The UK Islamic finance market has experienced significant growth and development over the years. Islamic finance refers to a financial system that operates in accordance with the principles of Shariah law, which prohibits the charging of interest and promotes ethical and responsible financial practices. The UK has emerged as one of the leading hubs for Islamic finance in the Western world, providing a range of Islamic financial products and services to both domestic and international customers.

Meaning

Islamic finance is a system of financial services that comply with the principles of Shariah law. It offers an alternative to conventional finance by promoting ethical and responsible financial practices. Islamic finance operates on the principles of fairness, transparency, and risk-sharing, and it prohibits the charging of interest (riba) and investment in activities that are considered unethical or harmful.

Executive Summary

The UK Islamic finance market has experienced steady growth in recent years, driven by increasing demand for Shariah-compliant financial products and services. The market has witnessed the emergence of Islamic banks, insurance companies, investment funds, and other financial institutions that cater to the needs of the Muslim population and those seeking ethical financial solutions. Despite facing challenges, such as regulatory constraints and lack of awareness, the UK Islamic finance market holds significant potential for further expansion and development.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Growing Muslim population: The UK has a substantial Muslim population, creating a strong demand for Shariah-compliant financial products and services.

Increasing awareness and acceptance: There has been a notable increase in awareness and acceptance of Islamic finance among both Muslims and non-Muslims in the UK.

Supportive regulatory framework: The UK government has taken initiatives to create a favorable regulatory environment for Islamic finance, attracting investments and promoting market growth.

Diverse range of financial products: The UK Islamic finance market offers a wide range of products, including Islamic mortgages, Islamic bonds (sukuk), Islamic insurance (takaful), and Islamic investment funds.

Global financial center: London, being a global financial center, provides a conducive environment for Islamic finance institutions to operate and expand their reach.

Market Drivers

Increasing demand for ethical finance: The growing awareness and consciousness regarding ethical finance among individuals and businesses have contributed to the demand for Shariah-compliant financial products.

Favorable regulatory environment: The UK government has introduced various regulatory reforms and initiatives to support the growth of Islamic finance, attracting domestic and international investors.

Infrastructure development: The development of Islamic finance infrastructure, including the establishment of Islamic banks, financial institutions, and regulatory bodies, has facilitated market growth.

Cross-border collaborations: The UK has formed partnerships with other countries, such as Malaysia and Gulf Cooperation Council (GCC) countries, to enhance cross-border Islamic finance activities and promote international investments.

Innovation and product diversification: Financial institutions in the UK Islamic finance market have introduced innovative products and services to cater to the evolving needs of customers, fostering market growth.

Market Restraints

Limited awareness and understanding: Despite the increasing awareness, many individuals and businesses still lack a thorough understanding of Islamic finance and its benefits, hindering market growth.

Regulatory challenges: Islamic finance faces certain regulatory constraints and challenges, such as tax treatment, accounting standards, and legal frameworks, which need to be addressed to further promote market growth.

Perception and misconceptions: Some individuals may have misconceptions or negative perceptions about Islamic finance, which may hinder their adoption of Shariah-compliant financial products.

Lack of standardized practices: There is a need for standardized practices and harmonization in Islamic finance to enhance transparency, consistency, and confidence among market participants.

Limited product offerings: The range of Shariah-compliant financial products and services available in the UK market is still relatively limited compared to conventional finance, limiting the options for customers.

Market Opportunities

Sustainable finance: Islamic finance principles align closely with sustainable finance, providing an opportunity for the UK Islamic finance market to contribute to environmental and social development.

Islamic fintech: The integration of technology and Islamic finance presents opportunities for the development of innovative fintech solutions catering to the needs of the Muslim population.

Green sukuk: The issuance of green sukuk, which are Islamic bonds dedicated to funding environmentally friendly projects, can attract investors interested in both ethical finance and sustainable investments.

Halal tourism and hospitality: The UK has the potential to develop Islamic finance products and services to cater to the needs of Muslim tourists, such as halal hotels and travel financing.

Islamic wealth management: The growing Muslim population and increasing wealth provide opportunities for the development of Islamic wealth management services, including Islamic private banking and asset management.

Market Dynamics

The UK Islamic finance market operates in a dynamic environment characterized by evolving customer preferences, regulatory changes, technological advancements, and global economic factors. The market is influenced by various stakeholders, including financial institutions, regulators, customers, and industry associations. Collaboration and partnerships between Islamic finance institutions, both domestically and internationally, play a crucial role in driving market growth and expanding the range of products and services.

