444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The United States Less than-Truck-Load (LTL) market represents a critical component of the nation’s freight transportation infrastructure, serving businesses that require shipping solutions for cargo that doesn’t fill an entire truck trailer. This specialized logistics sector has experienced remarkable transformation driven by e-commerce growth, supply chain optimization demands, and technological advancement. Market dynamics indicate robust expansion with the sector growing at a compound annual growth rate (CAGR) of 4.2% over the forecast period.

Regional carriers and national LTL providers have adapted their service offerings to meet evolving customer expectations for faster delivery times, enhanced tracking capabilities, and flexible pickup schedules. The market encompasses various service tiers from standard ground transportation to expedited and specialized handling services. Technology integration has become paramount, with carriers investing heavily in route optimization software, real-time tracking systems, and automated sorting facilities to improve operational efficiency and customer satisfaction.

Industry consolidation continues to shape the competitive landscape as larger carriers acquire regional players to expand their network coverage and service capabilities. The sector benefits from strong fundamentals including consistent demand from manufacturing, retail, and distribution sectors. Sustainability initiatives are increasingly important, with carriers implementing fuel-efficient vehicles, alternative fuel technologies, and optimized routing to reduce environmental impact while maintaining cost competitiveness.

The United States Less than-Truck-Load (LTL) market refers to the freight transportation sector that specializes in shipping cargo that occupies less than a full truck trailer, typically ranging from 150 to 15,000 pounds. This service model allows multiple shippers to share trailer space and transportation costs, making it an economical solution for businesses with smaller shipment volumes.

LTL carriers operate through hub-and-spoke networks where freight is consolidated at terminal facilities before being transported to destination terminals for final delivery. This system enables efficient resource utilization while providing comprehensive geographic coverage. Service classifications typically include standard, expedited, and specialized handling options, with pricing based on factors such as weight, dimensions, distance, and service level requirements.

Market participants range from large national carriers with extensive terminal networks to regional specialists serving specific geographic areas or industry verticals. The sector plays a vital role in supporting supply chain operations across manufacturing, retail, healthcare, automotive, and industrial sectors by providing reliable, cost-effective transportation solutions for businesses of all sizes.

Strategic positioning within the United States LTL market requires understanding of evolving customer demands, technological capabilities, and operational excellence requirements. The sector demonstrates resilience through economic cycles while adapting to changing shipping patterns driven by e-commerce growth and supply chain reconfiguration. Market leaders maintain competitive advantages through extensive terminal networks, advanced technology platforms, and superior service reliability.

Growth drivers include increasing demand for flexible shipping solutions, expansion of regional manufacturing, and continued e-commerce penetration across business-to-business segments. The market benefits from modal shift trends as shippers seek alternatives to full truckload transportation for smaller shipments. Operational efficiency improvements through automation and technology adoption have enhanced service quality while controlling cost inflation.

Competitive dynamics emphasize service differentiation, network density, and technological capabilities as key success factors. Leading carriers invest significantly in terminal modernization, fleet upgrades, and digital platform development to maintain market position. Customer retention rates average 85-90% among top-tier carriers, reflecting the importance of service consistency and relationship management in this sector.

Market intelligence reveals several critical trends shaping the United States LTL landscape. The sector demonstrates strong correlation with industrial production and manufacturing activity, with capacity utilization rates typically ranging between 92-96% during peak demand periods. Service reliability has become increasingly important as supply chains adopt just-in-time inventory strategies.

E-commerce expansion continues driving demand for flexible LTL services as businesses require reliable transportation solutions for varied shipment sizes and delivery requirements. The growth of omnichannel retail strategies necessitates sophisticated logistics capabilities that LTL carriers are uniquely positioned to provide. Supply chain optimization initiatives across industries create opportunities for carriers offering value-added services and technology-enabled solutions.

Manufacturing reshoring trends contribute to increased domestic freight volumes as companies relocate production facilities closer to end markets. This geographic redistribution of manufacturing activity creates new shipping lanes and service opportunities for LTL providers. Regional economic development in secondary markets generates additional demand for transportation services connecting emerging industrial centers with established distribution networks.

Technology advancement enables carriers to offer enhanced service capabilities including real-time tracking, predictive analytics, and automated customer communications. These technological improvements support customer retention and enable premium pricing for superior service levels. Regulatory compliance requirements create barriers to entry that benefit established carriers with comprehensive compliance programs and operational expertise.

Infrastructure investment in terminal facilities, sorting equipment, and fleet modernization supports capacity expansion and service improvement initiatives. MarkWide Research analysis indicates that carriers investing in technology and infrastructure improvements achieve customer satisfaction scores that are 15-20% higher than industry averages.

