444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The United States residential smart meters market represents a transformative segment within the nation’s energy infrastructure modernization efforts. Smart meters have emerged as critical components in the transition toward intelligent energy management systems, enabling two-way communication between utilities and consumers. The market demonstrates robust growth momentum driven by federal initiatives, state-level mandates, and increasing consumer awareness of energy efficiency benefits.

Market dynamics indicate substantial expansion across residential sectors, with deployment rates accelerating significantly over the past decade. The technology enables real-time energy consumption monitoring, demand response capabilities, and enhanced grid reliability. Utility companies across the United States are increasingly investing in smart meter infrastructure to modernize aging grid systems and improve operational efficiency.

Regional adoption patterns vary considerably, with states like California, Texas, and Florida leading deployment initiatives. The market benefits from supportive regulatory frameworks, including the Energy Policy Act and various state-level renewable energy standards. Growth projections suggest continued expansion at a compound annual growth rate of 8.2% through the forecast period, reflecting sustained investment in grid modernization programs.

The United States residential smart meters market refers to the comprehensive ecosystem encompassing the development, manufacturing, deployment, and maintenance of advanced metering infrastructure specifically designed for residential energy consumption monitoring and management across American households.

Smart meters represent sophisticated electronic devices that measure electricity, gas, or water consumption in real-time and communicate this information digitally to utility providers. Unlike traditional analog meters, these devices enable bidirectional communication, allowing utilities to remotely monitor usage patterns, detect outages, and implement dynamic pricing structures. The technology incorporates advanced features including automated meter reading, load profiling capabilities, and integration with home energy management systems.

Market participants include meter manufacturers, utility companies, technology integrators, and software providers who collectively contribute to the smart grid ecosystem. The residential focus distinguishes this market from commercial and industrial smart meter segments, addressing the unique requirements of single-family homes, apartments, and residential complexes throughout the United States.

Market leadership in the United States residential smart meters sector reflects the nation’s commitment to energy infrastructure modernization and grid reliability enhancement. The market has experienced unprecedented growth driven by federal funding programs, state regulatory mandates, and increasing consumer demand for energy transparency and control.

Key market drivers include the Infrastructure Investment and Jobs Act funding allocations, which dedicate 65% of grid modernization resources to smart meter deployment initiatives. Utility companies are leveraging these investments to replace aging mechanical meters with advanced digital alternatives, creating substantial market opportunities for technology providers and system integrators.

Competitive dynamics feature established players including Itron, Landis+Gyr, Honeywell, and Sensus competing alongside emerging technology companies specializing in IoT-enabled metering solutions. The market demonstrates strong consolidation trends as utilities seek comprehensive smart grid solutions from integrated providers.

Regional variations in deployment strategies reflect diverse regulatory environments and utility structures across states. California leads with 92% residential smart meter penetration, while emerging markets in the Southeast and Midwest present significant growth opportunities for market participants.

Strategic insights reveal several critical trends shaping the United States residential smart meters market landscape:

Primary market drivers propelling the United States residential smart meters market include comprehensive federal policy support, state-level regulatory mandates, and evolving consumer energy management preferences. The Infrastructure Investment and Jobs Act provides unprecedented funding for grid modernization initiatives, creating substantial opportunities for smart meter deployment across residential sectors.

Utility modernization requirements represent another significant driver as aging infrastructure necessitates replacement with advanced digital alternatives. Many utilities operate meter assets installed decades ago, requiring systematic upgrades to maintain reliability and regulatory compliance. Operational efficiency gains from smart meter deployment include reduced manual reading costs, improved outage detection, and enhanced customer service capabilities.

Environmental sustainability initiatives drive market growth as smart meters enable more effective energy conservation programs and renewable energy integration. Utilities utilize smart meter data to implement time-of-use pricing structures that encourage off-peak consumption and reduce overall system demand. The technology supports distributed energy resource management including rooftop solar installations and battery storage systems.

Consumer demand for energy transparency and control continues expanding as households seek greater visibility into consumption patterns and costs. Smart meters enable real-time usage monitoring through mobile applications and web portals, empowering consumers to make informed energy decisions. Home automation integration capabilities further enhance value propositions for tech-savvy residential customers.

Significant market restraints challenge the United States residential smart meters market despite overall positive growth trends. High upfront capital requirements for comprehensive smart meter deployment programs create financial barriers for smaller utility companies and rural cooperatives with limited resources. The technology requires substantial investments in communication infrastructure, data management systems, and workforce training programs.

