444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The US thermal power market represents a critical component of America’s energy infrastructure, encompassing coal-fired, natural gas, and oil-based power generation facilities. Thermal power generation continues to play a significant role in meeting the nation’s electricity demands despite the growing emphasis on renewable energy sources. The market has experienced substantial transformation over the past decade, with natural gas plants gaining prominence while coal-fired facilities face increasing pressure from environmental regulations and economic factors.

Market dynamics indicate a shift toward more efficient and cleaner thermal technologies, with combined cycle gas turbines achieving efficiency rates exceeding 60% in modern installations. The sector encompasses various stakeholders including utility companies, independent power producers, equipment manufacturers, and fuel suppliers. Regional variations in fuel availability, regulatory frameworks, and electricity demand patterns significantly influence market development across different states.

Technology advancement remains a key driver, with innovations in turbine design, emission control systems, and plant automation contributing to improved operational efficiency. The integration of digital technologies and predictive maintenance systems has enhanced plant reliability while reducing operational costs. According to MarkWide Research analysis, the thermal power sector is experiencing a gradual transition period characterized by modernization efforts and strategic capacity planning.

The US thermal power market refers to the comprehensive ecosystem of electricity generation facilities that convert thermal energy from fossil fuels into electrical power through steam turbines, gas turbines, or combined cycle systems. This market encompasses the entire value chain from fuel procurement and power plant operations to electricity transmission and distribution networks.

Thermal power generation involves the combustion of fossil fuels to produce high-temperature steam or hot gases that drive turbines connected to electrical generators. The process includes various technologies such as pulverized coal plants, natural gas combined cycle facilities, simple cycle gas turbines, and oil-fired power stations. Each technology offers distinct advantages in terms of efficiency, flexibility, and environmental impact.

Market participants include regulated utilities, merchant power generators, equipment manufacturers, fuel suppliers, and service providers. The sector operates within a complex regulatory environment governed by federal agencies, state public utility commissions, and regional transmission organizations that oversee grid reliability and market operations.

Strategic positioning within the US thermal power market reflects ongoing industry transformation driven by economic, environmental, and technological factors. The sector demonstrates resilience through adaptation to changing market conditions while maintaining critical grid reliability functions. Natural gas generation has emerged as the dominant thermal technology, accounting for approximately 40% of total electricity generation nationwide.

Investment patterns show continued focus on efficiency improvements and emission reduction technologies rather than new capacity additions. The market exhibits regional diversity with varying fuel preferences and regulatory approaches across different states. Operational flexibility has become increasingly valuable as thermal plants provide essential grid services including frequency regulation and backup power during renewable energy intermittency.

Future trajectory suggests continued evolution toward cleaner and more efficient thermal technologies while maintaining system reliability. The integration of carbon capture technologies and hydrogen co-firing represents emerging opportunities for long-term market sustainability. Market participants are adapting business models to accommodate changing electricity demand patterns and competitive pressures from renewable energy sources.

Fundamental market dynamics reveal several critical trends shaping the thermal power landscape:

Primary growth drivers supporting the thermal power market include reliable baseload generation requirements and grid stability needs. The sector benefits from established infrastructure and proven technology platforms that provide consistent electricity supply regardless of weather conditions. Natural gas abundance from domestic shale production has created favorable fuel economics for gas-fired generation.

Regulatory support for grid reliability ensures continued demand for dispatchable thermal generation capacity. The Federal Energy Regulatory Commission and regional grid operators recognize the importance of maintaining adequate thermal capacity for system security. Industrial electricity demand from manufacturing and data centers provides stable load growth in certain regions.

Technology advancement continues driving efficiency improvements and emission reductions in thermal power systems. Combined cycle technology offers superior fuel efficiency compared to older generation methods, making new installations economically attractive. The development of flexible operation capabilities allows thermal plants to complement renewable energy integration while maintaining grid stability.

