444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

What is Third-party Medical Diagnosis?

Third-party medical diagnosis refers to the evaluation and interpretation of medical data by an independent entity, often to provide unbiased insights into a patient’s health condition. This process can involve various diagnostic tests and assessments conducted outside the primary healthcare provider’s office.

What are the key players in the Third-party Medical Diagnosis Market?

Key players in the third-party medical diagnosis market include LabCorp, Quest Diagnostics, and Siemens Healthineers, which provide a range of diagnostic services and technologies. These companies are known for their extensive laboratory networks and innovative diagnostic solutions, among others.

What are the growth factors driving the Third-party Medical Diagnosis Market?

The growth of the third-party medical diagnosis market is driven by increasing demand for accurate and timely diagnoses, advancements in diagnostic technologies, and the rising prevalence of chronic diseases. Additionally, the growing emphasis on preventive healthcare is contributing to market expansion.

What challenges does the Third-party Medical Diagnosis Market face?

Challenges in the third-party medical diagnosis market include regulatory hurdles, data privacy concerns, and the need for standardization in diagnostic procedures. These factors can hinder the adoption of third-party services and affect overall market growth.

What opportunities exist in the Third-party Medical Diagnosis Market?

Opportunities in the third-party medical diagnosis market include the integration of artificial intelligence in diagnostic processes, expansion into emerging markets, and the development of personalized medicine approaches. These trends can enhance diagnostic accuracy and improve patient outcomes.

What trends are shaping the Third-party Medical Diagnosis Market?

Current trends in the third-party medical diagnosis market include the increasing use of telemedicine for remote diagnostics, the rise of home testing kits, and the growing focus on patient-centric care. These innovations are transforming how diagnostic services are delivered and accessed.

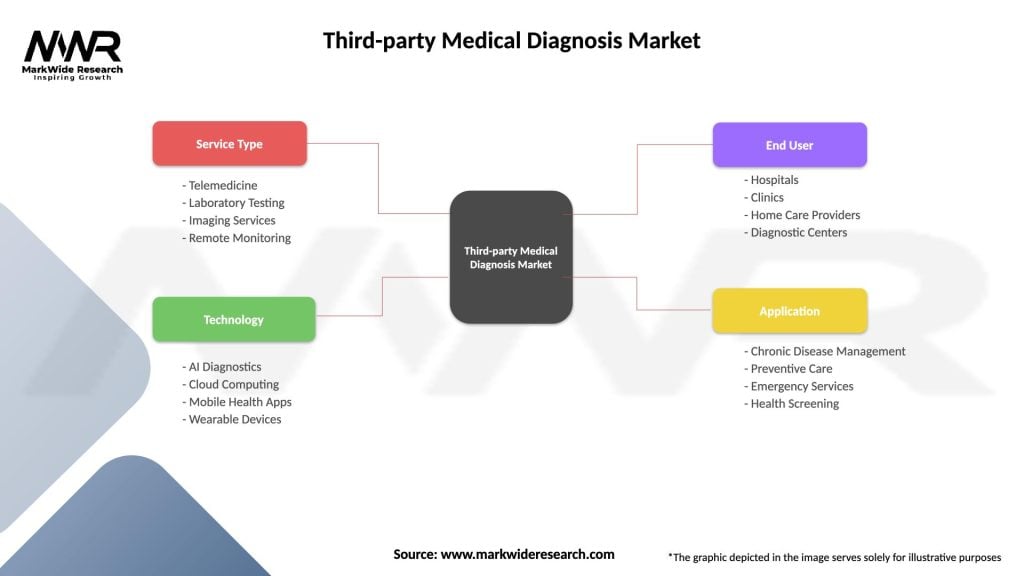

Third-party Medical Diagnosis Market

| Segmentation Details | Description |

|---|---|

| Service Type | Telemedicine, Laboratory Testing, Imaging Services, Remote Monitoring |

| Technology | AI Diagnostics, Cloud Computing, Mobile Health Apps, Wearable Devices |

| End User | Hospitals, Clinics, Home Care Providers, Diagnostic Centers |

| Application | Chronic Disease Management, Preventive Care, Emergency Services, Health Screening |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Third-party Medical Diagnosis Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA