444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Uruguay life and non-life insurance market represents a dynamic and evolving sector within South America’s financial services landscape. This comprehensive market encompasses various insurance products including life insurance, property insurance, automobile coverage, health insurance, and commercial lines. Uruguay’s insurance sector has demonstrated remarkable resilience and growth potential, driven by increasing consumer awareness, regulatory improvements, and economic stability.

Market dynamics in Uruguay reflect a mature insurance environment with significant penetration rates compared to regional peers. The country’s stable political climate and robust regulatory framework have fostered confidence among both domestic and international insurance providers. Insurance penetration in Uruguay currently stands at approximately 3.2% of GDP, positioning it as one of the more developed insurance markets in Latin America.

Digital transformation initiatives have accelerated across the Uruguayan insurance landscape, with companies investing heavily in technology infrastructure and customer-centric solutions. The market is experiencing a shift toward omnichannel distribution strategies, combining traditional agency networks with digital platforms to enhance customer accessibility and service delivery.

Regulatory evolution continues to shape market development, with the Superintendencia de Servicios Financieros implementing progressive policies that promote competition while ensuring consumer protection. These regulatory enhancements have contributed to increased market transparency and operational efficiency across the insurance value chain.

The Uruguay life and non-life insurance market refers to the comprehensive ecosystem of insurance products and services offered within Uruguay’s borders, encompassing both individual and commercial coverage solutions. This market includes life insurance policies that provide financial protection against mortality risks, alongside non-life insurance products covering property, casualty, health, and specialty risks.

Life insurance components within this market include term life policies, whole life insurance, universal life products, and group life coverage typically provided through employer-sponsored programs. These products serve to protect beneficiaries against financial hardship resulting from the policyholder’s death or disability.

Non-life insurance segments encompass a broader range of coverage areas including automobile insurance, property insurance for residential and commercial properties, health insurance plans, professional liability coverage, and specialized commercial lines such as marine and aviation insurance.

Market participants include domestic insurance companies, international insurers operating through subsidiaries or branches, mutual insurance organizations, and cooperative insurance entities. The distribution network comprises independent agents, brokers, bancassurance partnerships, and increasingly, direct-to-consumer digital channels.

Uruguay’s insurance market demonstrates strong fundamentals with consistent growth trajectories across both life and non-life segments. The market benefits from favorable demographic trends, including an aging population that drives demand for life insurance and retirement-related products, while urbanization and economic development fuel non-life insurance growth.

Key performance indicators reveal that the non-life insurance segment maintains a dominant position, accounting for approximately 78% of total premium volume, with automobile insurance representing the largest single line of business. Life insurance, while smaller in relative terms, shows promising growth potential driven by increased financial literacy and retirement planning awareness.

Technological advancement has emerged as a critical differentiator, with leading insurers implementing artificial intelligence, machine learning, and blockchain technologies to enhance underwriting accuracy, streamline claims processing, and improve customer experience. These innovations are contributing to operational efficiency gains of approximately 15-20% across various business processes.

Market consolidation trends are evident as larger players seek to achieve economies of scale and expand their product portfolios through strategic acquisitions and partnerships. This consolidation is expected to continue, potentially reducing the number of active market participants while strengthening the competitive position of remaining companies.

Strategic market insights reveal several fundamental trends shaping Uruguay’s insurance landscape. The following key insights provide comprehensive understanding of market dynamics:

Primary market drivers propelling growth in Uruguay’s insurance sector stem from multiple interconnected factors. Economic development and rising disposable incomes have created a more insurance-aware population with greater capacity to purchase coverage products.

Regulatory support continues to drive market expansion through progressive policies that encourage competition while maintaining stability. The government’s commitment to financial sector development has resulted in streamlined licensing procedures and enhanced consumer protection frameworks that boost market confidence.

Demographic transitions represent a significant growth catalyst, particularly the aging population’s increasing demand for life insurance and retirement planning products. Additionally, urbanization trends drive property insurance demand as more citizens acquire real estate assets requiring protection.