Environmental regulations present significant challenges for thermal power operations, particularly coal-fired facilities facing stringent emission standards. The Clean Air Act and state-level environmental policies impose costly compliance requirements that affect plant economics. Carbon pricing mechanisms in certain regions create additional operational costs for fossil fuel generation.

Renewable energy competition has fundamentally altered electricity market dynamics, with solar and wind generation achieving cost parity in many regions. The intermittent nature of renewable sources paradoxically creates both challenges and opportunities for thermal generation. Public opposition to fossil fuel infrastructure development complicates permitting processes for new thermal facilities.

Economic pressures from low natural gas prices have made older, less efficient thermal plants economically unviable. The capital intensive nature of emission control upgrades often exceeds the remaining economic life of aging facilities. Stranded asset risks concern investors as energy transition policies accelerate retirement schedules for certain thermal technologies.

Emerging opportunities within the thermal power sector focus on technology innovation and market adaptation strategies. The development of carbon capture, utilization, and storage technologies offers potential pathways for continued operation of thermal facilities while reducing environmental impact. Hydrogen co-firing and eventual conversion to pure hydrogen combustion represent long-term transformation opportunities.

Grid modernization initiatives create demand for flexible and responsive thermal generation assets. The integration of energy storage systems with thermal plants enhances operational flexibility and market value. District heating applications and industrial steam supply provide additional revenue streams for thermal facilities in appropriate locations.

International market opportunities exist for US thermal power technology and expertise, particularly in developing countries requiring reliable electricity infrastructure. The retrofit and modernization market offers significant potential as existing facilities seek efficiency improvements and emission reductions. Digitalization initiatives enable new service business models and operational optimization opportunities.

Complex market forces shape the thermal power landscape through interconnected economic, regulatory, and technological factors. The electricity market structure varies significantly across regions, with some areas operating under traditional regulated utility models while others embrace competitive wholesale markets. Capacity markets in certain regions provide additional revenue streams for thermal generators by compensating reliability contributions.

Fuel price volatility significantly impacts thermal plant economics, with natural gas price fluctuations affecting operational decisions and long-term planning. The correlation between fuel costs and electricity prices creates both risks and opportunities for thermal generators. Transportation infrastructure for fuel delivery influences regional market dynamics and competitive positioning.

Technological convergence between thermal power and renewable energy systems creates new operational paradigms. The need for grid flexibility has elevated the importance of fast-starting thermal units capable of rapid load following. Market design evolution continues adapting to accommodate changing generation mix and operational requirements.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into the US thermal power sector. Primary research includes extensive interviews with industry executives, utility managers, equipment manufacturers, and regulatory officials to gather firsthand market intelligence. Secondary research encompasses analysis of government databases, industry reports, and financial filings from publicly traded companies.

Data collection methods incorporate quantitative analysis of electricity generation statistics, fuel consumption data, and capacity additions or retirements. Qualitative assessment examines regulatory trends, technology developments, and market participant strategies. Regional analysis considers variations in market structure, fuel availability, and regulatory frameworks across different states and electricity market regions.

Validation processes ensure data accuracy through cross-referencing multiple sources and expert review. Market modeling techniques project future trends based on historical patterns, announced projects, and policy developments. The research methodology maintains objectivity while providing actionable insights for market participants and stakeholders.

Regional market characteristics demonstrate significant variation across the United States, reflecting differences in fuel resources, regulatory environments, and electricity demand patterns. The Southeast region maintains substantial natural gas and coal generation capacity, with approximately 45% of electricity derived from thermal sources. Texas represents the largest thermal power market with extensive natural gas infrastructure and growing renewable integration.

Northeast markets exhibit higher electricity prices and greater environmental regulation, driving efficiency improvements and fuel switching initiatives. The region’s aging thermal fleet faces retirement pressures while maintaining critical grid reliability functions. California demonstrates aggressive renewable energy policies that limit new thermal development while requiring existing plants for grid stability.

