The US hardware encryption market is a crucial segment within the broader cybersecurity industry, focusing on the development and deployment of encryption solutions for data protection. Hardware encryption involves the use of dedicated cryptographic hardware devices to secure sensitive data, offering enhanced security and performance compared to software-based encryption methods. With increasing cyber threats and data breaches, the demand for robust encryption solutions has grown, driving the expansion of the hardware encryption market in the US.

Meaning

Hardware encryption refers to the process of encrypting data using dedicated cryptographic hardware devices, such as encryption chips, modules, or drives, to safeguard information from unauthorized access or interception. Unlike software-based encryption, which relies on computer resources for encryption and decryption processes, hardware encryption offloads cryptographic operations to specialized hardware components, providing stronger protection against cyber threats and ensuring faster data processing speeds.

Executive Summary

The US hardware encryption market has experienced significant growth in recent years, fueled by escalating cybersecurity concerns, stringent regulatory requirements, and increasing adoption of data encryption solutions across various industries. As organizations strive to protect their sensitive data from cyberattacks and data breaches, hardware encryption solutions have emerged as a preferred choice for achieving robust security, compliance, and performance requirements.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Rising Cyber Threat Landscape: The proliferation of cyber threats, including malware, ransomware, and phishing attacks, has heightened the need for effective data protection measures, driving the demand for hardware encryption solutions in the US.

Stringent Data Protection Regulations: Regulatory mandates, such as the GDPR and CCPA, require organizations to implement strong encryption measures to safeguard sensitive data and ensure compliance with data privacy laws, driving the adoption of hardware encryption solutions.

Increased Awareness of Data Security: Growing awareness among businesses and consumers about the importance of data security and privacy has led to greater investment in encryption technologies, spurring market growth for hardware encryption solutions.

Advancements in Encryption Technologies: Continuous advancements in encryption algorithms, key management techniques, and hardware security modules (HSMs) have enhanced the effectiveness and reliability of hardware encryption solutions, driving their adoption in diverse applications.

Market Drivers

Data Breach Prevention: Hardware encryption helps prevent data breaches by encrypting data at rest and in transit, reducing the risk of unauthorized access and data theft.

Regulatory Compliance Requirements: Compliance mandates require organizations to implement encryption measures to protect sensitive data, driving the adoption of hardware encryption solutions to achieve regulatory compliance.

Performance and Efficiency: Hardware encryption accelerates cryptographic operations, offering superior performance and efficiency compared to software-based encryption, particularly in high-throughput applications and resource-constrained environments.

Data Security in Cloud Environments: With the increasing migration of data to cloud platforms, hardware encryption solutions play a vital role in securing data stored and transmitted across cloud environments, ensuring confidentiality and integrity.

Market Restraints

Cost Considerations: The initial investment and ongoing maintenance costs associated with hardware encryption solutions may pose challenges for budget-constrained organizations, limiting market adoption.

Integration Complexity: Integrating hardware encryption devices into existing IT infrastructure and applications may require specialized expertise and resources, hindering seamless deployment and implementation.

Key Management Challenges: Effective key management is essential for ensuring the security of encrypted data; however, managing encryption keys across multiple hardware devices and platforms can be complex and resource-intensive.

Vendor Lock-in: Organizations may face vendor lock-in issues when deploying proprietary hardware encryption solutions, limiting flexibility and interoperability with other security technologies and platforms.

Market Opportunities

Emergence of Quantum Encryption: The advent of quantum encryption technologies presents opportunities for the development of quantum-resistant hardware encryption solutions capable of protecting data against future quantum computing threats.

Growing Adoption of IoT Devices: The proliferation of Internet of Things (IoT) devices and sensors generates vast amounts of data that require secure encryption, creating opportunities for hardware encryption solutions in IoT deployments across various industries.

Expansion of Blockchain Technology: Blockchain-based applications and platforms rely on encryption for securing transactions and data integrity, driving demand for hardware encryption solutions to strengthen blockchain security.

Increased Focus on Endpoint Security: With the rise of remote work and mobile devices, there is a growing need for hardware-based endpoint encryption solutions to protect sensitive data on laptops, tablets, and smartphones from unauthorized access and theft.

