444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview:

The insurance landscape in Uruguay encompasses both life and non-life insurance, offering a robust safety net to individuals and businesses alike. As a South American nation known for its stable economy and progressive financial sector, Uruguay’s insurance market plays a pivotal role in safeguarding against unexpected risks and uncertainties. This comprehensive overview delves into the key aspects of the Uruguay Life and Non-Life Insurance Market, shedding light on its meaning, executive summary, key market insights, drivers, restraints, opportunities, dynamics, regional analysis, competitive landscape, segmentation, category-wise insights, benefits, SWOT analysis, key trends, Covid-19 impact, industry developments, analyst suggestions, future outlook, and conclusion.

Meaning:

Life and non-life insurance in Uruguay refer to the range of financial services aimed at mitigating various types of risks. Life insurance provides a safety net for individuals and families by offering coverage in the event of death, disability, or other critical situations. Non-life insurance, on the other hand, includes property, liability, health, and automobile coverage, shielding policyholders from losses arising due to accidents, damage, or unexpected events.

Executive Summary:

The executive summary of the Uruguay Life and Non-Life Insurance Market encapsulates its pivotal role in the country’s financial ecosystem. The market provides individuals, businesses, and institutions with a cushion against unforeseen events, fostering economic stability and confidence. This summary offers a glimpse into the market’s size, growth trajectory, major players, and the impact of recent events such as the Covid-19 pandemic.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Several factors are driving the growth of the Uruguay Life and Non-Life Insurance Market:

Market Restraints

Despite the positive outlook, the Uruguay Life and Non-Life Insurance Market faces several challenges:

Market Opportunities

The Uruguay Life and Non-Life Insurance Market presents several opportunities for growth:

Market Dynamics

The Uruguay Life and Non-Life Insurance Market is shaped by several dynamics:

Regional Analysis

The Uruguay Life and Non-Life Insurance Market is primarily influenced by the economic and demographic conditions within the country:

Competitive Landscape

Leading Companies in Uruguay Life and Non-Life Insurance Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

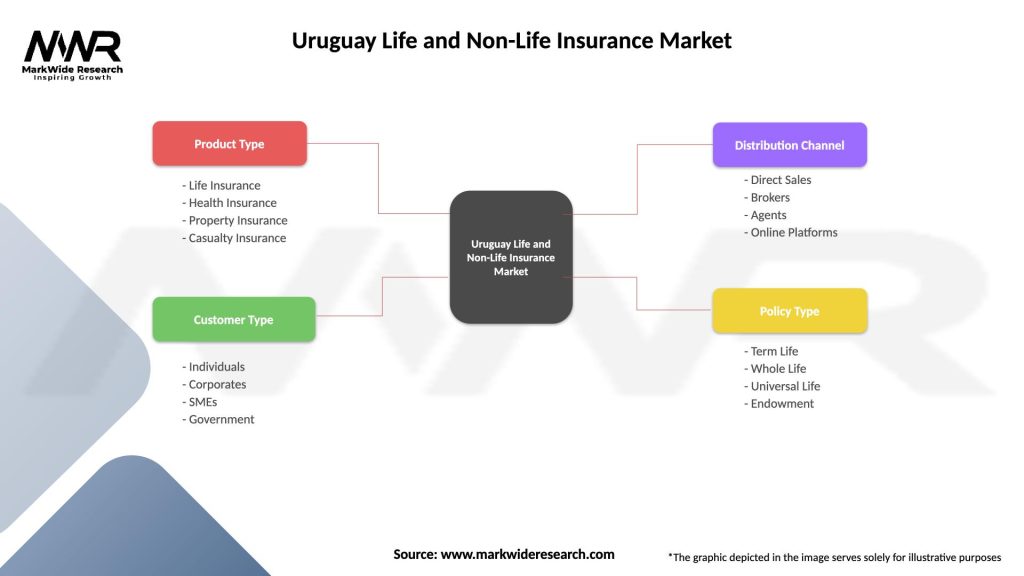

Segmentation

The Uruguay Life and Non-Life Insurance Market can be segmented by the following factors:

Type

Distribution Channel

End-User

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact:

The Covid-19 pandemic had a multifaceted impact on the Uruguay insurance market. While initial disruptions affected distribution and sales, the crisis underscored the importance of insurance in managing unexpected risks. The pandemic prompted insurers to enhance digital capabilities, expedite claims processing, and offer pandemic-specific coverage, thus adapting to the changing landscape.

