444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The US FTL brokerage market represents a critical component of the American logistics and transportation ecosystem, facilitating the efficient movement of full truckload shipments across the nation. Full truckload brokerage services have emerged as essential intermediaries connecting shippers with carriers, optimizing freight capacity utilization and streamlining supply chain operations. The market has experienced robust growth driven by increasing e-commerce activities, manufacturing expansion, and the growing complexity of modern supply chains.

Digital transformation has revolutionized the FTL brokerage landscape, with technology-enabled platforms providing real-time visibility, automated matching capabilities, and enhanced operational efficiency. The market demonstrates significant growth potential with adoption rates increasing by 12.5% annually as more businesses recognize the value of professional freight brokerage services. Regional distribution shows concentrated activity in major industrial corridors, with the Midwest and Southeast regions accounting for 45% of total market activity.

Market dynamics indicate strong demand from diverse industry sectors including automotive, retail, manufacturing, and agriculture. The integration of advanced technologies such as artificial intelligence, machine learning, and IoT devices has enhanced service delivery capabilities, resulting in operational efficiency improvements of up to 25% for leading brokerage providers.

The US FTL brokerage market refers to the comprehensive ecosystem of intermediary services that facilitate the arrangement, coordination, and management of full truckload freight transportation between shippers and motor carriers. FTL brokerage encompasses the professional services provided by licensed freight brokers who act as intermediaries to match available truck capacity with shipping requirements, negotiate rates, and manage the logistics process from pickup to delivery.

Full truckload brokerage involves dedicated truck capacity where the entire trailer space is utilized by a single shipper’s freight, distinguishing it from less-than-truckload (LTL) services. Freight brokers leverage their network relationships, market knowledge, and technological capabilities to provide value-added services including route optimization, carrier vetting, load tracking, and documentation management.

The market encompasses various service models including traditional brokerage, digital freight matching platforms, and hybrid technology-enabled services. These services facilitate efficient freight movement while providing shippers with access to carrier capacity and offering carriers consistent freight opportunities to maximize asset utilization.

Market leadership in the US FTL brokerage sector is characterized by a combination of established traditional brokers and innovative technology-driven platforms that are reshaping industry dynamics. The market demonstrates strong fundamentals supported by consistent freight demand, expanding e-commerce activities, and increasing supply chain complexity that drives demand for professional brokerage services.

Technology adoption has accelerated significantly, with digital platform utilization growing by 18.3% year-over-year as market participants embrace automation, real-time visibility, and data-driven decision-making capabilities. Competitive differentiation increasingly relies on technological sophistication, service quality, and the ability to provide comprehensive supply chain solutions beyond basic freight matching.

Regional market dynamics show concentrated activity in major freight corridors, with the Texas Triangle, Great Lakes region, and Northeast corridor representing primary growth areas. The market benefits from diverse industry demand including automotive manufacturing, retail distribution, agricultural products, and industrial goods transportation.

Future growth prospects remain positive, driven by continued e-commerce expansion, nearshoring trends, infrastructure investments, and the ongoing digital transformation of logistics operations. Market consolidation trends indicate opportunities for strategic partnerships and acquisitions as companies seek to enhance their technological capabilities and market reach.

Strategic market insights reveal several critical trends shaping the US FTL brokerage landscape:

Primary growth drivers propelling the US FTL brokerage market include the exponential expansion of e-commerce activities, which has fundamentally altered freight transportation patterns and increased demand for flexible, scalable logistics solutions. E-commerce growth has created new shipping requirements that traditional transportation models struggle to accommodate efficiently, driving increased reliance on professional brokerage services.

Supply chain complexity continues to increase as businesses adopt more sophisticated distribution strategies, multi-channel fulfillment models, and just-in-time inventory management practices. This complexity creates opportunities for specialized brokerage services that can navigate intricate logistics requirements and provide comprehensive solutions.

Capacity constraints in the trucking industry, including driver shortages and equipment limitations, have elevated the importance of efficient capacity utilization and professional freight matching services. Freight brokers play a crucial role in optimizing available capacity and ensuring efficient freight movement despite these constraints.

