opportunities for established market participants.

Capacity management remains a critical dynamic, with companies balancing asset utilization, service reliability, and cost efficiency. Market participants must optimize capacity allocation across different service segments while maintaining flexibility to respond to demand fluctuations.

Pricing strategies reflect complex market dynamics including fuel costs, capacity constraints, service requirements, and competitive pressures. Companies are increasingly adopting dynamic pricing models that reflect real-time market conditions and service value propositions.

Comprehensive analysis of the US Transportation and Logistics Market employs multiple research methodologies to ensure accuracy, reliability, and depth of insights. The research approach combines quantitative data analysis with qualitative market intelligence to provide a complete market perspective.

Primary research involves extensive interviews with industry executives, logistics managers, transportation providers, and technology vendors to gather firsthand insights into market trends, challenges, and opportunities. These interviews provide valuable perspectives on operational realities and strategic priorities within the industry.

Secondary research encompasses analysis of industry reports, government statistics, trade association data, and company financial statements to establish market baselines and identify trends. This research provides quantitative foundations for market analysis and forecasting.

Market modeling techniques incorporate economic indicators, demographic trends, and industry-specific factors to develop comprehensive market forecasts and scenario analyses. These models help identify key drivers and potential market developments over the forecast period.

Data validation processes ensure research accuracy through cross-referencing multiple sources, expert review, and statistical analysis. This validation approach maintains research quality standards and provides confidence in market insights and projections.

Geographic distribution of the US Transportation and Logistics Market reflects regional economic activity, population centers, and transportation infrastructure development. Each region demonstrates distinct characteristics and growth patterns that influence market dynamics.

Northeast region maintains approximately 22% market share, driven by high population density, extensive manufacturing activity, and major port facilities. The region benefits from established transportation networks and proximity to international markets, supporting both domestic and international logistics activities.

Southeast region demonstrates the highest growth rates, capturing 28% market share through expanding manufacturing, growing population, and strategic port investments. The region’s business-friendly environment and lower operating costs attract logistics investment and facility development.

Midwest region serves as the transportation hub with 25% market share, leveraging central geographic location, extensive rail networks, and agricultural production. The region’s intermodal capabilities and manufacturing base support diverse transportation and logistics activities.

West region holds 25% market share, driven by Pacific trade, technology industry growth, and population expansion. The region faces unique challenges including traffic congestion and environmental regulations while benefiting from innovation and international trade opportunities.

Market leadership in the US Transportation and Logistics Market is distributed among several categories of companies, each serving different market segments and customer requirements. The competitive landscape includes asset-based carriers, logistics service providers, technology companies, and integrated supply chain solutions providers.

Competitive strategies focus on technology investment, network expansion, service diversification, and customer relationship development. Companies are increasingly emphasizing digital capabilities and data analytics to differentiate their service offerings and improve operational efficiency.

Market segmentation of the US Transportation and Logistics Market reveals distinct categories based on transportation mode, service type, end-user industry, and geographic scope. Each segment demonstrates unique characteristics, growth patterns, and competitive dynamics.

By Transportation Mode:

By Service Type:

Freight transportation represents the largest market category, encompassing all modes of goods movement and serving as the foundation for economic activity. This category demonstrates steady growth driven by industrial production, consumer spending, and international trade activities.

Trucking services dominate the freight transportation category, handling approximately 72% of total freight tonnage due to flexibility, accessibility, and door-to-door service capabilities. The segment faces challenges from driver shortages and regulatory requirements while benefiting from e-commerce growth and last-mile delivery demand.

Intermodal transportation gains market share as companies seek cost-effective solutions for long-distance freight movement. This category combines the efficiency of rail transportation with the flexibility of trucking to optimize cost and service performance for appropriate freight types.

Logistics services experience rapid growth as companies outsource non-core activities to specialized providers. This category includes warehousing, distribution, inventory management, and value-added services that support supply chain optimization and customer service improvement.

Technology-enabled services represent the fastest-growing category, with companies investing in digital platforms, automation, and data analytics to enhance service delivery and operational efficiency. These services create competitive differentiation and enable new business models within the traditional transportation and logistics framework.

Operational efficiency improvements represent primary benefits for industry participants, with advanced technologies and optimized processes reducing costs while improving service quality. Companies implementing comprehensive logistics solutions typically achieve 15-25% efficiency gains through better asset utilization and process optimization.

Market access expansion enables companies to reach new customers and geographic markets through comprehensive transportation networks and logistics capabilities. This expanded reach supports business growth and revenue diversification across different market segments and customer types.

Supply chain visibility provides stakeholders with real-time information about inventory levels, shipment status, and delivery schedules. This visibility enables better decision-making, improved customer service, and proactive issue resolution that enhances overall supply chain performance.

