444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The United States sports promoter market represents a dynamic and rapidly evolving sector that serves as the backbone of America’s entertainment and sporting industries. Sports promoters play a crucial role in organizing, marketing, and executing sporting events ranging from local competitions to major league championships, creating substantial economic impact across multiple industries. The market encompasses various stakeholders including independent promoters, venue operators, talent agencies, and integrated entertainment companies that facilitate sporting events nationwide.

Market dynamics indicate robust growth driven by increasing consumer demand for live entertainment experiences, technological advancements in event management, and expanding digital marketing capabilities. The sector demonstrates remarkable resilience and adaptability, with promoters leveraging innovative approaches to engage audiences and maximize revenue streams. Growth projections suggest the market will expand at a compound annual growth rate (CAGR) of 6.2% through the forecast period, reflecting strong underlying demand for professional sports entertainment.

Regional distribution shows significant concentration in major metropolitan areas, with approximately 45% of promotional activities centered in top-tier markets including New York, Los Angeles, Chicago, and Dallas. The market benefits from America’s deeply ingrained sports culture, substantial disposable income levels, and sophisticated entertainment infrastructure that supports large-scale event production and promotion.

The United States sports promoter market refers to the comprehensive ecosystem of businesses, individuals, and organizations responsible for conceptualizing, organizing, marketing, and executing sporting events across various disciplines and competitive levels throughout the United States.

Sports promotion encompasses multiple interconnected activities including event planning, venue booking, talent acquisition, marketing campaigns, ticket sales, sponsorship development, media relations, and operational management. Professional promoters serve as intermediaries between athletes, venues, sponsors, media outlets, and audiences, creating value through strategic event development and audience engagement initiatives.

The market includes diverse promotional categories spanning professional leagues, amateur competitions, collegiate athletics, combat sports, motorsports, and specialty sporting events. Promotional activities extend beyond event execution to include brand development, athlete representation, venue partnerships, and comprehensive marketing strategies that maximize attendance, viewership, and commercial success.

Market analysis reveals the United States sports promoter market as a sophisticated and highly competitive sector characterized by significant growth potential and evolving consumer preferences. The industry demonstrates strong fundamentals supported by America’s passionate sports fanbase, substantial corporate sponsorship investments, and expanding digital engagement platforms that enhance promotional reach and effectiveness.

Key market drivers include rising consumer spending on entertainment experiences, technological innovations in event management and marketing, increasing corporate sponsorship budgets, and growing demand for premium live entertainment options. The sector benefits from approximately 78% of American adults regularly consuming sports content, creating substantial promotional opportunities across multiple channels and demographics.

Competitive landscape features a diverse mix of established entertainment conglomerates, specialized sports promotion companies, independent promoters, and emerging digital-first promotional platforms. Market leaders leverage integrated capabilities spanning event production, venue management, talent representation, and comprehensive marketing services to maintain competitive advantages and capture market share.

Future outlook indicates continued expansion driven by technological advancement, demographic shifts toward experiential consumption, and increasing integration between traditional sports promotion and digital entertainment platforms. The market is positioned for sustained growth as promoters adapt to evolving consumer preferences and leverage emerging technologies to enhance event experiences and operational efficiency.

Strategic analysis identifies several critical insights shaping the United States sports promoter market landscape and influencing future development trajectories:

Primary growth drivers propelling the United States sports promoter market include fundamental shifts in consumer behavior, technological advancement, and structural changes within the broader entertainment industry that create substantial promotional opportunities.

Consumer spending patterns demonstrate increasing allocation toward experiential purchases, with sports entertainment representing a significant portion of discretionary spending. Rising disposable income levels, particularly among key demographic segments, support premium ticket pricing and enhanced event experiences that generate higher promotional revenues and profit margins.

Corporate sponsorship investment continues expanding as businesses recognize sports promotion as an effective marketing channel for brand building, customer engagement, and market penetration. Companies increasingly view sporting events as platforms for comprehensive marketing campaigns that integrate traditional advertising, digital engagement, and experiential marketing strategies.

