444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The United Kingdom data center construction market represents a dynamic and rapidly evolving sector that has become fundamental to the nation’s digital infrastructure. Data center construction encompasses the planning, design, and building of specialized facilities that house critical IT infrastructure, servers, networking equipment, and storage systems. The UK market has experienced remarkable transformation driven by increasing digitalization, cloud computing adoption, and the growing demand for edge computing solutions.

Market dynamics in the UK data center construction sector reflect the country’s position as a leading European digital hub. The market has witnessed substantial growth with a projected CAGR of 8.2% over the forecast period, driven by increasing data consumption, regulatory requirements, and the need for enhanced digital services. London continues to dominate the market landscape, accounting for approximately 65% of total data center capacity in the UK, while emerging markets in Manchester, Birmingham, and Edinburgh are gaining significant traction.

Investment patterns in the UK data center construction market demonstrate strong confidence from both domestic and international players. The sector has attracted substantial capital from hyperscale cloud providers, colocation specialists, and enterprise organizations seeking to establish robust digital infrastructure. Sustainability initiatives have become increasingly important, with 72% of new data center projects incorporating renewable energy sources and advanced cooling technologies to meet environmental targets.

The United Kingdom data center construction market refers to the comprehensive ecosystem of activities, services, and investments involved in designing, building, and delivering specialized facilities that support digital infrastructure requirements across the UK. This market encompasses various stakeholders including construction companies, technology providers, real estate developers, and end-users who collaborate to create state-of-the-art data storage and processing facilities.

Data center construction involves multiple specialized components including structural engineering, electrical systems, cooling infrastructure, security systems, and network connectivity solutions. The market includes various facility types ranging from hyperscale data centers serving major cloud providers to edge computing facilities supporting low-latency applications and enterprise data centers meeting specific organizational requirements.

Market participants include construction contractors, mechanical and electrical specialists, technology integrators, and facility management providers who work together to deliver comprehensive data center solutions. The UK market is characterized by stringent regulatory requirements, advanced sustainability standards, and sophisticated technical specifications that drive innovation and best practices in data center construction methodologies.

Strategic positioning of the UK data center construction market reflects the country’s role as a critical digital gateway between Europe and global markets. The market has demonstrated resilience and growth potential despite economic uncertainties, with increasing demand from cloud service providers, financial institutions, and government organizations driving construction activity across multiple regions.

Key growth drivers include the accelerating digital transformation initiatives, increasing data sovereignty requirements, and the expansion of edge computing networks. The market has benefited from favorable government policies supporting digital infrastructure development, with 45% of organizations planning significant data center investments over the next three years. Sustainability considerations have become paramount, influencing design decisions and construction methodologies across the sector.

Competitive dynamics in the UK data center construction market feature a mix of international construction giants, specialized data center builders, and local contractors with deep market knowledge. The sector has witnessed increased consolidation and strategic partnerships as companies seek to enhance their technical capabilities and market reach. Innovation trends focus on modular construction techniques, advanced cooling systems, and integrated renewable energy solutions that address both performance and environmental requirements.

Market segmentation reveals diverse opportunities across different facility types and end-user categories. The UK data center construction market demonstrates strong demand across multiple sectors, with each segment presenting unique requirements and growth characteristics that influence construction approaches and investment strategies.

Regional distribution patterns show concentration in key metropolitan areas while emerging markets gain momentum. London maintains its dominant position due to connectivity advantages and market maturity, while regions like Manchester and Birmingham offer cost advantages and strategic positioning for national coverage.

Digital transformation acceleration represents the primary driver of UK data center construction demand. Organizations across all sectors are implementing comprehensive digitalization strategies that require robust, scalable, and secure data infrastructure. The shift toward cloud-first strategies has created unprecedented demand for data center capacity, with 78% of UK businesses planning to increase their cloud infrastructure investments significantly.

Regulatory compliance requirements continue to drive data center construction activity as organizations seek to meet evolving data protection and sovereignty requirements. GDPR compliance, financial services regulations, and government data localization mandates create strong demand for UK-based data center facilities that can ensure regulatory adherence while maintaining operational efficiency.

Edge computing expansion has emerged as a significant growth driver, with organizations requiring distributed data processing capabilities to support Internet of Things (IoT) applications, autonomous systems, and real-time analytics. The proliferation of 5G networks further accelerates edge computing requirements, creating demand for smaller, strategically located data centers across the UK.

