444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The United States data center power market represents a critical infrastructure segment experiencing unprecedented growth driven by digital transformation, cloud computing expansion, and increasing data consumption patterns. Data center power systems encompass uninterruptible power supplies (UPS), power distribution units (PDUs), generators, transformers, and energy management solutions that ensure continuous operation of mission-critical facilities. The market demonstrates robust expansion with a projected CAGR of 8.2% through the forecast period, reflecting the escalating demand for reliable power infrastructure.

Market dynamics indicate substantial investments in hyperscale data centers, edge computing facilities, and colocation services across major metropolitan areas. The increasing adoption of artificial intelligence, machine learning, and Internet of Things (IoT) applications drives higher power density requirements, necessitating advanced power management solutions. Energy efficiency concerns and sustainability initiatives further accelerate the deployment of innovative power technologies, including lithium-ion battery systems and renewable energy integration.

Regional distribution shows concentrated growth in technology hubs such as Northern Virginia, Silicon Valley, Dallas-Fort Worth, and Chicago, where approximately 65% of hyperscale capacity is located. The market benefits from favorable regulatory environments, abundant land availability, and proximity to major internet exchanges, creating optimal conditions for data center development and associated power infrastructure investments.

The United States data center power market refers to the comprehensive ecosystem of electrical infrastructure, equipment, and services designed to provide reliable, efficient, and scalable power solutions for data center facilities across the country. This market encompasses primary power systems, backup power solutions, power distribution networks, monitoring systems, and energy management technologies that collectively ensure uninterrupted operation of computing infrastructure.

Data center power systems include multiple layers of redundancy and protection, from utility connections and on-site generation to battery backup systems and sophisticated power distribution architectures. The market covers both capital equipment sales and ongoing services including maintenance, monitoring, and optimization solutions that maximize uptime while minimizing operational costs and environmental impact.

Market expansion in the United States data center power sector reflects the accelerating digitization of business operations and the proliferation of cloud-based services. The market demonstrates strong fundamentals driven by hyperscale cloud providers, enterprise digital transformation initiatives, and emerging technologies requiring substantial computing resources. Power density increases of approximately 12% annually challenge traditional infrastructure approaches, driving innovation in cooling integration and energy efficiency solutions.

Technology evolution toward higher efficiency power systems, modular architectures, and intelligent monitoring capabilities creates significant opportunities for market participants. The integration of renewable energy sources and energy storage systems addresses sustainability requirements while providing operational cost benefits. Edge computing deployment expands market reach beyond traditional data center locations, requiring distributed power solutions and standardized deployment models.

Competitive dynamics feature established infrastructure providers, emerging technology companies, and integrated solution providers competing across multiple market segments. The market benefits from strong demand fundamentals, technological innovation cycles, and increasing recognition of power infrastructure as a strategic competitive advantage for data center operators.

Strategic market developments reveal several critical trends shaping the United States data center power landscape:

Digital transformation initiatives across industries create sustained demand for data center capacity and associated power infrastructure. Enterprise migration to cloud platforms, adoption of software-as-a-service solutions, and implementation of digital business models drive consistent growth in computing requirements. Data generation from IoT devices, social media platforms, and business applications continues expanding at exponential rates, necessitating additional processing and storage capacity.

Artificial intelligence and machine learning workloads represent particularly significant drivers, requiring specialized computing architectures with higher power densities than traditional applications. The proliferation of AI applications across industries, from autonomous vehicles to financial services, creates sustained demand for high-performance computing infrastructure. 5G network deployment enables new applications and services requiring edge computing capabilities, expanding the geographic footprint of data center power requirements.

Regulatory compliance and data sovereignty requirements drive enterprises to maintain domestic data processing capabilities, supporting continued investment in United States data center infrastructure. Financial services, healthcare, and government sectors demonstrate particular sensitivity to data location requirements, creating stable demand for domestic facilities and associated power systems.

Capital intensity of data center power infrastructure creates barriers for smaller market participants and limits deployment flexibility. High upfront costs for redundant power systems, specialized equipment, and professional installation services require substantial financial commitments that may constrain market entry or expansion plans. Technical complexity of modern power systems demands specialized expertise for design, installation, and maintenance, creating potential bottlenecks in market growth.