Technological innovation enables promoters to enhance operational efficiency, improve audience targeting, and create more engaging event experiences. Advanced data analytics, mobile applications, virtual reality integration, and social media platforms provide powerful tools for promotional campaigns and audience development initiatives.

Media landscape evolution creates new promotional opportunities through streaming platforms, social media channels, and digital content distribution networks. The proliferation of sports-focused media outlets and content platforms increases demand for promotional services and creates additional revenue streams for event promoters.

Significant challenges facing the United States sports promoter market include operational complexities, regulatory constraints, and competitive pressures that impact profitability and growth potential across various market segments.

High operational costs associated with venue rental, talent acquisition, marketing campaigns, and event production create substantial financial barriers, particularly for smaller promoters and emerging market entrants. Rising insurance costs, security requirements, and compliance expenses further increase operational overhead and reduce profit margins.

Regulatory complexity presents ongoing challenges as promoters navigate varying state and local regulations, licensing requirements, safety standards, and tax obligations. Evolving regulations regarding sports betting, athlete compensation, and event safety create compliance burdens that require specialized expertise and additional operational resources.

Market saturation in major metropolitan areas creates intense competition for premium venues, dates, and audience attention. Established promoters with long-term venue relationships and exclusive talent agreements maintain significant competitive advantages that limit opportunities for new market entrants.

Economic sensitivity affects consumer spending on entertainment and corporate sponsorship budgets during economic downturns, creating revenue volatility and planning challenges. Promotional success depends heavily on broader economic conditions and consumer confidence levels that remain outside promoter control.

Emerging opportunities within the United States sports promoter market reflect changing consumer preferences, technological advancement, and evolving industry structures that create new avenues for growth and innovation.

Digital transformation presents substantial opportunities for promoters to develop new revenue streams through virtual events, streaming partnerships, digital content creation, and enhanced fan engagement platforms. The integration of augmented reality, virtual reality, and interactive technologies creates possibilities for innovative event experiences and expanded audience reach.

Demographic shifts toward younger, more diverse audiences create opportunities for promoters to develop specialized events, alternative sports programming, and culturally relevant promotional campaigns. Growing interest in esports, extreme sports, and non-traditional competitive activities opens new market segments with significant growth potential.

Geographic expansion into underserved markets presents opportunities for promoters to establish operations in secondary and tertiary cities where competition remains limited and infrastructure development creates new venue options. Regional sports promotion can capture local audience loyalty and corporate sponsorship opportunities.

Partnership development with technology companies, media platforms, and corporate sponsors creates opportunities for integrated promotional campaigns that leverage multiple distribution channels and revenue sources. Strategic alliances enable promoters to access new capabilities, audiences, and market segments while sharing operational risks and costs.

Complex market dynamics shape the United States sports promoter market through interconnected forces including consumer behavior evolution, technological disruption, competitive pressures, and regulatory changes that influence strategic decision-making and operational approaches.

Supply and demand balance varies significantly across different sports categories, geographic regions, and event types, creating opportunities for specialized promoters while challenging those seeking broad market coverage. Premium events in popular sports categories command substantial pricing power, while emerging sports and niche markets offer growth potential with lower entry barriers.

Competitive intensity continues increasing as traditional promoters face competition from new market entrants, technology-enabled platforms, and integrated entertainment companies. Market consolidation trends create larger promotional entities with enhanced capabilities while potentially reducing competition in specific market segments.

Technology integration transforms promotional strategies and operational approaches, with approximately 68% of promoters investing significantly in digital marketing platforms, data analytics capabilities, and automated operational systems. These investments enhance efficiency and effectiveness while requiring substantial capital commitments and specialized expertise.

Consumer expectations evolve toward more personalized, interactive, and technologically enhanced event experiences, driving promoters to invest in venue improvements, digital engagement platforms, and premium service offerings. Meeting these expectations requires ongoing innovation and investment in customer experience enhancement initiatives.

Comprehensive research methodology employed in analyzing the United States sports promoter market incorporates multiple data collection approaches, analytical frameworks, and validation processes to ensure accuracy, reliability, and actionable insights for industry stakeholders.