Sustainability imperatives drive innovation in data center construction as organizations seek to meet ambitious environmental targets. The UK government’s commitment to net-zero emissions by 2050 has created strong demand for energy-efficient data centers incorporating renewable energy sources, advanced cooling technologies, and sustainable construction materials.

High capital requirements present significant barriers to entry in the UK data center construction market. The substantial upfront investments required for land acquisition, construction, and technology infrastructure can limit market participation and slow project development timelines. Financing challenges particularly affect smaller players and specialized projects that may struggle to secure adequate funding.

Skilled labor shortages continue to constrain market growth as the specialized nature of data center construction requires experienced professionals with specific technical expertise. The shortage of qualified mechanical and electrical engineers, project managers, and specialized technicians has led to increased labor costs and extended project timelines across the sector.

Planning and regulatory complexities can significantly delay data center construction projects in the UK. Local planning authorities often require extensive environmental assessments, community consultations, and infrastructure impact studies that can extend approval processes. Grid connection challenges and power availability constraints in certain regions further complicate project development.

Environmental concerns and community opposition can create obstacles for data center construction projects, particularly in residential areas or environmentally sensitive locations. Concerns about energy consumption, noise levels, and visual impact require careful project planning and community engagement to ensure successful project completion.

Emerging technologies create substantial opportunities for innovation in UK data center construction. The integration of artificial intelligence, machine learning, and advanced automation systems presents opportunities for construction companies to differentiate their offerings and improve project efficiency. Modular construction techniques offer potential for faster deployment and cost optimization.

Regional expansion beyond traditional markets presents significant growth opportunities as organizations seek geographic diversification and cost optimization. Cities like Newcastle, Cardiff, and Glasgow offer attractive propositions with lower land costs, available power infrastructure, and skilled workforce availability.

Retrofit and modernization of existing facilities represent a growing market opportunity as organizations seek to upgrade aging infrastructure to meet current performance and efficiency standards. The legacy data center upgrade market offers potential for specialized contractors with expertise in complex renovation projects.

Sustainability solutions present opportunities for companies specializing in green construction technologies, renewable energy integration, and energy-efficient systems. The growing emphasis on carbon neutrality creates demand for innovative construction approaches that minimize environmental impact while maintaining operational performance.

Supply and demand dynamics in the UK data center construction market reflect the complex interplay between increasing digital infrastructure requirements and construction industry capacity constraints. Demand patterns show strong growth across multiple sectors, with particularly robust requirements from cloud service providers, financial institutions, and government organizations.

Technology evolution continues to influence market dynamics as new computing paradigms require different infrastructure approaches. The shift toward high-performance computing, artificial intelligence workloads, and quantum computing creates demand for specialized facility designs with enhanced power density and cooling capabilities.

Competitive pressures drive innovation and efficiency improvements across the construction value chain. Companies are investing in advanced project management systems, building information modeling (BIM) technologies, and prefabrication techniques to improve project delivery speed and quality while managing costs effectively.

Market consolidation trends reflect the increasing scale and complexity of data center construction projects. Strategic partnerships between construction companies, technology providers, and real estate developers create integrated service offerings that can address comprehensive client requirements more effectively.

Comprehensive market analysis for the UK data center construction market employs multiple research methodologies to ensure accurate and reliable insights. Primary research includes extensive interviews with industry executives, construction professionals, technology providers, and end-users to gather firsthand market intelligence and validate market trends.

Secondary research encompasses analysis of industry reports, government publications, regulatory filings, and company financial statements to establish market context and quantitative foundations. Market sizing methodologies combine top-down and bottom-up approaches to ensure accuracy and comprehensiveness in market assessment.

Data validation processes include cross-referencing multiple sources, expert consultations, and statistical analysis to ensure research reliability. MarkWide Research employs rigorous quality control measures throughout the research process to maintain the highest standards of accuracy and objectivity in market analysis.

Forecasting methodologies utilize advanced statistical models, scenario analysis, and expert judgment to project future market trends and growth patterns. The research incorporates various economic, technological, and regulatory factors that influence market development to provide comprehensive forward-looking insights.

London maintains its position as the dominant region in the UK data center construction market, accounting for the majority of construction activity and investment. The capital’s advantages include superior connectivity infrastructure, proximity to financial markets, and established ecosystem of technology providers and service companies. Greater London continues to attract major hyperscale projects despite higher land costs and planning complexities.