Technology integration serves as a powerful market driver, enabling insurers to reach previously underserved segments through digital channels while reducing operational costs. Mobile insurance applications and online policy management platforms have expanded market accessibility significantly.

Economic diversification efforts have created new commercial insurance opportunities as businesses expand into emerging sectors. The growth of tourism, renewable energy, and technology industries generates demand for specialized insurance products tailored to these sectors’ unique risk profiles.

Financial literacy initiatives promoted by both government and private sector organizations have increased consumer understanding of insurance benefits, leading to higher penetration rates across various product categories.

Market constraints within Uruguay’s insurance sector present challenges that require strategic navigation by industry participants. Limited market size relative to regional neighbors constrains growth potential and may limit economies of scale for domestic insurers.

Economic volatility in neighboring countries can impact Uruguay’s insurance market through reduced cross-border business opportunities and potential currency fluctuation effects. Regional economic instability may also affect reinsurance costs and availability.

Regulatory complexity occasionally creates operational challenges, particularly for smaller insurers lacking extensive compliance resources. Evolving regulatory requirements demand continuous investment in systems and personnel to ensure adherence.

Competition intensity from well-capitalized international insurers can pressure domestic companies’ market share and profitability. Foreign entrants often possess superior technology platforms and broader product portfolios that challenge local competitors.

Cultural factors may limit insurance adoption in certain demographic segments, where traditional risk management approaches persist. Overcoming these cultural barriers requires sustained education and awareness campaigns.

Talent shortage in specialized insurance disciplines, particularly actuarial science and risk management, can constrain innovation and growth initiatives. The limited pool of experienced insurance professionals may increase recruitment and retention costs.

Significant opportunities exist within Uruguay’s insurance market for companies positioned to capitalize on emerging trends and underserved segments. The growing middle class represents a substantial opportunity for life insurance expansion, particularly in the group insurance and employee benefits sectors.

Digital transformation creates opportunities for insurtech innovation, including usage-based insurance models, peer-to-peer insurance platforms, and artificial intelligence-driven underwriting solutions. Companies investing in these technologies can gain competitive advantages and access new customer segments.

Microinsurance development presents opportunities to serve lower-income populations with affordable, simplified insurance products. This segment remains largely untapped and could provide significant growth potential for innovative insurers.

Commercial lines expansion offers opportunities as Uruguay’s economy diversifies into new sectors requiring specialized insurance coverage. Cyber insurance, environmental liability, and professional indemnity products show particular promise.

Regional expansion opportunities exist for successful Uruguayan insurers to leverage their expertise in neighboring markets. The country’s stable regulatory environment and sophisticated insurance practices provide competitive advantages for international expansion.

Parametric insurance products represent emerging opportunities, particularly for agricultural and weather-related risks. These innovative products can address coverage gaps in traditional insurance offerings while providing more efficient claims settlement processes.

Market dynamics in Uruguay’s insurance sector reflect the interplay of various internal and external forces shaping industry evolution. MarkWide Research analysis indicates that competitive pressures are intensifying as market participants seek to differentiate their offerings through enhanced customer experience and innovative product development.

Pricing dynamics vary significantly across insurance lines, with automobile insurance experiencing competitive pressure that has compressed margins, while life insurance maintains more stable pricing structures. Market leaders are implementing sophisticated pricing models that incorporate big data analytics and predictive modeling to optimize profitability.

Distribution evolution represents a critical dynamic, with traditional agency networks adapting to compete with digital-first entrants. Successful insurers are developing hybrid distribution strategies that combine human expertise with digital convenience to serve diverse customer preferences.

Customer expectations continue evolving toward greater transparency, faster service delivery, and personalized product offerings. Insurers investing in customer experience improvements are achieving higher retention rates and premium growth compared to competitors maintaining traditional service models.