Primary research includes extensive interviews with industry executives, promotional professionals, venue operators, and sports marketing specialists to gather firsthand insights regarding market trends, competitive dynamics, and operational challenges. Survey data collection from promoters across various market segments provides quantitative insights into business practices, performance metrics, and strategic priorities.

Secondary research encompasses analysis of industry publications, financial reports, regulatory filings, and market studies to establish baseline market understanding and identify key trends. Data synthesis from multiple sources ensures comprehensive market coverage and validates primary research findings through triangulation methodologies.

Analytical frameworks include competitive landscape mapping, market segmentation analysis, trend identification, and forecasting models that project future market development based on historical patterns and identified growth drivers. MarkWide Research analytical capabilities provide sophisticated modeling and scenario analysis to support strategic planning and investment decision-making.

Data validation processes include cross-referencing multiple sources, expert review panels, and statistical validation techniques to ensure research accuracy and reliability. Ongoing market monitoring and periodic research updates maintain current market understanding and identify emerging trends and opportunities.

Geographic distribution of the United States sports promoter market reveals significant regional variations in market size, competitive intensity, consumer preferences, and growth opportunities that influence promotional strategies and investment priorities.

Northeast region represents approximately 28% of total market activity, driven by major metropolitan areas including New York, Boston, and Philadelphia that offer substantial population density, high disposable income levels, and sophisticated entertainment infrastructure. The region benefits from established sports franchises, premium venues, and corporate sponsorship opportunities that support high-value promotional activities.

West Coast markets account for roughly 25% of promotional activities, with Los Angeles, San Francisco, and Seattle serving as primary centers for sports promotion. The region demonstrates strong growth in technology integration, alternative sports programming, and innovative promotional approaches that appeal to diverse, tech-savvy audiences.

Southeast region shows rapid growth with approximately 22% market share, benefiting from population growth, economic development, and strong sports culture throughout states including Florida, Georgia, and North Carolina. College sports promotion represents a particularly strong segment within this region, supported by passionate fan bases and extensive alumni networks.

Midwest and Southwest regions collectively represent the remaining 25% of market activity, with Chicago, Dallas, and Denver serving as major promotional centers. These markets offer opportunities for cost-effective operations, strong community support, and growing corporate sponsorship availability as regional economies continue developing.

Competitive environment within the United States sports promoter market features diverse participants ranging from large integrated entertainment companies to specialized boutique promoters, each leveraging unique capabilities and market positioning strategies.

Market concentration shows moderate consolidation with top competitors maintaining significant market share while numerous smaller promoters serve niche markets and regional opportunities. Competitive differentiation occurs through specialization, venue relationships, talent exclusivity, and technological capabilities.

Market segmentation analysis reveals multiple classification approaches that help understand the diverse nature of the United States sports promoter market and identify specific opportunities within various market categories.

By Sport Category:

By Event Scale:

By Revenue Model:

Professional team sports promotion represents the largest market segment, benefiting from established fan bases, extensive media coverage, and substantial corporate sponsorship opportunities. This category demonstrates stable revenue streams and predictable seasonal patterns that support long-term promotional planning and investment strategies.

Combat sports promotion shows exceptional growth potential with approximately 12% annual growth rate driven by increasing mainstream acceptance, pay-per-view revenue opportunities, and global audience appeal. Promoters in this segment leverage celebrity athlete personalities and dramatic storylines to generate substantial audience engagement and premium pricing opportunities.

Esports promotion emerges as a rapidly expanding category with significant growth among younger demographics, technology integration opportunities, and innovative promotional approaches. This segment benefits from lower operational costs, global audience reach, and strong corporate sponsor interest in reaching tech-savvy consumer segments.

Alternative sports promotion creates opportunities for specialized promoters to develop niche markets with passionate fan bases and limited competition. These categories often demonstrate strong community engagement, grassroots marketing effectiveness, and opportunities for innovative promotional approaches that differentiate from mainstream sports.