Consumer privacy concerns represent persistent challenges as residential customers express apprehension about detailed energy usage data collection and potential surveillance implications. Cybersecurity vulnerabilities in connected meter systems create additional concerns among consumers and regulators regarding potential data breaches and grid security threats.

Regulatory complexity across different state jurisdictions creates implementation challenges for utilities operating in multiple markets. Varying approval processes, rate recovery mechanisms, and technical standards complicate deployment strategies and increase administrative costs. Rate case proceedings for smart meter cost recovery can extend project timelines and create uncertainty for market participants.

Technical integration challenges arise when implementing smart meters within existing utility infrastructure systems. Legacy billing systems, customer information platforms, and operational technology require significant upgrades to fully leverage smart meter capabilities. Interoperability issues between different vendor solutions can limit deployment flexibility and increase long-term maintenance costs.

Substantial market opportunities emerge from the convergence of federal infrastructure investments, state clean energy mandates, and advancing smart grid technologies. The Inflation Reduction Act provides additional funding mechanisms for grid modernization projects, creating expanded opportunities for smart meter deployment in previously underserved markets.

Rural electrification programs present significant growth potential as federal initiatives target smart meter deployment in rural and remote communities. These markets often lack modern metering infrastructure, creating opportunities for comprehensive system upgrades. Cooperative utilities increasingly recognize smart meter benefits for operational efficiency and member services enhancement.

Electric vehicle integration creates new market opportunities as smart meters enable sophisticated charging management and grid integration capabilities. Utilities leverage smart meter data to implement managed charging programs that optimize grid impacts and provide cost savings for residential customers. The growing EV adoption rate of 12% annually expands market potential for advanced metering solutions.

Energy storage integration opportunities expand as residential battery systems become more affordable and widespread. Smart meters facilitate virtual power plant programs that aggregate distributed storage resources for grid services. Demand response programs enabled by smart meters provide utilities with flexible load management tools while offering financial incentives to participating residential customers.

Market dynamics in the United States residential smart meters sector reflect complex interactions between technological advancement, regulatory evolution, and changing consumer expectations. Competitive pressures drive continuous innovation in meter functionality, communication capabilities, and data analytics features.

Supply chain considerations significantly impact market dynamics as global semiconductor shortages and manufacturing constraints affect meter production and deployment timelines. Domestic manufacturing initiatives gain momentum as utilities and policymakers prioritize supply chain resilience and reduced dependence on international suppliers.

Technological convergence creates dynamic market conditions as smart meters increasingly integrate with broader IoT ecosystems and home automation platforms. Edge computing capabilities enable advanced local processing and reduce communication bandwidth requirements. The integration of machine learning algorithms enhances predictive maintenance capabilities and system optimization.

Partnership dynamics evolve as utilities collaborate with technology companies, data analytics firms, and customer engagement specialists to maximize smart meter value propositions. MarkWide Research analysis indicates that strategic partnerships account for 43% of successful smart meter deployments, highlighting the importance of collaborative approaches in market development.

Comprehensive research methodology employed for analyzing the United States residential smart meters market incorporates multiple data sources and analytical approaches to ensure accuracy and reliability. Primary research activities include extensive interviews with utility executives, meter manufacturers, regulatory officials, and technology providers across diverse market segments.

Secondary research components encompass analysis of regulatory filings, utility rate cases, industry reports, and government databases to establish market sizing and trend analysis. Quantitative analysis utilizes statistical modeling techniques to project market growth patterns and identify key performance indicators across regional markets.

Data validation processes ensure information accuracy through cross-referencing multiple sources and conducting follow-up interviews with key market participants. Market segmentation analysis examines deployment patterns across utility types, geographic regions, and technology categories to provide comprehensive market insights.

Forecasting methodologies incorporate scenario analysis considering various regulatory, technological, and economic factors that may influence market development. Expert validation processes involve review by industry specialists and academic researchers to ensure analytical rigor and market relevance.

Regional market analysis reveals significant variations in smart meter adoption patterns across the United States, reflecting diverse regulatory environments, utility structures, and consumer demographics. Western states lead market development with California achieving 92% residential penetration and supporting policies that mandate smart meter deployment for investor-owned utilities.

