444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The UAE facility management market represents a rapidly expanding sector driven by the nation’s ambitious infrastructure development and growing emphasis on operational efficiency. Facility management services in the UAE encompass comprehensive building maintenance, security, cleaning, landscaping, and technical support across commercial, residential, and industrial properties. The market demonstrates robust growth potential, with industry analysts projecting a compound annual growth rate of 8.2% through the forecast period.

Dubai and Abu Dhabi serve as primary growth engines, hosting numerous multinational corporations, luxury hotels, shopping centers, and residential complexes requiring sophisticated facility management solutions. The market benefits from the UAE’s strategic position as a regional business hub, attracting international investments and driving demand for world-class facility management services. Smart building technologies and sustainable practices are increasingly integrated into facility management operations, reflecting the UAE’s commitment to innovation and environmental responsibility.

Government initiatives supporting infrastructure development, including the UAE Vision 2071 and Dubai Plan 2021, continue to fuel market expansion. The hospitality sector, representing approximately 25% of facility management demand, drives significant growth as the UAE positions itself as a global tourism destination. Commercial real estate development and the emergence of free zones further contribute to market dynamism, creating opportunities for both local and international facility management providers.

The UAE facility management market refers to the comprehensive ecosystem of services and solutions designed to ensure optimal functionality, safety, and efficiency of built environments across the United Arab Emirates. This market encompasses integrated management of physical assets, infrastructure, and support services for commercial buildings, residential complexes, industrial facilities, healthcare institutions, educational establishments, and hospitality venues.

Facility management services include maintenance and repair operations, security systems management, cleaning and housekeeping, landscaping and grounds maintenance, energy management, space planning, and technology support. The market integrates traditional maintenance approaches with advanced technologies such as Internet of Things sensors, predictive analytics, and automated building management systems to deliver enhanced operational efficiency and cost optimization.

Service providers in this market range from multinational corporations offering comprehensive facility management solutions to specialized local companies focusing on specific service segments. The market serves diverse client segments including government entities, multinational corporations, real estate developers, healthcare providers, educational institutions, and hospitality operators seeking to optimize their operational performance while focusing on core business activities.

Market dynamics in the UAE facility management sector reflect strong growth momentum driven by rapid urbanization, infrastructure expansion, and increasing adoption of outsourcing strategies. The market demonstrates resilience and adaptability, with service providers increasingly incorporating digital technologies and sustainable practices to meet evolving client expectations. Integrated facility management solutions are gaining prominence as organizations seek comprehensive service partnerships rather than fragmented vendor relationships.

Key growth drivers include the UAE’s position as a regional business hub, ongoing mega-projects such as Expo 2020 legacy developments, and the government’s focus on economic diversification. The market benefits from approximately 15% annual growth in commercial real estate development and expanding hospitality infrastructure. Sustainability initiatives are becoming increasingly important, with green building certifications driving demand for environmentally conscious facility management practices.

Competitive landscape features a mix of international facility management giants and regional specialists, creating a dynamic environment that fosters innovation and service excellence. The market shows strong potential for consolidation as smaller players seek partnerships with larger organizations to compete for comprehensive service contracts. Technology adoption rates are accelerating, with smart building solutions and predictive maintenance becoming standard offerings rather than premium services.

Strategic insights reveal several critical factors shaping the UAE facility management market landscape. The following key insights provide comprehensive understanding of market dynamics and growth opportunities:

Infrastructure development serves as the primary catalyst for UAE facility management market expansion. The nation’s ambitious construction projects, including smart cities, transportation hubs, and commercial complexes, create substantial demand for comprehensive facility management services. Government initiatives supporting economic diversification and tourism development drive continuous infrastructure investment, generating long-term facility management opportunities.

Outsourcing trends among UAE organizations reflect growing recognition of facility management as a strategic business function rather than a cost center. Companies increasingly focus on core competencies while partnering with specialized facility management providers to optimize operational efficiency. This trend is particularly pronounced in the financial services sector, where approximately 70% of organizations have adopted comprehensive facility management outsourcing strategies.

Regulatory requirements and international standards compliance drive demand for professional facility management services. UAE building codes, fire safety regulations, and environmental standards require specialized expertise and continuous monitoring. Quality certifications such as ISO 14001 and LEED compliance are becoming mandatory for many commercial properties, necessitating professional facility management support.

