444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The US diabetes care drugs market represents one of the most critical and rapidly evolving segments within the American healthcare landscape. With diabetes affecting millions of Americans, the demand for innovative therapeutic solutions continues to drive substantial growth across multiple drug categories. The market encompasses a comprehensive range of medications including insulin products, oral antidiabetic drugs, GLP-1 receptor agonists, and emerging biosimilar alternatives that collectively address the diverse needs of Type 1 and Type 2 diabetes patients.

Market dynamics indicate robust expansion driven by increasing diabetes prevalence, aging demographics, and continuous pharmaceutical innovation. The sector demonstrates remarkable resilience with consistent growth rates of approximately 8.2% CAGR projected through the forecast period. Technology integration and personalized medicine approaches are reshaping treatment paradigms, while regulatory support for breakthrough therapies accelerates market penetration of next-generation diabetes care solutions.

Healthcare infrastructure improvements and enhanced patient access programs contribute significantly to market expansion. The integration of digital health solutions with traditional pharmaceutical approaches creates comprehensive diabetes management ecosystems that improve patient outcomes while driving sustained market growth across diverse demographic segments.

The US diabetes care drugs market refers to the comprehensive pharmaceutical sector encompassing all therapeutic medications, treatments, and drug delivery systems specifically designed to manage, control, and treat diabetes mellitus in American patients. This market includes prescription medications for both Type 1 and Type 2 diabetes, ranging from traditional insulin formulations to advanced combination therapies and innovative drug delivery mechanisms.

Market scope extends beyond basic glucose control medications to include comprehensive therapeutic solutions addressing diabetes-related complications, cardiovascular risks, and metabolic disorders. The sector encompasses branded pharmaceuticals, generic alternatives, biosimilar products, and emerging precision medicine approaches that collectively serve the diverse treatment needs of America’s diabetic population.

Therapeutic categories within this market include rapid-acting and long-acting insulin preparations, oral hypoglycemic agents, injectable non-insulin medications, and combination drug formulations. The market also incorporates advanced drug delivery systems, continuous glucose monitoring integration, and personalized treatment protocols that enhance therapeutic efficacy and patient compliance across various diabetes management scenarios.

Strategic market analysis reveals the US diabetes care drugs market as a cornerstone of American healthcare, driven by unprecedented diabetes prevalence and continuous pharmaceutical innovation. The market demonstrates exceptional growth momentum with Type 2 diabetes medications representing approximately 85% market share while Type 1 diabetes treatments maintain steady demand growth. Insulin products continue dominating revenue generation, though newer drug classes including GLP-1 receptor agonists and SGLT-2 inhibitors capture increasing market segments.

Competitive landscape features established pharmaceutical giants alongside emerging biotechnology companies developing breakthrough therapies. Market leaders leverage extensive research capabilities, robust distribution networks, and comprehensive patient support programs to maintain competitive advantages. Generic competition intensifies pricing pressures while biosimilar alternatives create new market dynamics, particularly within insulin segments.

Regulatory environment supports accelerated drug approvals for innovative diabetes treatments while promoting generic competition to enhance patient affordability. Healthcare policy initiatives, insurance coverage expansions, and patient assistance programs collectively improve market accessibility. Digital health integration emerges as a key differentiator, with pharmaceutical companies incorporating technology solutions to enhance treatment outcomes and patient engagement across diverse therapeutic protocols.

Market intelligence reveals several transformative trends reshaping the US diabetes care drugs landscape. MarkWide Research analysis indicates that combination therapies represent the fastest-growing segment, with healthcare providers increasingly adopting multi-mechanism approaches to achieve optimal glycemic control while minimizing side effects and improving patient compliance rates.

Diabetes prevalence escalation serves as the primary market driver, with approximately 11.3% of American adults diagnosed with diabetes and millions more in pre-diabetic stages. The aging population demographic intensifies demand as diabetes incidence correlates strongly with advancing age, creating sustained market growth momentum across all therapeutic categories.

