444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The UAE automotive lubricant market represents a dynamic and rapidly evolving sector within the Middle East’s industrial landscape. Market dynamics indicate robust growth driven by expanding automotive manufacturing, increasing vehicle ownership rates, and rising demand for high-performance lubricants. The market encompasses a comprehensive range of products including engine oils, transmission fluids, brake fluids, and specialty automotive lubricants designed for various vehicle types and applications.

Regional positioning places the UAE as a strategic hub for automotive lubricant distribution across the Middle East and North Africa region. The market benefits from the country’s advanced infrastructure, strategic location, and growing automotive sector. Growth projections suggest the market is expanding at a 6.2% CAGR, reflecting strong demand from both passenger and commercial vehicle segments.

Key market characteristics include increasing adoption of synthetic and semi-synthetic lubricants, growing emphasis on fuel efficiency, and rising awareness of environmental sustainability. The market serves diverse applications ranging from passenger cars and commercial vehicles to motorcycles and heavy-duty industrial equipment, creating multiple growth opportunities for market participants.

The UAE automotive lubricant market refers to the comprehensive ecosystem encompassing the production, distribution, and consumption of specialized lubricating products designed for automotive applications within the United Arab Emirates. This market includes engine oils, transmission fluids, gear oils, brake fluids, coolants, and other specialty lubricants essential for vehicle operation and maintenance.

Market scope extends beyond traditional lubricants to include advanced synthetic formulations, bio-based alternatives, and high-performance products designed for modern automotive technologies. The market serves various end-users including individual vehicle owners, automotive service centers, fleet operators, and industrial applications requiring specialized lubrication solutions.

Industry significance lies in its critical role supporting the UAE’s transportation infrastructure, automotive manufacturing sector, and economic diversification initiatives. The market represents a vital component of the broader petrochemical industry while contributing to vehicle performance, fuel efficiency, and environmental sustainability objectives.

Market performance demonstrates consistent growth driven by expanding vehicle populations, increasing consumer awareness of lubricant quality, and technological advancements in automotive engineering. The UAE’s strategic position as a regional trade hub enhances market accessibility and distribution capabilities, supporting sustained market expansion.

Key growth drivers include rising disposable incomes, increasing vehicle ownership rates, and growing demand for premium lubricant products. The market benefits from 78% adoption rate of synthetic and semi-synthetic lubricants among premium vehicle segments, reflecting consumer preference for high-performance products. Additionally, the commercial vehicle segment contributes significantly to market demand, driven by expanding logistics and transportation industries.

Competitive landscape features both international oil companies and regional players competing across various market segments. Market leaders focus on product innovation, distribution network expansion, and strategic partnerships to maintain competitive positioning. The market also witnesses increasing emphasis on sustainability initiatives and environmentally friendly lubricant formulations.

Future prospects remain positive with anticipated growth in electric vehicle adoption, advanced automotive technologies, and continued economic development. Market participants are adapting strategies to address evolving consumer preferences and regulatory requirements while capitalizing on emerging opportunities in specialized lubricant applications.

Strategic insights reveal several critical factors shaping the UAE automotive lubricant market landscape:

Market intelligence indicates strong correlation between economic growth, vehicle sales, and lubricant consumption patterns. The market demonstrates resilience to economic fluctuations while maintaining steady growth trajectory supported by fundamental demand drivers and infrastructure development initiatives.

Primary growth drivers propelling the UAE automotive lubricant market include expanding vehicle ownership rates and increasing consumer awareness of lubricant quality benefits. The growing automotive sector, supported by rising disposable incomes and favorable economic conditions, creates sustained demand for various lubricant products across passenger and commercial vehicle segments.

Infrastructure development initiatives contribute significantly to market growth through expanded transportation networks, logistics operations, and commercial vehicle utilization. The UAE’s strategic investments in road infrastructure, ports, and logistics facilities drive increased vehicle activity and corresponding lubricant consumption. Commercial vehicle growth accounts for approximately 35% of total lubricant demand, reflecting the importance of transportation and logistics sectors.

