444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Turkey OOH and DOOH market represents a dynamic and rapidly evolving advertising landscape that has experienced remarkable transformation in recent years. Out-of-home advertising in Turkey encompasses traditional billboards, transit advertising, and street furniture, while digital out-of-home solutions include LED displays, digital billboards, and interactive kiosks strategically positioned across urban centers. The market demonstrates robust growth potential, driven by increasing urbanization rates of 76.8% and rising consumer mobility patterns throughout major Turkish cities including Istanbul, Ankara, and Izmir.

Market dynamics indicate significant investment in digital infrastructure, with advertisers increasingly recognizing the effectiveness of location-based marketing strategies. The integration of programmatic advertising technologies has revolutionized campaign management, enabling real-time optimization and enhanced targeting capabilities. Digital transformation across the advertising sector has accelerated adoption rates, with DOOH solutions experiencing particularly strong momentum due to their flexibility and measurable impact on consumer engagement.

Geographic distribution reveals concentrated activity in metropolitan areas, where high foot traffic and demographic diversity create optimal conditions for OOH campaigns. The market benefits from Turkey’s strategic position as a bridge between Europe and Asia, attracting international brands seeking regional exposure. Consumer behavior patterns show increasing receptivity to outdoor advertising, particularly among younger demographics who spend significant time in urban environments and public transportation systems.

The Turkey OOH and DOOH market refers to the comprehensive ecosystem of outdoor advertising solutions deployed across Turkish territories, encompassing both traditional static displays and advanced digital advertising platforms. Out-of-home advertising includes billboards, posters, transit advertising, street furniture, and ambient media designed to reach consumers outside their homes and workplaces. Digital out-of-home advertising represents the technological evolution of traditional OOH, incorporating LED screens, digital billboards, interactive displays, and programmatically-enabled advertising networks.

Market scope extends beyond simple advertising placement to include comprehensive campaign management, audience measurement, content creation, and performance analytics. The ecosystem encompasses media owners, advertising agencies, technology providers, content creators, and measurement companies working collaboratively to deliver impactful brand experiences. Strategic positioning within urban environments ensures maximum visibility and engagement opportunities across diverse consumer touchpoints.

Technological integration has transformed traditional outdoor advertising into sophisticated marketing platforms capable of delivering personalized, contextually relevant content. The market includes various formats ranging from large-format billboards and transit advertising to smaller-scale digital screens and interactive installations that create immersive brand experiences for Turkish consumers.

Turkey’s OOH and DOOH market demonstrates exceptional growth trajectory, positioning itself as a critical component of the country’s evolving media landscape. The market benefits from favorable demographic trends, including urbanization acceleration and increasing consumer mobility, which create optimal conditions for outdoor advertising effectiveness. Digital adoption rates have reached 68% among OOH inventory, reflecting the industry’s commitment to technological advancement and advertiser demand for measurable, flexible advertising solutions.

Key market drivers include rising advertising expenditure from both domestic and international brands, government infrastructure investments supporting digital advertising deployment, and growing consumer acceptance of outdoor advertising formats. The market has successfully adapted to changing consumer behaviors, particularly post-pandemic mobility patterns that emphasize outdoor activities and public space utilization. Programmatic advertising adoption has increased by 42% year-over-year, enabling more sophisticated targeting and campaign optimization capabilities.

Competitive landscape features both established international players and emerging local companies, creating a dynamic environment that fosters innovation and competitive pricing. The market’s strategic importance extends beyond advertising revenue generation to include urban beautification, information dissemination, and smart city integration initiatives that align with Turkey’s broader digital transformation objectives.

Market intelligence reveals several critical insights that define the Turkey OOH and DOOH landscape. Consumer engagement metrics demonstrate superior performance compared to traditional media channels, with outdoor advertising achieving 89% weekly reach among urban populations. The market exhibits strong seasonal variations, with peak performance during summer months when outdoor activities and tourism reach maximum levels.

Urbanization acceleration serves as the primary catalyst driving Turkey’s OOH and DOOH market expansion. With urban population growth rates maintaining steady momentum, cities are experiencing increased foot traffic, longer commute times, and greater public space utilization. Infrastructure development projects, including metro expansions, airport modernizations, and shopping center constructions, create new advertising inventory opportunities while enhancing existing location values.

Digital technology adoption across Turkish society has created favorable conditions for DOOH acceptance and engagement. Consumers demonstrate increasing comfort with digital interfaces and expect dynamic, relevant content experiences. Smartphone penetration rates exceeding 78% enable integration between outdoor advertising and mobile marketing strategies, creating comprehensive omnichannel campaigns that amplify message effectiveness and provide measurable consumer interactions.

