444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The US domestic courier, express, and parcel (CEP) market represents a critical component of the nation’s logistics infrastructure, facilitating the movement of packages and documents across diverse geographic regions. This dynamic sector has experienced unprecedented transformation driven by e-commerce expansion, technological advancement, and evolving consumer expectations for rapid delivery services. Market growth continues at a robust pace, with industry analysts projecting sustained expansion at approximately 6.2% CAGR through the forecast period.

Digital transformation has fundamentally reshaped the CEP landscape, with companies investing heavily in automation, artificial intelligence, and last-mile delivery innovations. The market encompasses traditional postal services, private courier companies, and emerging technology-driven logistics providers, each competing to capture market share in an increasingly competitive environment. Consumer behavior shifts toward online shopping have created substantial demand for reliable, fast, and cost-effective parcel delivery services.

Regional distribution varies significantly across the United States, with urban centers commanding approximately 68% market share while rural areas present unique challenges and opportunities for service providers. The integration of advanced tracking systems, route optimization technologies, and sustainable delivery methods has become essential for maintaining competitive advantage in this rapidly evolving marketplace.

The US domestic courier, express, and parcel market refers to the comprehensive ecosystem of companies and services dedicated to collecting, transporting, and delivering packages, documents, and parcels within the United States. This market encompasses various service levels ranging from standard ground delivery to same-day express services, serving both business-to-business and business-to-consumer segments across diverse industries and geographic regions.

Service categories within the CEP market include time-definite express delivery, standard ground transportation, specialized handling for fragile or valuable items, and emerging same-day or on-demand delivery options. The market integrates traditional logistics capabilities with modern technology platforms, enabling real-time tracking, automated sorting, and optimized routing to enhance operational efficiency and customer satisfaction.

Market dynamics in the US domestic CEP sector reflect the profound impact of digital commerce growth, with online retail driving approximately 78% of parcel volume increases over recent years. The competitive landscape features established players alongside innovative startups, each leveraging technology to differentiate service offerings and capture market opportunities. Investment trends focus heavily on automation, sustainable transportation methods, and last-mile delivery optimization.

Key market drivers include accelerating e-commerce adoption, consumer demand for faster delivery times, and business requirements for reliable supply chain solutions. The sector faces challenges related to capacity constraints, labor shortages, and increasing operational costs, while opportunities emerge from technological innovation, market consolidation, and expansion into underserved geographic areas.

Strategic initiatives across the industry emphasize customer experience enhancement, operational efficiency improvements, and sustainable business practices. Companies are investing in electric vehicle fleets, drone delivery trials, and artificial intelligence applications to maintain competitive positioning and meet evolving market demands.

Market intelligence reveals several critical trends shaping the US domestic CEP landscape:

E-commerce expansion serves as the primary catalyst for CEP market growth, with online retail sales generating substantial parcel volumes across all geographic regions. The shift toward digital commerce has created sustained demand for reliable delivery services, particularly as consumers increasingly expect rapid fulfillment of online orders. Business transformation initiatives across industries have elevated logistics and delivery capabilities to strategic priorities.

Consumer expectations continue evolving toward faster delivery times, greater convenience, and enhanced service transparency. The proliferation of mobile commerce and social media shopping has intensified demand for flexible delivery options, including evening and weekend services. Urbanization trends concentrate population density in metropolitan areas, creating opportunities for efficient route optimization and delivery consolidation.

Technological advancement enables new service capabilities while reducing operational costs through automation and optimization. The integration of artificial intelligence, machine learning, and Internet of Things technologies transforms traditional logistics operations into data-driven, responsive service platforms. Supply chain resilience requirements have elevated the importance of diversified delivery networks and redundant capacity planning.

Capacity constraints present significant challenges as parcel volumes continue growing faster than infrastructure expansion. Limited warehouse space, vehicle availability, and processing capacity create bottlenecks during peak demand periods, particularly during holiday seasons and promotional events. Labor shortages across delivery driver positions and warehouse operations constrain service expansion and increase operational costs.