Technological advancement in automotive engineering creates demand for specialized high-performance lubricants designed for modern engines, transmissions, and drivetrain systems. Vehicle manufacturers’ requirements for specific lubricant specifications drive market evolution toward premium products offering enhanced performance, fuel efficiency, and extended service intervals.

Economic diversification efforts and tourism industry growth contribute to increased vehicle utilization and lubricant consumption. The expanding rental car industry, taxi services, and ride-sharing platforms create additional demand streams for automotive lubricants across various vehicle categories and usage patterns.

Cost considerations represent a significant market restraint, particularly for price-sensitive consumer segments and small fleet operators. Premium synthetic lubricants command higher prices compared to conventional alternatives, potentially limiting adoption rates among cost-conscious consumers despite superior performance benefits.

Market saturation in certain segments creates competitive pressure and margin constraints for market participants. The mature passenger car lubricant segment faces intense competition, requiring companies to differentiate through product innovation, service quality, and brand positioning strategies.

Regulatory complexity and compliance requirements pose challenges for market participants, particularly smaller players lacking resources for extensive testing and certification processes. Environmental regulations and quality standards require ongoing investment in product development and manufacturing capabilities.

Supply chain dependencies on imported raw materials and base oils create potential vulnerabilities to global market fluctuations and geopolitical factors. Transportation costs and logistics complexities can impact product pricing and availability, particularly for specialized lubricant formulations requiring specific additives or components.

Electric vehicle transition presents significant opportunities for specialized lubricant products designed for electric drivetrains, cooling systems, and hybrid vehicle applications. While traditional engine oil demand may moderate, new product categories emerge requiring innovative formulations and technical expertise.

Industrial expansion creates opportunities for specialized lubricants serving manufacturing, construction, and heavy equipment applications. The UAE’s industrial diversification initiatives drive demand for high-performance lubricants in various industrial sectors beyond traditional automotive applications.

Regional export potential leverages the UAE’s strategic location and logistics infrastructure to serve broader Middle East and African markets. Companies can utilize the UAE as a regional hub for lubricant manufacturing, blending, and distribution operations targeting neighboring countries with growing automotive sectors.

Service sector development offers opportunities for integrated service solutions combining lubricant supply with maintenance services, fleet management, and technical support. Service integration represents a growing trend with 42% of commercial customers preferring comprehensive service packages over standalone product purchases.

Sustainability initiatives create opportunities for bio-based lubricants, recycling programs, and environmentally friendly product alternatives. Growing environmental awareness and corporate sustainability commitments drive demand for green lubricant solutions and circular economy approaches.

Demand patterns reflect seasonal variations, economic cycles, and automotive industry trends affecting lubricant consumption across different market segments. Peak demand periods typically align with vehicle maintenance seasons, new vehicle sales cycles, and commercial activity levels throughout the year.

Competitive dynamics involve both global oil companies and regional players competing through product differentiation, pricing strategies, and distribution network development. Market leaders leverage brand recognition, technical expertise, and comprehensive product portfolios to maintain market position while emerging players focus on niche segments and specialized applications.

Technology evolution drives continuous product development and market adaptation to meet changing automotive requirements. Advanced engine technologies, fuel efficiency standards, and emission regulations influence lubricant formulations and performance specifications, requiring ongoing research and development investments.

Supply chain dynamics encompass raw material sourcing, manufacturing processes, distribution networks, and retail channels serving diverse customer segments. Distribution efficiency improvements have resulted in 25% reduction in delivery times to retail outlets, enhancing market responsiveness and customer satisfaction.

Regulatory dynamics include quality standards, environmental regulations, and safety requirements affecting product development, manufacturing processes, and market access. Compliance with international standards and local regulations requires ongoing investment in quality assurance and certification processes.

