444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The US oil and gas upstream market represents a cornerstone of American energy independence and economic prosperity, encompassing exploration, drilling, and production activities across diverse geological formations. Upstream operations in the United States have undergone revolutionary transformation through technological innovations, particularly in hydraulic fracturing and horizontal drilling techniques. The market demonstrates remarkable resilience and adaptability, with operators continuously optimizing extraction methods to maximize resource recovery from both conventional and unconventional reserves.

Shale formations across key basins including the Permian, Bakken, and Eagle Ford have positioned the United States as a global energy powerhouse, achieving unprecedented production levels that have fundamentally altered international energy dynamics. The market exhibits strong growth momentum, with production efficiency improvements reaching 35% annually in major shale plays. Technological advancement remains the primary catalyst driving operational excellence, enabling operators to extract resources from previously uneconomical formations while reducing environmental impact through enhanced precision drilling techniques.

Market participants range from integrated oil majors to independent exploration and production companies, each contributing unique capabilities to the upstream value chain. The sector benefits from robust infrastructure development, supportive regulatory frameworks, and continuous innovation in drilling technologies that have revolutionized resource extraction methodologies across diverse geological environments.

The US oil and gas upstream market refers to the comprehensive sector encompassing all activities related to the exploration, development, and production of crude oil and natural gas resources within United States territories. Upstream operations include geological surveys, seismic analysis, exploratory drilling, well completion, and ongoing production management across conventional and unconventional resource formations.

This market segment represents the initial phase of the petroleum value chain, focusing on locating hydrocarbon deposits, assessing their commercial viability, and implementing extraction technologies to bring these resources to surface facilities. Upstream activities encompass both onshore and offshore operations, utilizing advanced drilling techniques, completion technologies, and production optimization systems to maximize resource recovery while maintaining operational safety and environmental compliance.

The scope extends beyond traditional drilling operations to include sophisticated reservoir management, enhanced oil recovery techniques, and digital technologies that optimize production performance throughout the lifecycle of oil and gas assets.

The US oil and gas upstream market continues demonstrating exceptional growth trajectory driven by technological innovation, operational efficiency improvements, and favorable geological conditions across major producing regions. Unconventional resource development has emerged as the dominant growth driver, with shale oil production accounting for approximately 78% of total US crude oil output. The market benefits from continuous technological advancement in drilling and completion techniques, enabling operators to achieve superior well performance while reducing development costs.

Key market dynamics include the ongoing digital transformation of upstream operations, implementation of artificial intelligence and machine learning technologies for reservoir optimization, and increasing focus on environmental sustainability through reduced emissions and water usage. Production efficiency has improved dramatically, with average well productivity increasing by 42% over the past five years through enhanced completion designs and drilling optimization.

Market consolidation trends continue shaping the competitive landscape, with larger operators acquiring strategic assets to optimize drilling programs and achieve economies of scale. The sector demonstrates remarkable adaptability to commodity price volatility, implementing flexible drilling programs and cost management strategies that maintain profitability across various price environments.

Strategic insights reveal fundamental shifts in upstream market dynamics, with operators increasingly prioritizing capital discipline and shareholder returns over pure production growth. Technology integration has become essential for competitive advantage, with leading companies investing heavily in digital solutions that optimize drilling performance and reduce operational costs.

Technological advancement serves as the primary catalyst propelling upstream market growth, with continuous innovation in drilling and completion techniques enabling access to previously uneconomical resources. Horizontal drilling combined with multi-stage hydraulic fracturing has revolutionized shale development, allowing operators to extract hydrocarbons from tight formations with unprecedented efficiency.

Energy security considerations drive sustained investment in domestic upstream development, reducing dependence on foreign oil imports and strengthening national energy independence. Digital technologies including artificial intelligence, machine learning, and advanced data analytics optimize drilling programs, enhance reservoir management, and improve operational decision-making processes.