Driver shortage challenges continue impacting the LTL sector as carriers compete for qualified professional drivers in a constrained labor market. This shortage affects service capacity and contributes to wage inflation that pressures operating margins. Regulatory compliance costs associated with hours of service requirements, electronic logging devices, and safety regulations create ongoing operational challenges.

Infrastructure limitations including highway congestion, bridge weight restrictions, and terminal capacity constraints affect operational efficiency and service reliability. These challenges are particularly acute in major metropolitan areas where traffic congestion impacts pickup and delivery schedules. Fuel price volatility creates cost uncertainty that requires sophisticated hedging strategies and fuel surcharge programs to manage financial risk.

Economic sensitivity makes the LTL sector vulnerable to industrial production cycles and business investment patterns. During economic downturns, reduced manufacturing activity and inventory destocking negatively impact freight volumes. Modal competition from parcel carriers, regional trucking companies, and intermodal transportation alternatives creates pricing pressure in certain market segments.

Technology investment requirements demand significant capital allocation for carriers to remain competitive in digital capabilities and operational automation. Smaller regional carriers may struggle to fund necessary technology upgrades while maintaining competitive pricing structures.

Digital transformation initiatives create opportunities for carriers to differentiate service offerings through advanced technology platforms and data analytics capabilities. The integration of artificial intelligence and machine learning technologies enables predictive maintenance, dynamic routing optimization, and enhanced customer service automation. Last-mile delivery expansion represents a significant growth opportunity as carriers extend services to final destination delivery.

Specialized services including temperature-controlled transportation, hazardous materials handling, and white glove delivery command premium pricing and higher margins. These niche markets often have less competition and stronger customer loyalty. Cross-border trade opportunities with Mexico and Canada provide additional revenue streams for carriers with appropriate operating authorities and customs expertise.

Sustainability initiatives create competitive advantages for carriers implementing environmental programs and alternative fuel technologies. Corporate customers increasingly prioritize suppliers with strong environmental credentials. Acquisition opportunities allow larger carriers to expand geographic coverage, acquire specialized capabilities, and achieve operational synergies through network consolidation.

Value-added services such as warehousing, distribution, and supply chain consulting enable carriers to capture additional revenue from existing customer relationships. These services often generate higher margins than traditional transportation and strengthen customer partnerships.

Competitive intensity within the United States LTL market reflects the balance between service quality, pricing competitiveness, and operational efficiency. Market leaders maintain advantages through extensive terminal networks that provide comprehensive geographic coverage and efficient freight consolidation capabilities. The sector demonstrates network effects where larger carriers achieve cost advantages through higher freight density and improved asset utilization.

Customer relationships play a critical role in market dynamics as businesses typically prefer working with a limited number of trusted LTL providers. This relationship-based approach creates switching costs that benefit established carriers with proven service reliability. Service differentiation increasingly focuses on technology capabilities, delivery speed, and specialized handling requirements rather than purely price-based competition.

Capacity management requires sophisticated demand forecasting and network optimization to balance service levels with operational efficiency. Carriers utilize dynamic pricing strategies to manage capacity during peak and off-peak periods. Seasonal variations in freight volumes require flexible operational models that can scale capacity appropriately while maintaining service quality standards.

Technology adoption continues reshaping market dynamics as carriers invest in automation, artificial intelligence, and digital customer interfaces. These investments create competitive moats while improving operational efficiency and customer satisfaction metrics.

Comprehensive analysis of the United States LTL market employs multiple research methodologies to ensure accuracy and completeness of market intelligence. Primary research includes structured interviews with industry executives, carrier management teams, and key customers to understand market trends, competitive dynamics, and operational challenges. This qualitative research provides insights into strategic decision-making processes and future market direction.

Secondary research encompasses analysis of public company financial reports, industry publications, regulatory filings, and trade association data. This quantitative foundation supports market sizing, trend analysis, and competitive benchmarking activities. Data validation processes ensure consistency and reliability across multiple information sources.

Market modeling techniques incorporate econometric analysis, regression modeling, and scenario planning to develop accurate market forecasts and trend projections. These analytical approaches consider macroeconomic factors, industry-specific drivers, and competitive dynamics that influence market performance. Expert consultation with industry specialists provides additional validation and insight into market developments.

Continuous monitoring of market conditions through ongoing research activities ensures that analysis remains current and relevant to market participants. This includes tracking regulatory changes, technology developments, and competitive actions that may impact market dynamics.