Regional Analysis

The UK Islamic finance market is primarily concentrated in major cities such as London, Birmingham, and Manchester, which have significant Muslim populations and strong financial sectors. London, being a global financial center, attracts a large portion of Islamic finance activities, including Islamic banking, sukuk issuances, and Islamic asset management. Birmingham is known as the hub of Islamic finance in the UK, hosting several Islamic banks and institutions. Manchester also plays a significant role, particularly in Islamic insurance (takaful) and real estate investments.

Competitive Landscape

Leading Companies in the UK Islamic Finance Market:

Gatehouse Bank plc

Al Rayan Bank (Masraf Al Rayan)

Islamic Bank of Britain (IBB)

BLME Holdings plc

FAB UK (First Abu Dhabi Bank)

Bank ABC (Arab Banking Corporation)

Abu Dhabi Islamic Bank (ADIB)

Barwa Bank (Qatar International Islamic Bank Q.P.S.C.)

Qatar Islamic Bank (QIB)

QIB (UK) plc

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

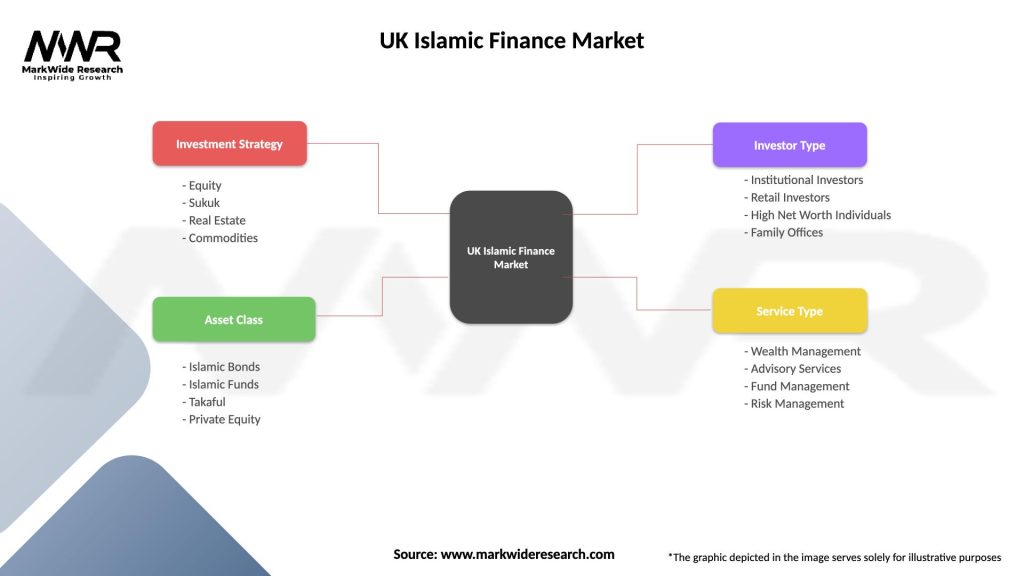

Segmentation

The UK Islamic finance market can be segmented based on various factors, including product type, customer segment, and geographic region. The product types include Islamic banking, Islamic insurance (takaful), Islamic bonds (sukuk), Islamic investment funds, and other financial services. Customer segments can be categorized into individuals, businesses, and institutional investors. Geographically, the market can be segmented based on regions within the UK, such as London, Birmingham, and Manchester.

Category-wise Insights

Islamic Banking: Islamic banks in the UK offer a range of services, including current accounts, savings accounts, home financing, and business financing. They operate based on the principles of profit-sharing (mudarabah) and joint-venture (musharakah), ensuring that the bank and the customer share both the risks and rewards of financial transactions.

Islamic Insurance (Takaful): Takaful companies provide Shariah-compliant insurance products, offering protection against various risks, such as life insurance, health insurance, and general insurance. Takaful operates on the principles of mutual cooperation and shared responsibility, with participants contributing to a common pool to cover potential losses.

Islamic Bonds (Sukuk): The UK has witnessed the issuance of sukuk, which are Shariah-compliant bonds, to finance infrastructure projects, corporate activities, and government financing needs. Sukuk represent ownership or partnership in an underlying asset and provide investors with a share of the income generated by the asset.