Manchester has emerged as a significant secondary market, offering attractive cost advantages while maintaining excellent connectivity to major UK cities. The region benefits from available land, competitive labor costs, and strong government support for digital infrastructure development. Manchester’s data center market has grown by approximately 35% over the past three years.

Birmingham represents another key growth region, leveraging its central UK location and excellent transport links. The city offers strategic advantages for organizations seeking national coverage while benefiting from lower operational costs compared to London. West Midlands has attracted significant investment from both domestic and international data center operators.

Scotland, particularly around Edinburgh and Glasgow, presents attractive opportunities with abundant renewable energy resources, cooler climate conditions, and supportive government policies. The region’s focus on sustainable technology aligns well with data center operators’ environmental objectives, creating a favorable investment climate.

Market leadership in the UK data center construction sector features a diverse mix of international construction giants, specialized data center builders, and technology-focused contractors. The competitive landscape reflects the complex requirements of modern data center projects that demand expertise across multiple technical disciplines.

Competitive strategies focus on developing specialized expertise, forming strategic partnerships, and investing in advanced construction technologies. Companies are differentiating themselves through sustainability credentials, speed of delivery, and technical innovation to capture market share in this growing sector.

By Facility Type:

By End-User Industry:

By Construction Type:

Hyperscale data centers represent the fastest-growing segment in the UK market, driven by major cloud providers expanding their European infrastructure. These facilities require specialized construction approaches focusing on standardization, efficiency, and scalability. Construction timelines typically range from 18-24 months for large-scale projects, with emphasis on power density optimization and cooling efficiency.

Colocation facilities continue to show strong growth as organizations seek flexible, cost-effective data center solutions. These projects require sophisticated design approaches to accommodate diverse tenant requirements while maintaining operational efficiency. Multi-tenant considerations drive complex mechanical and electrical designs that can support varying power densities and cooling requirements.

Edge computing facilities represent an emerging category with unique construction requirements. These smaller, distributed facilities require rapid deployment capabilities, remote monitoring systems, and standardized designs that can be replicated across multiple locations. Construction approaches emphasize modular techniques and prefabrication to enable faster market deployment.

Enterprise data centers demand highly customized construction approaches tailored to specific organizational requirements. These projects often involve complex integration with existing infrastructure and require specialized security, compliance, and operational considerations that influence construction methodologies and timelines.

Construction companies benefit from the UK data center construction market through access to high-value, technically sophisticated projects that command premium pricing. The sector offers opportunities for long-term partnerships with major technology companies and the development of specialized expertise that creates competitive advantages in related markets.

Technology providers gain access to a growing market for specialized data center equipment, systems, and services. The UK market’s emphasis on innovation and sustainability creates opportunities for companies developing advanced cooling systems, power management solutions, and monitoring technologies.

Real estate developers benefit from strong demand for data center-suitable properties and development opportunities. The sector offers attractive long-term lease arrangements and stable rental income streams that appeal to institutional investors seeking predictable returns.

End-users benefit from improved data center infrastructure that supports their digital transformation initiatives. Modern facilities offer enhanced reliability, security, and efficiency that enable organizations to focus on their core business activities while ensuring robust IT infrastructure support.

Local communities benefit from job creation, tax revenue generation, and infrastructure improvements associated with data center construction projects. Many projects contribute to local economic development while supporting the broader digital economy growth.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability integration has become a dominant trend in UK data center construction, with 85% of new projects incorporating renewable energy sources and advanced energy efficiency measures. Green building certifications, carbon-neutral operations, and circular economy principles are increasingly influencing design decisions and construction methodologies across the sector.

Modular construction adoption is accelerating as organizations seek faster deployment and cost optimization. Prefabricated data center modules enable reduced construction timelines while maintaining quality standards and technical specifications. This trend particularly benefits edge computing deployments and rapid capacity expansion requirements.

Artificial intelligence integration is transforming data center construction through smart building systems, predictive maintenance capabilities, and automated operations. Construction projects increasingly incorporate IoT sensors, advanced monitoring systems, and machine learning algorithms to optimize facility performance and operational efficiency.

Edge computing proliferation is driving demand for distributed data center infrastructure across the UK. The trend toward localized data processing creates opportunities for smaller, strategically located facilities that support low-latency applications and real-time analytics requirements.