Research approach encompasses comprehensive primary and secondary research methodologies designed to provide accurate market insights and strategic intelligence. The methodology combines quantitative data analysis with qualitative market assessment to deliver robust market understanding and forecasting capabilities.

Primary research involves direct engagement with market participants including lubricant manufacturers, distributors, automotive service providers, and end-users across various market segments. Structured interviews, surveys, and focus groups provide firsthand insights into market trends, customer preferences, and competitive dynamics.

Secondary research utilizes industry reports, trade publications, regulatory filings, and company disclosures to gather comprehensive market data and validate primary research findings. Government statistics, industry associations, and trade organizations provide additional data sources supporting market analysis and trend identification.

Data validation processes ensure accuracy and reliability through cross-referencing multiple sources, expert consultation, and statistical analysis. Market sizing, growth projections, and competitive assessments undergo rigorous validation to provide credible market intelligence for strategic decision-making.

Analytical framework incorporates market segmentation analysis, competitive positioning assessment, and trend analysis to identify growth opportunities and market dynamics. The methodology provides actionable insights supporting strategic planning, investment decisions, and market entry strategies.

Dubai market represents the largest regional segment, accounting for approximately 45% of total market share, driven by high vehicle density, commercial activity, and tourism-related transportation demand. The emirate’s status as a business hub and tourist destination creates diverse lubricant demand across passenger vehicles, commercial fleets, and rental car operations.

Abu Dhabi region contributes significantly to market demand through government fleet operations, industrial activities, and growing residential vehicle ownership. The capital emirate’s focus on economic diversification and infrastructure development supports sustained lubricant consumption across various applications and vehicle categories.

Northern Emirates including Sharjah, Ajman, and Ras Al Khaimah demonstrate growing market potential driven by industrial development, population growth, and increasing vehicle ownership rates. These regions offer opportunities for market expansion and distribution network development targeting emerging customer segments.

Regional distribution patterns reflect economic activity concentrations, population densities, and transportation infrastructure development. Urban areas account for 82% of total lubricant consumption, while rural and industrial zones represent growing market segments requiring specialized distribution strategies and product offerings.

Cross-border trade activities leverage the UAE’s strategic location for serving regional markets in the Middle East and Africa. The country’s advanced logistics infrastructure and free trade zones facilitate lubricant exports and re-exports, enhancing market opportunities for local and international companies.

Market leadership involves established international oil companies and regional players competing across various market segments and customer categories. The competitive environment emphasizes product quality, brand recognition, distribution capabilities, and technical support services.

Key market participants include:

Competitive strategies encompass product innovation, distribution network expansion, strategic partnerships, and customer service enhancement. Companies invest in research and development, manufacturing capabilities, and market-specific product formulations to maintain competitive positioning and market share growth.

Market consolidation trends involve strategic acquisitions, joint ventures, and partnership arrangements aimed at expanding market reach, enhancing product portfolios, and achieving operational efficiencies. These activities reshape competitive dynamics and create opportunities for market participants to strengthen their positions.