Risk mitigation benefits include diversified transportation options, backup capacity, and contingency planning that reduce supply chain disruption risks. Professional logistics providers offer expertise in risk management and business continuity planning that individual companies may lack internally.

Cost optimization through economies of scale, route optimization, and capacity utilization improvements provides significant financial benefits for stakeholders. Outsourcing transportation and logistics functions often reduces total supply chain costs while improving service levels and operational flexibility.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation continues to reshape the transportation and logistics landscape, with companies investing heavily in technology platforms that enable real-time visibility, predictive analytics, and automated decision-making. This trend is creating new competitive dynamics and service capabilities that differentiate market leaders.

Sustainability initiatives are becoming mainstream as companies respond to environmental regulations and customer demands for carbon-neutral logistics solutions. Electric vehicle adoption, alternative fuel usage, and carbon offset programs are increasingly common across the industry.

Autonomous vehicle development represents a transformative trend with potential to address driver shortages while improving safety and efficiency. While full deployment remains years away, pilot programs and limited deployments are beginning to demonstrate commercial viability for specific applications.

Last-mile delivery innovation focuses on urban delivery challenges through micro-fulfillment centers, drone delivery systems, and crowd-sourced delivery models. These innovations address growing customer expectations for faster, more convenient delivery options while managing cost pressures.

Supply chain resilience has become a strategic priority following recent disruptions, with companies diversifying suppliers, transportation modes, and geographic footprints to reduce risk. This trend creates opportunities for domestic transportation providers and regional logistics capabilities.

Technology partnerships between traditional logistics companies and technology providers are accelerating innovation and capability development. These partnerships combine logistics expertise with technological innovation to create advanced solutions for complex supply chain challenges.

Infrastructure investments by both government and private sector entities are expanding capacity and improving efficiency across transportation networks. Major port expansions, highway improvements, and rail infrastructure upgrades support market growth and service enhancement.

Merger and acquisition activity continues to reshape the competitive landscape as companies seek scale advantages, geographic expansion, and capability enhancement. Recent transactions demonstrate the ongoing consolidation trend across multiple market segments.

Regulatory developments including hours-of-service rules, environmental standards, and safety requirements continue to evolve, requiring industry adaptation and investment in compliance capabilities. These developments influence operational practices and competitive dynamics.

Workforce development initiatives address labor shortages through training programs, technology adoption, and improved working conditions. Industry associations and companies are collaborating on solutions to attract and retain qualified workers across all transportation modes.

Strategic recommendations for industry participants focus on technology investment, operational excellence, and customer relationship development. Companies should prioritize digital transformation initiatives that enhance operational efficiency while improving customer service capabilities.

MWR analysis suggests that successful companies will differentiate themselves through superior technology platforms, comprehensive service offerings, and strong customer partnerships. Investment in data analytics, automation, and visibility solutions will become essential for competitive positioning.

Market positioning strategies should emphasize specialized capabilities, geographic coverage, and industry expertise that create sustainable competitive advantages. Companies should focus on market segments where they can achieve leadership positions and premium pricing.

Partnership development with technology providers, customers, and other logistics companies can accelerate capability development and market expansion. Strategic alliances enable companies to access new technologies and markets while sharing investment risks and costs.

Sustainability planning should become integral to business strategy as environmental considerations increasingly influence customer decisions and regulatory requirements. Companies should develop comprehensive sustainability programs that address environmental impact while maintaining operational efficiency.

Market projections indicate continued growth for the US Transportation and Logistics Market, driven by economic expansion, technological advancement, and evolving customer requirements. The market is expected to maintain a compound annual growth rate of 6.2% through the forecast period, reflecting strong underlying demand fundamentals.

Technology evolution will continue to transform industry operations, with artificial intelligence, machine learning, and automation becoming standard capabilities rather than competitive differentiators. Companies that successfully integrate these technologies will achieve significant operational advantages and service improvements.

Sustainability requirements will intensify, with environmental considerations becoming central to customer selection criteria and regulatory compliance. Companies must develop comprehensive sustainability strategies that address carbon emissions, energy efficiency, and environmental impact across their operations.

Workforce transformation will address current labor challenges through technology adoption, process automation, and improved working conditions. The industry will likely see evolution toward higher-skilled positions focused on technology management and customer service rather than traditional manual labor.

Customer expectations will continue evolving toward greater transparency, faster delivery times, and more flexible service options. Companies must invest in capabilities that meet these expectations while maintaining cost competitiveness and operational efficiency.