Lifestyle factors including sedentary behaviors, processed food consumption, and obesity epidemic contribute significantly to Type 2 diabetes development. Healthcare awareness campaigns and improved diagnostic capabilities result in earlier detection and treatment initiation, expanding the addressable patient population and driving consistent prescription volume growth across diverse geographic markets.

Pharmaceutical innovation accelerates market expansion through breakthrough therapies offering superior efficacy, reduced side effects, and improved patient convenience. Research investments in novel drug mechanisms, combination therapies, and personalized medicine approaches create competitive advantages while addressing unmet medical needs within specific patient populations.

Insurance coverage improvements and patient assistance programs enhance medication accessibility, reducing financial barriers that previously limited treatment adoption. Healthcare policy initiatives supporting diabetes care, including Medicare coverage expansions and state-level programs, create favorable market conditions for sustained growth across all socioeconomic segments.

Pricing pressures represent significant market challenges as healthcare payers, government programs, and patients demand more affordable diabetes care solutions. Generic competition and biosimilar alternatives create downward price pressure on established branded products, potentially limiting revenue growth despite volume increases across various therapeutic categories.

Regulatory complexities surrounding drug approvals, safety monitoring, and post-market surveillance requirements increase development costs and timeline uncertainties. FDA oversight intensifies for diabetes medications following historical safety concerns, creating additional hurdles for new product launches and market entry strategies.

Side effect concerns and safety profiles of certain diabetes medications limit prescriber confidence and patient acceptance. Hypoglycemia risks, weight gain potential, and cardiovascular safety considerations influence treatment selection decisions, potentially restricting market penetration for specific drug classes despite therapeutic efficacy.

Healthcare access disparities across different geographic regions and socioeconomic groups create market limitations. Rural healthcare challenges, specialist availability constraints, and insurance coverage gaps prevent optimal market penetration in underserved communities, limiting overall growth potential despite high diabetes prevalence rates.

Precision medicine advancement creates unprecedented opportunities for targeted diabetes therapies based on genetic profiles, biomarkers, and individual patient characteristics. Pharmacogenomic testing integration enables personalized treatment selection, improving outcomes while commanding premium pricing for specialized therapeutic solutions.

Digital health convergence offers substantial growth opportunities through integrated diabetes management platforms combining medications with technology solutions. Smart drug delivery systems, continuous monitoring integration, and artificial intelligence-driven treatment optimization create comprehensive care ecosystems that enhance patient outcomes and market differentiation.

Emerging markets within diabetes care include pre-diabetes interventions, gestational diabetes management, and pediatric diabetes specialization. Prevention-focused therapies addressing at-risk populations expand addressable markets beyond traditional diabetes treatment, creating new revenue streams and competitive positioning opportunities.

Combination therapy development presents significant opportunities for pharmaceutical companies to create differentiated products addressing multiple diabetes-related conditions simultaneously. Cardiovascular protection, kidney disease prevention, and weight management integration within diabetes medications create premium market segments with enhanced value propositions for healthcare providers and patients.

Competitive intensity characterizes the US diabetes care drugs market as established pharmaceutical companies compete with emerging biotechnology firms and generic manufacturers. Innovation cycles accelerate as companies invest heavily in research and development to maintain market leadership positions while addressing evolving patient needs and regulatory requirements.

Supply chain optimization becomes increasingly critical as companies balance cost management with quality assurance and regulatory compliance. Manufacturing efficiency improvements and strategic partnerships enable companies to maintain competitive pricing while ensuring consistent product availability across diverse distribution channels.

Healthcare provider relationships significantly influence market dynamics as pharmaceutical companies develop comprehensive support programs including clinical education, patient assistance, and outcomes monitoring. Value-based care initiatives reshape commercial strategies, emphasizing real-world evidence generation and outcomes-based pricing models that demonstrate therapeutic value beyond traditional efficacy metrics.

