444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Based Banking Market")

Market Overview: The UK Intelligent Virtual Assistant (IVA) Based Banking Market represents a transformative segment within the financial services industry, leveraging artificial intelligence and virtual assistant technologies to enhance customer interactions, streamline processes, and provide personalized banking experiences.

Meaning: Intelligent Virtual Assistants (IVAs) in banking refer to AI-driven digital assistants designed to interact with customers, answer queries, perform tasks, and offer personalized financial advice. These virtual assistants use natural language processing and machine learning algorithms to understand user inputs and provide relevant information.

Executive Summary: The executive summary of the UK IVA-Based Banking Market highlights the industry’s rapid evolution, emphasizing the adoption of IVAs by banks to improve customer engagement, reduce operational costs, and stay competitive in the digital era. Key trends, technological advancements, and competitive dynamics shape the market landscape.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights:

Market Drivers:

Market Restraints:

Market Opportunities:

Market Dynamics: The UK IVA-Based Banking Market operates in a dynamic environment influenced by technological advancements, changing customer expectations, regulatory frameworks, and competitive strategies. Understanding these dynamics is essential for banks to navigate the evolving landscape and harness the benefits of IVAs.

Regional Analysis: Regional variations in consumer behavior, technological infrastructure, and regulatory landscapes impact the adoption of IVAs in banking. A comprehensive regional analysis helps banks tailor their IVA strategies to meet the unique needs of customers in different regions of the UK.

Competitive Landscape:

Leading Companies in UK Intelligent Virtual Assistant (IVA) Based Banking Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

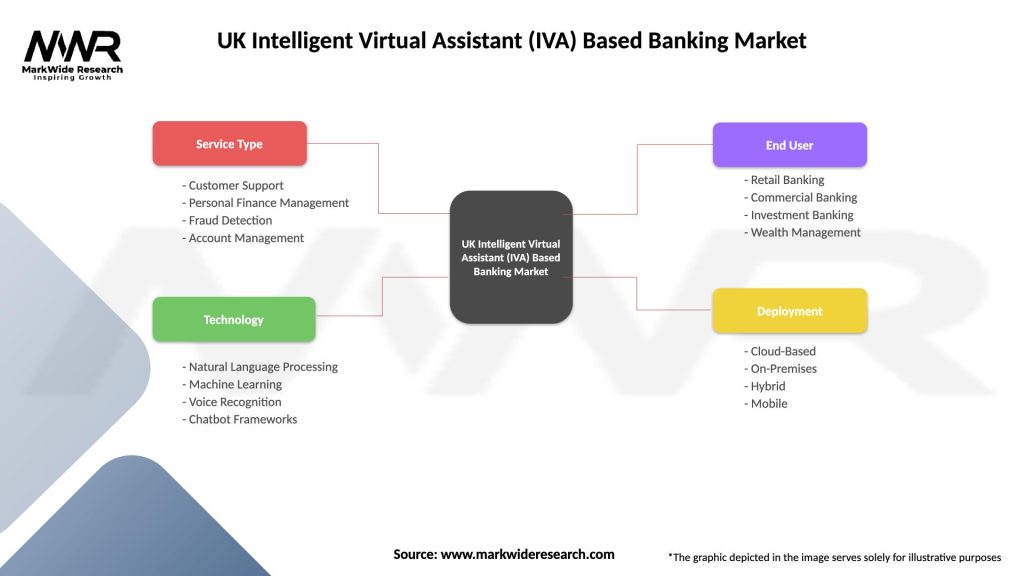

Segmentation: The UK IVA-Based Banking Market can be segmented based on various factors, including:

Category-wise Insights:

Key Benefits for Industry Participants and Stakeholders:

SWOT Analysis: A SWOT analysis provides an overview of the strengths, weaknesses, opportunities, and threats in the UK IVA-Based Banking Market:

Market Key Trends:

Covid-19 Impact: The Covid-19 pandemic accelerated the adoption of digital technologies, including IVAs, in the banking sector. Banks relied on IVAs to maintain customer services during lockdowns, handle increased call volumes, and provide assistance for pandemic-related financial queries.

Key Industry Developments:

Analyst Suggestions:

Future Outlook: The future outlook for the UK IVA-Based Banking Market is optimistic, with continued advancements in AI technologies, the proliferation of voice-activated devices, and a growing acceptance of digital banking. The market is poised for further innovation, with AI-driven virtual assistants becoming integral to the overall banking experience.

Conclusion: The UK Intelligent Virtual Assistant (IVA) Based Banking Market represents a pivotal shift in the way customers interact with financial institutions. As AI technologies continue to evolve, IVAs will play a central role in delivering personalized, efficient, and accessible banking services. Banks that embrace these technological advancements, address challenges effectively, and prioritize customer trust are well-positioned for sustained success in the dynamic landscape of digital banking.

What is Intelligent Virtual Assistant (IVA) Based Banking?

Intelligent Virtual Assistant (IVA) Based Banking refers to the use of AI-driven virtual assistants in the banking sector to enhance customer service, streamline operations, and provide personalized financial advice. These systems can handle inquiries, process transactions, and assist with account management, improving overall customer experience.

What are the key players in the UK Intelligent Virtual Assistant (IVA) Based Banking Market?

Key players in the UK Intelligent Virtual Assistant (IVA) Based Banking Market include banks and technology firms such as HSBC, Barclays, and Nuance Communications. These companies are leveraging AI technologies to develop innovative solutions for customer engagement and operational efficiency, among others.

What are the growth factors driving the UK Intelligent Virtual Assistant (IVA) Based Banking Market?

The growth of the UK Intelligent Virtual Assistant (IVA) Based Banking Market is driven by increasing demand for enhanced customer service, the need for operational efficiency, and the rise of digital banking. Additionally, advancements in AI technology and consumer preferences for personalized banking experiences are significant contributors.

What challenges does the UK Intelligent Virtual Assistant (IVA) Based Banking Market face?

Challenges in the UK Intelligent Virtual Assistant (IVA) Based Banking Market include concerns over data privacy and security, the need for regulatory compliance, and the potential for technology adoption resistance among customers. These factors can hinder the effective implementation of IVA solutions.

What opportunities exist in the UK Intelligent Virtual Assistant (IVA) Based Banking Market?

Opportunities in the UK Intelligent Virtual Assistant (IVA) Based Banking Market include the potential for expanding services to underserved demographics, integrating advanced analytics for better customer insights, and enhancing cross-channel customer interactions. These developments can lead to improved customer loyalty and satisfaction.

What trends are shaping the UK Intelligent Virtual Assistant (IVA) Based Banking Market?

Trends shaping the UK Intelligent Virtual Assistant (IVA) Based Banking Market include the increasing use of natural language processing for better user interaction, the integration of IVAs with mobile banking applications, and the growing focus on omnichannel customer experiences. These trends are driving innovation and competition in the sector.

UK Intelligent Virtual Assistant (IVA) Based Banking Market

| Segmentation Details | Description |

|---|---|

| Service Type | Customer Support, Personal Finance Management, Fraud Detection, Account Management |

| Technology | Natural Language Processing, Machine Learning, Voice Recognition, Chatbot Frameworks |

| End User | Retail Banking, Commercial Banking, Investment Banking, Wealth Management |

| Deployment | Cloud-Based, On-Premises, Hybrid, Mobile |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in UK Intelligent Virtual Assistant (IVA) Based Banking Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.