Geographic distribution of LTL market activity reflects regional economic patterns, manufacturing concentrations, and population centers across the United States. Northeast region maintains the highest freight density with approximately 28% market share due to concentrated industrial activity and urban population centers. This region benefits from established transportation infrastructure and proximity to major ports and distribution centers.

Southeast markets demonstrate strong growth momentum driven by manufacturing expansion, population migration, and distribution center development. This region accounts for approximately 24% of national LTL volume with continued growth expected from automotive, aerospace, and consumer goods industries. Infrastructure investment in ports and inland transportation facilities supports regional market expansion.

Midwest region represents approximately 22% of market activity with strength in manufacturing, agriculture, and industrial sectors. The region’s central location provides strategic advantages for national distribution networks. Great Lakes shipping connections and extensive rail networks complement LTL services for multimodal transportation solutions.

Western markets account for approximately 20% of LTL volume with growth driven by technology sector expansion, international trade through Pacific ports, and population growth in major metropolitan areas. Cross-border trade with Mexico creates additional opportunities for carriers with appropriate operating authorities. Mountain and Plains states represent the remaining 6% of market share with growth potential from energy sector development and agricultural exports.

Market leadership in the United States LTL sector is characterized by a relatively concentrated competitive structure with several major national carriers dominating market share. Competitive positioning depends on network coverage, service reliability, technology capabilities, and operational efficiency. The landscape includes both publicly traded corporations and privately held regional specialists.

Competitive strategies emphasize service differentiation, network optimization, and technology advancement to maintain market position. Acquisition activity continues as larger carriers seek to expand geographic coverage and acquire specialized capabilities. MWR analysis indicates that top-tier carriers maintain market share stability through superior service quality and customer relationship management.

Service segmentation within the United States LTL market reflects diverse customer requirements and operational characteristics. Standard LTL services represent the largest segment, providing cost-effective transportation for shipments between 150 and 15,000 pounds with typical transit times of 1-5 business days depending on distance and service level.

By Service Type:

By Industry Vertical:

Geographic segmentation considers regional market characteristics, service requirements, and competitive dynamics that vary across different areas of the United States.

Standard LTL services continue representing the core market segment with consistent demand from manufacturing and distribution customers. This category benefits from operational scale advantages and established customer relationships. Service reliability and competitive pricing remain primary customer selection criteria for standard services.

Expedited services command premium pricing while serving customers with time-sensitive delivery requirements. This segment demonstrates higher growth rates as supply chains adopt just-in-time inventory strategies. Technology integration enables real-time tracking and proactive communication that supports premium service positioning.

Specialized handling services including temperature-controlled, white glove, and hazardous materials transportation generate higher margins while serving niche market requirements. These services often require specialized equipment, trained personnel, and regulatory compliance capabilities that create competitive barriers.

Volume LTL services bridge the gap between standard LTL and full truckload transportation, serving customers with larger shipments that don’t require dedicated trailers. This category provides opportunities for carriers to optimize asset utilization while meeting specific customer requirements.

Last-mile delivery represents an emerging category as LTL carriers extend services to final destination delivery, particularly for business-to-business applications requiring appointment scheduling and specialized handling.

Shippers benefit from LTL services through cost-effective transportation solutions that eliminate the need for full truckload capacity when shipping smaller quantities. Consolidation advantages allow multiple shipments to share transportation costs while maintaining reliable delivery schedules. Network coverage provided by established LTL carriers enables businesses to reach customers throughout the United States without maintaining extensive logistics infrastructure.

Carriers achieve operational efficiency through freight consolidation and network optimization that maximizes asset utilization. Revenue diversification across multiple customers and industries provides stability during economic fluctuations. Technology investments create competitive advantages while improving operational efficiency and customer satisfaction.

Supply chain managers benefit from flexible transportation options that support inventory optimization and demand responsiveness. Visibility tools enable proactive management of freight movements and exception handling. Service reliability supports just-in-time inventory strategies and customer service commitments.

Economic stakeholders including communities and regions benefit from efficient freight transportation that supports local business development and economic growth. Employment opportunities in transportation, warehousing, and logistics sectors contribute to regional economic development. Infrastructure utilization through consolidated freight movements reduces highway congestion and environmental impact compared to individual shipment transportation.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation continues reshaping the LTL landscape as carriers invest in advanced technology platforms that enhance customer experience and operational efficiency. Artificial intelligence applications include route optimization, predictive maintenance, and automated customer service that improve service quality while reducing operational costs. Mobile applications provide customers with real-time shipment tracking and simplified booking processes.

