444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The UAE plastic packaging films market represents a dynamic and rapidly evolving sector within the broader packaging industry, driven by the country’s strategic position as a regional hub for trade and commerce. Plastic packaging films have become essential components across diverse industries including food and beverage, pharmaceuticals, consumer goods, and industrial applications throughout the United Arab Emirates. The market demonstrates robust growth momentum with increasing demand for flexible packaging solutions that offer superior barrier properties, cost-effectiveness, and sustainability features.

Market dynamics in the UAE are significantly influenced by the country’s growing population, rising disposable income, and expanding retail sector. The region’s commitment to economic diversification away from oil dependency has fostered substantial growth in manufacturing and consumer goods sectors, directly impacting demand for advanced packaging solutions. Additionally, the UAE’s position as a major re-export hub for the Middle East and Africa regions creates substantial opportunities for packaging film manufacturers and suppliers.

Growth projections indicate the market is expanding at a compound annual growth rate of 6.2%, reflecting strong underlying demand drivers and favorable economic conditions. The increasing adoption of sustainable packaging materials and advanced barrier technologies continues to shape market evolution, with manufacturers investing heavily in research and development to meet changing consumer preferences and regulatory requirements.

The UAE plastic packaging films market refers to the comprehensive ecosystem encompassing the production, distribution, and consumption of thin plastic materials used for packaging applications across various industries within the United Arab Emirates. Plastic packaging films are flexible, lightweight materials manufactured from various polymer resins including polyethylene, polypropylene, polyester, and specialty compounds designed to protect, preserve, and present products effectively.

These films serve multiple critical functions including moisture barrier protection, oxygen resistance, UV protection, and mechanical strength enhancement. The market encompasses various film types such as shrink films, stretch films, barrier films, and specialty films designed for specific applications. Manufacturing processes include blown film extrusion, cast film extrusion, and co-extrusion techniques that enable the production of mono-layer and multi-layer film structures with tailored properties.

Market participants include raw material suppliers, film manufacturers, converters, distributors, and end-users across industries such as food processing, pharmaceuticals, electronics, and consumer goods. The ecosystem also encompasses recycling and waste management companies focused on circular economy initiatives and sustainable packaging solutions.

The UAE plastic packaging films market demonstrates exceptional resilience and growth potential, supported by favorable demographic trends, economic diversification initiatives, and increasing consumer demand for convenient packaging solutions. Key market drivers include rapid urbanization, expanding e-commerce sector, and growing food processing industry, which collectively account for approximately 72% of total market demand.

Technological advancement remains a critical success factor, with manufacturers increasingly adopting advanced extrusion technologies, multi-layer film structures, and sustainable material formulations. The market benefits from the UAE’s strategic geographic location, world-class infrastructure, and business-friendly regulatory environment that attracts international investment and facilitates trade relationships across the region.

Sustainability initiatives are reshaping market dynamics, with increasing emphasis on recyclable materials, biodegradable alternatives, and circular economy principles. Government policies supporting environmental protection and waste reduction are driving innovation in eco-friendly packaging solutions, creating new opportunities for market participants focused on sustainable product development.

Competitive landscape features a mix of international corporations and regional players, with market consolidation trends evident as companies seek to achieve economies of scale and expand their technological capabilities. Strategic partnerships, mergers and acquisitions, and capacity expansion investments continue to shape the market structure and competitive dynamics.

Market segmentation analysis reveals distinct growth patterns across different application sectors and film types. The following key insights highlight critical market characteristics:

Population growth and urbanization serve as fundamental drivers for the UAE plastic packaging films market, with the country’s population expanding steadily and urban centers experiencing rapid development. Rising disposable income levels enable increased consumption of packaged goods, directly translating to higher demand for packaging films across various product categories.

The expanding food processing industry represents a major growth driver, with increasing investment in food manufacturing facilities and cold chain infrastructure. Consumer lifestyle changes toward convenience foods, ready-to-eat meals, and packaged beverages create substantial opportunities for flexible packaging solutions that offer superior preservation properties and attractive presentation.