Technology advancement serves as both a driver and enabler, with innovations in artificial intelligence, machine learning, and IoT devices creating new service capabilities and operational efficiencies. Digital transformation initiatives across industries are driving demand for technology-enabled logistics solutions that can integrate seamlessly with existing business systems.

Regulatory challenges present ongoing constraints for the FTL brokerage market, including licensing requirements, insurance obligations, and compliance with federal transportation regulations. Regulatory complexity can create barriers to entry for new market participants and impose ongoing operational costs for existing brokers.

Market fragmentation remains a significant challenge, with thousands of small and medium-sized brokers competing alongside larger established players. This fragmentation can lead to pricing pressures and difficulty in achieving economies of scale necessary for significant technology investments.

Economic volatility impacts freight demand patterns and can create uncertainty in capacity planning and pricing strategies. Economic downturns typically result in reduced shipping volumes and increased price competition among brokerage providers.

Technology integration costs represent substantial investments for traditional brokers seeking to modernize their operations. The need for continuous technology upgrades and system maintenance can strain resources, particularly for smaller brokerage firms with limited capital resources.

Carrier relationship management challenges include maintaining reliable capacity access during peak demand periods and managing relationships with diverse carrier types ranging from large fleets to independent owner-operators.

Digital transformation opportunities continue to emerge as traditional brokers modernize their operations and new technology-focused entrants disrupt established business models. Artificial intelligence and machine learning applications offer significant potential for improving matching algorithms, predictive analytics, and automated decision-making processes.

Vertical market specialization presents opportunities for brokers to develop expertise in specific industry sectors such as automotive, pharmaceuticals, food and beverage, or hazardous materials transportation. Specialized services can command premium pricing and create competitive differentiation.

Geographic expansion opportunities exist for regional brokers to extend their service areas and for national players to strengthen their presence in underserved markets. Cross-border trade with Mexico and Canada offers additional growth potential for brokers with international capabilities.

Value-added services beyond basic freight brokerage include warehousing, distribution, inventory management, and supply chain consulting. These comprehensive logistics solutions can increase customer retention and improve profit margins.

Sustainability initiatives create opportunities for brokers to differentiate their services through environmental responsibility programs, fuel-efficient routing, and carbon footprint reduction services that appeal to environmentally conscious shippers.

Competitive dynamics in the US FTL brokerage market are characterized by intense competition across multiple dimensions including pricing, service quality, technology capabilities, and geographic coverage. Market leaders are investing heavily in technology infrastructure to maintain competitive advantages and improve operational efficiency.

Pricing dynamics reflect the cyclical nature of freight demand, with rates fluctuating based on capacity availability, fuel costs, seasonal demand patterns, and economic conditions. Dynamic pricing models enabled by advanced analytics are becoming increasingly sophisticated, allowing brokers to optimize margins while remaining competitive.

Customer expectations continue to evolve, with shippers demanding greater visibility, faster response times, and more comprehensive service offerings. Digital-native customers particularly expect self-service capabilities, real-time tracking, and mobile-friendly interfaces.

Operational efficiency improvements through automation and process optimization have enabled leading brokers to achieve productivity gains of up to 30% while maintaining high service quality standards. MarkWide Research analysis indicates that technology-enabled efficiency improvements are becoming a primary competitive differentiator.

Market consolidation trends suggest ongoing opportunities for mergers and acquisitions as companies seek to achieve scale advantages, expand geographic coverage, and enhance technological capabilities.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into the US FTL brokerage market. Primary research includes extensive interviews with industry executives, freight brokers, shippers, and carriers to gather firsthand insights into market trends, challenges, and opportunities.

Secondary research encompasses analysis of industry reports, regulatory filings, company financial statements, and trade association data to validate primary findings and provide comprehensive market context. Data triangulation techniques ensure accuracy and reliability of research conclusions.

Market sizing methodologies utilize multiple approaches including top-down analysis based on total freight volumes and bottom-up analysis based on individual broker performance metrics. Statistical modeling techniques help identify growth patterns and forecast future market trends.

Technology assessment involves evaluation of digital platforms, software solutions, and emerging technologies that are shaping the brokerage landscape. Competitive intelligence gathering includes analysis of service offerings, pricing strategies, and market positioning of key industry participants.