Grid capacity constraints in high-demand metropolitan areas limit new data center development and associated power infrastructure investments. Utility infrastructure limitations, permitting delays, and interconnection challenges create obstacles for rapid capacity expansion. Environmental regulations and sustainability requirements add complexity and cost to power system design and operation, particularly for backup generation systems.

Supply chain vulnerabilities for critical power components create potential disruptions and cost pressures. Global semiconductor shortages, raw material price volatility, and manufacturing capacity constraints impact equipment availability and project timelines. Skilled workforce limitations in power systems engineering and maintenance create operational challenges for market participants.

Edge computing expansion creates substantial opportunities for distributed power solutions and standardized deployment models. The proliferation of edge locations requires scalable, efficient power systems that can operate with minimal on-site technical support. Renewable energy integration offers opportunities for innovative power system designs that combine grid connectivity, on-site generation, and energy storage capabilities.

Energy storage technologies present significant growth potential as battery costs decline and performance improves. Advanced battery systems enable improved power quality, reduced utility costs, and enhanced sustainability profiles for data center operations. Power-as-a-Service models create opportunities for recurring revenue streams and closer customer relationships through comprehensive service offerings.

Artificial intelligence applications in power management and optimization create opportunities for intelligent systems that automatically adjust power distribution, predict maintenance requirements, and optimize energy consumption. Modular power solutions enable faster deployment, improved scalability, and reduced installation complexity, addressing key customer requirements in rapidly growing markets.

Supply and demand dynamics in the United States data center power market reflect the interplay between rapidly growing capacity requirements and infrastructure development capabilities. Demand acceleration from cloud computing, artificial intelligence, and digital transformation initiatives consistently outpaces supply additions, creating favorable pricing conditions and strong utilization rates for existing facilities.

Technology evolution drives continuous improvement in power system efficiency, reliability, and functionality. The transition from traditional lead-acid batteries to lithium-ion systems demonstrates efficiency improvements of 15-20% while reducing space requirements and maintenance costs. Smart power management systems enable real-time optimization and predictive maintenance capabilities that improve overall system performance.

Competitive intensity varies across market segments, with established infrastructure providers maintaining strong positions in large-scale deployments while emerging companies focus on specialized applications and innovative technologies. Customer consolidation among hyperscale providers creates opportunities for preferred supplier relationships while increasing competitive pressure on pricing and service levels.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into the United States data center power market. Primary research includes extensive interviews with industry executives, technology providers, data center operators, and end-users to gather firsthand perspectives on market trends, challenges, and opportunities. Survey methodologies capture quantitative data on market preferences, adoption patterns, and investment priorities.

Secondary research incorporates analysis of industry publications, regulatory filings, company annual reports, and technical specifications to validate primary findings and identify emerging trends. Market modeling techniques combine historical data analysis with forward-looking projections based on identified growth drivers and market dynamics. MarkWide Research analytical frameworks ensure consistent methodology application and reliable market sizing approaches.

Data validation processes include cross-referencing multiple sources, expert review panels, and statistical analysis to ensure accuracy and reliability of market insights. Continuous monitoring of market developments, technology announcements, and regulatory changes maintains current perspective on rapidly evolving market conditions.

Northern Virginia maintains its position as the largest data center market in the United States, accounting for approximately 25% of total capacity and representing the highest concentration of hyperscale facilities. The region benefits from proximity to government agencies, excellent fiber connectivity, and supportive local policies that facilitate data center development. Power infrastructure investments in the region focus on grid reliability improvements and renewable energy integration to support continued growth.

Silicon Valley and the broader San Francisco Bay Area represent the second-largest market concentration, driven by technology company headquarters and cloud provider operations. The region demonstrates strong demand for high-density power solutions and sustainable energy sources, reflecting environmental priorities and operational efficiency requirements. Regulatory environment emphasizes renewable energy adoption and energy efficiency standards that influence power system design and operation.