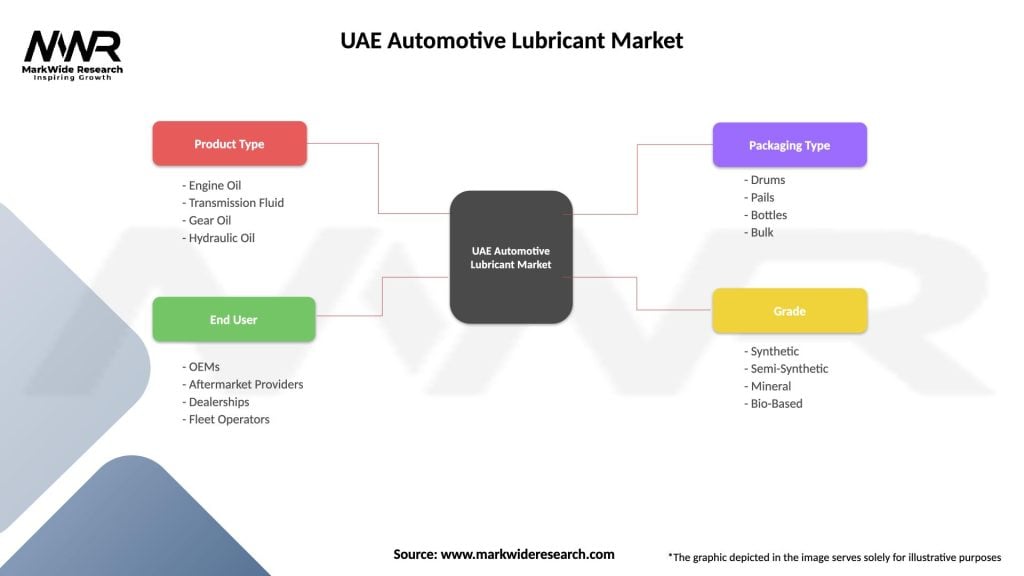

By Product Type:

By Vehicle Type:

By Distribution Channel:

Engine Oil Category dominates market demand with 68% market share, driven by regular maintenance requirements and increasing vehicle populations. Synthetic and semi-synthetic formulations gain popularity due to superior performance characteristics, extended drain intervals, and fuel efficiency benefits. Premium products command higher margins while conventional oils maintain price-competitive positioning.

Transmission Fluid Segment demonstrates steady growth supported by automatic transmission prevalence and commercial vehicle expansion. Advanced formulations designed for modern transmission technologies create opportunities for premium product positioning and technical differentiation among market participants.

Commercial Vehicle Lubricants represent high-value market segments requiring specialized formulations, bulk supply capabilities, and technical support services. Fleet operators prioritize total cost of ownership, equipment reliability, and service support, creating opportunities for integrated service solutions and long-term partnerships.

Specialty Products including brake fluids, coolants, and gear oils offer niche market opportunities with specific technical requirements and regulatory compliance needs. These segments typically feature higher margins and require specialized knowledge and distribution capabilities.

Synthetic Lubricants continue gaining market share driven by performance advantages, environmental benefits, and automotive manufacturer recommendations. Synthetic adoption rates reach 55% in premium vehicle segments, reflecting consumer willingness to invest in superior lubricant performance and protection.

Manufacturers benefit from growing market demand, product differentiation opportunities, and premium pricing potential for advanced lubricant formulations. The market offers multiple growth avenues through product innovation, market expansion, and strategic partnerships with automotive industry participants.

Distributors and Retailers gain from expanding customer base, recurring revenue streams, and opportunities for value-added services. The market provides stable demand patterns with growth potential across various customer segments and geographic regions within the UAE.

Automotive Service Providers benefit from lubricant sales margins, customer retention opportunities, and integrated service offerings. Professional service centers can differentiate through premium lubricant brands, technical expertise, and comprehensive maintenance solutions.

Fleet Operators achieve cost optimization through bulk purchasing, extended service intervals, and improved equipment reliability. Professional lubricant programs offer total cost of ownership benefits, reduced maintenance requirements, and enhanced operational efficiency.

End Consumers benefit from improved vehicle performance, extended engine life, and fuel efficiency gains through quality lubricant products. Access to diverse product options and professional service networks enhances customer satisfaction and vehicle ownership experience.

Economic Stakeholders benefit from job creation, industrial development, and contribution to economic diversification objectives. The lubricant industry supports various economic sectors including manufacturing, logistics, retail, and automotive services.

Strengths:

Weaknesses:

Opportunities:

Threats:

Synthetic Lubricant Adoption continues accelerating across all vehicle segments, driven by superior performance characteristics, extended service intervals, and fuel efficiency benefits. Market penetration of synthetic products reaches 48% overall market share, with particularly strong growth in premium vehicle segments and commercial applications.