E-commerce sector growth significantly impacts market demand, with online retail expansion requiring specialized packaging films for product protection during shipping and handling. Government initiatives supporting economic diversification and manufacturing sector development create favorable conditions for packaging industry growth and investment attraction.

Tourism industry expansion drives demand for packaged goods and hospitality-related packaging applications. The UAE’s position as a major tourist destination creates substantial market opportunities for premium packaging solutions serving hotels, restaurants, and retail establishments catering to international visitors.

Environmental concerns regarding plastic waste and marine pollution create significant challenges for the packaging films market, with increasing regulatory pressure and consumer resistance to single-use plastic products. Raw material price volatility affects manufacturing costs and profit margins, particularly given the dependence on petroleum-based polymer resins subject to global commodity price fluctuations.

Regulatory compliance requirements continue to evolve, with stricter standards for food contact materials, migration limits, and recyclability specifications creating additional costs and complexity for manufacturers. Competition from alternative packaging materials such as paper-based solutions, biodegradable materials, and reusable packaging systems poses ongoing challenges to market growth.

Supply chain disruptions and logistics challenges can impact raw material availability and product distribution, particularly given the global nature of polymer resin supply chains. Skilled labor shortages in specialized manufacturing and technical roles may constrain production capacity expansion and technology adoption initiatives.

Economic uncertainty and geopolitical factors affecting regional trade relationships can impact market demand and investment decisions. Technology transition costs associated with upgrading equipment and processes to meet sustainability requirements represent significant capital investment challenges for market participants.

Sustainable packaging innovation presents substantial opportunities for companies developing biodegradable films, recyclable materials, and circular economy solutions. Advanced barrier technologies offer potential for premium market positioning through enhanced product protection and extended shelf life capabilities.

Smart packaging integration creates opportunities for value-added solutions incorporating sensors, indicators, and digital connectivity features. Pharmaceutical packaging growth driven by healthcare sector expansion and aging population demographics offers attractive market segments with higher margins and specialized requirements.

Export market development leveraging the UAE’s strategic location and trade relationships provides opportunities for regional market expansion and economies of scale. Industrial packaging applications in growing manufacturing sectors including electronics, automotive, and construction materials create new demand streams.

Customization and specialty films development for niche applications enables differentiation and premium pricing strategies. Recycling infrastructure development creates opportunities for companies investing in waste management and circular economy initiatives, potentially supported by government incentives and regulatory frameworks.

Supply chain integration continues to evolve as market participants seek vertical integration opportunities and strategic partnerships to enhance operational efficiency and market positioning. Technology adoption rates accelerate as manufacturers invest in advanced extrusion equipment, quality control systems, and automation technologies to improve productivity and product quality.

Consumer behavior shifts toward sustainability and environmental responsibility influence product development priorities and marketing strategies across the industry. Regulatory landscape evolution requires continuous adaptation and compliance investment, with increasing focus on extended producer responsibility and waste reduction initiatives.

Competitive intensity drives innovation and operational efficiency improvements, with market participants investing in research and development to maintain technological leadership and market share. Raw material sourcing strategies become increasingly important as companies seek supply security and cost optimization through diversified supplier relationships and alternative material exploration.

Market consolidation trends reflect economies of scale requirements and technology investment needs, with larger players acquiring specialized companies and regional manufacturers. Investment patterns show increasing focus on sustainability-oriented projects and advanced manufacturing capabilities that support long-term market positioning.

Primary research methodology encompasses comprehensive interviews with industry executives, manufacturers, distributors, and end-users across the UAE plastic packaging films value chain. Data collection processes include structured surveys, in-depth interviews, and focus group discussions with key stakeholders to gather quantitative and qualitative insights regarding market trends, challenges, and opportunities.

