444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The United States plastic packaging films market represents a dynamic and rapidly evolving sector within the broader packaging industry. This market encompasses various types of flexible plastic films used across multiple applications, from food packaging to industrial wrapping solutions. Market dynamics indicate robust growth driven by increasing consumer demand for convenient packaging, sustainability initiatives, and technological advancements in film manufacturing.

Growth trajectories in the plastic packaging films sector demonstrate significant expansion, with the market experiencing a compound annual growth rate (CAGR) of 4.2% over recent years. This growth reflects the versatility and adaptability of plastic films in meeting diverse packaging requirements across industries. Innovation drivers include the development of biodegradable films, enhanced barrier properties, and smart packaging technologies that extend product shelf life and improve consumer experience.

Regional concentration shows the United States maintaining its position as a leading consumer of plastic packaging films, with approximately 35% market share in North America. The market benefits from advanced manufacturing capabilities, strong consumer goods sectors, and increasing adoption of flexible packaging solutions across food and beverage, pharmaceutical, and consumer goods industries.

The United States plastic packaging films market refers to the comprehensive ecosystem of flexible plastic materials used for packaging applications across various industries. These films are manufactured from different polymer resins including polyethylene, polypropylene, polyester, and specialty materials designed to provide protection, preservation, and presentation for packaged goods.

Packaging films serve multiple critical functions including moisture barrier protection, oxygen resistance, mechanical strength, and visual appeal. The market encompasses various film types such as shrink films, stretch films, barrier films, and specialty films engineered for specific applications. Manufacturing processes include blown film extrusion, cast film production, and co-extrusion techniques that create multi-layer structures with enhanced performance characteristics.

Market participants include raw material suppliers, film manufacturers, converters, and end-users across food processing, retail, pharmaceutical, and industrial sectors. The interconnected nature of this market reflects the essential role of plastic packaging films in modern supply chains and consumer product distribution systems.

Strategic positioning of the United States plastic packaging films market reveals a mature yet innovative sector experiencing steady growth driven by evolving consumer preferences and technological advancement. The market demonstrates resilience through adaptation to sustainability challenges while maintaining performance standards required by diverse applications.

Key growth drivers include the expansion of e-commerce packaging requirements, increasing demand for fresh food packaging, and the development of sustainable film alternatives. Market participants are investing heavily in research and development to create films with improved recyclability, reduced environmental impact, and enhanced functionality. Adoption rates for bio-based and compostable films show 18% annual growth, indicating strong market acceptance of sustainable alternatives.

Competitive dynamics feature both established multinational corporations and innovative specialty manufacturers competing on technology, sustainability, and cost-effectiveness. The market structure supports both high-volume commodity applications and specialized niche segments requiring customized film solutions. Investment trends show increased focus on circular economy principles and advanced recycling technologies.

Market intelligence reveals several critical insights shaping the United States plastic packaging films landscape:

Market penetration analysis shows plastic packaging films achieving 78% adoption rate in flexible packaging applications, demonstrating their essential role in modern packaging systems. These insights guide strategic decision-making for market participants and stakeholders.

Primary growth drivers propelling the United States plastic packaging films market include evolving consumer lifestyles, technological innovations, and expanding application areas. The increasing preference for convenient, portable food packaging solutions drives significant demand for flexible films across retail and foodservice sectors.

E-commerce expansion represents a major market driver, with online retail growth requiring specialized packaging films for product protection during shipping and handling. The surge in home delivery services and direct-to-consumer sales models creates substantial opportunities for protective and branded packaging films. Growth rates in e-commerce packaging show 12% annual increase in film consumption.

Food safety requirements drive demand for advanced barrier films that extend shelf life, maintain product quality, and ensure consumer safety. Regulatory standards for food contact materials and traceability requirements support market growth for specialized films with enhanced performance characteristics. Innovation investments in antimicrobial and active packaging technologies further accelerate market expansion.

Sustainability initiatives paradoxically drive market growth as companies develop eco-friendly film alternatives that maintain performance while reducing environmental impact. The push for circular economy solutions creates opportunities for recyclable, compostable, and bio-based film materials that meet both performance and sustainability requirements.