Patient advocacy and empowerment trends drive market evolution toward more transparent pricing, improved access programs, and enhanced treatment options. Social media influence and patient communities create new channels for market education and product adoption while potentially amplifying concerns about drug safety and accessibility issues.

Comprehensive market analysis employs multi-source data collection methodologies including primary research interviews with healthcare professionals, pharmaceutical executives, and diabetes care specialists across diverse geographic regions. Quantitative surveys capture prescribing patterns, treatment preferences, and market trend assessments from representative samples of endocrinologists, primary care physicians, and diabetes educators.

Secondary research integration incorporates extensive analysis of regulatory filings, clinical trial databases, patent landscapes, and competitive intelligence sources. Market modeling utilizes advanced statistical techniques to project growth trajectories, segment dynamics, and competitive positioning scenarios across multiple forecast periods and market conditions.

Data validation processes ensure accuracy through cross-referencing multiple information sources, expert panel reviews, and statistical significance testing. Quality assurance protocols maintain research integrity while addressing potential biases and limitations inherent in pharmaceutical market analysis methodologies.

Analytical frameworks incorporate both quantitative metrics and qualitative insights to provide comprehensive market understanding. Scenario planning methodologies evaluate potential market disruptions, regulatory changes, and competitive developments that could significantly impact future market dynamics and growth trajectories.

Geographic distribution across the United States reveals significant regional variations in diabetes care drug utilization patterns, with the Southern states demonstrating highest diabetes prevalence rates and corresponding medication demand. Texas, Florida, and California represent the largest state markets by absolute volume, while per-capita consumption rates peak in southeastern regions where diabetes incidence exceeds national averages.

Urban versus rural dynamics create distinct market characteristics, with metropolitan areas showing higher adoption rates for newer, premium-priced diabetes medications while rural regions rely more heavily on generic alternatives and traditional insulin formulations. Healthcare infrastructure availability significantly influences prescribing patterns and patient access to specialized diabetes care services.

Regional healthcare policies and state-level insurance programs create varying market conditions across different geographic areas. Medicaid expansion states demonstrate improved diabetes medication access and utilization rates compared to non-expansion states, with approximately 18% higher prescription volumes among low-income diabetic populations.

Demographic factors including age distribution, ethnic composition, and socioeconomic characteristics significantly influence regional market dynamics. Hispanic and African American communities show disproportionately high diabetes rates, creating concentrated demand in specific geographic regions while presenting unique challenges related to healthcare access and cultural treatment preferences.

Market leadership remains concentrated among several major pharmaceutical companies that have established dominant positions through extensive research capabilities, comprehensive product portfolios, and robust distribution networks. Strategic competition intensifies as companies pursue differentiation through innovative drug formulations, patient support programs, and digital health integration initiatives.

Drug class segmentation reveals distinct market dynamics across therapeutic categories, with insulin products maintaining the largest market share while newer drug classes demonstrate accelerated growth rates. Long-acting insulin formulations dominate the insulin segment, while GLP-1 receptor agonists represent the fastest-growing non-insulin category with approximately 15% annual growth rates.

By Drug Type:

By Diabetes Type:

Insulin category analysis reveals ongoing market evolution as biosimilar alternatives capture increasing market share while innovative formulations maintain premium positioning. Rapid-acting insulin products demonstrate steady demand growth driven by intensive diabetes management protocols and continuous glucose monitoring integration. Long-acting insulin formulations benefit from once-daily dosing convenience and improved glycemic control profiles.

Oral antidiabetic medications show diverse growth patterns with metformin maintaining foundational therapy status while newer drug classes including SGLT-2 inhibitors gain prescriber acceptance. Combination tablets address patient compliance challenges while providing comprehensive glucose control through multiple mechanisms of action.