Hybrid cloud strategies are influencing data center construction as organizations seek flexible infrastructure solutions that can support both private and public cloud requirements. This trend drives demand for interconnected facilities and multi-cloud connectivity capabilities.

Major infrastructure investments continue to reshape the UK data center construction landscape. Recent developments include significant capacity expansions by leading cloud providers, new colocation facility announcements, and strategic partnerships between construction companies and technology providers that enhance market capabilities.

Regulatory developments have influenced construction standards and operational requirements. New energy efficiency regulations, environmental impact assessments, and data sovereignty requirements are driving changes in facility design and construction approaches across the sector.

Technology partnerships between construction companies and equipment manufacturers are creating integrated solutions that improve project delivery efficiency. These collaborations focus on standardized designs, optimized supply chains, and advanced construction techniques that reduce costs and timelines.

Sustainability initiatives have gained momentum with several major projects achieving carbon-neutral operations and renewable energy integration. Industry leaders are setting ambitious environmental targets that influence construction practices and technology selection across the market.

Skills development programs have been launched to address workforce challenges in the sector. Industry associations, educational institutions, and construction companies are collaborating to develop specialized training programs that build technical expertise in data center construction.

Strategic positioning recommendations for market participants emphasize the importance of developing specialized expertise in data center construction while maintaining flexibility to adapt to evolving technology requirements. MWR analysis suggests that companies should invest in advanced construction techniques, sustainability capabilities, and strategic partnerships to capture growth opportunities.

Geographic diversification strategies should consider emerging markets beyond traditional centers while maintaining presence in core regions. Companies should evaluate opportunities in secondary cities that offer cost advantages and strategic positioning for national coverage while building relationships with local stakeholders.

Technology investment priorities should focus on digital construction tools, project management systems, and sustainability technologies that improve efficiency and differentiate service offerings. Companies should consider partnerships with technology providers to access advanced capabilities without significant capital investment.

Workforce development initiatives should address skills shortages through training programs, recruitment strategies, and retention policies that build technical expertise. Companies should invest in continuous learning programs that keep pace with evolving technology requirements and construction methodologies.

Sustainability leadership can create competitive advantages as environmental considerations become increasingly important in project selection. Companies should develop expertise in green construction, renewable energy integration, and energy efficiency optimization to meet growing market demand.

Long-term growth prospects for the UK data center construction market remain positive, driven by continued digital transformation, cloud adoption, and emerging technology requirements. MarkWide Research projects sustained growth with a CAGR of 8.2% over the next five years, supported by strong demand across multiple sectors and continued investment in digital infrastructure.

Technology evolution will continue to influence construction requirements as new computing paradigms emerge. Quantum computing, advanced AI workloads, and high-performance computing applications will drive demand for specialized facility designs with enhanced power density and cooling capabilities.

Sustainability imperatives will become increasingly important as organizations seek to meet ambitious environmental targets. Future construction projects will likely incorporate advanced renewable energy systems, innovative cooling technologies, and circular economy principles that minimize environmental impact while maintaining operational performance.

Regional development patterns suggest continued expansion beyond traditional markets as organizations seek geographic diversification and cost optimization. Secondary cities and emerging regions will likely capture increasing market share while maintaining connectivity to major business centers.

Market consolidation trends may accelerate as the scale and complexity of projects increase. Strategic partnerships, acquisitions, and joint ventures will likely reshape the competitive landscape as companies seek to enhance their capabilities and market reach in this growing sector.

The United Kingdom data center construction market represents a dynamic and rapidly evolving sector that plays a crucial role in supporting the nation’s digital infrastructure requirements. Market fundamentals remain strong, driven by increasing digitalization, cloud adoption, and emerging technology requirements that create sustained demand for modern data center facilities.

Growth opportunities exist across multiple segments and regions, with particular potential in edge computing, sustainability solutions, and regional expansion beyond traditional markets. The market’s emphasis on innovation, efficiency, and environmental responsibility creates opportunities for companies that can deliver advanced construction solutions while meeting evolving client requirements.

Success factors in the UK data center construction market include specialized technical expertise, strategic partnerships, sustainability leadership, and the ability to adapt to rapidly changing technology requirements. Companies that invest in these capabilities while maintaining operational excellence will be well-positioned to capture growth opportunities in this expanding market.