The US Transportation and Logistics Market stands at a pivotal point in its evolution, characterized by technological transformation, changing customer expectations, and evolving competitive dynamics. The market demonstrates strong growth potential driven by economic expansion, e-commerce growth, and increasing demand for sophisticated supply chain solutions.

Success factors for market participants include technology investment, operational excellence, customer focus, and strategic positioning in high-growth segments. Companies that successfully navigate current challenges while positioning for future opportunities will capture significant market value and establish sustainable competitive advantages.

Market transformation will continue as digital technologies, sustainability requirements, and customer expectations reshape traditional business models. The industry’s ability to adapt to these changes while maintaining service reliability and cost competitiveness will determine long-term success and market leadership positions.

Future opportunities remain substantial for companies that embrace innovation, invest in technology, and develop comprehensive service capabilities that address evolving customer needs. The US Transportation and Logistics Market will continue serving as a critical enabler of economic growth and commercial activity throughout the forecast period and beyond.

What is Transportation and Logistics?

Transportation and Logistics refers to the processes involved in the movement and management of goods and services from one location to another. This includes various modes of transport, warehousing, inventory management, and supply chain coordination.

What are the key players in the US Transportation and Logistics Market?

Key players in the US Transportation and Logistics Market include companies like FedEx, UPS, and XPO Logistics, which provide a range of services from freight transportation to supply chain management, among others.

What are the main drivers of growth in the US Transportation and Logistics Market?

The main drivers of growth in the US Transportation and Logistics Market include the rise of e-commerce, increasing demand for efficient supply chain solutions, and advancements in technology such as automation and data analytics.

What challenges does the US Transportation and Logistics Market face?

Challenges in the US Transportation and Logistics Market include rising fuel costs, regulatory compliance issues, and the need for sustainable practices to reduce environmental impact.

What opportunities exist in the US Transportation and Logistics Market?

Opportunities in the US Transportation and Logistics Market include the expansion of last-mile delivery services, the integration of green logistics practices, and the adoption of innovative technologies like blockchain for supply chain transparency.

What trends are shaping the US Transportation and Logistics Market?

Trends shaping the US Transportation and Logistics Market include the increasing use of artificial intelligence for route optimization, the growth of omnichannel logistics strategies, and the emphasis on sustainability and carbon footprint reduction.

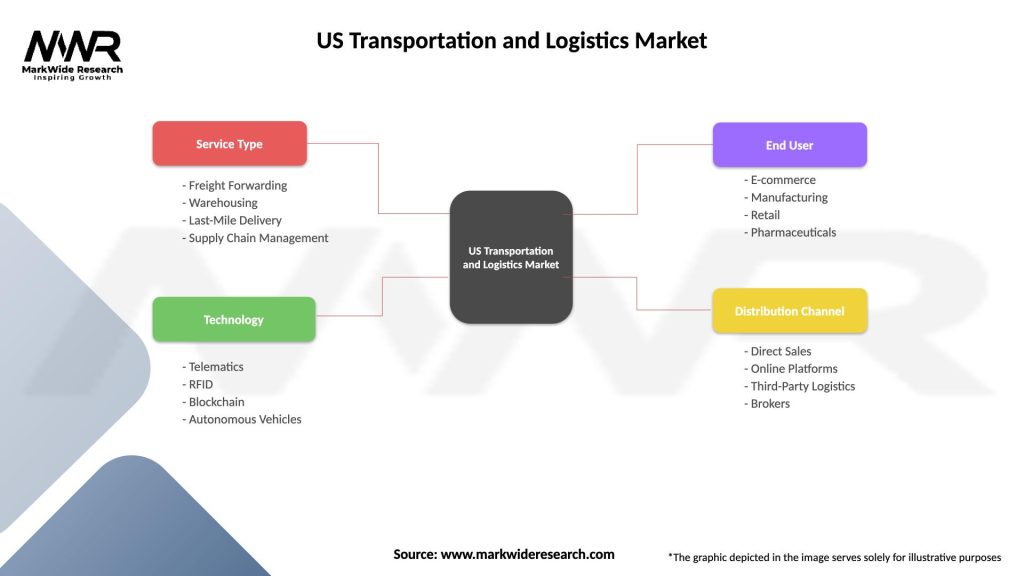

US Transportation and Logistics Market

| Segmentation Details | Description |

|---|---|

| Service Type | Freight Forwarding, Warehousing, Last-Mile Delivery, Supply Chain Management |

| Technology | Telematics, RFID, Blockchain, Autonomous Vehicles |

| End User | E-commerce, Manufacturing, Retail, Pharmaceuticals |

| Distribution Channel | Direct Sales, Online Platforms, Third-Party Logistics, Brokers |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the US Transportation and Logistics Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.