Key Industry Developments:

Recent industry developments showcase the market’s adaptability. The integration of InsurTech solutions for smoother customer interactions and quicker claims settlement is a significant trend. Moreover, collaborations between insurers and other industries, such as healthcare, pave the way for holistic coverage options.

Analyst Suggestions:

Industry analysts recommend a multi-pronged approach for sustained growth. Enhancing financial literacy through educational initiatives can boost insurance adoption. Developing flexible insurance products that cater to evolving customer needs is essential. Moreover, leveraging emerging technologies for data-driven insights and personalized services can enhance customer engagement.

Future Outlook:

The future of the Uruguay insurance market is promising. Increasing awareness, coupled with a growing economy, is likely to drive penetration further. Insurers’ emphasis on innovative solutions and customer-centricity will shape the landscape. The integration of advanced technologies and a proactive response to emerging risks will define the sector’s trajectory.

Conclusion:

In conclusion, the Uruguay Life and Non-Life Insurance Market stand as pillars of financial stability in the nation. With a robust foundation, the market navigates challenges and opportunities, adapting to changing dynamics. As insurers continue to innovate and provide comprehensive coverage, individuals, businesses, and the economy at large can stride confidently into an uncertain future, shielded by the protective embrace of insurance.

What is Life and Non-Life Insurance?

Life and Non-Life Insurance refers to the two main categories of insurance products. Life insurance provides financial protection to beneficiaries upon the policyholder’s death, while non-life insurance covers various risks such as property damage, liability, and health-related expenses.

What are the key players in the Uruguay Life and Non-Life Insurance Market?

Key players in the Uruguay Life and Non-Life Insurance Market include Banco de Seguros del Estado, Sancor Seguros, and Mapfre Uruguay, among others. These companies offer a range of insurance products catering to both individual and corporate clients.

What are the growth factors driving the Uruguay Life and Non-Life Insurance Market?

The growth of the Uruguay Life and Non-Life Insurance Market is driven by increasing awareness of insurance benefits, a growing middle class, and the rising demand for health and property insurance. Additionally, regulatory support and economic stability contribute to market expansion.

What challenges does the Uruguay Life and Non-Life Insurance Market face?

The Uruguay Life and Non-Life Insurance Market faces challenges such as regulatory compliance, competition from informal insurance providers, and the need for digital transformation. These factors can hinder market growth and customer acquisition.

What opportunities exist in the Uruguay Life and Non-Life Insurance Market?

Opportunities in the Uruguay Life and Non-Life Insurance Market include the potential for product innovation, expansion into underserved regions, and the integration of technology to enhance customer experience. Insurers can also explore partnerships to broaden their service offerings.

What trends are shaping the Uruguay Life and Non-Life Insurance Market?

Trends shaping the Uruguay Life and Non-Life Insurance Market include the increasing adoption of digital platforms for policy management, a focus on personalized insurance products, and the growing importance of sustainability in insurance practices. These trends are influencing how companies engage with customers.

Uruguay Life and Non-Life Insurance Market

| Segmentation Details | Description |

|---|---|

| Product Type | Life Insurance, Health Insurance, Property Insurance, Casualty Insurance |

| Customer Type | Individuals, Corporates, SMEs, Government |

| Distribution Channel | Direct Sales, Brokers, Agents, Online Platforms |

| Policy Type | Term Life, Whole Life, Universal Life, Endowment |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in Uruguay Life and Non-Life Insurance Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.