Sustainability initiatives gain prominence as carriers implement environmental programs including alternative fuel vehicles, carbon offset programs, and green terminal facilities. Corporate customers increasingly prioritize suppliers with strong environmental credentials, creating competitive advantages for carriers with comprehensive sustainability programs.

Service diversification trends include expansion into last-mile delivery, warehousing services, and supply chain consulting that enable carriers to capture additional revenue from existing customer relationships. Value-added services often generate higher margins than traditional transportation while strengthening customer partnerships.

Network optimization through terminal consolidation, route efficiency improvements, and capacity management enables carriers to improve service reliability while controlling operational costs. Data analytics support decision-making processes for network planning, pricing optimization, and customer service improvements.

Customer experience enhancement through improved digital interfaces, proactive communication, and flexible service options becomes increasingly important for competitive differentiation and customer retention.

Technological advancement initiatives include implementation of autonomous vehicle technologies, blockchain applications for supply chain transparency, and Internet of Things sensors for real-time freight monitoring. Pilot programs for autonomous trucks focus on linehaul operations between terminals where controlled environments enable technology testing and validation.

Acquisition activity continues reshaping the competitive landscape as larger carriers acquire regional specialists to expand geographic coverage and service capabilities. Strategic partnerships between LTL carriers and technology companies enable rapid deployment of advanced digital platforms and operational automation systems.

Infrastructure investment programs include terminal modernization projects, automated sorting equipment installation, and fleet renewal initiatives that support capacity expansion and service improvement. Government infrastructure spending on highways and bridges benefits the LTL sector through improved transportation efficiency and reduced operational costs.

Regulatory developments include electronic logging device requirements, hours of service modifications, and environmental regulations that impact operational procedures and compliance costs. Safety initiatives focus on driver training programs, vehicle maintenance standards, and accident prevention technologies.

Market expansion efforts include cross-border service development, specialized vertical market penetration, and last-mile delivery capability development that create new revenue opportunities for established carriers.

Strategic recommendations for LTL market participants emphasize technology investment, service differentiation, and operational excellence as key success factors. MarkWide Research analysis suggests that carriers prioritizing digital transformation initiatives achieve customer retention rates that are 12-15% higher than industry averages while maintaining superior profitability metrics.

Network optimization should focus on terminal efficiency improvements, route optimization, and capacity management systems that enhance service reliability while controlling operational costs. Technology integration recommendations include artificial intelligence applications for predictive analytics, automated customer service systems, and real-time visibility platforms that improve customer experience.

Service portfolio expansion into specialized handling, last-mile delivery, and value-added logistics services provides opportunities for revenue diversification and margin improvement. Sustainability programs including alternative fuel adoption and carbon reduction initiatives create competitive advantages while supporting corporate customer requirements.

Customer relationship management should emphasize service quality consistency, proactive communication, and flexible service options that strengthen partnerships and reduce customer churn. Pricing strategies should balance competitiveness with profitability while reflecting service value and operational costs.

Acquisition opportunities should focus on strategic network expansion, specialized capability acquisition, and operational synergy realization that strengthen competitive positioning and market coverage.

Long-term prospects for the United States LTL market remain positive driven by continued economic growth, e-commerce expansion, and supply chain optimization trends. Technology advancement will continue reshaping operational capabilities and customer service standards while creating competitive advantages for early adopters. Market consolidation is expected to continue as larger carriers seek to expand network coverage and achieve operational synergies.

Growth projections indicate sustained expansion with the market expected to grow at a CAGR of 4.2% through the forecast period. E-commerce growth will drive demand for flexible shipping solutions and last-mile delivery services. Manufacturing reshoring trends support domestic freight volume growth and create new service opportunities.

Operational evolution will emphasize automation, artificial intelligence, and sustainability initiatives that improve efficiency while reducing environmental impact. Customer expectations for real-time visibility, flexible service options, and reliable delivery performance will continue driving service innovation and technology investment.

Competitive dynamics will increasingly focus on service differentiation, technology capabilities, and customer relationship management rather than purely price-based competition. Regulatory environment changes may impact operational procedures and compliance requirements while creating opportunities for carriers with strong compliance capabilities.

Investment priorities should focus on technology platforms, terminal modernization, and fleet renewal that support long-term competitive positioning and operational efficiency improvements.

The United States Less than-Truck-Load market represents a dynamic and essential component of the nation’s freight transportation infrastructure, serving diverse customer requirements through comprehensive network coverage and specialized service offerings. Market fundamentals remain strong with consistent demand from manufacturing, retail, and distribution sectors supporting sustained growth prospects.