Reinsurance relationships play an increasingly important role in market dynamics, particularly for smaller domestic insurers seeking to expand their risk capacity. Strategic reinsurance partnerships enable local companies to compete more effectively with larger international players.

Regulatory dynamics continue influencing market structure through ongoing policy refinements aimed at enhancing consumer protection while promoting healthy competition. These regulatory changes require continuous adaptation by market participants.

Comprehensive research methodology employed in analyzing Uruguay’s life and non-life insurance market incorporates multiple data sources and analytical approaches to ensure accuracy and reliability. Primary research components include structured interviews with industry executives, regulatory officials, and key market participants.

Secondary research elements encompass analysis of regulatory filings, company annual reports, industry publications, and government statistical databases. This multi-source approach provides comprehensive market coverage and validates findings across different information channels.

Quantitative analysis utilizes statistical modeling techniques to identify market trends, growth patterns, and correlation factors affecting insurance demand. Time-series analysis helps project future market developments based on historical performance data.

Qualitative research methods include focus groups with insurance consumers, expert interviews with industry specialists, and case study analysis of successful market innovations. These qualitative insights provide context for quantitative findings and reveal underlying market dynamics.

Market segmentation analysis employs demographic, geographic, and behavioral criteria to identify distinct customer segments and their insurance preferences. This segmentation approach enables more precise market sizing and opportunity assessment.

Competitive intelligence gathering involves systematic monitoring of competitor activities, product launches, pricing strategies, and market positioning initiatives. This intelligence supports strategic recommendations and market opportunity identification.

Regional market distribution within Uruguay reveals distinct patterns reflecting population density, economic activity, and infrastructure development. Montevideo metropolitan area dominates insurance market activity, accounting for approximately 65% of total premium volume across both life and non-life segments.

Interior regions present unique characteristics with agricultural insurance playing a more prominent role, while coastal areas show higher demand for property insurance due to tourism-related commercial activities. These regional variations require tailored distribution strategies and product offerings.

Urban concentration in Montevideo creates both opportunities and challenges for insurers. While the concentration enables efficient distribution and service delivery, it also intensifies competition among market participants seeking to capture market share in this critical region.

Rural market development remains an area of significant potential, with agricultural producers requiring specialized coverage for crop, livestock, and equipment risks. However, serving these markets requires different distribution approaches and risk assessment methodologies.

Border region dynamics create unique cross-border insurance opportunities, particularly in areas with significant commercial activity between Uruguay and neighboring countries. These regions may require specialized products addressing international business risks.

Infrastructure development across different regions influences insurance demand patterns, with areas experiencing rapid development showing increased property and construction insurance requirements. Regional development initiatives continue creating new insurance opportunities.

Competitive landscape in Uruguay’s insurance market features a mix of domestic and international players competing across various segments. Market leadership positions vary by insurance line, with different companies excelling in specific product categories.

Market concentration shows moderate levels with the top five insurers controlling approximately 70% of market share, leaving room for smaller specialized players to compete in niche segments. This concentration level supports healthy competition while enabling economies of scale for leading participants.

Competitive strategies increasingly focus on digital transformation, customer experience enhancement, and product innovation. Successful competitors are investing heavily in technology infrastructure to improve operational efficiency and customer engagement capabilities.