Secondary research sources include government publications, industry association reports, trade publications, and company financial statements to validate primary research findings and provide comprehensive market context. Market sizing methodologies employ bottom-up and top-down approaches, incorporating production data, import-export statistics, and consumption patterns across different application segments.

Analytical frameworks utilize statistical modeling, trend analysis, and scenario planning to project market evolution and identify key success factors. Quality assurance processes include data triangulation, expert validation, and cross-referencing multiple sources to ensure accuracy and reliability of research findings.

Geographic scope covers all seven emirates within the UAE, with particular focus on major industrial and commercial centers including Dubai, Abu Dhabi, and Sharjah. Temporal analysis examines historical trends, current market conditions, and future projections to provide comprehensive market intelligence for strategic decision-making.

Dubai emerges as the dominant regional market, accounting for approximately 42% of total market demand driven by its position as a major commercial hub, extensive retail sector, and significant re-export activities. Abu Dhabi represents the second-largest market segment with 28% market share, supported by substantial government sector demand, growing industrial base, and major food processing facilities.

Sharjah’s industrial focus contributes 15% of market demand, with significant manufacturing activities and logistics operations driving packaging film consumption. Northern Emirates collectively account for the remaining 15% market share, with growing industrial development and agricultural activities creating steady demand for packaging solutions.

Regional infrastructure development varies significantly, with Dubai and Abu Dhabi featuring world-class logistics facilities and advanced manufacturing capabilities. Supply chain efficiency benefits from excellent transportation networks, modern ports, and strategic geographic positioning facilitating regional distribution activities.

Market concentration patterns reflect economic activity distribution, with major consumption centers aligned with population density and industrial development. Growth potential remains strong across all regions, supported by ongoing infrastructure investment and economic diversification initiatives throughout the UAE.

Market leadership is distributed among several key players, each bringing distinct competitive advantages and market positioning strategies. The competitive environment features both international corporations and regional specialists:

Competitive strategies emphasize technological innovation, sustainability initiatives, and customer service excellence. Market differentiation occurs through specialized product offerings, technical support capabilities, and supply chain reliability.

By Material Type:

By Application:

By Technology:

Food packaging films demonstrate the strongest growth momentum, with increasing demand for barrier properties and extended shelf life capabilities. Consumer preferences for convenience foods and ready-to-eat meals drive innovation in packaging design and functionality. Regulatory compliance requirements for food contact materials necessitate continuous investment in quality assurance and testing capabilities.

Industrial packaging applications benefit from expanding manufacturing activities and growing export-oriented industries. Performance requirements focus on mechanical strength, puncture resistance, and environmental protection capabilities. Cost optimization remains critical as industrial users seek packaging solutions that balance performance with economic efficiency.

Pharmaceutical packaging represents a high-value segment with stringent quality requirements and specialized barrier properties. Market growth is driven by healthcare sector expansion and increasing pharmaceutical manufacturing activities. Innovation opportunities exist in smart packaging technologies and tamper-evident solutions.

Specialty films for niche applications offer premium pricing opportunities and differentiation potential. Technical expertise requirements create barriers to entry and enable sustainable competitive advantages for specialized manufacturers.

Manufacturers benefit from growing market demand, technological advancement opportunities, and favorable business environment in the UAE. Operational advantages include access to skilled workforce, modern infrastructure, and strategic geographic location facilitating regional market access.

Distributors and suppliers gain from expanding customer base, diverse application segments, and growing re-export opportunities. Supply chain efficiency benefits from excellent logistics infrastructure and streamlined customs procedures.

End-users across industries benefit from improved product availability, competitive pricing, and access to advanced packaging technologies. Quality improvements in packaging films enhance product protection, shelf life extension, and consumer appeal.

Government stakeholders benefit from industrial development, employment creation, and economic diversification objectives. Environmental benefits emerge from increasing adoption of sustainable packaging solutions and circular economy initiatives.