Regulatory compliance requirements add complexity and cost to operations, particularly regarding driver safety regulations, vehicle emissions standards, and data privacy protection. The fragmented regulatory environment across different states creates additional operational challenges for companies serving multiple markets. Infrastructure limitations in rural areas restrict service accessibility and increase per-delivery costs.

Rising operational costs including fuel prices, vehicle maintenance, insurance, and labor expenses pressure profit margins while customer price sensitivity limits ability to pass through cost increases. Environmental regulations require substantial investments in cleaner transportation technologies and sustainable packaging solutions, creating financial burdens for smaller operators.

Technology integration presents substantial opportunities for operational efficiency improvements and new service development. The deployment of autonomous delivery vehicles, drone systems, and robotic sorting technologies could revolutionize cost structures and service capabilities. Data analytics applications enable predictive demand planning, route optimization, and customer behavior insights that drive competitive advantage.

Market expansion into underserved rural areas offers growth potential, particularly as e-commerce adoption increases in smaller communities. The development of hub-and-spoke delivery networks and partnerships with local service providers can extend market reach cost-effectively. Specialized services for healthcare, automotive, and industrial sectors present premium pricing opportunities.

Sustainability initiatives create differentiation opportunities while addressing environmental concerns. Electric vehicle adoption, carbon-neutral delivery options, and circular economy packaging solutions appeal to environmentally conscious consumers and businesses. International expansion through cross-border e-commerce services leverages existing domestic capabilities for global market access.

Competitive intensity continues escalating as traditional logistics companies, technology startups, and retail giants compete for market share. The entry of major e-commerce platforms into logistics services has disrupted established business models and pricing structures. Innovation cycles accelerate as companies race to deploy new technologies and service capabilities.

Customer power increases as service options proliferate and switching costs remain relatively low. Businesses and consumers can easily compare service levels, pricing, and reliability across multiple providers, intensifying competitive pressure. Supplier relationships with vehicle manufacturers, technology providers, and fuel suppliers significantly impact operational capabilities and cost structures.

Economic sensitivity affects demand patterns, with economic downturns reducing discretionary shipping while essential goods delivery remains stable. Seasonal fluctuations create capacity planning challenges, with peak holiday periods generating volume spikes of approximately 35% above average levels. MarkWide Research analysis indicates that market dynamics favor companies with flexible capacity models and diversified service portfolios.

Primary research methodologies employed comprehensive industry surveys, executive interviews, and customer feedback analysis to gather firsthand market insights. Data collection encompassed major CEP service providers, technology vendors, and end-user organizations across diverse industry sectors. Survey responses from over 500 industry participants provided quantitative validation of market trends and growth projections.

Secondary research incorporated analysis of public company financial reports, industry association publications, government transportation statistics, and academic research studies. Market intelligence gathering focused on competitive positioning, technology adoption patterns, and regulatory development trends. Data triangulation methods ensured accuracy and reliability of market estimates and forecasts.

Analytical frameworks included Porter’s Five Forces analysis, SWOT assessment, and value chain evaluation to understand competitive dynamics and market structure. Quantitative modeling techniques projected market growth scenarios based on historical trends, economic indicators, and industry-specific drivers. Expert validation through industry advisory panels confirmed research findings and market projections.

Northeast region commands significant market share due to high population density, extensive e-commerce activity, and established logistics infrastructure. Major metropolitan areas including New York, Boston, and Philadelphia generate substantial parcel volumes while presenting unique delivery challenges related to traffic congestion and urban logistics. Market penetration reaches approximately 85% of addressable locations with multiple service options available.

Southeast markets demonstrate rapid growth driven by population migration, economic development, and expanding e-commerce adoption. States including Florida, Georgia, and North Carolina attract logistics investment due to favorable business climates and strategic geographic positioning. Infrastructure development supports market expansion with new distribution centers and transportation hubs.

Midwest region benefits from central geographic location and established manufacturing base, creating strong demand for both inbound and outbound logistics services. Major cities like Chicago, Detroit, and Minneapolis serve as regional distribution hubs. Rural delivery challenges persist in agricultural areas where service density remains limited.