Regional analysis incorporates geographic segmentation to understand local market dynamics, regulatory variations, and regional growth opportunities across different US markets.

Regional market distribution across the United States shows distinct patterns reflecting industrial activity, population centers, and transportation infrastructure. The Midwest region maintains the largest market share at approximately 28% due to its central location, manufacturing base, and agricultural production that generates substantial freight volumes.

Southeast markets demonstrate rapid growth driven by population migration, manufacturing expansion, and port activity, representing 24% of market activity. States like Texas, Georgia, and Florida serve as major freight hubs with significant brokerage operations supporting diverse industry sectors.

Western region markets, including California, benefit from international trade flows, agricultural exports, and technology sector growth. The region’s 22% market share reflects the importance of Pacific Coast ports and cross-border trade with Mexico in driving freight brokerage demand.

Northeast corridor maintains strong market presence despite geographic constraints, with dense population centers and established industrial base supporting consistent freight demand. The region accounts for approximately 18% of market activity with particular strength in retail distribution and manufacturing sectors.

Mountain and Plains states represent emerging growth opportunities as businesses seek lower-cost operating environments and improved logistics connectivity. These regions show above-average growth rates as distribution networks expand to serve growing populations and economic activity.

Market leadership in the US FTL brokerage sector is distributed among several categories of participants, each with distinct competitive advantages and market positioning strategies:

Competitive differentiation strategies include technology innovation, service specialization, geographic coverage, industry expertise, and customer relationship management. Digital transformation initiatives are becoming increasingly important for maintaining competitive positioning in the evolving market landscape.

Market segmentation analysis reveals distinct categories based on multiple criteria that help define competitive dynamics and growth opportunities within the US FTL brokerage market.

By Service Type:

By Industry Vertical:

By Geographic Scope:

Traditional brokerage services continue to maintain significant market presence despite technological disruption, with established relationships and industry expertise providing competitive advantages. These services typically emphasize personal customer service, carrier relationship management, and problem-solving capabilities that complement technological solutions.

Digital freight platforms are experiencing rapid growth as they offer operational efficiency, cost transparency, and real-time visibility that appeal to both shippers and carriers. Technology adoption rates in this category show accelerating growth of 22% annually as market participants embrace digital transformation.

Managed transportation services represent the highest-value segment, providing comprehensive logistics outsourcing that includes strategic planning, network optimization, and performance management. This category demonstrates strong customer retention rates exceeding 85% due to the strategic nature of these partnerships.

Specialized freight services command premium pricing through expertise in specific cargo types, regulatory requirements, or handling procedures. Specialization strategies enable brokers to differentiate their services and build competitive moats in niche market segments.

Industry vertical focus allows brokers to develop deep expertise in specific sectors, understanding unique requirements, seasonal patterns, and regulatory considerations that create value for customers in those industries.

Shippers benefit significantly from professional FTL brokerage services through access to expanded carrier networks, improved capacity utilization, and reduced transportation costs. Cost optimization typically ranges from 8-15% compared to direct carrier relationships, while service reliability improvements enhance supply chain performance.

Operational efficiency gains include reduced administrative burden, automated documentation, and streamlined communication processes that free up internal resources for core business activities. Technology integration provides real-time visibility, predictive analytics, and performance reporting that support strategic decision-making.

Carriers benefit from consistent freight opportunities, reduced empty miles, and access to diverse shipping customers through broker networks. Revenue optimization opportunities include better load matching, route planning, and capacity utilization that improve overall profitability.

Risk mitigation advantages include professional insurance coverage, regulatory compliance support, and dispute resolution services that protect both shippers and carriers from potential liabilities and operational disruptions.

Scalability benefits allow businesses to adjust transportation capacity based on demand fluctuations without long-term commitments or capital investments in transportation assets. This flexibility is particularly valuable for seasonal businesses and growing companies.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation acceleration represents the most significant trend reshaping the FTL brokerage landscape, with artificial intelligence, machine learning, and predictive analytics becoming standard capabilities rather than competitive differentiators. Automation levels in leading platforms now handle over 60% of routine transactions without human intervention.

Real-time visibility has evolved from a premium service to a basic customer expectation, with shippers demanding comprehensive tracking, predictive delivery estimates, and proactive communication throughout the transportation process. IoT integration and telematics data provide unprecedented insight into freight movement and carrier performance.