Technology advancement enables facility management providers to offer enhanced service value through predictive maintenance, energy optimization, and real-time monitoring capabilities. The integration of artificial intelligence and machine learning in building management systems creates opportunities for proactive facility management approaches that reduce downtime and operational costs.

Skilled workforce shortage represents a significant challenge for UAE facility management market growth. The industry requires technicians, engineers, and managers with specialized knowledge of building systems, safety protocols, and emerging technologies. Training and certification requirements create barriers for market entry and limit the availability of qualified personnel, particularly for advanced technical services.

Price competition among facility management providers often leads to margin compression and service quality concerns. The market’s competitive nature encourages aggressive pricing strategies that may compromise service delivery standards. Client expectations for cost reduction while maintaining service quality create operational challenges for facility management companies seeking sustainable business models.

Economic fluctuations and market volatility can impact facility management demand, particularly in discretionary spending categories such as landscaping and aesthetic improvements. Budget constraints during economic downturns may lead to service contract renegotiations or scope reductions, affecting revenue stability for facility management providers.

Technology integration costs and complexity present barriers for smaller facility management companies seeking to compete with larger organizations offering advanced digital solutions. The investment required for building management systems, mobile applications, and data analytics platforms may exceed the financial capabilities of emerging market participants.

Smart city initiatives across the UAE create unprecedented opportunities for facility management providers specializing in technology-enabled services. The integration of IoT sensors, automated systems, and data analytics in urban infrastructure requires sophisticated facility management expertise. Dubai Smart City 2025 and similar initiatives represent substantial market potential for companies capable of delivering intelligent facility management solutions.

Healthcare sector expansion presents significant growth opportunities as the UAE invests in medical infrastructure and healthcare tourism. Specialized facility management requirements for hospitals, clinics, and medical research facilities demand expertise in infection control, medical equipment maintenance, and regulatory compliance. The healthcare facility management segment shows potential for 12% annual growth driven by population expansion and medical tourism development.

Sustainability consulting and green building management services offer differentiation opportunities for facility management providers. The UAE’s commitment to environmental sustainability and carbon neutrality goals creates demand for energy-efficient building operations, waste management optimization, and renewable energy integration. LEED and BREEAM certification support services represent high-value market segments with limited competition.

Industrial facility management opportunities are expanding with the UAE’s manufacturing sector development and free zone growth. Specialized services for industrial facilities, including equipment maintenance, safety compliance, and environmental monitoring, offer stable revenue streams and long-term contract potential.

Supply and demand dynamics in the UAE facility management market reflect the balance between rapid infrastructure development and service provider capacity. Demand growth consistently outpaces supply expansion, creating opportunities for new market entrants and service expansion by existing providers. The market demonstrates resilience to economic fluctuations due to the essential nature of facility management services.

Competitive intensity varies across service segments, with basic maintenance services experiencing high competition while specialized technical services maintain higher barriers to entry. Market consolidation trends are emerging as larger facility management companies acquire smaller specialists to expand service capabilities and geographic coverage.

Client relationship dynamics are evolving toward long-term partnerships rather than transactional service arrangements. Organizations increasingly value facility management providers that demonstrate strategic thinking, innovation capability, and alignment with business objectives. Performance-based contracting models are gaining acceptance, linking service provider compensation to measurable outcomes and client satisfaction metrics.

Technology disruption continues to reshape market dynamics, with traditional service delivery methods being replaced by data-driven, predictive approaches. Facility management providers must continuously invest in technology capabilities to remain competitive and meet evolving client expectations for transparency, efficiency, and innovation.

Primary research methodology for UAE facility management market analysis incorporates comprehensive stakeholder interviews, industry surveys, and direct observation of market trends. Data collection involves structured interviews with facility management executives, client organizations, technology providers, and regulatory authorities to ensure comprehensive market understanding.

Secondary research utilizes government publications, industry reports, trade association data, and academic studies to validate primary research findings and provide historical context. Market sizing methodologies combine top-down and bottom-up approaches to ensure accuracy and reliability of growth projections and market segment analysis.

Quantitative analysis employs statistical modeling techniques to identify market trends, growth patterns, and correlation factors affecting facility management demand. Qualitative assessment incorporates expert opinions, case studies, and best practice analysis to provide strategic insights beyond numerical data.

Data validation processes include cross-referencing multiple sources, expert review panels, and sensitivity analysis to ensure research accuracy and reliability. The methodology ensures comprehensive coverage of market segments, geographic regions, and service categories within the UAE facility management ecosystem.