Market Dynamics

The US hardware encryption market operates in a dynamic environment shaped by technological advancements, regulatory developments, evolving threat landscapes, and changing customer preferences. Market dynamics such as mergers and acquisitions, partnerships and collaborations, product innovations, and competitive strategies influence the growth and competitiveness of hardware encryption vendors in the US market.

Regional Analysis

The US hardware encryption market is characterized by strong demand from various industries, including finance, healthcare, government, defense, and IT, driving market growth across different regions and states. Key technology hubs such as Silicon Valley, Boston, and Seattle serve as centers of innovation and investment in hardware encryption technologies, fostering industry collaboration and talent development.

Competitive Landscape

Leading Companies in the US Hardware Encryption Market:

Kingston Technology Corporation

Seagate Technology PLC

Western Digital Corporation

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

Toshiba Corporation

NetApp, Inc.

Thales Group

Kanguru Solutions

Apricorn, LLC

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

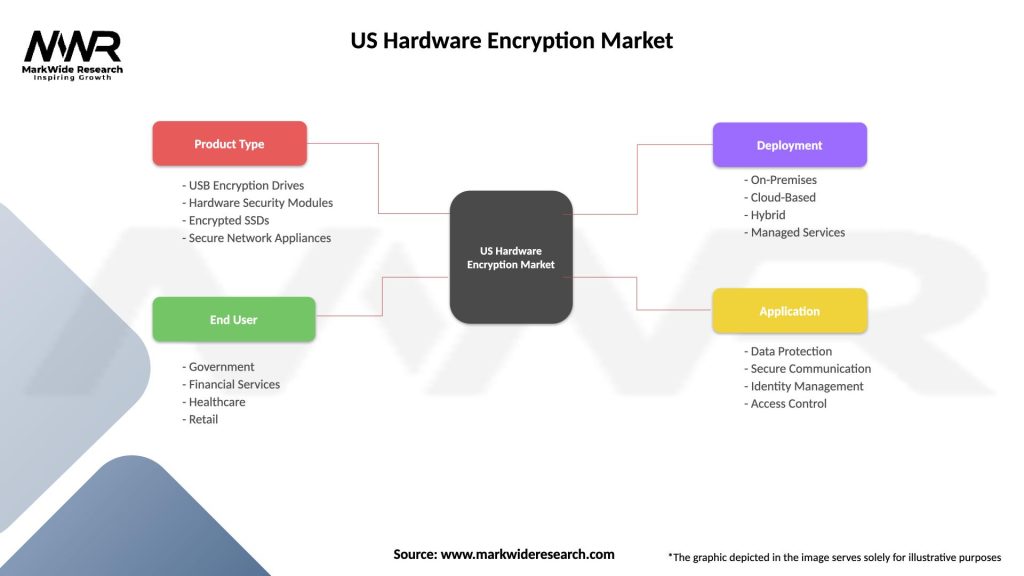

The US hardware encryption market can be segmented based on various factors such as product type, application, end-user industry, and geography. Common segmentation categories include:

Product Type: Self-encrypting drives (SEDs), hardware security modules (HSMs), encrypted USB flash drives, hardware-encrypted storage devices, and network encryption appliances.

End-user Industry: Finance, healthcare, government and defense, IT and telecommunications, manufacturing, retail, and others.

Geography: Regional markets such as the West Coast, East Coast, Midwest, and South, as well as major metropolitan areas and technology hubs.

Segmentation enables vendors and stakeholders to identify target markets, tailor their product offerings, and develop targeted marketing strategies to address specific customer needs and industry verticals.

Category-wise Insights

Self-Encrypting Drives (SEDs): SEDs integrate encryption capabilities directly into the storage device, offering transparent and hardware-accelerated encryption for data-at-rest protection in desktops, laptops, servers, and storage arrays.

Hardware Security Modules (HSMs): HSMs provide cryptographic processing and key management functions in dedicated hardware devices, ensuring secure key storage, cryptographic operations, and compliance with regulatory requirements.

Encrypted USB Flash Drives: Encrypted USB flash drives offer portable and secure storage solutions for data on the go, featuring built-in encryption and authentication mechanisms to protect data from unauthorized access and theft.