Texas market dynamics demonstrate unique characteristics due to the state’s deregulated electricity market structure. Retail electric providers leverage smart meter data for competitive differentiation and customer engagement programs. The state’s ERCOT grid operator utilizes smart meter infrastructure for enhanced demand response and grid reliability programs.

Southeastern regional markets present substantial growth opportunities as states including Florida, Georgia, and North Carolina accelerate smart meter deployment initiatives. Hurricane resilience considerations drive utility investments in advanced metering infrastructure that enables faster outage detection and restoration capabilities.

Northeastern markets focus on smart meter integration with energy efficiency programs and renewable energy initiatives. States like Massachusetts and Connecticut leverage smart meters for Green Button data sharing programs and advanced rate structures. Cold climate considerations influence meter design requirements and deployment strategies in northern regions.

Midwest and Mountain West regions demonstrate growing market activity as rural cooperatives and municipal utilities recognize smart meter benefits for operational efficiency and member services. Agricultural load management applications create unique market opportunities in farming communities.

Competitive landscape analysis reveals a concentrated market structure with several established players dominating the United States residential smart meters sector. Market leadership positions reflect companies’ technological capabilities, manufacturing scale, and utility relationship strength.

Competitive strategies emphasize technological differentiation, comprehensive service offerings, and strategic utility partnerships. Innovation focus areas include advanced analytics capabilities, cybersecurity enhancements, and integration with emerging grid technologies.

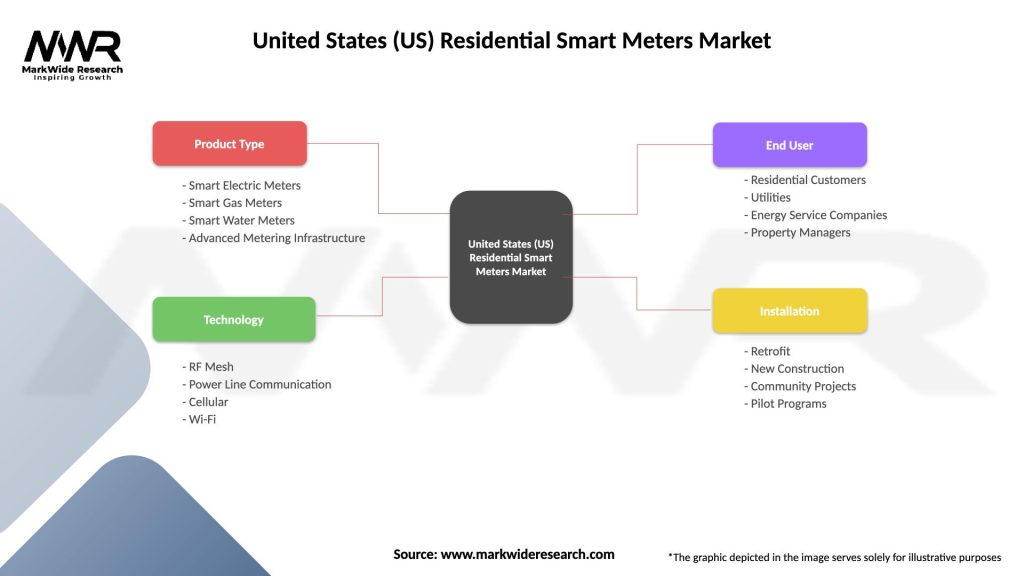

Market segmentation analysis provides detailed insights into the United States residential smart meters market structure across multiple dimensions including technology type, communication method, and utility category.

By Technology Type:

By Communication Technology:

By Utility Type:

Advanced Metering Infrastructure (AMI) represents the dominant technology category, accounting for 76% of new residential deployments due to comprehensive functionality and utility operational benefits. AMI systems enable sophisticated demand response programs, outage management, and customer engagement applications that justify higher implementation costs.

Communication technology preferences vary significantly across regional markets and utility types. RF mesh networks dominate urban and suburban deployments due to reliability and scalability advantages. Cellular communication gains traction in rural markets where mesh network coverage proves challenging or cost-prohibitive.

Investor-owned utilities lead smart meter adoption with comprehensive deployment programs supported by regulatory cost recovery mechanisms. These utilities typically implement system-wide upgrades affecting millions of residential customers simultaneously. Rate case approvals provide funding certainty that enables large-scale procurement and deployment initiatives.

Rural electric cooperatives demonstrate increasing smart meter adoption as federal funding programs and technology cost reductions improve project economics. Cooperative governance structures require member approval for significant infrastructure investments, creating unique market dynamics and decision-making processes.