Injectable non-insulin therapies represent the most dynamic market segment with GLP-1 receptor agonists demonstrating exceptional growth driven by weight loss benefits and cardiovascular protection properties. Weekly injection formulations gain preference over daily alternatives due to improved patient convenience and compliance rates.

Emerging categories include dual-action medications addressing both diabetes and related conditions such as obesity or cardiovascular disease. Smart insulin formulations incorporating glucose-responsive mechanisms represent future market opportunities with potential to revolutionize diabetes care through automated glucose regulation capabilities.

Pharmaceutical companies benefit from sustained market demand driven by chronic disease characteristics and expanding patient populations. Revenue stability results from recurring prescription patterns while innovation opportunities enable premium pricing for breakthrough therapies addressing unmet medical needs.

Healthcare providers gain access to comprehensive treatment options enabling personalized diabetes management approaches. Clinical outcomes improvement through advanced therapeutics enhances patient satisfaction while reducing long-term complications and associated healthcare costs.

Patients experience improved quality of life through better glucose control, reduced injection frequency, and enhanced convenience with modern drug formulations. Treatment flexibility allows personalized approaches accommodating individual lifestyle preferences and medical requirements.

Healthcare systems benefit from reduced diabetes-related complications and hospitalizations through effective medication management. Cost-effectiveness improves as generic alternatives and biosimilars provide affordable treatment options while maintaining therapeutic efficacy standards.

Insurance providers realize long-term cost savings through preventive diabetes care and complications reduction. Value-based care models align pharmaceutical costs with patient outcomes, creating sustainable healthcare economics while improving population health metrics.

Strengths:

Weaknesses:

Opportunities:

Threats:

Personalized medicine integration emerges as a transformative trend with pharmaceutical companies developing targeted therapies based on genetic profiles and biomarker analysis. Pharmacogenomic testing enables optimized drug selection while reducing adverse reactions and improving therapeutic outcomes across diverse patient populations.

Digital health convergence accelerates as diabetes medications integrate with smart devices, mobile applications, and telemedicine platforms. Connected insulin pens and automated dose tracking systems enhance patient compliance while providing healthcare providers with real-time treatment monitoring capabilities.

Combination therapy emphasis reflects clinical recognition that diabetes management requires multi-mechanism approaches. Fixed-dose combinations simplify treatment regimens while addressing glucose control, cardiovascular protection, and weight management simultaneously through single medication formulations.

Biosimilar adoption accelerates as healthcare systems seek cost-effective alternatives to branded insulin products. MWR analysis indicates biosimilar penetration reaching 30% market share in insulin segments as prescriber confidence and patient acceptance continue improving through clinical experience and regulatory validation.

Prevention-focused strategies expand market opportunities beyond traditional diabetes treatment to include pre-diabetes interventions and risk reduction therapies. Early intervention approaches create new market segments while potentially reducing long-term healthcare costs through disease progression prevention.

Regulatory milestone achievements include FDA approvals for breakthrough diabetes therapies incorporating novel mechanisms of action and improved safety profiles. Fast-track designations accelerate innovative treatment availability while maintaining rigorous safety and efficacy standards through streamlined review processes.

Strategic partnerships between pharmaceutical companies and technology firms create integrated diabetes management solutions combining medications with digital health platforms. Collaboration initiatives leverage complementary expertise to develop comprehensive care ecosystems addressing multiple aspects of diabetes management simultaneously.

Manufacturing capacity expansions respond to growing market demand while ensuring supply chain resilience and quality assurance. Biosimilar production facilities increase competitive alternatives availability while maintaining therapeutic equivalence standards through advanced manufacturing technologies.

Clinical trial innovations incorporate real-world evidence generation and patient-reported outcomes to demonstrate therapeutic value beyond traditional efficacy metrics. Outcomes-based research supports value-based care initiatives while providing evidence for optimal treatment selection and healthcare resource allocation.