Economic growth and increasing consumer spending power drive advertiser investment in outdoor advertising channels. Turkish brands are expanding their marketing budgets to include OOH and DOOH solutions, recognizing their effectiveness in building brand awareness and driving purchase consideration. International brand presence continues expanding in Turkish markets, creating additional demand for premium outdoor advertising placements that can effectively reach diverse consumer segments across major metropolitan areas.

Regulatory complexities present ongoing challenges for OOH and DOOH market participants, with varying municipal regulations across different Turkish cities creating compliance difficulties. Permit acquisition processes can be lengthy and complex, potentially delaying campaign launches and increasing operational costs. Zoning restrictions in certain urban areas limit advertising placement opportunities, particularly in historic districts and residential neighborhoods where aesthetic considerations take precedence.

Economic volatility and currency fluctuations impact advertiser spending patterns, creating uncertainty in campaign planning and budget allocation. Seasonal demand variations result in revenue concentration during peak periods, while winter months often experience reduced advertising activity. The market faces challenges from competing media channels, including digital advertising platforms that offer precise targeting and immediate performance measurement capabilities.

Technical infrastructure limitations in certain regions restrict DOOH deployment opportunities, particularly in smaller cities where power supply reliability and internet connectivity may be insufficient for advanced digital advertising systems. Content creation costs for high-quality digital advertising campaigns can be substantial, potentially limiting participation from smaller advertisers who lack resources for professional creative development and ongoing content management.

Smart city initiatives across Turkey present unprecedented opportunities for OOH and DOOH integration with urban infrastructure systems. Government investment in digital infrastructure creates possibilities for advertising networks to contribute to public information systems while generating revenue through commercial messaging. The integration of outdoor advertising with traffic management, weather information, and emergency communication systems enhances public utility while creating new advertising formats.

Programmatic advertising expansion offers significant growth potential, with current adoption rates suggesting substantial room for market development. Data integration capabilities enable sophisticated audience targeting and campaign optimization, attracting advertisers seeking measurable performance outcomes. The opportunity to connect outdoor advertising with mobile marketing, social media campaigns, and e-commerce platforms creates comprehensive marketing ecosystems that deliver superior return on investment.

Tourism recovery and international travel resumption create opportunities for destination marketing, hospitality advertising, and retail campaigns targeting both domestic and international visitors. Event marketing opportunities, including sports events, cultural festivals, and business conferences, provide platforms for premium advertising placements and experiential marketing campaigns that generate significant brand exposure and consumer engagement.

Supply and demand dynamics in Turkey’s OOH and DOOH market reflect the interplay between available advertising inventory and advertiser requirements. Premium location scarcity in high-traffic areas creates competitive pricing environments, while emerging locations offer growth opportunities at more accessible price points. The market demonstrates cyclical patterns aligned with economic conditions, seasonal consumer behavior, and major events that influence advertising demand.

Technology evolution continues reshaping market dynamics, with artificial intelligence integration enabling predictive analytics, automated campaign optimization, and enhanced audience measurement capabilities. MarkWide Research analysis indicates that technology-driven efficiency improvements have increased campaign effectiveness by 34% over the past two years. The integration of Internet of Things sensors, facial recognition technology, and mobile device detection creates new possibilities for audience analysis and campaign personalization.

Competitive pressures drive innovation and service enhancement across the market, with companies investing in proprietary technology platforms, exclusive location partnerships, and comprehensive service offerings. Market consolidation trends create opportunities for strategic partnerships and acquisitions that enhance geographic coverage and service capabilities while maintaining competitive pricing structures.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into Turkey’s OOH and DOOH market landscape. Primary research includes structured interviews with industry executives, media owners, advertising agencies, and technology providers to gather firsthand insights into market trends, challenges, and opportunities. Survey research among advertisers and consumers provides quantitative data on usage patterns, preferences, and effectiveness perceptions.

Secondary research encompasses analysis of industry reports, government statistics, trade association data, and company financial statements to establish market context and validate primary research findings. Market observation through field studies in major Turkish cities provides direct insights into advertising deployment patterns, consumer interaction behaviors, and competitive positioning strategies across different urban environments.

Data triangulation ensures research accuracy by comparing findings across multiple sources and methodologies. Expert validation through industry advisory panels confirms research conclusions and provides additional context for market interpretation. The methodology incorporates both quantitative metrics and qualitative insights to deliver comprehensive market understanding that supports strategic decision-making for market participants.