Infrastructure expansion continues supporting market growth through pipeline development, processing facility construction, and transportation network enhancement. Regulatory stability provides operators with confidence to make long-term capital investments, while favorable tax policies and lease terms encourage continued exploration and development activities. Market demand for domestic energy production remains robust, supported by industrial growth, petrochemical expansion, and export opportunities that create sustainable revenue streams for upstream operators.

Environmental regulations present ongoing challenges for upstream operators, requiring substantial investments in compliance systems, emissions control technologies, and environmental monitoring programs. Commodity price volatility creates uncertainty in capital allocation decisions, with operators needing to maintain flexible drilling programs that can adapt to changing market conditions.

Infrastructure constraints in certain regions limit production growth potential, particularly in areas where pipeline capacity lags behind drilling activity. Water availability and disposal challenges affect operations in water-scarce regions, requiring innovative solutions for water sourcing, recycling, and waste management.

Labor shortages in specialized technical roles impact operational efficiency and project timelines, particularly during periods of rapid industry expansion. Capital intensity of upstream operations requires significant financial resources, limiting participation for smaller operators and creating barriers to entry. Community relations and social acceptance challenges in certain regions can delay project development and increase operational costs through additional stakeholder engagement requirements.

Enhanced oil recovery techniques present substantial opportunities for increasing production from existing wells and mature fields through advanced completion technologies and chemical injection programs. Digital transformation initiatives offer significant potential for operational optimization, cost reduction, and productivity enhancement through artificial intelligence and predictive analytics implementation.

Carbon capture and storage technologies create new revenue streams while addressing environmental concerns, positioning operators as leaders in sustainable energy development. Unconventional resource expansion into underdeveloped basins and formations provides growth opportunities for companies with advanced drilling capabilities and geological expertise.

Export market development offers substantial revenue potential as global demand for US energy resources continues expanding. Technology licensing and service provision to international markets create additional income streams for companies with proprietary drilling and completion technologies. Strategic partnerships with technology companies, research institutions, and international operators facilitate knowledge sharing and market expansion opportunities.

Market dynamics in the US upstream sector reflect complex interactions between technological innovation, regulatory frameworks, commodity prices, and global energy demand patterns. Supply chain optimization has become increasingly important, with operators implementing just-in-time delivery systems and strategic supplier partnerships to reduce costs and improve operational efficiency.

Consolidation trends continue reshaping the competitive landscape, with larger operators acquiring strategic assets to achieve economies of scale and optimize drilling programs. Financial discipline has emerged as a key differentiator, with successful companies balancing growth investments with shareholder returns and debt management.

Environmental, social, and governance considerations increasingly influence investment decisions and operational practices, driving adoption of cleaner technologies and sustainable development approaches. Digitalization efforts are transforming traditional upstream operations through real-time monitoring, predictive maintenance, and automated drilling systems that improve safety and efficiency. Market volatility requires operators to maintain flexible business models capable of adapting to changing commodity prices and economic conditions while preserving long-term growth potential.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into US upstream market dynamics. Primary research includes extensive interviews with industry executives, technical specialists, and regulatory officials to gather firsthand perspectives on market trends, challenges, and opportunities.

Secondary research encompasses analysis of industry reports, regulatory filings, production data, and financial statements from publicly traded companies to establish quantitative market foundations. Data validation processes involve cross-referencing multiple sources and conducting expert reviews to ensure information accuracy and reliability.

Market modeling utilizes advanced statistical techniques and econometric analysis to project future trends and identify key growth drivers. Regional analysis examines production patterns, drilling activity, and infrastructure development across major US oil and gas basins to provide comprehensive geographic insights. Technology assessment evaluates emerging innovations and their potential impact on upstream operations through expert consultation and technical literature review.

The Permian Basin dominates US upstream activity, accounting for approximately 48% of total crude oil production and representing the most active drilling region in North America. West Texas and New Mexico portions of the Permian continue attracting substantial investment due to superior well economics, extensive infrastructure, and multiple productive formations including the Wolfcamp and Bone Spring.

