The transaction banking market serves as a critical component of the global financial system, providing essential services to facilitate financial transactions between businesses, financial institutions, and government entities. Transaction banking encompasses a wide range of services, including cash management, trade finance, liquidity management, and payment processing, which are essential for the efficient functioning of modern economies. As businesses increasingly engage in cross-border trade and seek optimized cash flow management solutions, the demand for transaction banking services continues to grow, driving innovation and competition within the market.

Meaning:

Transaction banking refers to the provision of financial services that facilitate the movement and management of funds between businesses, financial institutions, and government entities. These services include cash management, trade finance, liquidity management, and payment processing, which are essential for businesses to conduct their day-to-day operations and manage their financial resources efficiently. Transaction banking plays a crucial role in supporting domestic and international trade, enabling businesses to streamline their financial processes, mitigate risks, and optimize liquidity management.

Executive Summary:

The transaction banking market is witnessing significant growth driven by globalization, digitalization, and the increasing demand for efficient financial solutions by businesses worldwide. Key trends shaping the market include the adoption of digital technologies, the expansion of cross-border trade, regulatory changes, and the emergence of non-bank competitors. Despite the opportunities presented by market growth, transaction banks face challenges such as margin pressures, regulatory compliance costs, cybersecurity risks, and competition from fintechs. To succeed in this dynamic environment, transaction banks must prioritize innovation, customer-centricity, and operational efficiency.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights:

Digital Transformation: Transaction banks are investing in digital technologies such as artificial intelligence, blockchain, and cloud computing to enhance operational efficiency, improve customer experience, and offer innovative solutions to meet evolving market demands.

Globalization: The increasing globalization of trade and business operations is driving demand for cross-border transaction banking services, including trade finance, foreign exchange, and international payments, as businesses seek to expand their global footprint and access new markets.

Regulatory Compliance: Transaction banks are grappling with stringent regulatory requirements aimed at enhancing transparency, reducing financial crime, and safeguarding customer data. Compliance costs and regulatory complexities pose challenges for banks, requiring ongoing investment in compliance infrastructure and processes.

Competition: Transaction banks face competition from traditional competitors, such as other banks, as well as non-bank entities, including fintechs, payment service providers, and technology companies. To remain competitive, banks must differentiate themselves through innovative product offerings, superior customer service, and strategic partnerships.

Market Drivers:

Global Trade Expansion: The growth of international trade and cross-border transactions is driving demand for transaction banking services, including trade finance, supply chain finance, and export-import financing, as businesses seek efficient and reliable solutions to support their global trade operations.

Digitalization: The digitalization of financial services is transforming the transaction banking landscape, enabling banks to offer innovative digital solutions such as real-time payments, mobile banking, and API-based integrations to streamline financial processes and enhance customer experience.

Efficiency and Cost Reduction: Businesses are increasingly focused on optimizing cash flow management, liquidity, and working capital efficiency to improve financial performance and reduce operational costs. Transaction banking services such as cash management, treasury solutions, and automated payment processing help businesses achieve these objectives.

Risk Mitigation: Transaction banking services play a crucial role in mitigating financial risks for businesses, including credit risk, liquidity risk, foreign exchange risk, and counterparty risk. Banks offer risk management solutions such as hedging instruments, derivatives, and trade finance products to help businesses manage these risks effectively.

Market Restraints:

Regulatory Compliance Burden: Stringent regulatory requirements and compliance obligations impose significant costs and operational burdens on transaction banks, including regulatory reporting, anti-money laundering (AML) measures, Know Your Customer (KYC) requirements, and data privacy regulations.

Margin Compression: Transaction banks face margin pressures due to intense competition, low-interest-rate environments, and fee compression, which erode profitability margins and challenge revenue growth. Banks must innovate and diversify revenue streams to offset margin pressures and maintain profitability.

Cybersecurity Risks: The increasing reliance on digital technologies exposes transaction banks to cybersecurity risks, including data breaches, cyber-attacks, ransomware, and fraud. Banks must invest in robust cybersecurity infrastructure, employee training, and risk management practices to safeguard customer data and protect against cyber threats.

Disintermediation: Non-bank competitors, including fintechs, payment service providers, and technology companies, pose a threat to traditional transaction banks by offering innovative digital solutions and alternative payment methods that bypass traditional banking channels. Banks must adapt to changing market dynamics and collaborate with fintechs to stay competitive.