Istanbul metropolitan area dominates Turkey’s OOH and DOOH market, accounting for approximately 45% of total advertising inventory and revenue generation. The city’s diverse demographics, high tourist volumes, and extensive transportation networks create optimal conditions for outdoor advertising effectiveness. Premium locations including Taksim Square, Bosphorus Bridge approaches, and major shopping districts command premium pricing while delivering exceptional brand exposure opportunities.

Ankara region represents the second-largest market segment, benefiting from government sector advertising, diplomatic community presence, and university populations that create diverse audience segments. Commercial districts and transportation hubs provide strategic advertising placement opportunities, while government infrastructure investments support continued market development. The region demonstrates steady growth patterns with particular strength in public service and corporate advertising categories.

Izmir and Mediterranean coastal regions show strong seasonal performance driven by tourism activities and summer population increases. Resort destinations including Antalya and Bodrum create unique advertising opportunities targeting both domestic and international visitors. Regional cities including Bursa, Adana, and Gaziantep represent emerging opportunities with growing urban populations and increasing commercial activity that supports outdoor advertising market development.

Market leadership in Turkey’s OOH and DOOH sector features a combination of international companies and domestic players, each contributing unique strengths and market positioning strategies. Competitive differentiation occurs through location portfolio quality, technology capabilities, service offerings, and pricing strategies that address diverse advertiser requirements across different market segments.

Strategic partnerships between media owners, technology providers, and advertising agencies create comprehensive service offerings that address complex campaign requirements. Innovation competition drives continuous improvement in measurement capabilities, content management systems, and audience targeting technologies that enhance advertiser value propositions.

Format-based segmentation reveals distinct market characteristics and growth patterns across different OOH and DOOH categories. Traditional billboards maintain significant market presence, particularly in highway locations and urban periphery areas where large-format displays provide maximum visibility for brand awareness campaigns. Digital billboards demonstrate superior growth rates, offering flexibility, dynamic content capabilities, and enhanced measurement opportunities that attract premium advertiser investment.

By Technology:

By Location Category:

Transit advertising demonstrates exceptional performance in Turkey’s urban environments, where extensive public transportation usage creates captive audiences with extended exposure times. Metro advertising particularly excels in Istanbul, Ankara, and Izmir, where subway systems provide controlled environments for premium advertising placements. Airport advertising targets affluent, internationally-minded consumers while benefiting from extended dwell times and high attention levels during travel experiences.

Digital billboard networks show remarkable growth potential, with content flexibility enabling multiple advertiser rotation, seasonal campaign adjustments, and real-time message updates. Programmatic capabilities allow advertisers to optimize campaigns based on weather conditions, traffic patterns, and demographic data, creating more relevant and effective advertising experiences. Interactive installations generate superior engagement rates, particularly among younger demographics who appreciate technology-enabled brand interactions.

Street furniture advertising provides consistent revenue streams while contributing to urban infrastructure development. Bus shelter advertising combines utility with marketing effectiveness, reaching diverse demographic segments across different neighborhoods and commercial districts. Retail environment advertising captures consumers at critical purchase decision moments, creating opportunities for immediate sales impact and brand preference influence.

Advertisers benefit from OOH and DOOH solutions through enhanced brand visibility, broad audience reach, and cost-effective marketing impact compared to traditional media channels. Geographic targeting capabilities enable precise market penetration strategies, while demographic diversity in outdoor environments ensures comprehensive audience coverage across different consumer segments. Brand building effectiveness of outdoor advertising creates lasting consumer impressions that support long-term marketing objectives.

Media owners enjoy stable revenue streams from long-term advertising contracts while benefiting from premium pricing for high-traffic locations. Digital transformation opportunities enable service expansion, operational efficiency improvements, and enhanced client value propositions. Asset utilization optimization through programmatic advertising maximizes revenue potential while reducing unsold inventory challenges.

Technology providers find expanding market opportunities through digital infrastructure development, software solutions, and measurement systems that support industry growth. Urban planners benefit from outdoor advertising contributions to city beautification, public information systems, and infrastructure funding that supports broader urban development objectives. Consumers receive valuable information, entertainment, and aesthetic improvements to urban environments through well-designed outdoor advertising installations.