Digital Transformation reshapes distribution channels and customer engagement through e-commerce platforms, mobile applications, and digital service booking systems. Online lubricant sales and digital customer interfaces enhance market accessibility and customer convenience while providing valuable market intelligence.

Sustainability Focus drives development of bio-based lubricants, recycling programs, and environmentally friendly packaging solutions. Companies invest in sustainable product alternatives and circular economy initiatives responding to growing environmental awareness and regulatory requirements.

Service Integration trends involve combining lubricant supply with maintenance services, technical support, and fleet management solutions. Integrated service offerings create customer loyalty, recurring revenue streams, and competitive differentiation for market participants.

Premium Product Positioning emphasizes high-performance formulations, brand differentiation, and value-added services. Market participants focus on premium segments offering higher margins and customer loyalty while maintaining competitive positioning in price-sensitive segments.

Regional Hub Development leverages the UAE’s strategic location for serving broader Middle East and African markets through manufacturing, blending, and distribution operations. Companies establish regional headquarters and logistics centers to capitalize on export opportunities and market expansion potential.

Manufacturing Investments include new production facilities, blending plants, and packaging operations established by major lubricant companies. These investments enhance local supply capabilities, reduce logistics costs, and support market growth while creating employment opportunities and industrial development.

Strategic Partnerships between lubricant manufacturers and automotive companies create opportunities for original equipment manufacturer approvals, co-branded products, and integrated service solutions. These partnerships enhance market credibility and access to specific customer segments.

Technology Advancements in lubricant formulations include advanced additive packages, improved base oil technologies, and specialized products for modern automotive applications. Research and development investments focus on performance enhancement, environmental compliance, and cost optimization.

Distribution Network Expansion involves new retail outlets, service centers, and logistics facilities improving market coverage and customer accessibility. Companies invest in distribution infrastructure to enhance market reach and service quality across various customer segments.

Sustainability Initiatives encompass product development, packaging innovations, and recycling programs addressing environmental concerns and regulatory requirements. MarkWide Research indicates that 72% of companies have implemented sustainability programs as part of their strategic initiatives.

Digital Platform Development includes e-commerce capabilities, mobile applications, and digital customer service platforms enhancing market accessibility and customer engagement. Digital transformation initiatives improve operational efficiency and customer satisfaction while providing competitive advantages.

Product Innovation remains critical for maintaining competitive positioning and capturing premium market segments. Companies should invest in advanced formulations, specialized applications, and environmentally friendly alternatives to differentiate their offerings and command higher margins in competitive markets.

Distribution Strategy optimization should focus on multi-channel approaches combining traditional retail, professional service channels, and digital platforms. Comprehensive distribution networks enhance market coverage while providing flexibility to serve diverse customer segments and geographic regions effectively.

Customer Segmentation strategies should recognize distinct requirements across passenger car owners, commercial fleet operators, and industrial customers. Tailored product offerings, service solutions, and pricing strategies can optimize market penetration and customer satisfaction across different segments.

Regional Expansion opportunities should leverage the UAE’s strategic location and infrastructure advantages to serve broader Middle East and African markets. Export-oriented strategies can enhance revenue diversification and growth potential while utilizing existing operational capabilities.

Sustainability Integration should become central to product development, operations, and marketing strategies. Environmental considerations increasingly influence customer decisions and regulatory requirements, making sustainability a competitive necessity rather than optional consideration.

Technology Adoption should encompass both product technology and operational technology to enhance competitiveness and efficiency. Digital platforms, data analytics, and automation can improve customer service, operational efficiency, and market responsiveness.

Market trajectory indicates continued growth driven by expanding automotive sector, increasing vehicle ownership, and rising demand for premium lubricant products. Long-term projections suggest sustained market expansion with annual growth rates maintaining 5.8% to 7.2% range over the forecast period, supported by fundamental demand drivers and economic development initiatives.