Dallas-Fort Worth emerges as a rapidly growing market benefiting from central geographic location, favorable business climate, and abundant land availability. The region attracts hyperscale deployments and enterprise data centers serving national markets, creating substantial demand for scalable power infrastructure. Chicago maintains strong market position as a financial services hub and network interconnection point, supporting diverse data center applications and associated power requirements.

Emerging markets including Atlanta, Phoenix, and Denver demonstrate accelerating growth driven by edge computing deployments and regional enterprise requirements. These markets benefit from lower costs, available land, and improving fiber connectivity while maintaining proximity to major population centers.

Market leadership in the United States data center power sector features established infrastructure providers with comprehensive product portfolios and extensive service capabilities:

Competitive differentiation focuses on technology innovation, service capabilities, energy efficiency, and integrated solution offerings that address comprehensive customer requirements. Strategic partnerships between power providers and data center operators create preferred supplier relationships and collaborative product development initiatives.

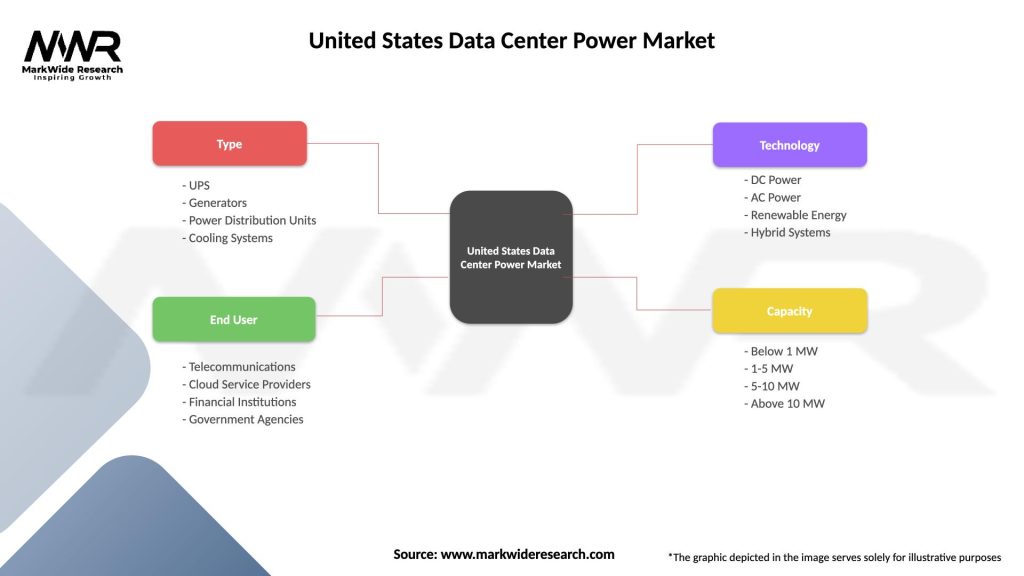

By Component:

By Data Center Type:

By Power Rating:

UPS Systems represent the largest component segment, driven by critical power protection requirements and increasing power density demands. Modular UPS architectures gain market share due to scalability advantages and improved efficiency characteristics. The segment demonstrates strong growth in lithium-ion battery integration, achieving 30% adoption rate in new installations due to space savings and performance benefits.

Power Distribution Units experience rapid growth driven by intelligent monitoring and control capabilities that enable remote management and optimization. Smart PDUs with advanced metering and switching capabilities become standard requirements for modern data center deployments, supporting both operational efficiency and sustainability initiatives.

Generator Systems maintain steady demand driven by reliability requirements and grid resilience concerns. Natural gas generators gain preference over diesel systems in urban areas due to environmental considerations and fuel availability advantages. The segment benefits from improved efficiency and reduced emissions through advanced engine technologies.

Battery Systems undergo significant transformation with lithium-ion technology adoption accelerating due to performance advantages and declining costs. Energy storage integration enables demand charge management and grid services participation, creating additional value streams beyond backup power applications.

Data Center Operators benefit from improved reliability, enhanced efficiency, and reduced operational costs through advanced power management systems. Intelligent monitoring capabilities enable predictive maintenance and optimization strategies that minimize downtime risks while maximizing asset utilization. Scalable architectures support rapid capacity expansion and changing power requirements without major infrastructure modifications.