Environmental concerns represent the most significant restraint facing the United States plastic packaging films market. Growing awareness of plastic pollution, marine debris, and waste management challenges creates regulatory pressure and consumer resistance to traditional plastic packaging solutions. Legislative initiatives targeting single-use plastics and packaging waste reduction impact market growth in certain segments.

Raw material volatility poses ongoing challenges for film manufacturers, with petroleum-based resin prices subject to fluctuations based on crude oil markets and supply chain disruptions. These cost variations affect profit margins and pricing strategies, particularly for commodity film applications where price sensitivity is high.

Recycling infrastructure limitations constrain market growth as inadequate collection and processing systems for flexible films create waste management challenges. The complexity of multi-layer film structures and contamination issues limit recycling rates, contributing to environmental concerns and regulatory scrutiny.

Competition from alternatives including paper-based packaging, rigid containers, and reusable packaging systems challenges market share in certain applications. The development of alternative packaging materials with comparable performance characteristics creates competitive pressure on traditional plastic films.

Sustainable innovation presents the most significant opportunity for the United States plastic packaging films market. The development of biodegradable, compostable, and recyclable film materials addresses environmental concerns while maintaining performance standards. Investment opportunities in bio-based polymers and advanced recycling technologies show 25% growth potential over the next five years.

Smart packaging integration offers substantial growth opportunities through the incorporation of sensors, indicators, and digital technologies into film structures. These intelligent packaging solutions provide real-time information about product freshness, temperature exposure, and authenticity, creating value-added applications across multiple industries.

Medical and pharmaceutical applications represent expanding opportunities driven by aging demographics, healthcare innovation, and stringent packaging requirements. Specialized films for medical device packaging, pharmaceutical products, and sterile applications command premium pricing and demonstrate strong growth potential.

Agricultural applications provide emerging opportunities for greenhouse films, mulch films, and crop protection materials. The growing focus on sustainable agriculture and food security creates demand for specialized films that improve crop yields while reducing environmental impact. Market expansion in agricultural films shows 8% annual growth rate.

Supply chain dynamics in the United States plastic packaging films market reflect complex interactions between raw material suppliers, film manufacturers, converters, and end-users. The market operates through integrated value chains that optimize efficiency, quality, and cost-effectiveness across multiple production stages.

Technological evolution drives continuous market transformation through advanced manufacturing processes, material innovations, and application development. The adoption of Industry 4.0 technologies, including automation, data analytics, and predictive maintenance, enhances production efficiency and product quality while reducing operational costs.

Regulatory landscape significantly influences market dynamics through food safety standards, environmental regulations, and packaging requirements. Compliance with FDA regulations, state-level plastic reduction initiatives, and international standards shapes product development and market strategies. Regulatory compliance costs account for approximately 6% of total production expenses.

Consumer behavior patterns increasingly emphasize convenience, sustainability, and product transparency, driving demand for innovative packaging solutions. The shift toward premium and organic products creates opportunities for specialized films with enhanced barrier properties and visual appeal. Market research indicates 42% of consumers consider packaging sustainability in purchasing decisions.

Comprehensive analysis of the United States plastic packaging films market employs multiple research methodologies to ensure accuracy, reliability, and depth of insights. The research approach combines quantitative data analysis with qualitative market intelligence to provide a complete market perspective.

Primary research involves extensive interviews with industry executives, technical experts, and key stakeholders across the value chain. This includes film manufacturers, raw material suppliers, packaging converters, and end-users in food, pharmaceutical, and consumer goods industries. Survey methodologies capture market trends, technology adoption patterns, and future investment plans.

Secondary research encompasses analysis of industry reports, trade publications, regulatory filings, and company financial statements. Patent analysis, technology assessments, and competitive intelligence provide insights into innovation trends and market positioning strategies. Data validation through multiple sources ensures research accuracy and reliability.

Market modeling techniques include statistical analysis, trend extrapolation, and scenario planning to project future market conditions. The research methodology incorporates economic indicators, demographic trends, and regulatory developments to provide comprehensive market forecasts and strategic recommendations.