Regional event promotion provides opportunities for smaller promoters to establish market presence, develop local relationships, and create sustainable business models without competing directly with major market players. Success in regional promotion often depends on community engagement, local sponsorship development, and cost-effective operational approaches.

Industry participants within the United States sports promoter market realize substantial benefits through strategic positioning, operational excellence, and stakeholder relationship development that create sustainable competitive advantages and revenue growth opportunities.

Revenue diversification enables promoters to develop multiple income streams including ticket sales, sponsorship agreements, media rights, merchandise sales, and ancillary services that reduce dependence on single revenue sources and improve financial stability. Successful promoters typically generate approximately 35% of revenue from ticket sales, with the remainder from various partnership and commercial activities.

Brand development opportunities allow promoters to establish market recognition, build audience loyalty, and create valuable intellectual property that supports long-term business growth. Strong promotional brands command premium pricing, attract quality talent, and secure favorable venue and partnership agreements.

Network effects benefit established promoters through industry relationships, venue partnerships, talent connections, and sponsor relationships that create barriers to entry and support business expansion opportunities. These networks provide access to exclusive opportunities and preferential terms that enhance competitive positioning.

Technology leverage enables promoters to improve operational efficiency, enhance audience engagement, and develop new revenue streams through digital platforms, data analytics, and automated systems. Technology investments typically generate efficiency improvements of 25-30% while enabling new promotional capabilities and audience reach expansion.

Market expansion opportunities allow successful promoters to replicate proven models in new geographic markets, sports categories, or audience segments, creating scalable growth platforms and diversified market exposure that reduces business risk and increases revenue potential.

Strengths:

Weaknesses:

Opportunities:

Threats:

Transformative trends shaping the United States sports promoter market reflect broader changes in consumer behavior, technology adoption, and industry structure that influence promotional strategies and business models.

Digital-first promotion becomes increasingly important as promoters leverage social media, streaming platforms, and mobile applications to reach audiences and enhance engagement. Approximately 82% of promotional campaigns now include significant digital components, representing a fundamental shift from traditional marketing approaches toward integrated digital strategies.

Experiential enhancement drives promoters to create more immersive and personalized event experiences through premium amenities, exclusive access opportunities, and technology integration. Consumer willingness to pay premium prices for enhanced experiences creates revenue opportunities while requiring substantial operational investment and innovation.

Data-driven decision making transforms promotional strategies through advanced analytics, audience segmentation, and performance measurement capabilities. Promoters increasingly rely on data insights to optimize pricing strategies, marketing campaigns, and operational efficiency while improving audience targeting and engagement effectiveness.

Sustainability focus influences promotional practices as environmental consciousness grows among consumers and corporate sponsors. Green event practices, sustainable venue operations, and environmental responsibility messaging become important differentiators and stakeholder requirements.

Content creation integration expands promotional activities beyond event execution to include documentary production, social media content, and multimedia storytelling that extends audience engagement and creates additional revenue streams. This trend reflects the convergence of sports promotion with broader entertainment and media industries.

Recent industry developments demonstrate the dynamic nature of the United States sports promoter market and highlight emerging trends that influence competitive positioning and strategic planning across various market segments.

Technology partnerships between promoters and technology companies create innovative promotional capabilities including virtual reality experiences, artificial intelligence-powered audience targeting, and automated operational systems. These collaborations enable promoters to enhance efficiency while creating differentiated event experiences that attract audiences and sponsors.

Venue innovation includes development of flexible, technology-enabled facilities that support multiple sports and entertainment formats while providing enhanced audience experiences. New venue designs incorporate advanced audio-visual systems, premium amenities, and sustainable operations that meet evolving consumer expectations and operational requirements.

Media rights evolution reflects changing consumption patterns as streaming platforms, social media channels, and digital content distributors compete with traditional television networks for sports content rights. This evolution creates new revenue opportunities for promoters while requiring adaptation to different distribution models and audience engagement approaches.

Regulatory developments include evolving sports betting regulations, athlete compensation rules, and safety requirements that impact promotional operations and create new compliance obligations. Promoters must adapt to these changes while identifying opportunities to leverage regulatory developments for business advantage.