Midwest regions historically dependent on coal generation are experiencing rapid transformation toward natural gas and renewable sources. The PJM Interconnection operates the largest competitive electricity market, where thermal generators compete based on operational efficiency and fuel costs. Regional transmission organizations play crucial roles in market operations and capacity planning across interconnected grid systems.

Market leadership within the US thermal power sector encompasses diverse participant categories including integrated utilities, independent power producers, and equipment manufacturers. Major players demonstrate varying strategies for adapting to changing market conditions:

Competitive strategies emphasize operational excellence, environmental compliance, and technology innovation. Market consolidation continues as companies seek economies of scale and operational synergies. Strategic partnerships between utilities and technology providers accelerate innovation adoption and market development.

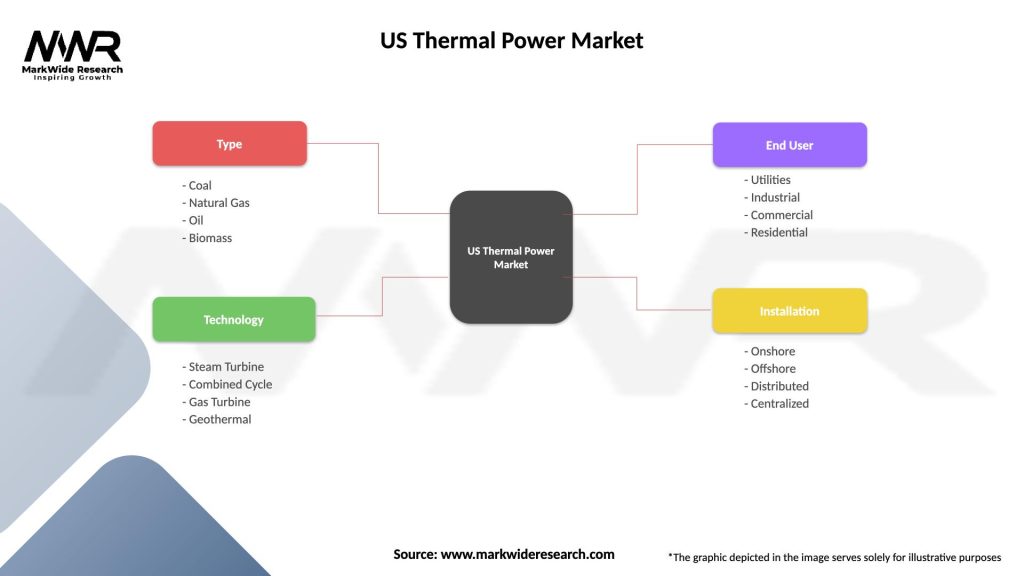

Market segmentation within the US thermal power sector reflects diverse technology platforms, fuel types, and operational characteristics:

By Technology:

By Fuel Type:

By Application:

Natural gas generation dominates thermal power growth with combined cycle technology achieving superior efficiency and environmental performance. These facilities demonstrate operational flexibility essential for grid stability while maintaining competitive economics. Load following capabilities enable natural gas plants to complement renewable energy integration effectively.

Coal-fired generation faces continued challenges from environmental regulations and economic competition, resulting in accelerated retirement schedules. However, remaining coal facilities provide essential grid services and maintain importance in certain regional markets. Emission control investments extend operational life for economically viable plants while ensuring environmental compliance.

Peaking power facilities serve critical grid reliability functions during high demand periods and emergency conditions. These units demonstrate rapid start capabilities and operational flexibility that complement renewable energy variability. Capacity market revenues provide economic support for maintaining peaking resources despite limited operational hours.

Cogeneration systems offer enhanced efficiency through combined electricity and thermal energy production for industrial applications. These facilities achieve overall efficiency rates exceeding 80% by utilizing waste heat for process steam or district heating. Industrial partnerships create stable revenue streams and improve project economics for cogeneration developments.

Utility companies benefit from thermal power assets through reliable generation capacity and operational flexibility essential for grid management. Dispatchable generation provides utilities with tools to maintain system reliability while integrating variable renewable energy sources. Fuel diversity reduces supply risk and provides operational options during market volatility.