Investors and financial institutions find attractive opportunities in a growing market with strong fundamentals and government support for industrial development. Risk mitigation benefits from market diversification and stable regulatory environment.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability transformation represents the most significant trend reshaping the UAE plastic packaging films market, with manufacturers investing heavily in recyclable materials and biodegradable alternatives. Circular economy principles gain traction as companies develop closed-loop systems and waste reduction strategies.

Smart packaging integration emerges as a key differentiator, with advanced films incorporating sensors, indicators, and digital connectivity features. Consumer engagement through interactive packaging experiences creates new value propositions and brand differentiation opportunities.

E-commerce packaging optimization drives demand for specialized films designed for online retail applications, emphasizing product protection and unboxing experience enhancement. Automation adoption in packaging operations increases demand for films compatible with high-speed machinery and automated systems.

Customization and personalization trends create opportunities for short-run production and specialized film properties tailored to specific applications. Supply chain localization initiatives aim to reduce dependence on imports and enhance supply security through regional manufacturing development.

Recent capacity expansions by major manufacturers demonstrate confidence in market growth potential and commitment to serving regional demand. Technology partnerships between international companies and local manufacturers facilitate knowledge transfer and capability development.

Sustainability initiatives include significant investments in recycling infrastructure and development of biodegradable film alternatives. Government policy developments support circular economy objectives and environmental protection through regulatory frameworks and incentive programs.

Strategic acquisitions and joint ventures reshape competitive landscape as companies seek to expand technological capabilities and market reach. Research and development investments focus on advanced barrier technologies, sustainable materials, and smart packaging solutions.

Infrastructure development projects enhance manufacturing capabilities and logistics efficiency throughout the UAE. Export market development initiatives leverage the country’s strategic location to serve broader regional markets and create economies of scale.

MarkWide Research recommends that market participants prioritize sustainability initiatives and circular economy solutions to address evolving regulatory requirements and consumer preferences. Investment strategies should focus on advanced manufacturing technologies that enable production of high-performance, environmentally responsible packaging films.

Strategic partnerships with technology providers and research institutions can accelerate innovation and market development initiatives. Market diversification across application segments and geographic regions reduces risk and creates multiple growth opportunities.

Supply chain optimization through vertical integration or strategic supplier relationships enhances operational efficiency and cost competitiveness. Talent development programs addressing skilled labor shortages support long-term growth and technological advancement objectives.

Customer relationship management focusing on technical support and customized solutions creates competitive advantages and customer loyalty. Regulatory compliance investment ensures market access and reduces operational risks associated with evolving standards.

Market growth prospects remain robust with projected expansion at 6.2% CAGR through the forecast period, driven by favorable demographic trends and economic diversification initiatives. Sustainability transformation will continue reshaping market dynamics, with increasing market share for eco-friendly packaging solutions reaching an estimated 35% by 2028.

Technology evolution toward smart packaging and advanced barrier films creates opportunities for premium market positioning and value creation. Regional market expansion leveraging UAE’s strategic advantages offers significant growth potential beyond domestic demand.

Investment requirements for technology advancement and sustainability initiatives will drive market consolidation and strategic partnerships. Regulatory evolution supporting circular economy objectives will create both challenges and opportunities for market participants.

MWR analysis indicates that companies investing in sustainable technologies and regional market development will achieve superior long-term performance and market positioning. Innovation leadership in biodegradable materials and smart packaging technologies will become increasingly important for competitive success.

The UAE plastic packaging films market presents compelling opportunities for growth and innovation, supported by strong economic fundamentals, strategic geographic advantages, and favorable business environment. Market dynamics reflect the country’s successful economic diversification efforts and growing consumer market sophistication.

Sustainability imperatives will continue driving market transformation, creating opportunities for companies that successfully balance environmental responsibility with operational efficiency. Technology advancement remains critical for maintaining competitive positioning and meeting evolving customer requirements across diverse application segments.