Geographic distribution of the United States plastic packaging films market shows concentrated activity in major manufacturing regions with strong industrial bases and transportation infrastructure. The Midwest region leads market activity with approximately 32% market share, driven by food processing industries and agricultural applications.

Southeast markets demonstrate strong growth in packaging films consumption, supported by expanding food and beverage manufacturing, pharmaceutical production, and distribution centers. The region benefits from favorable business climates, logistics advantages, and proximity to major consumer markets. Growth rates in southeastern states average 5.8% annually.

West Coast markets focus on innovation and sustainability, with California leading in sustainable packaging initiatives and technology development. The region’s emphasis on environmental regulations and consumer awareness drives demand for eco-friendly film alternatives and advanced packaging solutions.

Northeast corridor maintains significant market presence through established manufacturing facilities, research institutions, and proximity to major consumer markets. The region’s mature market structure supports both commodity and specialty film applications across diverse industries.

Market leadership in the United States plastic packaging films sector features a combination of large multinational corporations and specialized regional manufacturers competing across different market segments and applications.

Competitive strategies emphasize technological innovation, sustainability initiatives, and customer-specific solutions. Market participants invest heavily in research and development, manufacturing efficiency, and strategic acquisitions to maintain competitive advantages.

Material-based segmentation of the United States plastic packaging films market reveals diverse polymer types serving specific application requirements:

By Material Type:

By Application:

Food packaging films represent the largest category within the United States market, driven by consumer demand for fresh, convenient, and safe food products. This category encompasses barrier films for meat and dairy products, breathable films for fresh produce, and specialty films for frozen and processed foods. Innovation focus includes active packaging technologies that extend shelf life and maintain product quality.

Industrial packaging films serve critical functions in manufacturing and distribution operations, providing protection during transportation, storage, and handling. This category includes stretch films for pallet wrapping, shrink films for product bundling, and protective films for surface protection. Performance requirements emphasize strength, puncture resistance, and load stability.

Medical and pharmaceutical films represent a high-value category with stringent regulatory requirements and specialized performance characteristics. These films must meet FDA standards for medical device packaging, pharmaceutical products, and sterile applications. Growth drivers include aging demographics, healthcare innovation, and increasing demand for single-use medical products.

Sustainable film categories show rapid growth as manufacturers develop biodegradable, compostable, and recyclable alternatives to traditional plastic films. According to MarkWide Research analysis, sustainable films demonstrate 22% annual growth rate as companies respond to environmental concerns and regulatory requirements.

Manufacturing efficiency benefits include optimized production processes, reduced material waste, and improved quality control through advanced film technologies. Manufacturers achieve cost savings through automation, energy efficiency, and streamlined operations while maintaining product quality and consistency.

Brand differentiation opportunities enable consumer goods companies to enhance product appeal through innovative packaging designs, premium film materials, and sustainable packaging solutions. Advanced printing capabilities and specialty films support brand marketing objectives and consumer engagement strategies.

Supply chain optimization benefits include improved product protection, extended shelf life, and reduced transportation costs through lightweight, high-performance films. Enhanced barrier properties and protective characteristics minimize product loss and waste throughout distribution channels.

Regulatory compliance advantages help companies meet evolving food safety, environmental, and packaging requirements through certified film materials and documented quality systems. Compliance with industry standards reduces regulatory risks and supports market access across different regions and applications.

Innovation partnerships between film manufacturers, equipment suppliers, and end-users drive collaborative development of customized solutions that address specific market needs and performance requirements. These partnerships accelerate technology adoption and market penetration for advanced film technologies.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability transformation represents the most significant trend reshaping the United States plastic packaging films market. Companies are investing heavily in developing circular economy solutions, including chemical recycling technologies, bio-based materials, and design for recyclability initiatives. Investment levels in sustainable technologies show 30% annual increase across major market participants.

Digital integration trends include the adoption of smart packaging technologies, digital printing capabilities, and data-driven manufacturing processes. These technologies enable real-time monitoring, quality control, and customer engagement through interactive packaging solutions. Technology adoption rates for digital printing reach 15% of total film production.

Customization and personalization trends drive demand for shorter production runs, variable printing, and application-specific film formulations. Manufacturers are developing flexible production systems that can efficiently produce customized films for niche applications and regional market requirements.