Independent power producers leverage thermal generation assets to participate in competitive electricity markets and capacity auctions. Merchant power facilities offer revenue opportunities through energy sales, ancillary services, and capacity payments. Operational expertise in thermal technologies provides competitive advantages in market operations and asset optimization.

Equipment manufacturers benefit from ongoing demand for efficiency improvements, emission control systems, and modernization projects. Service contracts provide recurring revenue streams through maintenance, parts supply, and performance optimization services. Technology innovation creates market differentiation and premium pricing opportunities for advanced thermal power solutions.

Regional economies benefit from thermal power facilities through employment opportunities, tax revenues, and local economic activity. Construction projects and ongoing operations support skilled workforce development and supply chain businesses. Fuel supply industries maintain market demand and economic activity through thermal power consumption.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digitalization transformation represents a fundamental trend reshaping thermal power operations through advanced analytics, artificial intelligence, and Internet of Things technologies. Predictive maintenance systems reduce unplanned outages while optimizing maintenance costs and equipment reliability. Real-time monitoring and control systems enhance operational efficiency and environmental performance.

Fuel switching initiatives continue driving market evolution as utilities transition from coal to natural gas generation. This trend reflects both economic advantages and environmental benefits of cleaner-burning fuels. Dual-fuel capabilities provide operational flexibility and fuel supply security for thermal facilities.

Grid integration complexity increases as thermal plants adapt to support renewable energy integration and maintain system stability. Flexible operation modes enable thermal facilities to provide rapid response capabilities and load following services. According to MWR analysis, thermal plants are increasingly valued for grid services beyond energy production.

Environmental technology adoption accelerates as thermal facilities invest in emission control systems and efficiency improvements. Carbon capture pilot projects demonstrate potential pathways for continued thermal generation with reduced environmental impact. Waste heat recovery systems improve overall facility efficiency and economic performance.

Recent industry developments highlight ongoing transformation within the thermal power sector. Major utility companies have announced accelerated coal plant retirement schedules while investing in natural gas and renewable capacity. Technology partnerships between utilities and equipment manufacturers focus on efficiency improvements and emission reductions.

Regulatory developments include updated environmental standards and grid reliability requirements affecting thermal plant operations. State energy policies increasingly emphasize clean energy transitions while maintaining grid reliability through thermal backup capacity. Federal infrastructure investments support grid modernization and clean energy technology development.

Market structure evolution continues with capacity market reforms and ancillary service market enhancements recognizing the value of flexible thermal resources. Regional transmission organizations implement new market mechanisms to ensure adequate generation capacity and grid reliability services.

Technology breakthroughs in turbine efficiency, emission control, and plant automation drive operational improvements across the thermal fleet. Demonstration projects for carbon capture and hydrogen co-firing advance toward commercial deployment. Digital twin technology enables advanced plant optimization and predictive maintenance capabilities.

Strategic recommendations for thermal power market participants emphasize adaptation to changing market conditions while maintaining operational excellence. Investment priorities should focus on efficiency improvements, environmental compliance, and operational flexibility enhancements. Portfolio optimization requires careful evaluation of asset economics and retirement timing decisions.

Technology adoption strategies should prioritize digitalization initiatives and advanced control systems that improve operational performance and reduce costs. Fuel supply diversification provides risk mitigation and operational flexibility benefits. Market participation in capacity and ancillary service markets maximizes revenue opportunities for thermal assets.

Regulatory engagement remains critical for influencing policy development and ensuring fair market treatment of thermal resources. Stakeholder communication should emphasize the reliability and grid stability benefits provided by thermal generation. Environmental stewardship initiatives demonstrate commitment to responsible operations and community engagement.

Long-term planning must consider energy transition scenarios while maintaining near-term operational viability. Partnership opportunities with renewable energy developers and technology providers create synergistic value propositions. Workforce development ensures availability of skilled personnel for evolving thermal power operations.