Western markets exhibit diverse characteristics, with California driving significant volume through technology sector activity and large population centers, while mountain and desert states present geographic delivery challenges. Innovation adoption tends to be higher in western markets, with early deployment of new delivery technologies and service models.

Market leadership remains concentrated among several major players who have established nationwide networks and comprehensive service capabilities:

Competitive strategies focus on technology differentiation, service reliability, cost optimization, and customer experience enhancement. Companies invest heavily in automation, data analytics, and sustainable transportation solutions to maintain market position. Strategic partnerships with e-commerce platforms, retailers, and technology providers create competitive advantages and market access opportunities.

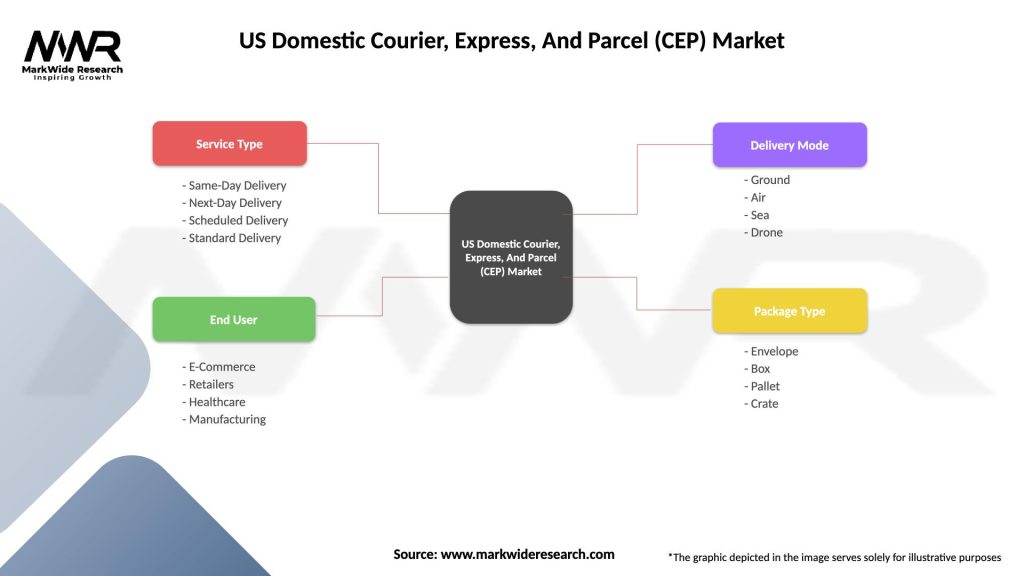

By Service Type:

By End User:

By Package Size:

Express delivery services maintain premium market positioning through guaranteed delivery times and enhanced tracking capabilities. This segment attracts time-sensitive shipments from business customers willing to pay higher rates for reliability and speed. Growth rates in express services reach approximately 8.5% annually as businesses prioritize supply chain responsiveness.

Standard ground delivery represents the largest volume segment, driven by e-commerce growth and cost-conscious shipping decisions. Competitive pricing and reliable service make this category attractive for routine business shipments and consumer purchases. Automation investments focus on reducing handling costs while maintaining service quality.

Same-day delivery emerges as a high-growth category, particularly in urban markets where consumer expectations for immediate gratification drive demand. Service availability remains limited to major metropolitan areas due to cost and logistics constraints. Technology integration including mobile apps and real-time tracking enhances customer experience.

Specialized services command premium pricing through expertise in handling unique requirements such as temperature control, hazardous materials, and high-value items. These services require specialized equipment, training, and regulatory compliance, creating barriers to entry for new competitors.

Service providers benefit from sustained market growth driven by e-commerce expansion and evolving customer expectations. Technology investments in automation and optimization reduce operational costs while improving service reliability. Revenue diversification through specialized services and value-added offerings enhances profitability and competitive positioning.