Dubai emirate dominates the UAE facility management market, accounting for approximately 45% of total market activity. The emirate’s status as a global business hub, extensive commercial real estate portfolio, and thriving hospitality sector drive substantial facility management demand. Dubai International Financial Centre and Dubai Multi Commodities Centre represent key market segments requiring sophisticated facility management services.

Abu Dhabi represents the second-largest regional market, contributing approximately 35% of market share through government facilities, oil and gas infrastructure, and cultural institutions. The emirate’s focus on economic diversification and sustainable development creates opportunities for advanced facility management solutions. Masdar City serves as a showcase for sustainable facility management practices and smart building technologies.

Sharjah and Northern Emirates collectively account for approximately 20% of market activity, driven by industrial development, educational institutions, and residential communities. These regions offer growth opportunities for facility management providers seeking to expand beyond Dubai and Abu Dhabi markets. Cost-conscious clients in these regions often prioritize value-based service delivery over premium offerings.

Regional specialization trends are emerging, with Dubai focusing on luxury and hospitality facility management, Abu Dhabi emphasizing government and institutional services, and Northern Emirates developing industrial and residential facility management expertise. This geographic specialization creates opportunities for targeted service development and market positioning strategies.

Market leadership in the UAE facility management sector is characterized by a mix of international corporations and regional specialists, each bringing unique strengths and service capabilities. The competitive environment fosters innovation and service excellence while creating opportunities for strategic partnerships and market consolidation.

Competitive differentiation strategies include technology integration, sustainability expertise, sector specialization, and comprehensive service portfolios. Companies are increasingly investing in digital platforms, mobile applications, and data analytics capabilities to enhance service delivery and client satisfaction.

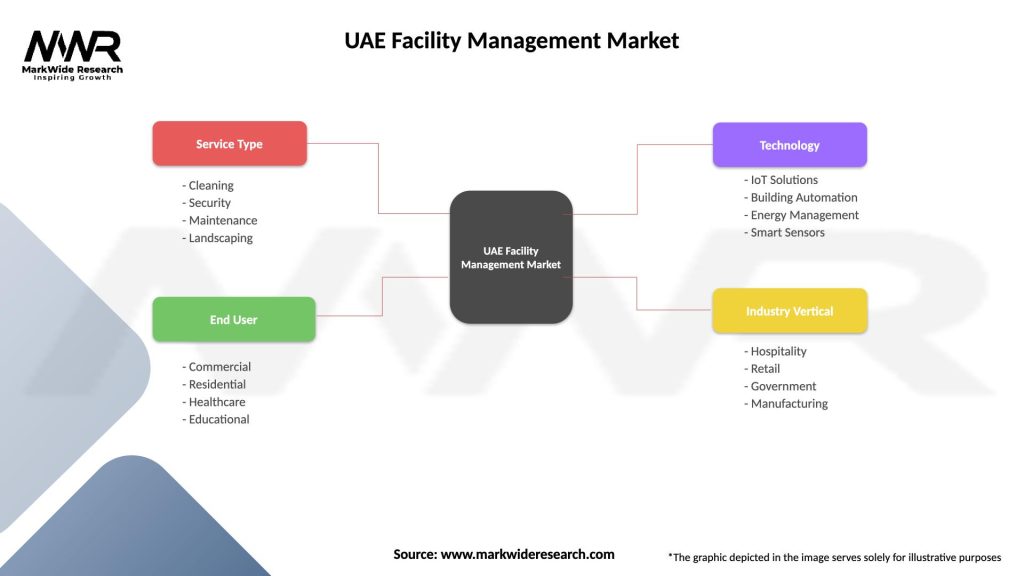

Service-based segmentation reveals diverse facility management categories serving different client needs and operational requirements. The market demonstrates balanced growth across multiple service segments, with integrated solutions gaining preference over single-service offerings.

By Service Type:

By End-User Sector:

Hard services category demonstrates steady growth driven by increasing complexity of building systems and technology integration requirements. HVAC maintenance represents the largest segment within hard services, accounting for approximately 30% of technical service demand. The category benefits from mandatory maintenance requirements and energy efficiency initiatives driving regular service needs.