Strengths:

Weaknesses:

Opportunities:

Threats:

Programmatic advertising adoption represents the most significant trend transforming Turkey’s OOH and DOOH market landscape. Automated buying platforms enable real-time campaign optimization, audience targeting, and performance measurement that attract digital-native advertisers seeking measurable outcomes. Data integration capabilities allow outdoor advertising campaigns to leverage mobile data, weather information, and traffic patterns for enhanced relevance and effectiveness.

Interactive technology integration creates immersive brand experiences that engage consumers actively rather than passively receiving advertising messages. Augmented reality installations, touch-enabled displays, and mobile app integration transform outdoor advertising from simple message delivery to comprehensive brand interaction platforms. Social media integration extends campaign reach beyond physical locations, creating viral marketing opportunities and user-generated content that amplifies advertising impact.

Sustainability focus drives adoption of energy-efficient LED displays, solar-powered installations, and environmentally responsible advertising practices that align with corporate social responsibility objectives. MWR research indicates that 73% of advertisers consider environmental impact when selecting outdoor advertising partners. Smart city alignment creates opportunities for advertising infrastructure to contribute to urban functionality while generating commercial revenue through innovative public-private partnerships.

Digital infrastructure expansion continues accelerating across Turkey’s major metropolitan areas, with significant investments in high-resolution LED displays, fiber optic connectivity, and advanced content management systems. 5G network deployment enables new possibilities for real-time content delivery, interactive advertising experiences, and seamless integration with mobile marketing campaigns that create comprehensive omnichannel strategies.

Strategic partnerships between international technology companies and local media owners create comprehensive service offerings that combine global expertise with local market knowledge. Acquisition activity consolidates market fragmentation while creating larger, more capable organizations that can invest in advanced technology platforms and premium location portfolios. Government digitalization initiatives support outdoor advertising industry development through infrastructure investments and regulatory frameworks that encourage innovation.

Measurement technology advancement provides advertisers with sophisticated analytics capabilities, including facial recognition systems, mobile device detection, and artificial intelligence-powered audience analysis. Privacy-compliant solutions ensure consumer protection while delivering valuable insights that support campaign optimization and advertiser confidence in outdoor advertising effectiveness and return on investment measurement.

Market participants should prioritize digital transformation initiatives that enhance service capabilities and competitive positioning. Investment in programmatic advertising platforms will become essential for maintaining advertiser relationships and capturing market share growth. Location portfolio optimization through strategic acquisitions and partnerships can improve market coverage while reducing operational complexity and costs.

Technology integration should focus on solutions that provide measurable advertiser value, including audience measurement systems, campaign optimization platforms, and interactive capabilities that differentiate outdoor advertising from competing media channels. Data partnerships with mobile operators, retail chains, and transportation authorities can enhance targeting capabilities and campaign effectiveness while creating new revenue opportunities.

Regulatory engagement with municipal authorities and government agencies can help shape favorable policy environments while ensuring compliance with evolving regulations. Sustainability initiatives will become increasingly important for advertiser selection criteria and public acceptance of outdoor advertising installations. International expansion opportunities should be evaluated carefully, considering Turkey’s strategic position for regional market development and cross-border advertising campaigns.

Long-term growth prospects for Turkey’s OOH and DOOH market remain highly favorable, supported by continuing urbanization, economic development, and digital technology adoption. Market maturation will likely result in increased consolidation, technology standardization, and service sophistication that benefits both advertisers and media owners. MarkWide Research projections indicate sustained growth momentum with digital formats expected to represent 85% of total market inventory within the next five years.

Technology evolution will continue driving market transformation, with artificial intelligence, machine learning, and Internet of Things integration creating new possibilities for audience engagement and campaign optimization. Smart city development will provide platforms for outdoor advertising integration with urban infrastructure, creating value for both commercial advertisers and public service communications. Cross-border opportunities may emerge as Turkey’s strategic position enables regional advertising campaigns targeting multiple markets simultaneously.

Advertiser expectations will increasingly focus on measurable outcomes, requiring continued investment in analytics capabilities and performance measurement systems. Consumer privacy considerations will shape technology deployment strategies, emphasizing transparent data usage and consent-based targeting approaches. Environmental sustainability will become a critical factor in location development and technology selection, driving adoption of energy-efficient solutions and environmentally responsible practices.

Turkey’s OOH and DOOH market stands at a pivotal moment of transformation, characterized by robust growth potential, technological advancement, and evolving advertiser requirements. The market’s strategic advantages, including geographic positioning, urbanization trends, and digital infrastructure development, create favorable conditions for sustained expansion and innovation. Digital transformation continues reshaping industry dynamics, with programmatic advertising, interactive technologies, and data-driven campaign optimization becoming standard market expectations.