The future outlook for the UK data center construction market remains positive, with continued growth expected across multiple sectors and regions. As digital transformation accelerates and new technologies emerge, the demand for sophisticated, efficient, and sustainable data center infrastructure will continue to drive market expansion and create opportunities for industry participants who can deliver innovative construction solutions.

What is Data Center Construction?

Data Center Construction refers to the process of building facilities that house computer systems and associated components, such as telecommunications and storage systems. These facilities are designed to support the growing demand for data processing and storage in various industries.

What are the key players in the United Kingdom Data Center Construction Market?

Key players in the United Kingdom Data Center Construction Market include companies like Equinix, Digital Realty, and Interxion, which are known for their significant contributions to data center infrastructure. These companies focus on providing robust and scalable solutions to meet the increasing data demands, among others.

What are the main drivers of the United Kingdom Data Center Construction Market?

The main drivers of the United Kingdom Data Center Construction Market include the rapid growth of cloud computing, the increasing demand for data storage, and the rise of big data analytics. These factors are pushing companies to invest in new data center facilities to enhance their operational capabilities.

What challenges does the United Kingdom Data Center Construction Market face?

The United Kingdom Data Center Construction Market faces challenges such as high energy costs, regulatory compliance issues, and the need for sustainable building practices. These challenges can impact project timelines and overall costs for construction companies.

What opportunities exist in the United Kingdom Data Center Construction Market?

Opportunities in the United Kingdom Data Center Construction Market include the growing demand for edge computing facilities and the expansion of renewable energy sources for powering data centers. These trends present avenues for innovation and investment in more efficient and sustainable data center designs.

What trends are shaping the United Kingdom Data Center Construction Market?

Trends shaping the United Kingdom Data Center Construction Market include the adoption of modular construction techniques and the integration of advanced cooling technologies. These innovations aim to improve energy efficiency and reduce the environmental impact of data center operations.

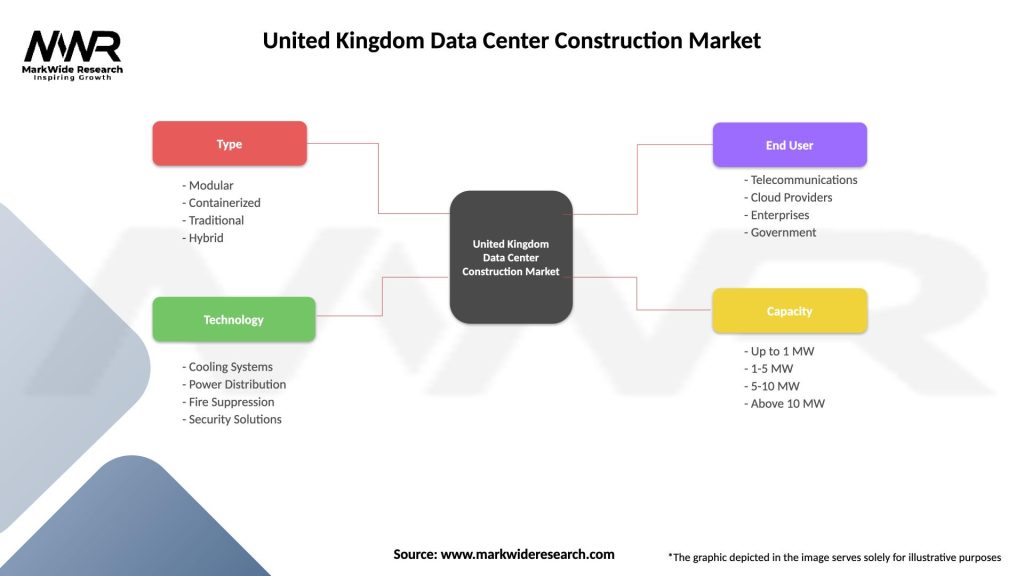

United Kingdom Data Center Construction Market

| Segmentation Details | Description |

|---|---|

| Type | Modular, Containerized, Traditional, Hybrid |

| Technology | Cooling Systems, Power Distribution, Fire Suppression, Security Solutions |

| End User | Telecommunications, Cloud Providers, Enterprises, Government |

| Capacity | Up to 1 MW, 1-5 MW, 5-10 MW, Above 10 MW |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the United Kingdom Data Center Construction Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.