Market Opportunities:

Emerging Markets: The growth of emerging markets presents opportunities for transaction banks to expand their presence and tap into new market segments, including SMEs, micro-enterprises, and unbanked populations. Banks can leverage digital technologies and innovative solutions to reach underserved markets and offer tailored financial services.

Open Banking: The adoption of open banking frameworks and application programming interfaces (APIs) creates opportunities for transaction banks to collaborate with third-party developers, fintechs, and technology companies to offer integrated financial solutions, personalized services, and value-added products to customers.

E-commerce Growth: The rapid growth of e-commerce and digital payments presents opportunities for transaction banks to provide payment processing, merchant acquiring, and online payment solutions to e-commerce businesses, enabling seamless and secure transactions across digital channels.

Supply Chain Finance: Transaction banks can capitalize on the growing demand for supply chain finance solutions to provide working capital financing, inventory financing, and supplier financing to businesses engaged in global trade and supply chain operations, helping them optimize cash flow and mitigate financial risk.

Market Dynamics:

The transaction banking market operates in a dynamic environment characterized by rapid technological advancements, shifting regulatory landscapes, changing customer expectations, and evolving market dynamics. Banks must adapt to these dynamics by embracing innovation, enhancing operational efficiency, and delivering superior customer value to remain competitive and drive sustainable growth.

Regional Analysis:

The transaction banking market exhibits regional variations in terms of market size, maturity, regulatory frameworks, and competitive dynamics. Major financial centers such as New York, London, Singapore, and Hong Kong serve as hubs for transaction banking activities, attracting multinational corporations, financial institutions, and fintech startups. Regional differences in market dynamics require banks to tailor their strategies and offerings to meet the specific needs and preferences of customers in each market.

Competitive Landscape:

Leading Companies in the Transaction Banking Market:

JPMorgan Chase & Co.

Bank of America Corporation

Citigroup Inc.

HSBC Holdings plc

Wells Fargo & Company

Barclays PLC

Deutsche Bank AG

BNP Paribas SA

Standard Chartered Bank

Industrial and Commercial Bank of China Limited (ICBC)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

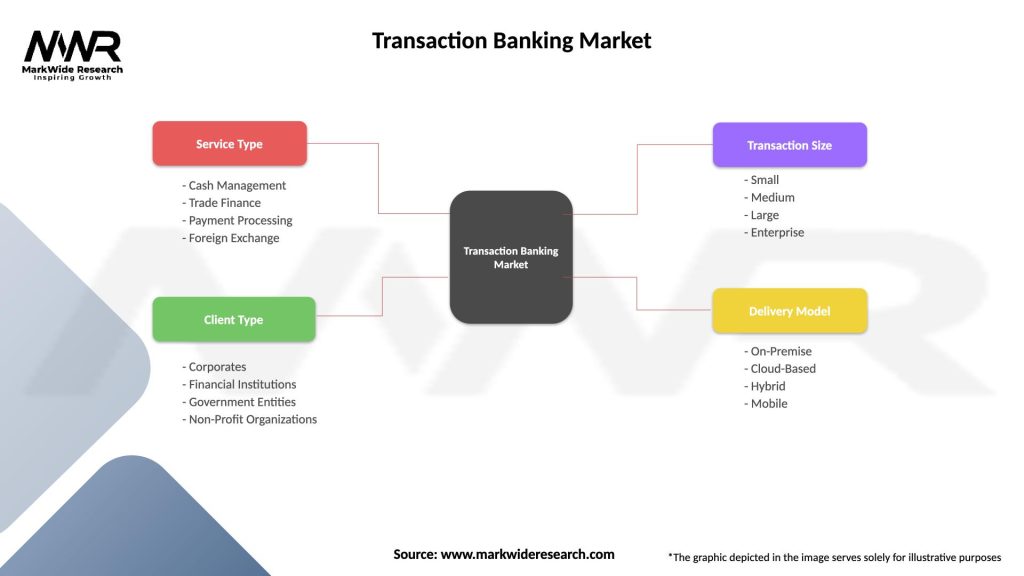

Segmentation:

The transaction banking market can be segmented based on various factors such as:

Service Type: Segmentation by service type includes cash management, trade finance, liquidity management, payment processing, and other financial services tailored to the needs of corporate clients, financial institutions, and government entities.

Customer Segment: Segmentation by customer segment includes corporate banking, commercial banking, SME banking, institutional banking, government banking, and retail banking, reflecting the diverse range of clients served by transaction banks.