Network Encryption Appliances: Network encryption appliances encrypt data-in-transit across network connections, tunnels, and communication links, ensuring confidentiality, integrity, and privacy for sensitive information transmitted over public or private networks.

Key Benefits for Industry Participants and Stakeholders

Enhanced Data Security: Hardware encryption provides robust protection against unauthorized access, data breaches, and cyber threats, ensuring the confidentiality, integrity, and availability of sensitive information.

Regulatory Compliance: Hardware encryption solutions help organizations achieve compliance with data protection regulations such as GDPR, HIPAA, PCI DSS, and FIPS, mitigating regulatory risks and penalties associated with non-compliance.

Improved Performance: Hardware-based encryption accelerates cryptographic operations, reducing processing overhead and latency compared to software-based encryption methods, thereby enhancing system performance and user experience.

Simplified Key Management: Dedicated hardware devices offer secure key storage and management capabilities, streamlining key generation, distribution, rotation, and revocation processes, and ensuring cryptographic key integrity and confidentiality.

Cost-Effective Security: Hardware encryption solutions provide cost-effective security measures by offloading cryptographic operations to dedicated hardware devices, minimizing the impact on CPU resources and reducing operational overhead.

SWOT Analysis

A SWOT analysis provides insights into the strengths, weaknesses, opportunities, and threats facing the US hardware encryption market:

Strengths:

Advanced cryptographic capabilities

High-performance encryption and decryption

Compliance with regulatory requirements

Strong partnerships with technology vendors and industry partners

Weaknesses:

Initial cost and investment

Complexity of integration and deployment

Limited interoperability with legacy systems

Dependence on vendor-specific hardware and proprietary technologies

Opportunities:

Growing demand for cloud encryption solutions

Expansion of IoT and edge computing applications

Integration with emerging technologies (e.g., AI, blockchain)

Development of quantum-resistant encryption algorithms and hardware

Threats:

Intense competition from software-based encryption solutions

Cybersecurity vulnerabilities and exploits

Rapid technological obsolescence and market disruption

Regulatory changes and compliance challenges

Understanding these factors enables stakeholders to capitalize on market opportunities, address weaknesses, mitigate threats, and leverage strengths to maintain a competitive edge in the US hardware encryption market.

Market Key Trends

Integration with Cloud Services: Hardware encryption solutions are increasingly integrated with cloud platforms and services to provide end-to-end data protection for cloud-based applications, data storage, and virtualized environments.

Shift towards Quantum-Safe Cryptography: With the emergence of quantum computing threats, there is a growing focus on developing and standardizing quantum-safe encryption algorithms and hardware to protect data against future quantum attacks.

Convergence with Blockchain Technology: Hardware encryption solutions are being integrated with blockchain platforms to enhance data security, privacy, and integrity for distributed ledger applications, smart contracts, and digital transactions.

Focus on User-Friendly Interfaces: Vendors are emphasizing user-friendly interfaces, intuitive management consoles, and seamless integration with existing IT infrastructure to enhance usability, accessibility, and adoption of hardware encryption solutions.

Covid-19 Impact

The COVID-19 pandemic has accelerated the adoption of hardware encryption solutions as organizations prioritize data security and privacy in remote work environments. With the rapid shift to remote work, cloud-based collaboration, and digital transformation initiatives, the need for secure encryption technologies to protect sensitive data has become paramount, driving market demand for hardware encryption solutions.

Key Industry Developments

Intel’s Secure Device Onboard (SDO) Initiative: Intel has introduced the Secure Device Onboard (SDO) initiative, which aims to enhance IoT device security by integrating hardware-based encryption and identity protection capabilities into IoT devices and edge computing platforms.

Samsung’s Knox Platform: Samsung’s Knox platform offers hardware-backed security features, including encryption, authentication, and secure boot mechanisms, to protect data on mobile devices, IoT endpoints, and enterprise workspaces.

Thales’ Hardware Security Modules (HSMs): Thales offers a range of hardware security modules (HSMs) that provide cryptographic services, key management, and secure storage for sensitive data, addressing the security requirements of cloud, IoT, and digital transformation initiatives.