Market access initiatives include patient assistance programs, insurance coverage expansions, and pricing transparency measures addressing affordability concerns. Healthcare equity programs target underserved populations while creating sustainable business models for comprehensive diabetes care delivery.

Investment priorities should focus on innovative drug development programs addressing unmet medical needs while maintaining competitive positioning in established therapeutic categories. Research and development allocation requires balanced approaches between breakthrough therapy development and lifecycle management of existing product portfolios.

Market expansion strategies should emphasize digital health integration and personalized medicine capabilities to differentiate products in increasingly competitive markets. Technology partnerships enable comprehensive diabetes management solutions while creating barriers to competitive entry through integrated care platforms.

Regulatory compliance remains critical as FDA oversight intensifies for diabetes medications with emphasis on real-world safety monitoring and post-market surveillance. Quality assurance investments ensure manufacturing excellence while supporting regulatory submissions for new product approvals and market expansions.

Pricing strategies must balance revenue optimization with market access requirements and competitive pressures from generic alternatives. Value-based pricing models align pharmaceutical costs with patient outcomes while demonstrating economic value to healthcare payers and providers.

Geographic expansion opportunities exist in underserved regions and specialized patient populations requiring targeted marketing approaches and culturally appropriate treatment solutions. Healthcare partnership development enables market penetration while addressing access barriers through collaborative care delivery models.

Market trajectory indicates sustained growth driven by increasing diabetes prevalence, aging demographics, and continuous therapeutic innovation. Growth projections suggest the market will maintain robust expansion with approximately 7.5% CAGR through the next decade as new patient populations enter treatment protocols and existing patients require advanced therapeutic interventions.

Technology integration will fundamentally reshape diabetes care delivery through artificial intelligence-driven treatment optimization, automated insulin delivery systems, and predictive analytics for complication prevention. Smart therapeutics incorporating glucose-responsive mechanisms represent revolutionary advancement opportunities that could transform diabetes management paradigms.

Regulatory evolution will likely emphasize real-world evidence requirements and outcomes-based approvals while maintaining safety standards through enhanced post-market surveillance. FDA initiatives supporting innovative diabetes care solutions will accelerate breakthrough therapy availability while ensuring patient safety through comprehensive monitoring systems.

Competitive dynamics will intensify as biosimilar alternatives expand across insulin categories while innovative drug classes capture premium market segments. Market consolidation may occur as smaller companies seek strategic partnerships or acquisitions to compete effectively in increasingly complex and capital-intensive diabetes care markets.

Patient empowerment trends will drive demand for personalized treatment options, transparent pricing, and comprehensive support services. Healthcare consumerism influences will reshape pharmaceutical marketing strategies while creating opportunities for direct patient engagement and education initiatives that improve treatment outcomes and brand loyalty.

The US diabetes care drugs market stands as a cornerstone of American healthcare, demonstrating remarkable resilience and growth potential driven by increasing disease prevalence and continuous therapeutic innovation. Market dynamics reflect a complex interplay of clinical needs, regulatory requirements, competitive pressures, and technological advancement that collectively create both challenges and opportunities for industry participants.

Strategic positioning within this market requires comprehensive understanding of diverse patient populations, evolving treatment paradigms, and emerging technology integration opportunities. Companies that successfully balance innovation investments with market access initiatives while maintaining competitive pricing will capture the greatest market share and sustainable growth opportunities.

Future success in the US diabetes care drugs market will depend on adaptability to changing healthcare landscapes, commitment to patient-centered solutions, and strategic partnerships that leverage complementary capabilities. The convergence of pharmaceuticals, digital health, and personalized medicine creates unprecedented opportunities for companies willing to invest in comprehensive diabetes care ecosystems that address the full spectrum of patient needs and healthcare provider requirements.

What is Diabetes Care Drugs?

Diabetes Care Drugs refer to medications used to manage diabetes, including insulin and oral hypoglycemic agents. These drugs help regulate blood sugar levels and prevent complications associated with diabetes.