Technology Providers gain access to growing market opportunities driven by digital transformation and cloud computing adoption. Service integration creates recurring revenue opportunities and stronger customer relationships through comprehensive support offerings. Innovation leadership in efficiency and sustainability enables premium positioning and competitive differentiation.

End Users achieve improved application performance and business continuity through reliable power infrastructure. Energy efficiency improvements reduce operational costs and support corporate sustainability objectives. Standardized solutions enable faster deployment and simplified management across multiple locations.

Utility Companies benefit from improved grid stability and demand management through intelligent data center power systems. Demand response capabilities enable grid services participation and load optimization during peak periods. Renewable energy integration supports clean energy adoption and grid modernization initiatives.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability Integration emerges as a dominant trend driving adoption of renewable energy sources, energy storage systems, and high-efficiency power technologies. Corporate environmental commitments from major cloud providers and enterprises create demand for clean energy solutions and carbon-neutral operations. Circular economy principles influence product design and end-of-life management strategies.

Artificial Intelligence Applications in power management enable predictive maintenance, automated optimization, and intelligent load balancing capabilities. Machine learning algorithms analyze power consumption patterns and environmental conditions to optimize system performance and prevent failures. Digital twin technologies enable virtual modeling and simulation for improved system design and operation.

Modular Deployment Models gain adoption due to faster installation, improved scalability, and standardized configurations that reduce complexity and costs. Prefabricated power modules enable factory testing and quality control while accelerating on-site deployment timelines. Containerized solutions support edge computing applications and temporary capacity requirements.

Edge Computing Expansion drives demand for distributed power solutions that operate reliably with minimal local support. Standardized designs enable consistent deployment across multiple locations while reducing engineering and maintenance requirements. Remote monitoring capabilities ensure reliable operation and proactive maintenance support.

Technology Partnerships between power providers and data center operators accelerate innovation and deployment of advanced power management solutions. Collaborative development programs focus on efficiency improvements, sustainability initiatives, and operational optimization capabilities. Strategic alliances enable integrated solution offerings and comprehensive customer support.

Acquisition Activity consolidates market participants and creates comprehensive solution providers with expanded capabilities and geographic reach. Vertical integration strategies enable better control over supply chains and customer relationships while improving operational efficiency. Technology acquisitions accelerate innovation and market entry in emerging segments.

Regulatory Developments influence power system design and operation through environmental standards, safety requirements, and grid interconnection rules. Energy efficiency mandates drive adoption of high-performance systems and intelligent management capabilities. Renewable energy incentives support integration of clean energy sources and storage systems.

Infrastructure Investments by utilities and government agencies improve grid reliability and support data center growth in key markets. Smart grid initiatives enable advanced demand management and grid services participation by data center facilities. Transmission upgrades increase available capacity and improve power quality in high-demand areas.

Strategic Focus on sustainability and efficiency becomes critical for long-term market success as environmental requirements and operational cost pressures intensify. MWR analysis indicates that companies investing in clean energy integration and advanced efficiency technologies achieve stronger market positioning and customer preference. Innovation investment in artificial intelligence and automation capabilities creates competitive advantages and operational differentiation.

Service Integration strategies enable stronger customer relationships and recurring revenue streams while providing comprehensive support for complex power systems. Predictive maintenance and remote monitoring capabilities become standard customer expectations, requiring investment in digital technologies and service capabilities. Partnership development with complementary technology providers expands solution capabilities and market reach.

Geographic Expansion into emerging data center markets provides growth opportunities while diversifying market exposure and reducing concentration risks. Edge computing applications require distributed service capabilities and standardized solution offerings that can operate with minimal local support. International expansion leverages United States technology leadership and market experience in global markets.

Talent Development in power systems engineering, digital technologies, and service delivery becomes critical for supporting market growth and maintaining competitive positioning. Training programs and certification initiatives ensure adequate skilled workforce availability for installation, maintenance, and support services. Technology partnerships with educational institutions support workforce development and innovation initiatives.