Gemalto’s SafeNet Hardware Security Modules (HSMs): Gemalto’s SafeNet HSMs offer FIPS-certified encryption and key management capabilities, enabling organizations to secure their cryptographic keys and sensitive data across hybrid cloud environments and distributed networks.

Analyst Suggestions

Invest in Quantum-Safe Encryption: Organizations should invest in quantum-safe encryption technologies and hardware solutions to future-proof their data protection strategies against emerging quantum computing threats and vulnerabilities.

Adopt Zero Trust Security Frameworks: Implementing zero trust security frameworks, which assume that all devices and connections are untrusted by default, can enhance data security and resilience against insider threats, malware, and cyberattacks.

Enhance Endpoint Security: Strengthen endpoint security measures by deploying hardware-based encryption solutions on laptops, desktops, mobile devices, and IoT endpoints to protect sensitive data from unauthorized access and malware attacks.

Leverage Hardware Security Modules (HSMs): Utilize hardware security modules (HSMs) for secure key management, cryptographic operations, and compliance with data protection regulations, ensuring the integrity, confidentiality, and availability of cryptographic keys and sensitive information.

Future Outlook

The US hardware encryption market is poised for continued growth and innovation, driven by escalating cybersecurity threats, increasing regulatory pressures, and growing adoption of encryption solutions across diverse industries. Opportunities for market expansion abound as organizations prioritize data security, privacy, and compliance, fueling demand for hardware encryption solutions that offer robust protection, performance, and scalability. However, challenges such as cost considerations, integration complexity, and evolving threat landscapes need to be addressed to unlock the full potential of hardware encryption technologies in safeguarding sensitive data and digital assets.

Conclusion

The US hardware encryption market plays a critical role in addressing cybersecurity challenges and protecting sensitive data from unauthorized access, data breaches, and cyber threats. With increasing reliance on digital technologies, cloud services, and IoT devices, the demand for robust encryption solutions continues to rise, driving market growth and innovation in hardware-based encryption technologies. By investing in quantum-safe encryption, adopting zero trust security frameworks, enhancing endpoint security, and leveraging hardware security modules (HSMs), organizations can strengthen their data protection strategies, mitigate risks, and ensure compliance with regulatory requirements in an increasingly interconnected and digitalized world.

What is Hardware Encryption?

Hardware encryption refers to the process of encrypting data using dedicated hardware devices, which provide enhanced security and performance compared to software-based solutions. This technology is commonly used in various applications, including secure data storage, communication, and device authentication.

What are the key players in the US Hardware Encryption Market?

Key players in the US Hardware Encryption Market include companies like Thales, Gemalto, and IBM, which offer a range of hardware encryption solutions for data protection and secure communications. These companies are known for their innovative technologies and extensive product portfolios, among others.

What are the growth factors driving the US Hardware Encryption Market?

The US Hardware Encryption Market is driven by increasing concerns over data security, the rise in cyber threats, and the growing adoption of cloud services. Additionally, regulatory compliance requirements for data protection are pushing organizations to invest in hardware encryption solutions.

What challenges does the US Hardware Encryption Market face?

Challenges in the US Hardware Encryption Market include the high cost of implementation and the complexity of integrating hardware encryption solutions into existing systems. Furthermore, the rapid pace of technological advancements can make it difficult for companies to keep up with the latest security measures.

What opportunities exist in the US Hardware Encryption Market?

The US Hardware Encryption Market presents opportunities for growth through advancements in encryption technologies and the increasing demand for secure mobile devices. Additionally, the expansion of IoT devices and the need for secure data transmission in various industries are likely to drive market growth.

What trends are shaping the US Hardware Encryption Market?

Trends in the US Hardware Encryption Market include the integration of artificial intelligence for enhanced security measures and the development of more compact and efficient encryption hardware. Moreover, the shift towards remote work and cloud computing is increasing the demand for robust hardware encryption solutions.

Leading Companies in the US Hardware Encryption Market:

Kingston Technology Corporation

Seagate Technology PLC

Western Digital Corporation

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

Toshiba Corporation

NetApp, Inc.

Thales Group

Kanguru Solutions

Apricorn, LLC

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.