Geography: Segmentation by geography includes regional markets such as North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa, each with its unique market characteristics, regulatory environments, and growth opportunities.

Category-wise Insights:

Cash Management: Cash management services enable businesses to optimize their cash flow, liquidity, and working capital management through solutions such as cash pooling, cash concentration, cash forecasting, and automated cash management platforms.

Trade Finance: Trade finance services facilitate international trade and commerce by providing financing, risk mitigation, and documentary services such as letters of credit, trade finance loans, export-import financing, and supply chain finance solutions.

Payment Processing: Payment processing services enable businesses to send, receive, and reconcile payments efficiently through channels such as wire transfers, Automated Clearing House (ACH) payments, real-time payments, electronic funds transfers (EFTs), and card payments.

Liquidity Management: Liquidity management services help businesses optimize their cash reserves, investment portfolios, and liquidity buffers to meet short-term and long-term funding requirements, mitigate liquidity risks, and maximize returns on idle cash.

Key Benefits for Industry Participants and Stakeholders:

Efficiency: Transaction banking services help businesses streamline their financial processes, automate routine tasks, and improve operational efficiency, enabling them to focus on core business activities and strategic initiatives.

Risk Management: Transaction banks provide risk management solutions such as hedging instruments, derivatives, insurance products, and regulatory compliance services to help businesses mitigate financial risks and protect against market volatility.

Liquidity Optimization: Transaction banking services enable businesses to optimize their cash flow, liquidity, and working capital management, ensuring adequate funding for operational needs, capital expenditures, and growth initiatives.

Global Reach: Transaction banks offer international banking services, cross-border payment solutions, and trade finance products that enable businesses to expand their global footprint, enter new markets, and access international trade opportunities.

SWOT Analysis:

Strengths:

Extensive network of branches and correspondent banks

Breadth of product offerings and financial solutions

Strong regulatory compliance and risk management practices

Established brand reputation and customer relationships

Weaknesses:

Margin pressures and fee compression

Legacy systems and infrastructure limitations

Cybersecurity vulnerabilities and data privacy concerns

Regulatory compliance costs and complexities

Opportunities:

Digital innovation and technology adoption

Emerging market expansion and growth opportunities

Open banking and collaboration with fintechs

E-commerce growth and digital payments adoption

Threats:

Competition from non-bank entities and fintechs

Regulatory changes and compliance requirements

Cybersecurity risks and data breaches

Economic uncertainty and geopolitical tensions

Understanding these factors through a SWOT analysis helps transaction banks identify their strengths, address weaknesses, capitalize on opportunities, and mitigate potential threats to their business operations and market position.

Market Key Trends:

Digital Transformation: Transaction banks are undergoing digital transformation initiatives to modernize their infrastructure, enhance customer experience, and offer innovative digital solutions such as mobile banking, API integrations, and real-time payments.

Open Banking: The adoption of open banking frameworks and APIs enables transaction banks to collaborate with third-party developers, fintechs, and technology firms to offer integrated financial solutions, personalized services, and value-added products to customers.

Real-Time Payments: The shift towards real-time payments and instant settlement systems is driving demand for faster, more efficient payment processing solutions that enable businesses to send and receive payments in real-time, improving cash flow and liquidity management.

Data Analytics and AI: Transaction banks are leveraging data analytics, artificial intelligence (AI), and machine learning (ML) technologies to gain insights into customer behavior, identify patterns, detect fraud, and offer personalized financial services and recommendations.

Covid-19 Impact:

The Covid-19 pandemic has had a profound impact on the transaction banking market, accelerating digitalization, changing customer behavior, and reshaping market dynamics. Some key impacts of Covid-19 on the market include:

Remote Workforce: The shift to remote work and virtual collaboration has increased demand for digital banking solutions, online payments, and remote access to financial services, driving adoption of digital channels and self-service banking options.

E-commerce Boom: The surge in e-commerce and online shopping during the pandemic has led to increased demand for digital payments, payment processing services, and fraud prevention solutions to support online transactions and mitigate risks.

Cashless Payments: The pandemic has accelerated the shift towards cashless payments, contactless transactions, and mobile wallets as consumers and businesses seek safer and more convenient payment methods to minimize physical contact and reduce the risk of virus transmission.