Corporate sponsorship innovation moves beyond traditional advertising toward integrated brand experiences, content partnerships, and data-driven marketing collaborations that provide enhanced value for sponsors while creating new revenue streams for promoters.

Strategic recommendations for United States sports promoter market participants focus on leveraging emerging opportunities while addressing operational challenges and competitive pressures that influence long-term success and profitability.

Technology investment should prioritize platforms and capabilities that enhance audience engagement, improve operational efficiency, and create new revenue streams. MWR analysis suggests promoters allocating approximately 15-20% of revenue toward technology development and digital marketing capabilities typically achieve superior growth and profitability compared to competitors with limited technology investment.

Partnership development offers opportunities to access new capabilities, markets, and revenue streams while sharing operational risks and costs. Successful partnerships typically focus on complementary strengths, shared strategic objectives, and clear performance metrics that ensure mutual benefit and sustainable collaboration.

Market diversification reduces dependence on single sports categories, geographic markets, or revenue sources while creating opportunities for cross-promotion and operational synergies. Diversification strategies should balance growth opportunities with operational complexity and resource requirements.

Audience development requires understanding evolving consumer preferences, demographic shifts, and engagement patterns that influence promotional effectiveness. Successful promoters invest in audience research, segmentation analysis, and personalized marketing approaches that enhance loyalty and lifetime value.

Operational excellence becomes increasingly important as competition intensifies and profit margins face pressure from rising costs and market saturation. Focus areas include cost management, process optimization, quality improvement, and performance measurement systems that support sustainable competitive advantage.

Long-term prospects for the United States sports promoter market remain positive, supported by fundamental growth drivers including demographic trends, technology advancement, and evolving consumer preferences that create substantial opportunities for well-positioned market participants.

Market expansion is projected to continue at a steady growth rate of 5.8% annually through the next decade, driven by increasing consumer spending on entertainment experiences, corporate sponsorship investment, and technological innovations that enhance promotional capabilities and audience engagement. This growth trajectory reflects strong underlying demand and market fundamentals.

Technology integration will accelerate as promoters leverage artificial intelligence, virtual reality, blockchain, and advanced analytics to create differentiated experiences, improve operational efficiency, and develop new revenue streams. Early technology adopters are expected to gain significant competitive advantages and market share.

Geographic expansion opportunities will emerge in secondary and tertiary markets as infrastructure development, demographic changes, and economic growth create new promotional possibilities. International expansion may also present opportunities for established promoters seeking growth beyond domestic markets.

Industry consolidation trends may continue as larger promoters acquire specialized companies, technology capabilities, and market access while smaller players focus on niche markets and regional opportunities. This consolidation could create both challenges and opportunities depending on market positioning and strategic capabilities.

Regulatory evolution will continue influencing market dynamics as sports betting expansion, athlete compensation changes, and safety requirements create new compliance obligations and business opportunities that require adaptive strategies and operational flexibility.

The United States sports promoter market represents a dynamic and growing sector with substantial opportunities for well-positioned participants who can navigate competitive challenges while leveraging emerging trends and technological capabilities. Market fundamentals remain strong, supported by America’s passionate sports culture, increasing consumer spending on entertainment experiences, and expanding corporate sponsorship investment that creates multiple revenue streams and growth opportunities.

Success factors in this market include technology adoption, audience engagement capabilities, operational excellence, strategic partnerships, and adaptability to evolving consumer preferences and industry dynamics. Promoters who invest in digital capabilities, develop strong stakeholder relationships, and maintain operational flexibility are best positioned to capture growth opportunities and achieve sustainable competitive advantages.

Future growth will be driven by continued demographic shifts, technology advancement, geographic expansion opportunities, and evolving entertainment consumption patterns that favor experiential purchases and premium event experiences. The market’s resilience and adaptability demonstrate its potential for continued expansion and innovation despite periodic challenges and competitive pressures.