Sustainability focus is driving demand for environmentally responsible transportation solutions, including fuel-efficient routing, carbon footprint reporting, and participation in green logistics initiatives. Environmental considerations are increasingly influencing carrier selection and routing decisions.

Customer experience enhancement through user-friendly interfaces, mobile applications, and self-service portals is becoming critical for customer acquisition and retention. Digital-native expectations are pushing traditional brokers to modernize their customer interaction models.

Data monetization opportunities are emerging as brokers leverage their transaction data to provide market intelligence, benchmarking services, and predictive insights that create additional revenue streams beyond traditional brokerage fees.

Strategic acquisitions continue to reshape the competitive landscape as established players acquire technology companies and regional brokers to enhance their capabilities and market coverage. Consolidation activity has accelerated with acquisition volumes increasing by 35% over the past two years.

Technology partnerships between traditional brokers and software providers are creating innovative solutions that combine industry expertise with cutting-edge technology capabilities. These collaborations enable faster innovation cycles and reduced development costs.

Regulatory developments including electronic logging device (ELD) mandates and hours-of-service regulations continue to impact carrier operations and create opportunities for brokers to provide compliance support and operational optimization services.

Investment activity in freight technology startups has attracted significant venture capital funding, driving innovation in areas such as autonomous freight matching, blockchain applications, and advanced analytics platforms.

International expansion initiatives by major US brokers are extending their service capabilities into cross-border trade with Mexico and Canada, creating new growth opportunities and service offerings for customers with international shipping requirements.

Technology investment priorities should focus on artificial intelligence and machine learning capabilities that can provide competitive differentiation through superior matching algorithms, predictive analytics, and automated decision-making processes. MWR analysis suggests that companies investing in advanced technology achieve operational efficiency gains of 20-25% compared to traditional approaches.

Customer experience optimization requires comprehensive digital transformation including mobile-friendly interfaces, self-service capabilities, and real-time communication tools that meet evolving customer expectations. User experience design should prioritize simplicity, functionality, and accessibility across all customer touchpoints.

Strategic partnerships with technology providers, carriers, and complementary service providers can accelerate capability development and market expansion while reducing capital requirements and implementation risks.

Vertical market specialization offers opportunities to develop deep industry expertise and command premium pricing through specialized knowledge of regulatory requirements, handling procedures, and customer needs in specific sectors.

Data strategy development should focus on collecting, analyzing, and monetizing the vast amounts of transaction and operational data generated through brokerage operations to create additional value for customers and new revenue opportunities.

Long-term growth prospects for the US FTL brokerage market remain positive, supported by continued e-commerce expansion, supply chain complexity, and the ongoing digital transformation of logistics operations. Market evolution will likely favor technology-enabled providers that can deliver superior efficiency, visibility, and customer experience.

Technology integration will continue accelerating, with artificial intelligence, machine learning, and automation becoming standard capabilities across the industry. MarkWide Research projects that technology adoption rates will reach 75% market penetration within the next five years as competitive pressures drive modernization efforts.

Market consolidation trends suggest continued opportunities for mergers and acquisitions as companies seek scale advantages, technological capabilities, and expanded geographic coverage. Industry structure may evolve toward fewer, larger players with comprehensive service offerings and advanced technology platforms.

Sustainability initiatives will become increasingly important as environmental regulations tighten and customer demand for green logistics solutions grows. Carbon footprint reduction and fuel efficiency optimization will become standard service offerings rather than premium features.

International expansion opportunities will grow as cross-border trade increases and US brokers extend their capabilities into adjacent markets, particularly trade with Mexico and Canada where regulatory harmonization creates operational efficiencies.

The US FTL brokerage market stands at a critical inflection point where traditional relationship-based business models are evolving to incorporate advanced technology capabilities and enhanced customer experiences. Market fundamentals remain strong, supported by consistent freight demand, supply chain complexity, and the essential role that professional brokerage services play in optimizing transportation efficiency.

Digital transformation has emerged as the primary competitive differentiator, with leading companies investing heavily in artificial intelligence, automation, and data analytics capabilities that provide superior operational efficiency and customer value. The market’s evolution toward technology-enabled solutions creates both opportunities and challenges for industry participants at all levels.