Long-term market prospects for US thermal power reflect continued evolution toward cleaner and more efficient technologies while maintaining essential grid reliability functions. Natural gas generation is projected to maintain dominant position among thermal technologies with continued capacity additions in strategic locations. Combined cycle efficiency improvements are expected to reach 65% thermal efficiency in next-generation facilities.

Carbon management technologies will likely determine the long-term viability of thermal power generation as environmental policies become more stringent. Hydrogen integration represents a potential transformation pathway for existing thermal infrastructure. Energy storage integration with thermal plants may create new operational models and market opportunities.

Market structure evolution will continue adapting to accommodate higher renewable energy penetration while ensuring grid reliability through thermal backup capacity. Regional variations in market development will persist based on fuel availability, regulatory frameworks, and electricity demand patterns. MarkWide Research projects that thermal power will maintain approximately 35-40% market share in the US electricity generation mix through 2030.

Investment patterns are expected to focus on modernization and efficiency improvements rather than new capacity additions in most regions. Retirement schedules for aging thermal facilities will accelerate while remaining plants receive strategic upgrades to extend operational life and improve performance.

The US thermal power market continues demonstrating resilience and adaptability amid significant industry transformation driven by environmental, economic, and technological factors. Natural gas generation has emerged as the dominant thermal technology, providing essential grid reliability services while achieving superior environmental performance compared to traditional coal-fired facilities. Market participants are successfully adapting business models and operational strategies to maintain competitiveness in evolving electricity markets.

Future success in the thermal power sector will depend on continued innovation in efficiency improvements, emission reductions, and operational flexibility enhancements. Technology integration and digitalization initiatives offer significant opportunities for performance optimization and cost reduction. Strategic positioning as reliable grid resources supporting renewable energy integration creates long-term value propositions for thermal power assets.

Market outlook suggests continued importance of thermal generation for grid stability and reliability while evolving toward cleaner and more efficient technologies. Industry stakeholders who embrace innovation, maintain operational excellence, and adapt to changing market conditions will be best positioned for sustained success in the dynamic US thermal power market.

What is Thermal Power?

Thermal power refers to the generation of electricity through the conversion of heat energy, typically from fossil fuels or nuclear sources. It plays a crucial role in the energy mix, providing a significant portion of electricity in various regions.

What are the key players in the US Thermal Power Market?

Key players in the US Thermal Power Market include Duke Energy, NextEra Energy, and Southern Company, among others. These companies are involved in the generation and distribution of thermal power, contributing to the overall energy supply.

What are the main drivers of the US Thermal Power Market?

The main drivers of the US Thermal Power Market include the increasing demand for electricity, the need for reliable energy sources, and advancements in thermal power technologies. Additionally, regulatory frameworks supporting energy security contribute to market growth.

What challenges does the US Thermal Power Market face?

The US Thermal Power Market faces challenges such as environmental regulations, competition from renewable energy sources, and the aging infrastructure of power plants. These factors can impact operational efficiency and investment in new technologies.

What opportunities exist in the US Thermal Power Market?

Opportunities in the US Thermal Power Market include the modernization of existing plants, integration of cleaner technologies, and potential investments in carbon capture and storage solutions. These developments can enhance sustainability and operational efficiency.

What trends are shaping the US Thermal Power Market?

Trends shaping the US Thermal Power Market include the shift towards cleaner energy production, increased investment in hybrid systems, and the adoption of digital technologies for operational optimization. These trends aim to improve efficiency and reduce environmental impact.

US Thermal Power Market

| Segmentation Details | Description |

|---|---|

| Type | Coal, Natural Gas, Oil, Biomass |

| Technology | Steam Turbine, Combined Cycle, Gas Turbine, Geothermal |

| End User | Utilities, Industrial, Commercial, Residential |

| Installation | Onshore, Offshore, Distributed, Centralized |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the US Thermal Power Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.