Strategic success factors include investment in advanced manufacturing capabilities, development of sustainable product portfolios, and cultivation of strong customer relationships. Market participants that effectively navigate regulatory evolution and consumer preference shifts will capture disproportionate value creation opportunities in this dynamic and growing market.

What is Plastic Packaging Films?

Plastic packaging films are thin layers of plastic used for wrapping and protecting products. They are commonly utilized in various applications such as food packaging, medical supplies, and consumer goods.

What are the key players in the UAE Plastic Packaging Films Market?

Key players in the UAE Plastic Packaging Films Market include companies like Al Bayader International, Gulf Plastic Industries, and National Plastic Factory, among others.

What are the main drivers of the UAE Plastic Packaging Films Market?

The main drivers of the UAE Plastic Packaging Films Market include the growing demand for packaged food products, the rise in e-commerce, and the increasing focus on convenience in consumer lifestyles.

What challenges does the UAE Plastic Packaging Films Market face?

The UAE Plastic Packaging Films Market faces challenges such as environmental concerns regarding plastic waste, regulatory pressures for sustainable packaging solutions, and competition from alternative materials.

What opportunities exist in the UAE Plastic Packaging Films Market?

Opportunities in the UAE Plastic Packaging Films Market include the development of biodegradable films, innovations in recycling technologies, and the expansion of the food and beverage sector.

What trends are shaping the UAE Plastic Packaging Films Market?

Trends shaping the UAE Plastic Packaging Films Market include the increasing adoption of smart packaging technologies, the shift towards sustainable materials, and the growing demand for customized packaging solutions.

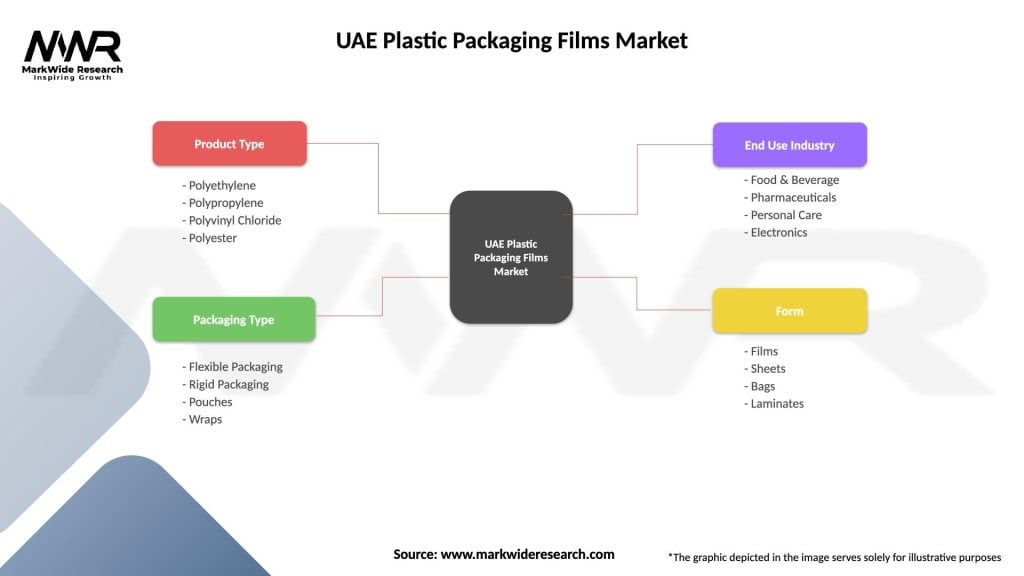

UAE Plastic Packaging Films Market

| Segmentation Details | Description |

|---|---|

| Product Type | Polyethylene, Polypropylene, Polyvinyl Chloride, Polyester |

| Packaging Type | Flexible Packaging, Rigid Packaging, Pouches, Wraps |

| End Use Industry | Food & Beverage, Pharmaceuticals, Personal Care, Electronics |

| Form | Films, Sheets, Bags, Laminates |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the UAE Plastic Packaging Films Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.