The Bakken formation in North Dakota remains a significant contributor to US oil production, with operators implementing advanced completion techniques to maintain productivity despite mature development. Eagle Ford Shale in South Texas provides substantial oil and natural gas production, benefiting from proximity to Gulf Coast refining and export infrastructure.

Appalachian Basin leads natural gas production through extensive Marcellus and Utica shale development, with Pennsylvania, West Virginia, and Ohio serving as primary production centers. Gulf of Mexico offshore operations contribute significant production volumes through deepwater developments, with operators implementing advanced subsea technologies to access remote reserves. Regional infrastructure development varies significantly, with established basins benefiting from extensive pipeline networks while emerging areas require substantial transportation investments to support production growth.

The competitive landscape encompasses diverse participants ranging from integrated oil majors to independent exploration and production companies, each contributing unique capabilities and strategic approaches to upstream development. Market leadership is determined by production volumes, operational efficiency, technological innovation, and financial performance across various commodity price environments.

Competitive differentiation increasingly depends on technological innovation, operational efficiency, and environmental performance rather than pure asset scale. Strategic partnerships and joint ventures enable companies to share risks, combine expertise, and access capital for large-scale development projects.

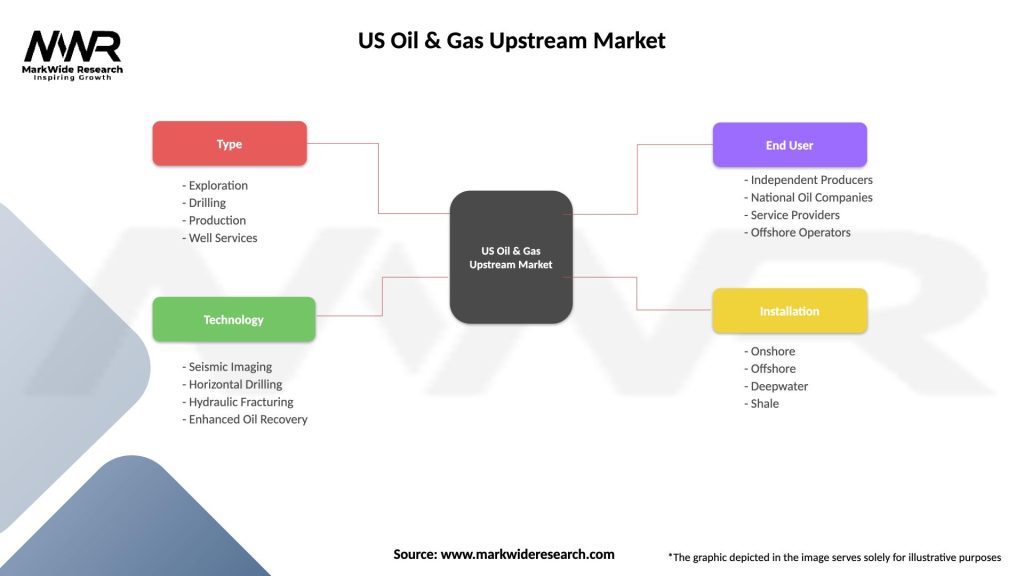

Market segmentation reflects diverse operational approaches, resource types, and geographic concentrations that characterize the US upstream sector. By Resource Type, the market divides into crude oil, natural gas, and natural gas liquids production, each requiring specialized extraction and processing techniques.

By Technology:

By Operation Type:

By Basin: Geographic segmentation includes major producing regions such as Permian, Bakken, Eagle Ford, Marcellus, and Gulf of Mexico, each with distinct geological characteristics and operational requirements.

Crude oil production dominates upstream revenue generation, with light tight oil from shale formations representing the fastest-growing segment. Unconventional oil development has transformed the market landscape, enabling the United States to achieve net oil exporter status and reducing dependence on foreign imports.