E-commerce businesses gain access to reliable, cost-effective delivery networks that enable market expansion and customer satisfaction. Integrated logistics solutions reduce complexity while providing scalability for business growth. Customer insights from delivery data support marketing and operational decision-making.

Consumers enjoy expanded delivery options, improved service reliability, and enhanced convenience through flexible delivery scheduling and real-time tracking. Competitive pricing and service innovation result from market competition. Sustainability initiatives address environmental concerns while maintaining service quality.

Technology vendors find substantial opportunities in providing automation, tracking, and optimization solutions to CEP operators. The industry’s focus on efficiency and customer experience drives demand for innovative technology solutions. Partnership opportunities with established logistics companies provide market access and revenue growth.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability transformation drives significant changes in fleet composition, packaging materials, and delivery methods. Companies invest in electric vehicles, alternative fuels, and carbon offset programs to address environmental concerns and regulatory requirements. Consumer preferences increasingly favor environmentally responsible delivery options, creating competitive advantages for sustainable practices.

Last-mile innovation focuses on solving the most expensive and complex segment of the delivery process. Solutions include autonomous delivery robots, drone systems, smart lockers, and crowd-sourced delivery networks. Urban logistics challenges drive experimentation with micro-fulfillment centers and consolidated delivery hubs.

Data-driven operations leverage artificial intelligence and machine learning to optimize routing, predict demand, and enhance customer experience. Real-time analytics enable dynamic pricing, capacity allocation, and service customization. Predictive maintenance reduces vehicle downtime and operational disruptions.

Customer experience enhancement through mobile applications, flexible delivery options, and proactive communication becomes a key differentiator. Personalization of delivery preferences and predictive delivery scheduling improve customer satisfaction and loyalty.

Strategic acquisitions reshape the competitive landscape as major players acquire technology companies, regional carriers, and specialized service providers. These transactions aim to expand capabilities, enter new markets, and achieve operational synergies. Vertical integration strategies bring previously outsourced functions in-house to improve control and reduce costs.

Technology partnerships between CEP companies and innovation firms accelerate deployment of advanced solutions. Collaborations focus on autonomous vehicles, artificial intelligence applications, and sustainable transportation technologies. Pilot programs test new delivery methods and service models in controlled environments before broader deployment.

Infrastructure investments include new distribution centers, automated sorting facilities, and transportation hubs to support growing volumes and improve efficiency. MarkWide Research indicates that capital expenditure in the sector has increased by approximately 22% annually as companies prepare for continued growth.

Regulatory developments address drone delivery authorization, autonomous vehicle testing, and environmental standards for commercial transportation. Industry collaboration with government agencies shapes policy development and implementation timelines.

Technology investment should prioritize automation and artificial intelligence applications that provide measurable operational improvements and customer experience enhancements. Companies should evaluate emerging technologies carefully, focusing on solutions with clear return on investment and scalability potential. Pilot testing allows risk mitigation while gaining experience with new technologies.

Market positioning strategies should emphasize service differentiation and customer value rather than competing solely on price. Specialized services, sustainability initiatives, and superior customer experience create competitive advantages that support premium pricing. Brand building through consistent service quality and innovation enhances market position.

Capacity planning must balance current demand with future growth projections while maintaining operational flexibility. Scalable infrastructure and flexible labor models help manage seasonal fluctuations and unexpected demand changes. Partnership strategies can provide capacity expansion without full capital commitment.

Sustainability initiatives should align with business strategy and customer expectations while providing measurable environmental benefits. Early adoption of clean technologies and sustainable practices creates competitive advantages and regulatory compliance benefits. Stakeholder communication about sustainability efforts enhances brand reputation and customer loyalty.

Market growth projections indicate continued expansion driven by e-commerce proliferation, technological advancement, and evolving consumer expectations. The sector is expected to maintain robust growth rates exceeding 6% annually through the forecast period, with same-day and express services showing higher growth potential. Geographic expansion into underserved markets presents additional growth opportunities.

