444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The underground cabling EPC (Engineering, Procurement, and Construction) market is experiencing significant growth and is poised for further expansion in the coming years. This market primarily involves the installation, maintenance, and upgrading of underground cable systems for various applications such as power transmission, telecommunication networks, and transportation infrastructure. The demand for underground cabling EPC services has been fueled by the need for reliable and efficient energy transmission, the increasing adoption of smart grid technologies, and the rapid expansion of urbanization and industrialization.

Meaning

Underground cabling EPC refers to the comprehensive process of engineering, procuring, and constructing underground cable systems for different purposes. It involves designing and planning the cable routes, procuring the necessary materials and equipment, and executing the installation and commissioning of the underground cables. This approach offers numerous advantages over overhead power lines, including enhanced aesthetics, reduced environmental impact, and improved reliability in adverse weather conditions.

Executive Summary

The underground cabling EPC market has witnessed substantial growth in recent years due to several factors, such as the increasing demand for electricity, the need for efficient and reliable power transmission infrastructure, and the rise in renewable energy projects. This report provides a comprehensive analysis of the market, highlighting key trends, drivers, restraints, and opportunities. It also offers insights into the regional landscape, competitive dynamics, and future prospects of the underground cabling EPC market.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

The global underground cabling EPC market is projected to grow at a significant CAGR over the forecast period. The increasing demand for electricity, especially in emerging economies, is a major driver for the market. Governments worldwide are investing in infrastructure development, including underground cable systems, to support economic growth and ensure reliable power supply. The rising adoption of renewable energy sources, such as solar and wind, is creating additional opportunities for underground cabling EPC services. Technological advancements, such as the development of high-voltage direct current (HVDC) cables, are further driving market growth.

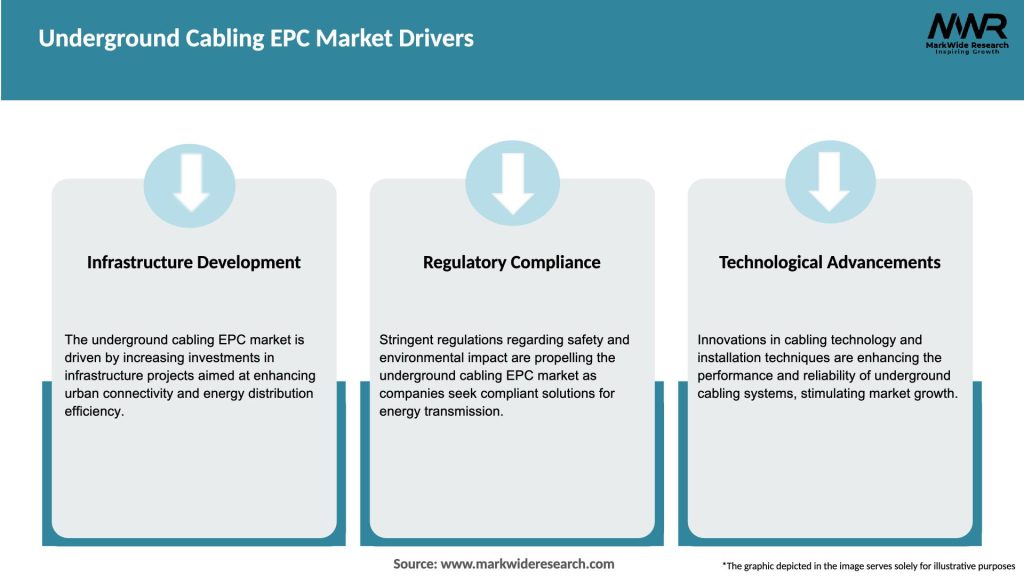

Market Drivers

The underground cabling EPC market is propelled by several key drivers:

Market Restraints

Despite the promising growth prospects, the underground cabling EPC market faces certain challenges:

Market Opportunities

The underground cabling EPC market presents several opportunities for growth and expansion:

Market Dynamics

The underground cabling EPC market operates in a dynamic environment influenced by various factors:

Regional Analysis

The underground cabling EPC market can be analyzed based on regional segments, including North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Competitive Landscape

Leading Companies in Underground Cabling EPC Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