Soft services category shows resilience and consistent demand across all market segments, with cleaning services representing the most stable revenue stream. Security services are experiencing enhanced demand due to increased safety awareness and regulatory requirements. The integration of technology in soft services, including automated cleaning systems and digital security monitoring, is creating differentiation opportunities.

Integrated facility management category demonstrates the highest growth potential as organizations seek simplified vendor relationships and operational efficiency. Single-source contracting reduces administrative burden while enabling comprehensive service optimization. This category typically commands premium pricing due to the complexity of service coordination and management expertise required.

Specialized services category offers the highest margins and growth potential, particularly in healthcare, industrial, and technology sectors. These services require specific certifications, training, and equipment, creating barriers to entry and enabling premium pricing strategies. Compliance-driven services in this category demonstrate recession-resistant characteristics due to mandatory regulatory requirements.

Client organizations benefit from facility management outsourcing through cost optimization, operational efficiency, and access to specialized expertise. Core business focus is enhanced when facility management responsibilities are transferred to professional service providers, enabling organizations to allocate resources to strategic priorities. Risk mitigation through professional facility management reduces liability exposure and ensures regulatory compliance.

Facility management providers benefit from stable revenue streams, long-term contract relationships, and opportunities for service expansion within existing client accounts. Economies of scale achieved through portfolio management enable cost optimization and competitive pricing strategies. Technology investments are leveraged across multiple client sites, improving return on investment and service capabilities.

Property owners and developers benefit from enhanced asset value, reduced vacancy rates, and improved tenant satisfaction through professional facility management. Preventive maintenance programs extend building lifecycle and reduce capital expenditure requirements. Professional facility management supports premium rental rates and tenant retention in competitive real estate markets.

Government stakeholders benefit from improved public facility operations, enhanced citizen services, and optimized budget utilization through facility management partnerships. Performance-based contracting ensures accountability and measurable service outcomes while transferring operational risks to private sector partners.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation represents the most significant trend reshaping the UAE facility management market. IoT integration enables real-time monitoring of building systems, predictive maintenance scheduling, and energy optimization. Mobile applications and cloud-based platforms are becoming standard tools for service delivery, client communication, and performance reporting.

Sustainability integration is becoming a core requirement rather than an optional service enhancement. Green building operations focus on energy efficiency, waste reduction, and environmental compliance to support UAE sustainability goals. Carbon footprint reduction and renewable energy integration are increasingly important factors in facility management service selection.

Integrated service delivery models are gaining preference as clients seek simplified vendor relationships and operational efficiency. Single-source contracting enables comprehensive service coordination while reducing administrative burden. This trend favors larger facility management providers capable of delivering diverse service portfolios under unified management structures.

Performance-based contracting is emerging as clients demand measurable outcomes and accountability from facility management providers. Key performance indicators linked to service level agreements ensure service quality while enabling continuous improvement initiatives. This trend drives investment in monitoring systems and data analytics capabilities.

Technology partnerships between facility management companies and technology providers are accelerating innovation and service capabilities. Strategic alliances enable facility management providers to offer advanced building automation, energy management, and predictive maintenance solutions without significant internal technology investments.

Market consolidation activities include acquisitions and mergers among facility management providers seeking to expand service capabilities and geographic coverage. International expansion by regional providers and local market entry by global facility management companies are reshaping competitive dynamics and service standards.

Certification and training programs are being developed to address skilled workforce shortages and ensure service quality standards. Professional development initiatives supported by industry associations and government entities aim to build local expertise and reduce dependence on expatriate workers.

Regulatory developments include updated building codes, safety standards, and environmental regulations affecting facility management service requirements. MarkWide Research analysis indicates that regulatory compliance is becoming increasingly complex, driving demand for specialized facility management expertise and creating opportunities for service providers with strong compliance capabilities.

Investment in technology capabilities is essential for facility management providers seeking sustainable competitive advantage. Digital platforms enabling predictive maintenance, energy optimization, and client communication should be prioritized to meet evolving market expectations. Companies should consider strategic partnerships with technology providers to accelerate capability development while managing investment costs.

Workforce development initiatives require immediate attention to address skilled labor shortages and ensure service quality standards. Training programs focusing on technical skills, safety protocols, and customer service should be implemented to build internal capabilities and reduce recruitment challenges. Partnerships with educational institutions and certification bodies can support long-term workforce development objectives.