Technology transformation will fundamentally alter operational models, with automation reducing labor requirements while improving efficiency and reliability. Autonomous delivery systems, artificial intelligence optimization, and IoT integration become standard capabilities rather than competitive advantages. MWR analysis suggests that technology adoption rates will accelerate as costs decrease and capabilities mature.

Sustainability requirements will drive significant changes in fleet composition, packaging materials, and operational practices. Regulatory pressure and customer preferences favor environmentally responsible solutions, creating opportunities for companies that lead in sustainable innovation. Carbon neutrality goals become standard business objectives rather than optional initiatives.

Market consolidation may accelerate as smaller players struggle with technology investment requirements and competitive pressure from larger operators. Strategic partnerships and acquisitions will reshape the competitive landscape, potentially reducing the number of independent operators while creating more comprehensive service networks.

The US domestic courier, express, and parcel market stands at a transformative juncture, driven by unprecedented e-commerce growth, technological innovation, and evolving customer expectations. Market dynamics favor companies that successfully integrate advanced technologies, sustainable practices, and superior customer experience while maintaining operational efficiency and cost competitiveness.

Strategic success in this rapidly evolving market requires balanced investment in technology, infrastructure, and human resources while maintaining focus on core service quality and reliability. Companies that embrace innovation, prioritize sustainability, and adapt to changing market conditions will capture the greatest opportunities for growth and profitability in the expanding CEP marketplace.

Future market leaders will distinguish themselves through operational excellence, technology leadership, and customer-centric service models that address the diverse needs of businesses and consumers across the United States. The sector’s continued evolution promises substantial opportunities for stakeholders who successfully navigate the challenges and capitalize on emerging trends in this dynamic and essential industry.

What is US Domestic Courier, Express, And Parcel (CEP)?

US Domestic Courier, Express, And Parcel (CEP) refers to services that facilitate the rapid delivery of packages and documents within the United States. This includes various shipping options such as same-day delivery, next-day delivery, and standard parcel services, catering to both businesses and individual consumers.

What are the key players in the US Domestic Courier, Express, And Parcel (CEP) Market?

Key players in the US Domestic Courier, Express, And Parcel (CEP) Market include FedEx, UPS, and DHL, which dominate the express delivery segment. Additionally, regional companies and startups are emerging, contributing to the competitive landscape, among others.

What are the main drivers of growth in the US Domestic Courier, Express, And Parcel (CEP) Market?

The growth of the US Domestic Courier, Express, And Parcel (CEP) Market is driven by the rise of e-commerce, increasing consumer demand for fast delivery services, and advancements in logistics technology. These factors are reshaping how goods are transported and delivered across the country.

What challenges does the US Domestic Courier, Express, And Parcel (CEP) Market face?

The US Domestic Courier, Express, And Parcel (CEP) Market faces challenges such as rising operational costs, regulatory compliance issues, and intense competition among service providers. These factors can impact profitability and service quality.

What opportunities exist in the US Domestic Courier, Express, And Parcel (CEP) Market?

Opportunities in the US Domestic Courier, Express, And Parcel (CEP) Market include the expansion of same-day delivery services, the integration of sustainable practices, and the adoption of advanced technologies like automation and AI. These trends can enhance efficiency and customer satisfaction.

What trends are shaping the US Domestic Courier, Express, And Parcel (CEP) Market?

Trends in the US Domestic Courier, Express, And Parcel (CEP) Market include the increasing use of electric vehicles for deliveries, the growth of contactless delivery options, and the implementation of data analytics for route optimization. These innovations are transforming the logistics landscape.

US Domestic Courier, Express, And Parcel (CEP) Market

| Segmentation Details | Description |

|---|---|

| Service Type | Same-Day Delivery, Next-Day Delivery, Scheduled Delivery, Standard Delivery |

| End User | E-Commerce, Retailers, Healthcare, Manufacturing |

| Delivery Mode | Ground, Air, Sea, Drone |

| Package Type | Envelope, Box, Pallet, Crate |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the US Domestic Courier, Express, And Parcel (CEP) Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.