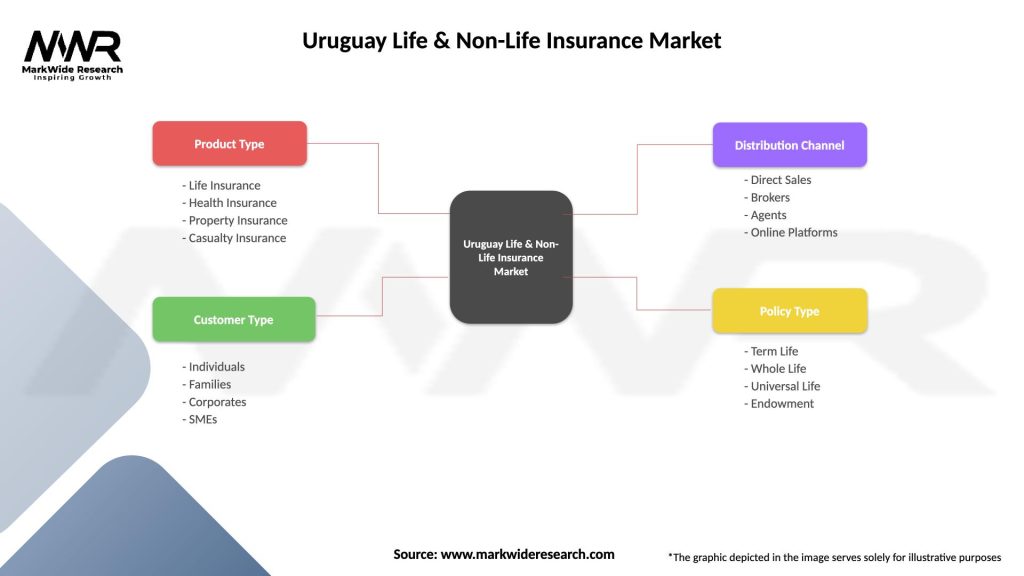

Market segmentation within Uruguay’s insurance sector reveals distinct categories based on product type, customer demographics, and distribution channels. Understanding these segments enables more targeted marketing strategies and product development initiatives.

By Product Type:

By Customer Segment:

By Distribution Channel:

Life insurance category demonstrates steady growth potential driven by demographic trends and increasing financial awareness. Term life products remain popular among younger demographics seeking affordable protection, while whole life and universal life products appeal to customers with longer-term financial planning objectives.

Group life insurance through employer-sponsored programs represents a significant growth opportunity as companies enhance employee benefit packages to attract and retain talent. This segment benefits from economies of scale and simplified underwriting processes.

Automobile insurance category faces ongoing challenges from competitive pricing pressure and evolving vehicle technologies. Usage-based insurance models utilizing telematics technology are gaining traction, offering more personalized pricing based on actual driving behavior.

Property insurance insights reveal growing demand for comprehensive coverage as property values increase and natural disaster awareness rises. Climate change considerations are influencing product design and pricing strategies across this category.

Health insurance category serves as a complement to Uruguay’s public healthcare system, with private health insurance providing additional coverage options and faster access to specialized medical services. This segment shows consistent growth as healthcare costs continue rising.

Commercial insurance categories reflect Uruguay’s economic diversification, with emerging sectors such as renewable energy and technology requiring specialized coverage solutions. Professional liability and cyber insurance represent high-growth subcategories within commercial lines.

Insurance companies operating in Uruguay’s market benefit from a stable regulatory environment that supports long-term business planning and investment decisions. The country’s strong rule of law and transparent regulatory framework reduce operational risks and enable predictable business operations.

Consumers benefit from increased competition that drives product innovation and competitive pricing across insurance categories. Enhanced consumer protection regulations ensure fair treatment and transparent policy terms, building trust in insurance products.

Economic stakeholders including banks, businesses, and government entities benefit from a robust insurance market that provides essential risk transfer mechanisms supporting economic growth and development. Insurance availability enables business expansion and investment by transferring potential losses to specialized risk bearers.

Reinsurance partners benefit from Uruguay’s sophisticated insurance market that generates quality business with strong underwriting standards and regulatory oversight. The market’s stability and growth potential make it attractive for international reinsurance capacity.

Technology providers find opportunities to serve insurance companies seeking digital transformation solutions. The market’s openness to innovation creates demand for insurtech solutions, data analytics platforms, and customer engagement technologies.

Professional service providers including actuaries, lawyers, and consultants benefit from the market’s complexity and regulatory requirements that create demand for specialized expertise and advisory services.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation trends continue reshaping Uruguay’s insurance landscape, with companies investing heavily in artificial intelligence, machine learning, and automation technologies. These investments are generating significant efficiency improvements and enabling more sophisticated risk assessment capabilities.