Islamic Investment Funds: Islamic investment funds offer individuals and institutional investors the opportunity to invest in a diversified portfolio of Shariah-compliant assets, such as equities, real estate, and commodities. These funds are managed in accordance with Islamic principles and follow strict ethical guidelines.

Other Financial Services: The UK Islamic finance market also offers other financial services, including trade finance, project finance, wealth management, and advisory services, catering to the diverse needs of customers seeking Shariah-compliant solutions.

Key Benefits for Industry Participants and Stakeholders

Access to ethical finance: Islamic finance provides industry participants and stakeholders with access to ethical and responsible financial solutions that align with their values and beliefs.

Diversification of product offerings: Islamic finance allows financial institutions to diversify their product portfolios and cater to a broader customer base, expanding their revenue streams.

Market growth and expansion opportunities: The UK Islamic finance market offers opportunities for industry participants to grow their businesses, tap into new customer segments, and expand their geographical presence.

Attracting socially conscious customers: Shariah-compliant financial products and services attract customers who prioritize ethical and responsible finance, providing a competitive advantage to industry participants.

Collaborative partnerships: The nature of Islamic finance encourages collaboration and partnerships among industry participants, fostering knowledge sharing, innovation, and market development.

SWOT Analysis

Strengths:

Growing Muslim population and demand for Shariah-compliant financial products.

Supportive regulatory environment and government initiatives.

Established financial infrastructure and global financial center status.

Collaboration opportunities with international Islamic finance markets.

Weaknesses:

Limited awareness and understanding of Islamic finance among the general population.

Regulatory challenges and lack of harmonization in practices.

Relatively limited product offerings compared to conventional finance.

Perception and misconceptions about Islamic finance.

Opportunities:

Integration of Islamic finance and sustainable finance.

Development of Islamic fintech solutions.

Issuance of green sukuk for sustainable investments.

Halal tourism and hospitality services.

Islamic wealth management services for a growing Muslim population.

Threats:

Regulatory constraints and legal challenges.

Competition from conventional finance institutions.

Economic and geopolitical factors impacting global financial markets.

Negative perceptions and misconceptions about Islamic finance.

Market Key Trends

Rise of sustainable and ethical finance: The demand for ethical and sustainable finance is increasing, leading to the integration of Islamic finance principles with sustainable finance initiatives.

Fintech innovations: The emergence of Islamic fintech startups and the adoption of technology by existing Islamic finance institutions are driving innovation in the market, enhancing customer experience and product offerings.

Increased cross-border collaborations: The UK Islamic finance market is engaging in partnerships with other countries, particularly in the Middle East and Asia, to facilitate cross-border investments, knowledge sharing, and market development.

Growth in Islamic wealth management: With a growing Muslim population and increasing wealth, there is a rising demand for Islamic wealth management services, including private banking, asset management, and estate planning.

Expansion of Islamic capital markets: The issuance of sukuk and the development of Islamic capital market infrastructure are promoting the growth and liquidity of the Islamic capital market in the UK.

Covid-19 Impact

The COVID-19 pandemic has had a significant impact on the UK Islamic finance market, as it has on the global financial industry. The pandemic resulted in economic uncertainties and disruptions, affecting customer behavior and investment decisions. However, the crisis also highlighted the resilience of Islamic finance principles, as they emphasize risk-sharing and ethical financial practices. The pandemic has accelerated the adoption of digital technologies in Islamic finance, facilitating remote operations, customer service, and digital onboarding. The UK government implemented various support measures to mitigate the impact of the pandemic on businesses, including Islamic finance institutions.

Key Industry Developments

Regulatory reforms and initiatives: The UK government has introduced regulatory reforms to support the growth of Islamic finance, including tax and legal frameworks that promote Shariah-compliant finance. The establishment of regulatory bodies, such as the Islamic Finance Council UK (UKIFC), has also contributed to market development.

Collaboration with international markets: The UK has strengthened its ties with other Islamic finance markets, such as Malaysia and the GCC countries, through collaborations, partnerships, and knowledge-sharing initiatives. These collaborations have facilitated cross-border investments and the development of best practices.

Innovation and technology adoption: Islamic finance institutions in the UK are increasingly adopting technology and partnering with fintech startups to enhance customer experience, improve operational efficiency, and develop innovative financial solutions.

Sukuk issuances and Islamic capital market growth: The UK has witnessed significant sukuk issuances, attracting both domestic and international investors. The development of the Islamic capital market infrastructure, including secondary market trading platforms, has contributed to market liquidity and growth.