Municipal utilities often pioneer innovative smart meter applications due to local control and community focus. These utilities frequently implement pilot programs that test advanced features before broader market adoption. Public ownership enables flexible deployment strategies and community-specific customization.

Utility companies realize substantial operational benefits from residential smart meter deployment including reduced manual reading costs, improved outage detection capabilities, and enhanced customer service delivery. Operational efficiency gains typically range from 15-25% in meter reading and customer service functions. Grid reliability improvements result from real-time monitoring capabilities and faster fault detection systems.

Residential customers benefit from increased energy awareness, consumption control, and access to innovative rate structures that can reduce electricity costs. Energy savings from smart meter-enabled programs average 2-5% of annual consumption through behavioral changes and efficiency improvements. Convenience benefits include elimination of estimated bills and remote service connections.

Technology providers access expanding market opportunities as utilities modernize aging infrastructure and implement advanced grid technologies. Recurring revenue streams from maintenance, software licensing, and data analytics services provide sustainable business models beyond initial hardware sales.

Regulatory agencies leverage smart meter data for improved market oversight, consumer protection, and grid reliability monitoring. Policy implementation benefits include enhanced ability to track renewable energy integration, demand response program effectiveness, and energy efficiency initiative outcomes.

Environmental stakeholders support smart meter deployment as enabling technology for renewable energy integration, demand response programs, and overall grid efficiency improvements that reduce carbon emissions and environmental impacts.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial intelligence integration emerges as a dominant trend transforming smart meter capabilities and utility operations. Machine learning algorithms enable predictive analytics for equipment maintenance, load forecasting, and customer behavior analysis. AI-powered applications enhance grid optimization and demand response program effectiveness.

Edge computing deployment gains momentum as utilities seek to process smart meter data locally rather than transmitting all information to central systems. Edge analytics reduce communication bandwidth requirements while enabling real-time decision-making capabilities. This trend supports grid resilience and reduces dependence on centralized data processing infrastructure.

Blockchain technology adoption for secure data management and peer-to-peer energy trading applications represents an emerging trend in advanced smart meter systems. Distributed ledger technology enables secure transaction processing and enhanced cybersecurity for residential energy markets.

5G communication integration creates opportunities for enhanced smart meter connectivity and advanced applications requiring high-speed data transmission. Ultra-low latency 5G networks support real-time grid control applications and improved customer engagement platforms.

Sustainability focus drives development of environmentally friendly smart meters with reduced material usage, improved recyclability, and extended operational lifespans. Circular economy principles influence meter design and end-of-life management strategies.

Recent industry developments highlight accelerating innovation and market expansion across the United States residential smart meters sector. Major utility deployments continue expanding with several multi-million meter programs reaching completion phases and demonstrating successful implementation outcomes.

Technology partnerships between traditional meter manufacturers and software companies create comprehensive solutions addressing utility operational requirements and customer engagement needs. Strategic acquisitions consolidate market capabilities and expand geographic coverage for leading industry participants.

Regulatory developments include updated cybersecurity standards, data privacy requirements, and interoperability mandates that influence product development and deployment strategies. Federal funding programs continue providing financial support for smart meter initiatives in underserved communities and rural markets.

Innovation initiatives focus on advanced analytics capabilities, enhanced cybersecurity features, and integration with emerging grid technologies including energy storage and electric vehicle charging systems. Pilot programs test next-generation meter capabilities and validate new business models for utility operations.

International expansion by US-based companies creates opportunities for technology export and global market development, while foreign companies establish North American operations to access growing domestic markets.

Strategic recommendations for market participants emphasize the importance of comprehensive cybersecurity capabilities, interoperability standards compliance, and customer engagement platform development. MWR analysis suggests that companies prioritizing these areas achieve higher customer satisfaction rates and stronger utility partnerships.

Investment priorities should focus on research and development activities that enhance meter functionality, reduce manufacturing costs, and improve deployment efficiency. Technology differentiation becomes increasingly important as market competition intensifies and utilities seek advanced capabilities beyond basic metering functions.

Partnership strategies with software companies, data analytics firms, and customer engagement specialists provide opportunities to offer comprehensive solutions that address evolving utility requirements. Vertical integration considerations should balance control benefits against flexibility and innovation advantages from specialized partnerships.