Supply chain resilience trends emphasize local sourcing, diversified supplier networks, and inventory optimization strategies to mitigate disruption risks. Companies are investing in regional manufacturing capabilities and strategic partnerships to ensure supply chain stability and responsiveness to market demands.

Technology breakthroughs in the United States plastic packaging films market include the development of next-generation barrier films with enhanced performance characteristics and reduced environmental impact. Recent innovations feature mono-material structures that maintain barrier properties while improving recyclability and reducing material complexity.

Strategic acquisitions and partnerships reshape the competitive landscape as companies seek to expand capabilities, access new technologies, and strengthen market positions. Major transactions focus on sustainable packaging technologies, specialty film capabilities, and regional market expansion opportunities.

Regulatory developments include new FDA guidelines for food contact materials, state-level plastic reduction initiatives, and extended producer responsibility programs affecting packaging design and waste management. These regulations drive innovation in sustainable materials and circular economy solutions.

Infrastructure investments in recycling facilities, manufacturing equipment, and research and development capabilities support market growth and sustainability objectives. Companies are modernizing production facilities to improve efficiency, reduce environmental impact, and meet evolving customer requirements.

Strategic recommendations for United States plastic packaging films market participants emphasize the critical importance of sustainability integration and innovation investment. Companies should prioritize development of recyclable, biodegradable, and bio-based film alternatives while maintaining performance standards required by diverse applications.

Technology investment strategies should focus on advanced manufacturing processes, digital integration, and smart packaging capabilities that create competitive advantages and customer value. MWR analysis suggests companies allocating 8-12% of revenue to research and development achieve superior market performance and growth rates.

Market positioning recommendations include developing specialized capabilities in high-growth segments such as medical packaging, sustainable films, and smart packaging solutions. Companies should leverage expertise in specific applications to command premium pricing and build customer loyalty.

Partnership strategies should emphasize collaboration with technology providers, research institutions, and supply chain partners to accelerate innovation and market development. Strategic alliances can provide access to new technologies, markets, and capabilities while sharing development costs and risks.

Regulatory preparedness requires proactive engagement with evolving environmental regulations and industry standards. Companies should anticipate regulatory changes and invest in compliance capabilities that support long-term market participation and growth.

Long-term projections for the United States plastic packaging films market indicate continued growth driven by innovation, sustainability initiatives, and expanding applications. The market is expected to maintain a compound annual growth rate of 4.5% over the next five years, supported by technology advancement and market diversification strategies.

Sustainability transformation will fundamentally reshape the market landscape as companies transition to circular economy models and develop environmentally responsible packaging solutions. Bio-based and recyclable films are projected to capture 25% market share within the next decade, driven by regulatory requirements and consumer preferences.

Technology evolution will enable new applications and performance capabilities through advanced materials, smart packaging integration, and manufacturing process innovations. The convergence of packaging and digital technologies creates opportunities for value-added solutions that enhance product protection, consumer engagement, and supply chain efficiency.

Market consolidation trends may accelerate as companies seek scale advantages, technology access, and market position strengthening through strategic acquisitions and partnerships. This consolidation will likely favor companies with strong innovation capabilities, sustainability leadership, and customer relationships.

Global competitiveness will require continued investment in manufacturing efficiency, product innovation, and customer service capabilities. According to MarkWide Research projections, companies maintaining technology leadership and sustainability focus will achieve superior growth and profitability in the evolving market landscape.

Market assessment of the United States plastic packaging films sector reveals a dynamic industry undergoing significant transformation driven by sustainability imperatives, technological innovation, and evolving customer requirements. The market demonstrates resilience and adaptability while addressing environmental challenges and regulatory pressures through innovative solutions and strategic investments.

Growth prospects remain positive despite environmental concerns and regulatory challenges, supported by expanding applications, technology advancement, and sustainable innovation initiatives. The successful companies will be those that effectively balance performance requirements with environmental responsibility while maintaining cost competitiveness and customer satisfaction.