Supply Chain Disruptions: The pandemic has disrupted global supply chains, trade flows, and economic activities, leading to increased demand for trade finance, supply chain financing, and working capital solutions to support businesses and mitigate financial risks.

Key Industry Developments:

Digital Onboarding: Transaction banks are investing in digital onboarding processes and remote account opening solutions to streamline customer acquisition, improve account activation rates, and enhance customer experience through digital channels.

Real-Time Payments: The adoption of real-time payments systems and instant settlement platforms is gaining momentum, driven by increasing demand for faster, more efficient payment processing solutions that enable instant fund transfers and real-time transaction monitoring.

Blockchain and DLT: Transaction banks are exploring the potential of blockchain technology and distributed ledger technology (DLT) to improve transparency, reduce transaction costs, and streamline cross-border payments, trade finance, and supply chain operations.

Embedded Finance: The emergence of embedded finance models and banking-as-a-service (BaaS) platforms enables transaction banks to offer embedded financial services, integrated payment solutions, and white-labeled banking products to non-financial businesses, fintechs, and technology companies.

Analyst Suggestions:

Embrace Digital Transformation: Transaction banks should embrace digital transformation initiatives to modernize their infrastructure, enhance operational efficiency, and deliver seamless, personalized digital experiences to customers across digital channels.

Focus on Innovation: Transaction banks should prioritize innovation and invest in emerging technologies such as AI, blockchain, and real-time payments to develop innovative financial products, streamline processes, and drive business growth.

Enhance Cybersecurity: Transaction banks should strengthen their cybersecurity posture by implementing robust cybersecurity measures, conducting regular security assessments, and enhancing employee training to mitigate cyber threats and protect customer data.

Customer-Centricity: Transaction banks should adopt a customer-centric approach by understanding customer needs, preferences, and pain points and designing solutions that meet their expectations, add value, and enhance customer satisfaction and loyalty.

Future Outlook:

The transaction banking market is poised for continued growth and innovation, driven by digital transformation, globalization, regulatory changes, and evolving customer demands. Banks that prioritize innovation, customer-centricity, and operational excellence are likely to thrive in a rapidly evolving market landscape and capitalize on opportunities for growth and expansion.

Conclusion:

The transaction banking market plays a crucial role in facilitating financial transactions, supporting global trade, and driving economic growth. With increasing digitalization, globalization, and regulatory changes, transaction banks must innovate, adapt, and differentiate themselves to stay competitive and meet the evolving needs of customers. By embracing digital transformation, enhancing operational efficiency, and delivering superior customer value, transaction banks can navigate market challenges, capitalize on opportunities, and drive sustainable growth in the future.

What is Transaction Banking?

Transaction Banking refers to a suite of services provided by banks to facilitate the management of cash flow, payments, and other financial transactions for businesses and institutions. It includes services such as payment processing, trade finance, and liquidity management.

What are the key players in the Transaction Banking Market?

Key players in the Transaction Banking Market include JPMorgan Chase, Citigroup, HSBC, and Deutsche Bank, among others. These institutions offer a range of transaction banking services to corporate clients and financial institutions.

What are the main drivers of growth in the Transaction Banking Market?

The main drivers of growth in the Transaction Banking Market include the increasing demand for efficient payment solutions, the rise of e-commerce, and the need for enhanced cash management services. Additionally, globalization has led to a greater need for cross-border transaction capabilities.

What challenges does the Transaction Banking Market face?

The Transaction Banking Market faces challenges such as regulatory compliance, cybersecurity threats, and the need for technological upgrades. Banks must navigate complex regulations while ensuring the security of transactions and adapting to rapidly changing technology.

What opportunities exist in the Transaction Banking Market?

Opportunities in the Transaction Banking Market include the adoption of digital banking solutions, the integration of artificial intelligence for transaction processing, and the expansion of services to emerging markets. These trends can enhance customer experience and operational efficiency.

What trends are shaping the Transaction Banking Market?

Trends shaping the Transaction Banking Market include the increasing use of blockchain technology for secure transactions, the rise of mobile banking applications, and the focus on sustainability in banking practices. These innovations are transforming how banks operate and serve their clients.

Leading Companies in the Transaction Banking Market:

JPMorgan Chase & Co.

Bank of America Corporation

Citigroup Inc.

HSBC Holdings plc

Wells Fargo & Company

Barclays PLC

Deutsche Bank AG

BNP Paribas SA

Standard Chartered Bank

Industrial and Commercial Bank of China Limited (ICBC)

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.