Natural gas production benefits from robust domestic demand and expanding export opportunities through liquefied natural gas facilities. Associated gas from oil wells provides additional revenue streams for operators while supporting broader energy infrastructure development.

Natural gas liquids extraction creates valuable byproducts including ethane, propane, and butane that serve petrochemical and heating markets. Offshore operations contribute significant production volumes through technologically advanced deepwater projects that access large hydrocarbon accumulations.

Enhanced oil recovery techniques extend field life and increase ultimate recovery factors from existing wells through water flooding, gas injection, and chemical stimulation methods. Digital technologies optimize production across all categories through real-time monitoring, predictive analytics, and automated control systems.

Operators benefit from technological advancement that reduces drilling costs, improves well productivity, and extends field life through enhanced recovery techniques. Cost optimization through digital technologies and operational efficiency improvements enables profitability across various commodity price environments.

Investors gain from improved capital discipline, enhanced shareholder returns, and reduced operational risks through advanced drilling technologies and reservoir management systems. Service companies benefit from steady demand for specialized equipment, technical services, and innovative solutions that support upstream operations.

Local communities receive economic benefits through job creation, tax revenue generation, and infrastructure development that supports regional economic growth. National energy security improves through reduced import dependence and increased domestic production capacity.

Environmental stakeholders benefit from cleaner extraction technologies, reduced emissions, and improved water management practices that minimize operational environmental impact. Technology providers gain from continuous innovation demand and opportunities to develop next-generation drilling and completion solutions.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation represents the most significant trend reshaping upstream operations, with operators implementing artificial intelligence, machine learning, and advanced analytics to optimize drilling programs and enhance production performance. Automation technologies are reducing operational costs while improving safety through remote monitoring and automated drilling systems.

Environmental sustainability initiatives are driving adoption of cleaner technologies, emissions reduction programs, and water recycling systems that minimize operational environmental impact. Carbon management strategies including carbon capture, utilization, and storage are creating new revenue opportunities while addressing climate change concerns.

Consolidation activities continue reshaping the competitive landscape as operators seek economies of scale and operational synergies through strategic acquisitions. Capital discipline has become a defining characteristic, with companies prioritizing shareholder returns and cash flow generation over pure production growth. Supply chain optimization through strategic partnerships and inventory management systems is reducing costs and improving operational efficiency across the upstream value chain.

Recent industry developments highlight the sector’s continued evolution toward greater efficiency, sustainability, and technological sophistication. Major operators have announced significant investments in carbon capture and storage projects, positioning themselves as leaders in sustainable energy development while creating new revenue streams.

Technology partnerships between oil companies and tech firms are accelerating digital transformation initiatives, with artificial intelligence applications showing promising results in drilling optimization and predictive maintenance. Infrastructure investments continue expanding pipeline capacity and processing facilities to support growing production from key basins.

Regulatory developments include updated environmental standards and permitting processes that balance energy development needs with environmental protection requirements. Market consolidation activities have created larger, more efficient operating platforms capable of implementing advanced technologies and achieving superior operational performance. International partnerships are expanding market access and technology sharing opportunities that benefit US upstream operators in global markets.

Industry analysts recommend that upstream operators prioritize technology investments that deliver measurable productivity improvements and cost reductions. MarkWide Research analysis indicates that companies implementing comprehensive digital transformation strategies achieve 25% higher operational efficiency compared to traditional operators.

Strategic recommendations include developing flexible drilling programs that can adapt to commodity price volatility while maintaining long-term growth potential. Environmental compliance investments should be viewed as competitive advantages rather than regulatory burdens, positioning companies for sustainable long-term success.

Capital allocation strategies should balance growth investments with shareholder returns, maintaining financial discipline while pursuing strategic opportunities. Partnership development with technology providers, service companies, and research institutions can accelerate innovation adoption and reduce development risks. Market diversification through geographic expansion and resource type variety provides stability during volatile market conditions.