Strategic success in this market requires comprehensive approaches encompassing sustainability leadership, technology innovation, customer partnership, and operational excellence. Companies that invest in circular economy solutions, advanced manufacturing capabilities, and market-specific applications will achieve competitive advantages and superior growth performance in the evolving market landscape.

What is Plastic Packaging Films?

Plastic packaging films are thin layers of plastic material used for packaging products. They are commonly utilized in various applications such as food packaging, medical supplies, and consumer goods due to their lightweight and protective properties.

What are the key players in the United States Plastic Packaging Films Market?

Key players in the United States Plastic Packaging Films Market include companies like Amcor plc, Berry Global, and Sealed Air Corporation. These companies are known for their innovative packaging solutions and extensive product offerings, among others.

What are the growth factors driving the United States Plastic Packaging Films Market?

The growth of the United States Plastic Packaging Films Market is driven by increasing demand for convenient packaging solutions, the rise of e-commerce, and the need for sustainable packaging options. Additionally, advancements in film technology are enhancing product performance.

What challenges does the United States Plastic Packaging Films Market face?

The United States Plastic Packaging Films Market faces challenges such as environmental concerns regarding plastic waste and regulatory pressures for sustainable materials. Additionally, competition from alternative packaging solutions can impact market growth.

What opportunities exist in the United States Plastic Packaging Films Market?

Opportunities in the United States Plastic Packaging Films Market include the development of biodegradable films and innovations in smart packaging technologies. The growing focus on sustainability is also prompting companies to explore eco-friendly materials.

What trends are shaping the United States Plastic Packaging Films Market?

Trends in the United States Plastic Packaging Films Market include the increasing adoption of recyclable materials and the integration of digital printing technologies. Additionally, there is a growing emphasis on lightweight packaging to reduce material usage and enhance efficiency.

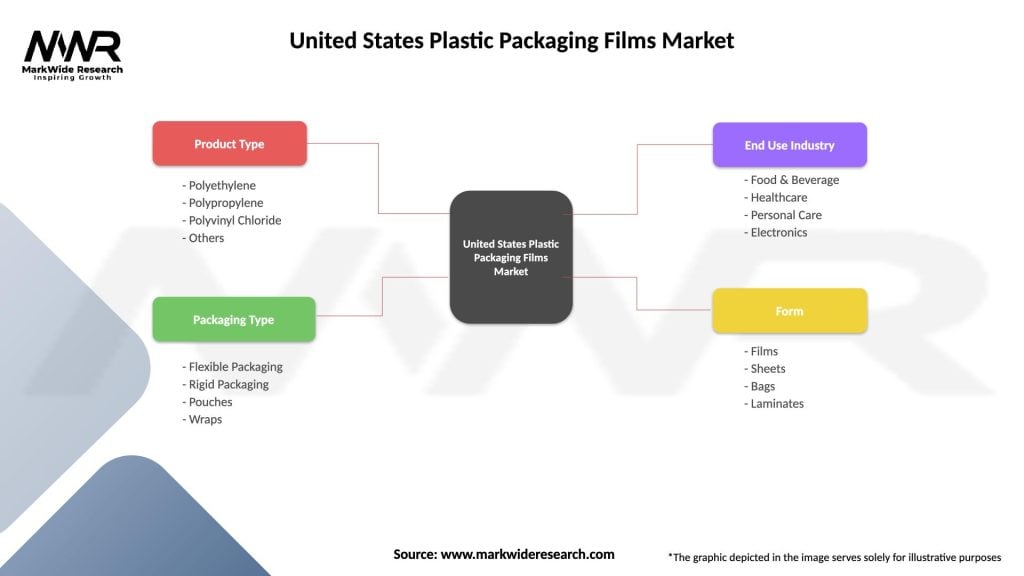

United States Plastic Packaging Films Market

| Segmentation Details | Description |

|---|---|

| Product Type | Polyethylene, Polypropylene, Polyvinyl Chloride, Others |

| Packaging Type | Flexible Packaging, Rigid Packaging, Pouches, Wraps |

| End Use Industry | Food & Beverage, Healthcare, Personal Care, Electronics |

| Form | Films, Sheets, Bags, Laminates |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the United States Plastic Packaging Films Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.