Future success in the FTL brokerage market will depend on the ability to balance technological innovation with human expertise, providing customers with the efficiency and transparency they demand while maintaining the relationship-based service quality that has traditionally defined the industry. Companies that successfully navigate this transformation will be well-positioned to capture the significant growth opportunities that lie ahead in this dynamic and essential market segment.

What is US FTL Brokerage?

US FTL Brokerage refers to the business of facilitating full truckload shipping services within the United States, connecting shippers with carriers to transport goods efficiently. This sector plays a crucial role in logistics and supply chain management.

What are the key players in the US FTL Brokerage Market?

Key players in the US FTL Brokerage Market include C.H. Robinson, XPO Logistics, and Echo Global Logistics, among others. These companies provide a range of services, including freight matching, logistics management, and supply chain solutions.

What are the main drivers of growth in the US FTL Brokerage Market?

The main drivers of growth in the US FTL Brokerage Market include the increasing demand for efficient logistics solutions, the rise of e-commerce, and advancements in technology that enhance tracking and management of shipments.

What challenges does the US FTL Brokerage Market face?

The US FTL Brokerage Market faces challenges such as fluctuating fuel prices, driver shortages, and regulatory compliance issues. These factors can impact operational costs and service reliability.

What opportunities exist in the US FTL Brokerage Market?

Opportunities in the US FTL Brokerage Market include the expansion of digital freight platforms, increased automation in logistics, and the growing emphasis on sustainability in transportation practices.

What trends are shaping the US FTL Brokerage Market?

Trends shaping the US FTL Brokerage Market include the adoption of artificial intelligence for route optimization, the integration of blockchain for enhanced transparency, and a shift towards more sustainable logistics practices.

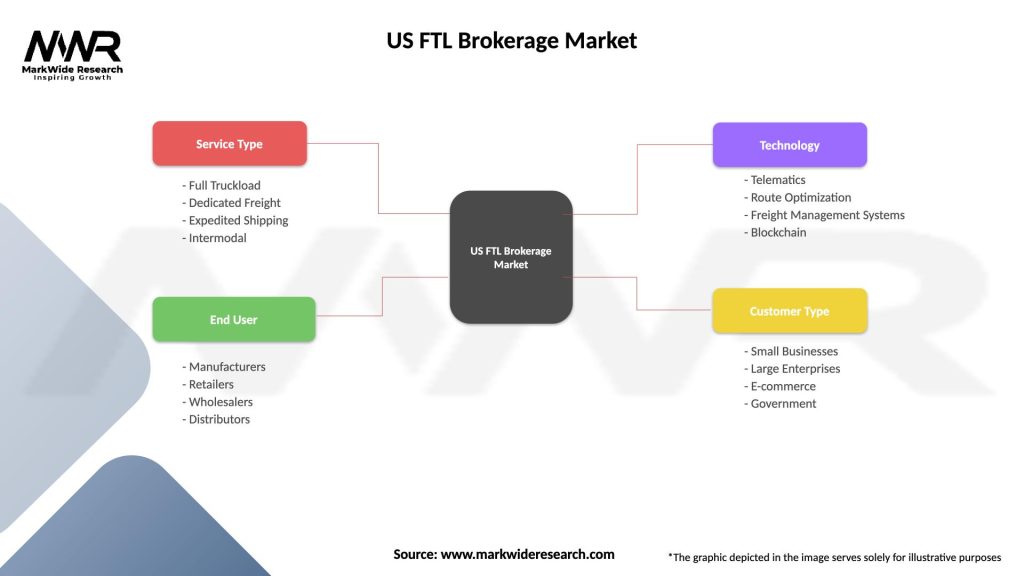

US FTL Brokerage Market

| Segmentation Details | Description |

|---|---|

| Service Type | Full Truckload, Dedicated Freight, Expedited Shipping, Intermodal |

| End User | Manufacturers, Retailers, Wholesalers, Distributors |

| Technology | Telematics, Route Optimization, Freight Management Systems, Blockchain |

| Customer Type | Small Businesses, Large Enterprises, E-commerce, Government |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the US FTL Brokerage Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.