Awareness and education initiatives: Various organizations, including industry associations, educational institutions, and think tanks, are actively promoting awareness and education about Islamic finance, targeting both Muslims and non-Muslims.

Analyst Suggestions

Enhance awareness and education: Continued efforts are required to raise awareness and educate the general population about Islamic finance, its principles, and the benefits it offers. This can be achieved through targeted marketing campaigns, collaborations with educational institutions, and community outreach programs.

Address regulatory challenges: The UK government should work closely with industry stakeholders to address regulatory challenges and create a more harmonized and supportive regulatory framework for Islamic finance. This includes tax treatment, accounting standards, and legal frameworks that align with Shariah principles.

Encourage innovation and fintech integration: Islamic finance institutions should embrace technology and collaborate with fintech startups to develop innovative solutions that enhance customer experience, improve operational efficiency, and expand product offerings.

Strengthen international collaborations: The UK should continue to strengthen its collaborations with international Islamic finance markets, facilitating cross-border investments, knowledge sharing, and market development. This includes partnerships with countries in the Middle East, Asia, and Africa.

Promote sustainable finance initiatives: Islamic finance institutions should actively participate in sustainable finance initiatives and explore opportunities to integrate Islamic finance principles with environmental, social, and governance (ESG) considerations.

Future Outlook

The future outlook for the UK Islamic finance market appears positive, with opportunities for growth and development. The market is expected to witness increased adoption of Islamic finance products and services by both Muslims and non-Muslims, driven by ethical considerations and the demand for responsible finance. The integration of Islamic finance with sustainable finance is expected to gain further traction, contributing to environmental and social development. The development of innovative fintech solutions, the expansion of Islamic wealth management services, and the issuance of green sukuk are expected to shape the future landscape of the UK Islamic finance market.

Conclusion

The UK Islamic finance market has made significant progress in recent years, driven by increasing awareness and demand for Shariah-compliant financial products and services. The market has witnessed the emergence of Islamic banks, insurance companies, investment funds, and other financial institutions, offering a diverse range of Islamic finance solutions. Despite challenges, such as regulatory constraints and limited awareness, the market holds considerable potential for growth and development. Collaborations, innovation, and sustainable finance initiatives are expected to shape the future of the UK Islamic finance market, providing opportunities for industry participants, investors, and stakeholders.

What is Islamic Finance?

Islamic Finance refers to financial activities that comply with Islamic law (Sharia). It encompasses various products and services, including banking, investment, and insurance, that adhere to principles such as risk-sharing and the prohibition of interest (riba).

What are the key players in the UK Islamic Finance Market?

The UK Islamic Finance Market features several prominent players, including Al Baraka Banking Group, Abu Dhabi Islamic Bank, and Qatar Islamic Bank. These institutions offer a range of Sharia-compliant financial products and services, catering to both individual and corporate clients, among others.

What are the growth factors driving the UK Islamic Finance Market?

The UK Islamic Finance Market is driven by increasing demand for ethical investment options, a growing Muslim population, and the expansion of Sharia-compliant financial products. Additionally, favorable regulatory frameworks and government support contribute to market growth.

What challenges does the UK Islamic Finance Market face?

The UK Islamic Finance Market faces challenges such as a lack of awareness among potential customers, limited product offerings compared to conventional finance, and regulatory hurdles. These factors can hinder the growth and acceptance of Islamic finance solutions.

What opportunities exist in the UK Islamic Finance Market?

The UK Islamic Finance Market presents opportunities for innovation in product development, particularly in areas like fintech and sustainable finance. There is also potential for collaboration between Islamic finance institutions and conventional banks to expand service offerings.

What trends are shaping the UK Islamic Finance Market?

Trends in the UK Islamic Finance Market include the rise of digital banking solutions, increased focus on sustainability and ethical investing, and the integration of technology in financial services. These trends are reshaping how Islamic finance products are developed and delivered.

Leading Companies in the UK Islamic Finance Market:

Gatehouse Bank plc

Al Rayan Bank (Masraf Al Rayan)

Islamic Bank of Britain (IBB)

BLME Holdings plc

FAB UK (First Abu Dhabi Bank)

Bank ABC (Arab Banking Corporation)

Abu Dhabi Islamic Bank (ADIB)

Barwa Bank (Qatar International Islamic Bank Q.P.S.C.)

Qatar Islamic Bank (QIB)

QIB (UK) plc

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.