The future outlook for the US oil and gas upstream market remains positive, driven by continued technological innovation, abundant resource base, and growing global energy demand. Production growth is expected to continue at a sustainable pace, with operators focusing on capital efficiency and environmental responsibility rather than pure volume expansion.

Technology advancement will remain the primary catalyst for industry evolution, with artificial intelligence, automation, and enhanced recovery techniques driving productivity improvements. MWR projections suggest that digital technology adoption could improve operational efficiency by 30% over the next decade.

Environmental considerations will increasingly influence operational practices and investment decisions, with successful companies integrating sustainability initiatives into core business strategies. Market consolidation trends are expected to continue, creating larger, more efficient operators capable of implementing advanced technologies and achieving superior returns.

Export opportunities will provide substantial growth potential as global demand for US energy resources continues expanding. Infrastructure development will support production growth while enabling access to international markets through expanded pipeline and export facility capacity.

The US oil and gas upstream market stands at the forefront of global energy transformation, demonstrating remarkable resilience, innovation, and adaptability in an evolving energy landscape. Technological advancement continues driving operational excellence, enabling operators to extract resources more efficiently while reducing environmental impact through precision drilling and advanced completion techniques.

Market fundamentals remain strong, supported by abundant unconventional resources, robust infrastructure, and favorable regulatory frameworks that encourage continued investment and development. Digital transformation initiatives are revolutionizing traditional upstream operations, creating opportunities for significant productivity improvements and cost reductions that enhance long-term competitiveness.

The sector’s evolution toward greater sustainability, operational efficiency, and technological sophistication positions it for continued success in meeting growing global energy demand while addressing environmental challenges. Strategic focus on capital discipline, shareholder returns, and sustainable development practices ensures the US upstream market remains a vital component of national energy security and economic prosperity for decades to come.

What is Oil & Gas Upstream?

Oil & Gas Upstream refers to the exploration and production segment of the oil and gas industry, focusing on locating and extracting crude oil and natural gas from the earth. This includes activities such as drilling, well completion, and reservoir management.

What are the key players in the US Oil & Gas Upstream Market?

Key players in the US Oil & Gas Upstream Market include companies like ExxonMobil, Chevron, and ConocoPhillips, which are involved in exploration and production activities. These companies operate in various regions and utilize advanced technologies to enhance extraction efficiency, among others.

What are the main drivers of the US Oil & Gas Upstream Market?

The main drivers of the US Oil & Gas Upstream Market include the increasing global energy demand, advancements in drilling technologies, and the discovery of new oil and gas reserves. Additionally, geopolitical factors and regulatory changes can significantly impact market dynamics.

What challenges does the US Oil & Gas Upstream Market face?

The US Oil & Gas Upstream Market faces challenges such as fluctuating oil prices, environmental regulations, and the need for sustainable practices. These factors can affect profitability and operational efficiency for companies in the sector.

What opportunities exist in the US Oil & Gas Upstream Market?

Opportunities in the US Oil & Gas Upstream Market include the potential for technological innovations in extraction methods, the expansion of shale oil production, and increased investment in renewable energy integration. These factors can lead to enhanced operational efficiencies and new market entrants.

What trends are shaping the US Oil & Gas Upstream Market?

Trends shaping the US Oil & Gas Upstream Market include the adoption of digital technologies, such as data analytics and automation, to optimize production processes. Additionally, there is a growing focus on environmental sustainability and reducing carbon footprints within the industry.

US Oil & Gas Upstream Market

| Segmentation Details | Description |

|---|---|

| Type | Exploration, Drilling, Production, Well Services |

| Technology | Seismic Imaging, Horizontal Drilling, Hydraulic Fracturing, Enhanced Oil Recovery |

| End User | Independent Producers, National Oil Companies, Service Providers, Offshore Operators |

| Installation | Onshore, Offshore, Deepwater, Shale |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the US Oil & Gas Upstream Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.