Customer experience enhancement has emerged as a critical competitive differentiator, with leading insurers implementing omnichannel strategies that seamlessly integrate digital and traditional touchpoints. Mobile applications and online policy management platforms are becoming standard offerings across the market.

Sustainability integration is gaining momentum as insurers incorporate environmental, social, and governance considerations into their business strategies. This trend includes sustainable investment practices, green insurance products, and climate risk assessment methodologies.

Parametric insurance development represents an innovative trend addressing traditional coverage gaps through index-based products that provide faster claims settlement and more transparent coverage terms. This approach is particularly relevant for agricultural and weather-related risks.

Collaborative ecosystem development involves partnerships between traditional insurers, insurtech startups, and technology providers to accelerate innovation and improve customer service delivery. These collaborations are creating new business models and distribution approaches.

Data analytics advancement enables more sophisticated underwriting, pricing, and customer segmentation strategies. Insurers leveraging advanced analytics are achieving better risk selection and improved profitability compared to competitors using traditional approaches.

Regulatory modernization initiatives have introduced enhanced consumer protection measures while streamlining operational requirements for insurance companies. Recent regulatory updates focus on improving market transparency and promoting fair competition among market participants.

Technology infrastructure investments by leading insurers have resulted in improved operational efficiency and customer service capabilities. MWR data indicates that companies investing in digital transformation are achieving customer satisfaction scores approximately 25% higher than industry averages.

Market consolidation activities include strategic acquisitions and partnerships aimed at achieving economies of scale and expanding product portfolios. These consolidation trends are expected to continue as companies seek competitive advantages through size and scope.

Product innovation developments encompass new insurance solutions addressing emerging risks such as cyber threats, climate change impacts, and sharing economy exposures. Innovative products are helping insurers differentiate their offerings and capture new market segments.

Distribution channel evolution includes expansion of bancassurance partnerships and development of direct-to-consumer digital platforms. These distribution innovations are improving market accessibility and reducing acquisition costs for insurance companies.

International expansion initiatives by successful Uruguayan insurers demonstrate growing confidence in leveraging domestic expertise for regional growth opportunities. These expansion efforts are creating new revenue streams and diversifying business risks.

Strategic recommendations for insurance companies operating in Uruguay emphasize the importance of digital transformation investments to remain competitive in an evolving market landscape. Companies should prioritize customer experience enhancement through technology integration and omnichannel service delivery.

Product development focus should address emerging customer needs and risk exposures, particularly in areas such as cyber insurance, climate-related coverage, and sharing economy risks. Innovation in product design can create competitive advantages and capture new market segments.

Distribution strategy optimization requires balancing traditional agency networks with digital channels to serve diverse customer preferences effectively. Successful companies will develop hybrid distribution models that leverage the strengths of both approaches.

Operational efficiency improvements through automation and process optimization can help companies maintain profitability in competitive market conditions. Investment in technology infrastructure and data analytics capabilities is essential for long-term success.

Risk management enhancement should incorporate climate change considerations and emerging risk exposures into underwriting and pricing strategies. Companies with superior risk assessment capabilities will achieve better underwriting results and profitability.

Talent development initiatives are crucial for building capabilities in digital technologies, data analytics, and emerging insurance disciplines. Companies investing in employee development will be better positioned to execute strategic initiatives successfully.

Future market prospects for Uruguay’s life and non-life insurance sector appear positive, supported by favorable demographic trends, economic stability, and ongoing digital transformation initiatives. MarkWide Research projections indicate continued growth across both life and non-life segments, with technology-enabled innovations driving market expansion.

Growth trajectory expectations suggest that the market will benefit from increasing insurance awareness, rising disposable incomes, and expanding commercial activity. Life insurance growth is expected to accelerate as the aging population drives demand for retirement planning and wealth transfer products.