Geographic expansion opportunities exist in underserved rural markets and states with developing smart meter programs. Market entry strategies should consider local regulatory requirements, utility preferences, and competitive dynamics when establishing regional presence.

Long-term planning must account for emerging technologies including artificial intelligence, edge computing, and 5G communications that will influence future meter requirements and capabilities. Technology roadmap development ensures product evolution aligns with market needs and regulatory trends.

Future market prospects for the United States residential smart meters sector remain highly positive, driven by sustained federal infrastructure investments, advancing grid modernization requirements, and evolving consumer energy management preferences. Market expansion is projected to continue at a robust pace of 8.2% CAGR through the next decade as utilities complete comprehensive deployment programs.

Technology evolution will focus on enhanced artificial intelligence capabilities, improved cybersecurity features, and seamless integration with emerging grid technologies. Next-generation meters will incorporate advanced edge computing capabilities that enable sophisticated local processing and real-time grid optimization functions.

Regulatory developments are expected to strengthen cybersecurity requirements, enhance consumer data protection standards, and promote interoperability across diverse utility systems. Federal policy support will likely continue through additional infrastructure funding programs and clean energy initiatives.

Market consolidation trends may accelerate as utilities seek comprehensive smart grid solutions from integrated providers capable of delivering end-to-end capabilities. Strategic partnerships and acquisitions will shape competitive dynamics and technology development priorities.

MarkWide Research projects that residential smart meter penetration will reach 85% of US households by 2030, representing substantial market opportunities for technology providers and service companies. Rural market development will contribute significantly to this growth as federal funding programs address previously underserved communities.

The United States residential smart meters market represents a dynamic and rapidly expanding sector within the nation’s energy infrastructure modernization landscape. Strong fundamentals including federal policy support, utility modernization requirements, and advancing technology capabilities create sustained growth opportunities for market participants across the value chain.

Market leadership will increasingly depend on companies’ ability to deliver comprehensive solutions that address utility operational needs, regulatory requirements, and consumer expectations. Technology differentiation through artificial intelligence integration, enhanced cybersecurity, and advanced analytics capabilities will determine competitive success in evolving market conditions.

Regional market variations provide diverse opportunities for strategic expansion and technology deployment, while federal infrastructure investments create unprecedented funding availability for smart meter programs. Stakeholder benefits across utilities, consumers, and technology providers support continued market development and innovation initiatives.

The future outlook remains highly positive as the United States continues its transition toward a modernized, intelligent electrical grid that leverages smart meter technology as a foundational element for enhanced reliability, efficiency, and sustainability in residential energy management.

What is Residential Smart Meters?

Residential smart meters are advanced devices that measure electricity, gas, or water consumption in homes. They provide real-time data to consumers and utility companies, enabling better energy management and efficiency.

What are the key players in the United States (US) Residential Smart Meters Market?

Key players in the United States (US) Residential Smart Meters Market include Itron, Landis+Gyr, and Sensus, among others. These companies are known for their innovative technologies and solutions in smart metering.

What are the growth factors driving the United States (US) Residential Smart Meters Market?

The growth of the United States (US) Residential Smart Meters Market is driven by increasing demand for energy efficiency, government initiatives promoting smart grid technologies, and the rising adoption of renewable energy sources.

What challenges does the United States (US) Residential Smart Meters Market face?

The United States (US) Residential Smart Meters Market faces challenges such as high initial installation costs, cybersecurity concerns, and resistance from consumers regarding data privacy.

What opportunities exist in the United States (US) Residential Smart Meters Market?

Opportunities in the United States (US) Residential Smart Meters Market include advancements in IoT technology, the integration of smart home systems, and the potential for enhanced energy management solutions.

What trends are shaping the United States (US) Residential Smart Meters Market?

Trends in the United States (US) Residential Smart Meters Market include the increasing use of wireless communication technologies, the development of user-friendly mobile applications for monitoring consumption, and a growing focus on sustainability and energy conservation.

United States (US) Residential Smart Meters Market

| Segmentation Details | Description |

|---|---|

| Product Type | Smart Electric Meters, Smart Gas Meters, Smart Water Meters, Advanced Metering Infrastructure |

| Technology | RF Mesh, Power Line Communication, Cellular, Wi-Fi |

| End User | Residential Customers, Utilities, Energy Service Companies, Property Managers |

| Installation | Retrofit, New Construction, Community Projects, Pilot Programs |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the United States (US) Residential Smart Meters Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.