Service portfolio expansion into high-value segments such as healthcare, industrial, and sustainability consulting offers growth opportunities and margin improvement potential. Specialization strategies enable differentiation from competitors while commanding premium pricing for expertise and certifications. Companies should evaluate market opportunities and invest in capabilities aligned with UAE economic development priorities.

Client relationship management should focus on long-term partnerships rather than transactional service arrangements. Account management strategies emphasizing value creation, innovation, and strategic alignment with client objectives can drive contract renewals and service expansion opportunities. Performance measurement systems should demonstrate tangible value delivery and continuous improvement initiatives.

Market growth prospects for the UAE facility management sector remain positive, supported by continued infrastructure development, economic diversification, and technology adoption. MWR projections indicate sustained growth momentum with expanding opportunities across multiple service segments and geographic regions. The market is expected to benefit from UAE’s position as a regional hub for business, tourism, and innovation.

Technology evolution will continue driving market transformation, with artificial intelligence, machine learning, and automation becoming standard components of facility management service delivery. Smart building integration will create new service categories while potentially reducing demand for traditional maintenance approaches. Facility management providers must adapt to technological changes while maintaining core service excellence.

Sustainability requirements will become increasingly important as the UAE pursues carbon neutrality goals and environmental leadership in the region. Green facility management services focusing on energy efficiency, waste reduction, and environmental compliance will represent significant growth opportunities. Companies developing expertise in sustainability consulting and green building operations will be well-positioned for future success.

Market maturation is expected to drive consolidation among smaller providers while creating opportunities for specialized service companies. Industry standards and professional certifications will become more important for market credibility and client confidence. The market will likely evolve toward higher service standards, greater technology integration, and more sophisticated client relationships over the forecast period.

The UAE facility management market presents substantial growth opportunities driven by robust infrastructure development, economic diversification, and increasing adoption of professional facility management services. Market dynamics favor providers capable of delivering integrated solutions, embracing technology innovation, and demonstrating sustainability expertise. The competitive landscape rewards companies that invest in workforce development, technology capabilities, and client relationship management.

Strategic success factors include technology integration, service portfolio diversification, and geographic expansion beyond traditional Dubai and Abu Dhabi markets. Companies must balance growth ambitions with operational excellence while navigating challenges such as skilled labor shortages and intense price competition. The market’s evolution toward performance-based contracting and integrated service delivery creates opportunities for providers capable of demonstrating measurable value creation.

Future market development will be shaped by smart city initiatives, sustainability requirements, and continued economic growth across the UAE. Facility management providers that align their strategies with these trends while maintaining service excellence will be well-positioned to capitalize on market opportunities and achieve sustainable competitive advantage in this dynamic and growing market.

What is Facility Management?

Facility Management refers to the integrated approach to maintaining and managing buildings, infrastructure, and services to ensure functionality, comfort, safety, and efficiency. It encompasses various services such as cleaning, maintenance, security, and space management.

Who are the key players in the UAE Facility Management Market?

Key players in the UAE Facility Management Market include Emrill Services LLC, Farnek Services LLC, and JLL, among others. These companies provide a range of services from maintenance to energy management, catering to both commercial and residential sectors.

What are the main drivers of growth in the UAE Facility Management Market?

The main drivers of growth in the UAE Facility Management Market include the rapid urbanization and infrastructure development in the region, increasing demand for energy-efficient solutions, and the rising focus on sustainability and compliance with regulations.

What challenges does the UAE Facility Management Market face?

The UAE Facility Management Market faces challenges such as the high competition among service providers, fluctuating demand due to economic conditions, and the need for skilled labor to meet the evolving technological requirements.

What opportunities exist in the UAE Facility Management Market?

Opportunities in the UAE Facility Management Market include the growing trend of smart building technologies, increased investment in green building initiatives, and the potential for expansion into emerging sectors such as healthcare and education.

What trends are shaping the UAE Facility Management Market?

Trends shaping the UAE Facility Management Market include the adoption of digital technologies for operational efficiency, a shift towards integrated facility management solutions, and an emphasis on sustainability practices to reduce environmental impact.

UAE Facility Management Market

| Segmentation Details | Description |

|---|---|

| Service Type | Cleaning, Security, Maintenance, Landscaping |

| End User | Commercial, Residential, Healthcare, Educational |

| Technology | IoT Solutions, Building Automation, Energy Management, Smart Sensors |

| Industry Vertical | Hospitality, Retail, Government, Manufacturing |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the UAE Facility Management Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.