What are the key players in the US Diabetes Care Drugs Market?

Key players in the US Diabetes Care Drugs Market include companies like Novo Nordisk, Sanofi, and Eli Lilly. These companies are known for their innovative diabetes treatments and extensive product portfolios, among others.

What are the main drivers of growth in the US Diabetes Care Drugs Market?

The main drivers of growth in the US Diabetes Care Drugs Market include the rising prevalence of diabetes, increasing awareness about diabetes management, and advancements in drug formulations. Additionally, the growing aging population contributes to the demand for effective diabetes care solutions.

What challenges does the US Diabetes Care Drugs Market face?

The US Diabetes Care Drugs Market faces challenges such as high drug costs, regulatory hurdles, and competition from generic medications. These factors can impact accessibility and affordability for patients requiring diabetes management.

What opportunities exist in the US Diabetes Care Drugs Market?

Opportunities in the US Diabetes Care Drugs Market include the development of new drug formulations, the integration of digital health technologies, and personalized medicine approaches. These innovations can enhance patient outcomes and improve adherence to treatment.

What trends are shaping the US Diabetes Care Drugs Market?

Trends shaping the US Diabetes Care Drugs Market include the increasing use of continuous glucose monitoring systems, the rise of biosimilars, and a focus on patient-centric care. These trends reflect a shift towards more effective and personalized diabetes management strategies.

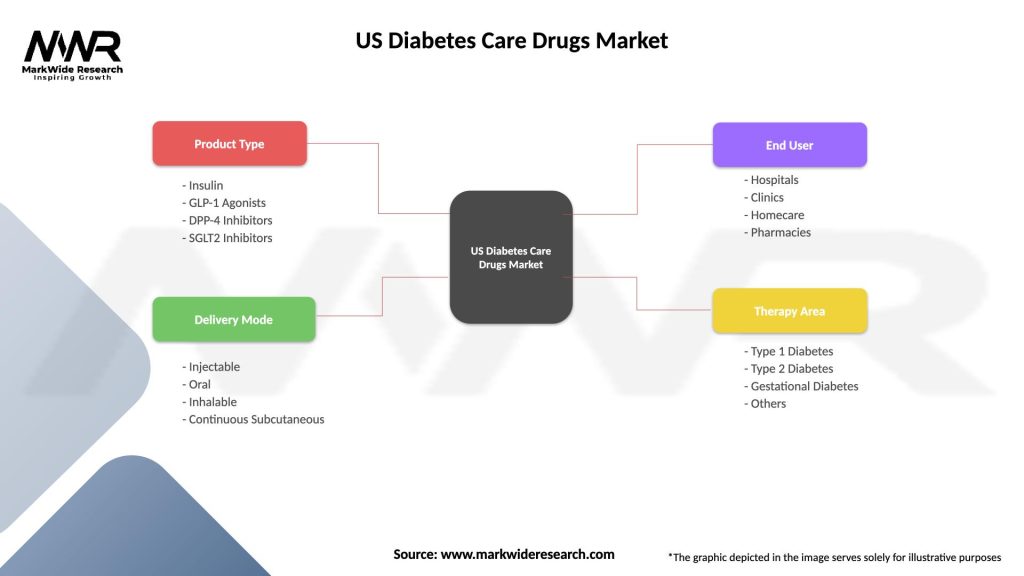

US Diabetes Care Drugs Market

| Segmentation Details | Description |

|---|---|

| Product Type | Insulin, GLP-1 Agonists, DPP-4 Inhibitors, SGLT2 Inhibitors |

| Delivery Mode | Injectable, Oral, Inhalable, Continuous Subcutaneous |

| End User | Hospitals, Clinics, Homecare, Pharmacies |

| Therapy Area | Type 1 Diabetes, Type 2 Diabetes, Gestational Diabetes, Others |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the US Diabetes Care Drugs Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.