As the sports promotion industry continues evolving, participants must balance growth ambitions with operational realities while maintaining focus on audience satisfaction, stakeholder value creation, and sustainable business practices that support long-term success in this dynamic and rewarding market sector.

What is Sports Promoter?

Sports promoters are individuals or organizations that manage and promote sporting events, athletes, and teams. They play a crucial role in organizing events, securing sponsorships, and enhancing the visibility of sports in various markets.

What are the key players in the United States Sports Promoter Market?

Key players in the United States Sports Promoter Market include companies like IMG, Octagon, and Wasserman Media Group. These firms are known for their extensive networks and expertise in managing sports events and athlete representation, among others.

What are the growth factors driving the United States Sports Promoter Market?

The growth of the United States Sports Promoter Market is driven by increasing sports viewership, rising sponsorship deals, and the expansion of digital media platforms. Additionally, the growing popularity of e-sports and live events contributes to market expansion.

What challenges does the United States Sports Promoter Market face?

Challenges in the United States Sports Promoter Market include intense competition among promoters, fluctuating economic conditions affecting sponsorship budgets, and the impact of unforeseen events like pandemics on live sports. These factors can hinder event planning and execution.

What opportunities exist in the United States Sports Promoter Market?

Opportunities in the United States Sports Promoter Market include the rise of virtual and hybrid events, increased investment in women’s sports, and the potential for innovative marketing strategies through social media. These trends can enhance audience engagement and revenue streams.

What trends are shaping the United States Sports Promoter Market?

Trends shaping the United States Sports Promoter Market include the integration of technology in event management, the growing importance of data analytics for audience targeting, and the rise of influencer marketing in sports promotion. These trends are transforming how events are marketed and experienced.

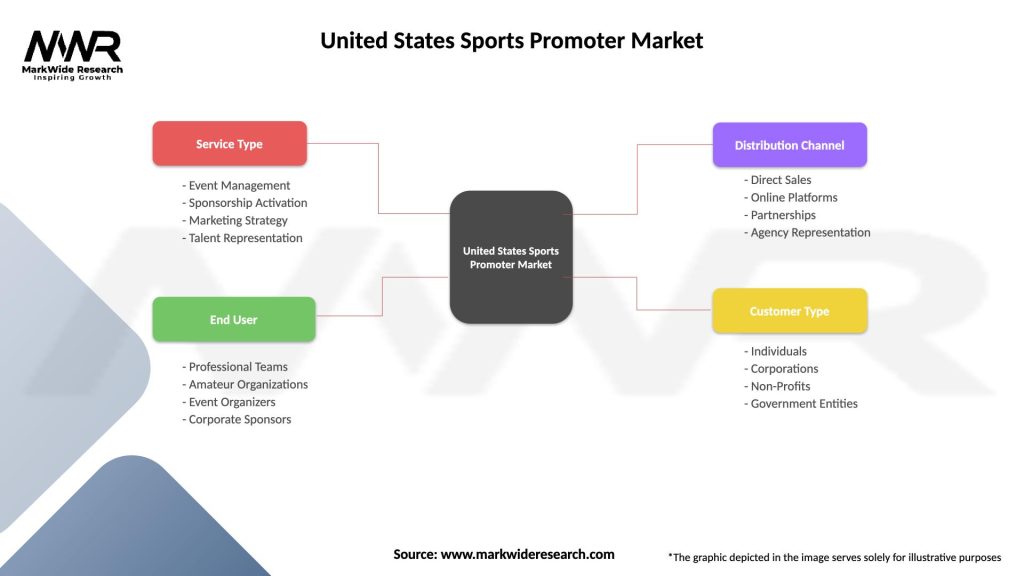

United States Sports Promoter Market

| Segmentation Details | Description |

|---|---|

| Service Type | Event Management, Sponsorship Activation, Marketing Strategy, Talent Representation |

| End User | Professional Teams, Amateur Organizations, Event Organizers, Corporate Sponsors |

| Distribution Channel | Direct Sales, Online Platforms, Partnerships, Agency Representation |

| Customer Type | Individuals, Corporations, Non-Profits, Government Entities |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the United States Sports Promoter Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.