Market participants who successfully navigate regulatory complexities, invest in advanced technology platforms, and develop comprehensive service offerings will be best positioned to capture growth opportunities and maintain competitive advantages. Collaboration between stakeholders, including media owners, technology providers, advertisers, and government agencies, will be essential for addressing challenges and maximizing market potential. The industry’s contribution to urban development, economic growth, and consumer engagement ensures its continued relevance in Turkey’s evolving media landscape, making it an attractive sector for investment and strategic development initiatives.

What is OOH and DOOH?

OOH stands for Out-Of-Home advertising, which includes any advertising that reaches the consumer while they are outside their home. DOOH, or Digital Out-Of-Home, refers to digital screens used for advertising in public spaces, such as billboards and transit displays.

What are the key players in the Turkey OOH And DOOH Market?

Key players in the Turkey OOH And DOOH Market include companies like Clear Channel, JCDecaux, and Ströer, which provide various advertising solutions across urban environments and transportation hubs, among others.

What are the growth factors driving the Turkey OOH And DOOH Market?

The Turkey OOH And DOOH Market is driven by increasing urbanization, the rise of digital technology, and the growing demand for targeted advertising. These factors enhance the effectiveness of advertising campaigns in high-traffic areas.

What challenges does the Turkey OOH And DOOH Market face?

Challenges in the Turkey OOH And DOOH Market include regulatory restrictions on outdoor advertising, competition from digital media, and the need for continuous technological upgrades to keep pace with consumer expectations.

What opportunities exist in the Turkey OOH And DOOH Market?

The Turkey OOH And DOOH Market presents opportunities for innovation in interactive advertising and the integration of data analytics to enhance audience targeting. Additionally, the expansion of smart city initiatives can further boost market growth.

What trends are shaping the Turkey OOH And DOOH Market?

Trends in the Turkey OOH And DOOH Market include the increasing use of programmatic advertising, the rise of augmented reality experiences, and the growing emphasis on sustainability in advertising practices. These trends are transforming how brands engage with consumers.

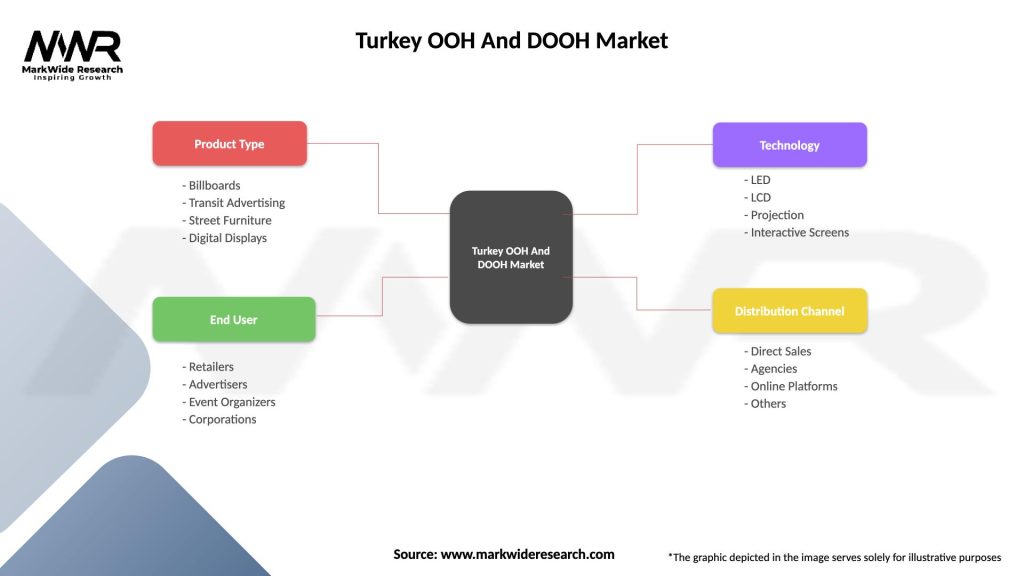

Turkey OOH And DOOH Market

| Segmentation Details | Description |

|---|---|

| Product Type | Billboards, Transit Advertising, Street Furniture, Digital Displays |

| End User | Retailers, Advertisers, Event Organizers, Corporations |

| Technology | LED, LCD, Projection, Interactive Screens |

| Distribution Channel | Direct Sales, Agencies, Online Platforms, Others |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Turkey OOH And DOOH Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.