Market expansion continues through the forecast period driven by sustained demand for data center capacity and associated power infrastructure. Digital transformation initiatives across industries create consistent growth in computing requirements while artificial intelligence applications drive higher power density demands. Edge computing deployment expands market reach and creates opportunities for distributed power solutions.

Technology evolution toward higher efficiency, greater intelligence, and improved sustainability characteristics shapes product development and market competition. Battery technology advancement enables improved performance and cost-effectiveness while supporting grid services and renewable energy integration. Automation capabilities reduce operational complexity and improve system reliability through predictive maintenance and intelligent optimization.

Regulatory environment increasingly emphasizes environmental performance and energy efficiency, driving adoption of clean energy technologies and high-performance power systems. Grid modernization initiatives improve power quality and reliability while enabling advanced demand management and grid services participation. Sustainability requirements become standard procurement criteria for major data center operators and enterprise customers.

Competitive dynamics favor companies with comprehensive solution capabilities, strong service offerings, and demonstrated sustainability leadership. Market consolidation continues as companies seek scale advantages and expanded capabilities through strategic acquisitions and partnerships. Innovation leadership in efficiency, reliability, and intelligent management creates sustainable competitive advantages and premium market positioning.

The United States data center power market demonstrates robust growth prospects driven by fundamental technology trends and increasing digitization across industries. Market dynamics favor established providers with comprehensive capabilities while creating opportunities for innovative companies addressing emerging requirements such as edge computing and sustainability initiatives. The projected 8.2% CAGR reflects sustained demand fundamentals and continuous technology evolution.

Strategic success factors include technology leadership in efficiency and reliability, comprehensive service capabilities, and strong sustainability credentials that address evolving customer requirements. Market participants must balance innovation investment with operational excellence while building scalable business models that support geographic expansion and diverse customer segments. The integration of artificial intelligence, renewable energy, and advanced battery technologies creates significant opportunities for differentiation and value creation.

Future market development depends on continued digital transformation, artificial intelligence adoption, and edge computing deployment that drive sustained demand for reliable, efficient power infrastructure. Regulatory support for clean energy and grid modernization initiatives creates favorable conditions for technology advancement and market expansion. The United States data center power market remains well-positioned for continued growth and innovation, offering substantial opportunities for companies with strategic vision and execution capabilities.

What is Data Center Power?

Data Center Power refers to the electrical power supply and management systems that support the operation of data centers, which house computer systems and associated components. This includes power distribution, backup systems, and energy efficiency measures.

What are the key players in the United States Data Center Power Market?

Key players in the United States Data Center Power Market include companies like Schneider Electric, Vertiv, and Eaton, which provide power management solutions and infrastructure for data centers, among others.

What are the main drivers of growth in the United States Data Center Power Market?

The main drivers of growth in the United States Data Center Power Market include the increasing demand for cloud computing services, the rise of big data analytics, and the need for energy-efficient power solutions to reduce operational costs.

What challenges does the United States Data Center Power Market face?

Challenges in the United States Data Center Power Market include the high energy consumption of data centers, regulatory pressures for sustainability, and the need for continuous upgrades to power infrastructure to keep pace with technological advancements.

What opportunities exist in the United States Data Center Power Market?

Opportunities in the United States Data Center Power Market include the development of renewable energy sources for power supply, advancements in energy storage technologies, and the growing trend of modular data centers that enhance flexibility and efficiency.

What trends are shaping the United States Data Center Power Market?

Trends shaping the United States Data Center Power Market include the adoption of artificial intelligence for power management, the integration of edge computing, and a focus on sustainability initiatives to minimize carbon footprints.

United States Data Center Power Market

| Segmentation Details | Description |

|---|---|

| Type | UPS, Generators, Power Distribution Units, Cooling Systems |

| End User | Telecommunications, Cloud Service Providers, Financial Institutions, Government Agencies |

| Technology | DC Power, AC Power, Renewable Energy, Hybrid Systems |

| Capacity | Below 1 MW, 1-5 MW, 5-10 MW, Above 10 MW |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the United States Data Center Power Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.