Competitive success in this market requires balancing operational efficiency, service quality, and technology capabilities while maintaining cost competitiveness. Leading carriers demonstrate that investments in digital platforms, network optimization, and customer service excellence generate superior financial performance and market positioning.

Future opportunities include service diversification, technology advancement, and sustainability initiatives that create competitive advantages while meeting evolving customer expectations. Market participants that successfully navigate these trends while maintaining operational excellence will be well-positioned to capture growth opportunities and strengthen their competitive positioning in this vital transportation sector.

What is Less than-Truck-Load (LTL)?

Less than-Truck-Load (LTL) refers to a shipping method where multiple shipments from different customers are combined into one truckload. This approach is cost-effective for transporting smaller freight volumes and is commonly used in industries such as retail, manufacturing, and e-commerce.

What are the key players in the United States Less than-Truck-Load (LTL) Market?

Key players in the United States Less than-Truck-Load (LTL) Market include companies like FedEx Freight, XPO Logistics, and Old Dominion Freight Line. These companies provide a range of LTL services and have extensive networks to facilitate efficient freight movement, among others.

What are the growth factors driving the United States Less than-Truck-Load (LTL) Market?

The growth of the United States Less than-Truck-Load (LTL) Market is driven by the increasing demand for e-commerce logistics, the rise in small and medium-sized enterprises requiring flexible shipping options, and advancements in technology that enhance supply chain efficiency.

What challenges does the United States Less than-Truck-Load (LTL) Market face?

The United States Less than-Truck-Load (LTL) Market faces challenges such as fluctuating fuel prices, capacity constraints, and the need for improved infrastructure. These factors can impact service reliability and operational costs for LTL providers.

What opportunities exist in the United States Less than-Truck-Load (LTL) Market?

Opportunities in the United States Less than-Truck-Load (LTL) Market include the expansion of e-commerce, the integration of technology for better tracking and management, and the potential for sustainability initiatives to attract environmentally conscious customers.

What trends are shaping the United States Less than-Truck-Load (LTL) Market?

Trends shaping the United States Less than-Truck-Load (LTL) Market include the adoption of digital freight matching platforms, increased focus on sustainability practices, and the use of data analytics to optimize routes and improve service efficiency.

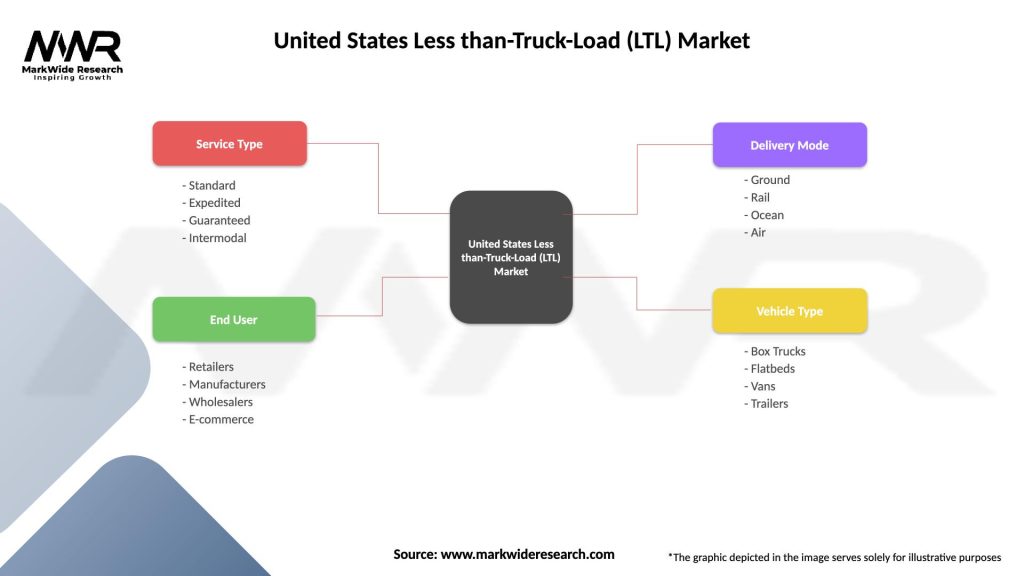

United States Less than-Truck-Load (LTL) Market

| Segmentation Details | Description |

|---|---|

| Service Type | Standard, Expedited, Guaranteed, Intermodal |

| End User | Retailers, Manufacturers, Wholesalers, E-commerce |

| Delivery Mode | Ground, Rail, Ocean, Air |

| Vehicle Type | Box Trucks, Flatbeds, Vans, Trailers |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the United States Less than-Truck-Load (LTL) Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.