Technology integration will continue transforming market dynamics, with artificial intelligence, blockchain, and Internet of Things technologies creating new opportunities for product innovation and operational efficiency. Companies successfully implementing these technologies will gain significant competitive advantages.

Regulatory evolution is expected to support market development through continued modernization efforts that balance consumer protection with industry growth objectives. Progressive regulatory policies will likely encourage innovation while maintaining market stability.

Market consolidation trends may accelerate as companies seek economies of scale and expanded capabilities through strategic partnerships and acquisitions. This consolidation could result in a more concentrated market structure with stronger competitive positions for remaining participants.

International expansion opportunities for successful Uruguayan insurers will likely increase as companies leverage their domestic expertise and stable regulatory environment to compete in regional markets. Cross-border growth initiatives could provide significant revenue diversification benefits.

Uruguay’s life and non-life insurance market represents a mature and stable sector with significant growth potential driven by favorable demographics, economic stability, and technological advancement. The market’s sophisticated regulatory framework and competitive landscape create an environment conducive to innovation and sustainable growth.

Key success factors for market participants include digital transformation capabilities, customer experience excellence, and operational efficiency optimization. Companies that successfully navigate these priorities while maintaining strong risk management practices will be well-positioned for future growth and profitability.

Market opportunities span across various segments, from traditional life and property insurance to emerging areas such as cyber coverage and parametric products. The ongoing evolution of customer expectations and risk exposures creates continuous opportunities for product innovation and market expansion.

Strategic positioning in Uruguay’s insurance market requires balancing traditional strengths with innovative approaches to meet evolving customer needs. Companies that effectively combine regulatory compliance, technological advancement, and customer-centric strategies will achieve sustainable competitive advantages in this dynamic market environment.

What is Life & Non-Life Insurance?

Life & Non-Life Insurance refers to the two main categories of insurance products. Life insurance provides financial protection to beneficiaries upon the policyholder’s death, while non-life insurance covers various risks such as property damage, liability, and health-related expenses.

What are the key players in the Uruguay Life & Non-Life Insurance Market?

Key players in the Uruguay Life & Non-Life Insurance Market include Banco de Seguros del Estado, Sancor Seguros, and Mapfre Uruguay, among others. These companies offer a range of insurance products catering to both individual and corporate clients.

What are the growth factors driving the Uruguay Life & Non-Life Insurance Market?

The growth of the Uruguay Life & Non-Life Insurance Market is driven by increasing awareness of insurance products, a growing middle class, and the rising need for financial security among individuals and businesses. Additionally, regulatory support and technological advancements are enhancing service delivery.

What challenges does the Uruguay Life & Non-Life Insurance Market face?

The Uruguay Life & Non-Life Insurance Market faces challenges such as regulatory compliance, competition from alternative financial products, and the need for digital transformation. Additionally, economic fluctuations can impact consumer spending on insurance.

What opportunities exist in the Uruguay Life & Non-Life Insurance Market?

Opportunities in the Uruguay Life & Non-Life Insurance Market include the expansion of digital insurance solutions, the introduction of innovative products tailored to specific consumer needs, and the potential for growth in underserved segments such as health and travel insurance.

What trends are shaping the Uruguay Life & Non-Life Insurance Market?

Trends shaping the Uruguay Life & Non-Life Insurance Market include the increasing adoption of insurtech solutions, a focus on customer-centric services, and the integration of sustainability practices in insurance offerings. These trends are influencing how companies engage with customers and manage risks.

Uruguay Life & Non-Life Insurance Market

| Segmentation Details | Description |

|---|---|

| Product Type | Life Insurance, Health Insurance, Property Insurance, Casualty Insurance |

| Customer Type | Individuals, Families, Corporates, SMEs |

| Distribution Channel | Direct Sales, Brokers, Agents, Online Platforms |

| Policy Type | Term Life, Whole Life, Universal Life, Endowment |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Uruguay Life & Non-Life Insurance Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.