Electric vehicle impact will gradually reshape market dynamics while creating new opportunities for specialized lubricants and cooling fluids. Traditional engine oil demand may moderate in the long term, but overall lubricant market growth continues through diversification into new product categories and applications.

Technology evolution will drive continued product development and market sophistication with emphasis on performance enhancement, environmental compliance, and cost optimization. Advanced formulations and specialized applications will create opportunities for premium positioning and market differentiation.

Regional integration will enhance the UAE’s role as a Middle East lubricant hub through expanded manufacturing, distribution, and export capabilities. MWR analysis suggests that regional market integration could increase export opportunities by 35% over the next five years, supporting market growth and diversification.

Sustainability transformation will become increasingly important as environmental regulations evolve and consumer awareness grows. Companies investing in sustainable products and practices will gain competitive advantages while contributing to environmental objectives and regulatory compliance.

The UAE automotive lubricant market demonstrates robust growth potential supported by expanding automotive sector, increasing consumer awareness, and strategic geographic advantages. Market dynamics favor continued expansion through product innovation, distribution network development, and regional integration opportunities.

Strategic positioning as a regional hub enhances long-term growth prospects while creating opportunities for market participants to serve broader Middle East and African markets. The combination of local demand growth and export potential provides multiple avenues for market expansion and revenue diversification.

Industry transformation through technology advancement, sustainability initiatives, and digital integration will reshape competitive dynamics while creating new opportunities for innovative companies. Market participants adapting to evolving trends and customer requirements will achieve sustainable competitive advantages and market leadership positions.

Future success will depend on strategic investments in product development, distribution capabilities, and customer service excellence. Companies focusing on quality, innovation, and customer satisfaction while maintaining operational efficiency will capture the greatest benefits from the UAE automotive lubricant market’s continued growth and evolution.

What is Automotive Lubricant?

Automotive lubricants are substances used to reduce friction between moving parts in vehicles, enhancing performance and longevity. They include engine oils, transmission fluids, and greases, which are essential for the smooth operation of automotive systems.

What are the key players in the UAE Automotive Lubricant Market?

Key players in the UAE Automotive Lubricant Market include ADNOC Distribution, TotalEnergies, and Castrol, among others. These companies offer a range of products tailored to various automotive needs, including synthetic and mineral oils.

What are the growth factors driving the UAE Automotive Lubricant Market?

The growth of the UAE Automotive Lubricant Market is driven by increasing vehicle ownership, rising demand for high-performance lubricants, and advancements in automotive technology. Additionally, the expansion of the automotive sector in the region contributes to market growth.

What challenges does the UAE Automotive Lubricant Market face?

The UAE Automotive Lubricant Market faces challenges such as fluctuating crude oil prices and stringent environmental regulations. These factors can impact production costs and the formulation of lubricants to meet compliance standards.

What opportunities exist in the UAE Automotive Lubricant Market?

Opportunities in the UAE Automotive Lubricant Market include the growing trend towards electric vehicles and the demand for eco-friendly lubricants. Innovations in lubricant formulations and the expansion of distribution networks also present significant growth potential.

What trends are shaping the UAE Automotive Lubricant Market?

Trends in the UAE Automotive Lubricant Market include the shift towards synthetic lubricants, increased focus on sustainability, and the integration of smart technologies in automotive maintenance. These trends reflect changing consumer preferences and advancements in automotive engineering.

UAE Automotive Lubricant Market

| Segmentation Details | Description |

|---|---|

| Product Type | Engine Oil, Transmission Fluid, Gear Oil, Hydraulic Oil |

| End User | OEMs, Aftermarket Providers, Dealerships, Fleet Operators |

| Packaging Type | Drums, Pails, Bottles, Bulk |

| Grade | Synthetic, Semi-Synthetic, Mineral, Bio-Based |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the UAE Automotive Lubricant Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.