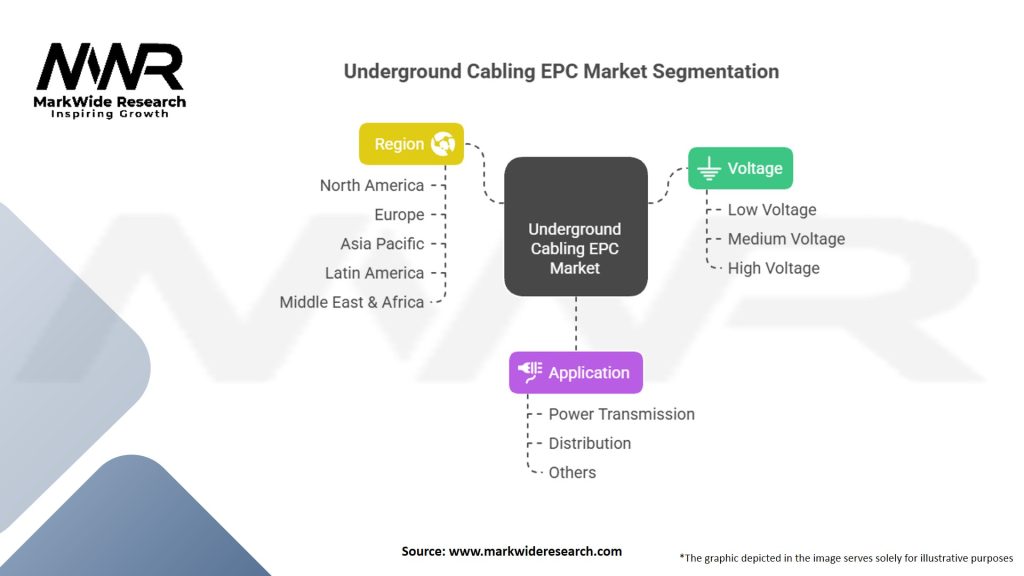

Segmentation

The underground cabling EPC market can be segmented based on various factors such as:

Accurate segmentation allows market players to identify specific customer needs and tailor their services accordingly.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

Industry participants and stakeholders in the underground cabling EPC market can benefit from:

SWOT Analysis

Market Key Trends

The underground cabling EPC market is influenced by several key trends:

Covid-19 Impact

The Covid-19 pandemic has had mixed effects on the underground cabling EPC market:

Key Industry Developments

Analyst Suggestions

Based on the analysis of the underground cabling EPC market, the following suggestions are made:

Future Outlook

The future of the underground cabling EPC market looks promising, with significant growth opportunities on the horizon. The increasing demand for reliable and efficient power transmission, the expansion of renewable energy projects, and the focus on infrastructure development are expected to drive the market. Technological advancements, collaboration among industry players, and favorable government policies will play crucial roles in shaping the future of the underground cabling EPC market.

Conclusion

The underground cabling EPC market is witnessing substantial growth and offers numerous opportunities for industry participants and stakeholders. With the increasing demand for reliable power transmission, the integration of renewable energy sources, and the emphasis on sustainable infrastructure, underground cabling EPC services are becoming indispensable. While challenges such as high installation costs and regulatory complexities exist, technological advancements, partnerships, and strategic investments will propel the market forward. The future outlook for the underground cabling EPC market is optimistic, driven by the need for efficient energy transmission, smart grid development, and infrastructure upgrades worldwide.

What is Underground Cabling EPC?

Underground Cabling EPC refers to the engineering, procurement, and construction services involved in the installation of underground cabling systems. These systems are essential for various applications, including power distribution, telecommunications, and data transmission.

Who are the key players in the Underground Cabling EPC Market?

Key players in the Underground Cabling EPC Market include companies like Siemens AG, Nexans, and Prysmian Group, which provide comprehensive solutions for underground cabling projects. These companies are known for their expertise in engineering and construction services, among others.

What are the main drivers of the Underground Cabling EPC Market?

The main drivers of the Underground Cabling EPC Market include the increasing demand for reliable power supply, the need for improved infrastructure in urban areas, and the growing focus on renewable energy projects. These factors contribute to the expansion of underground cabling installations.

What challenges does the Underground Cabling EPC Market face?

The Underground Cabling EPC Market faces challenges such as high installation costs, regulatory hurdles, and the complexity of underground construction. These factors can hinder project timelines and increase overall expenses.

What opportunities exist in the Underground Cabling EPC Market?

Opportunities in the Underground Cabling EPC Market include advancements in cable technology, the expansion of smart grid initiatives, and increased investments in renewable energy infrastructure. These trends are likely to drive future growth in the sector.

What trends are shaping the Underground Cabling EPC Market?

Trends shaping the Underground Cabling EPC Market include the adoption of sustainable practices, the integration of digital technologies for project management, and the growing preference for underground solutions to minimize environmental impact. These trends are influencing how projects are planned and executed.

Underground Cabling EPC Market

| Segmentation Details | Description |

|---|---|

| Voltage | Low Voltage, Medium Voltage, High Voltage |

| Application | Power Transmission, Distribution, Others |

| Region | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in Underground Cabling EPC Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA