444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Thailand oral antidiabetic drug market represents a critical component of the nation’s healthcare landscape, addressing the growing prevalence of diabetes mellitus across the population. Thailand’s pharmaceutical sector has witnessed substantial expansion in diabetes management solutions, driven by increasing awareness of metabolic disorders and improved healthcare accessibility. The market encompasses various therapeutic classes including metformin, sulfonylureas, DPP-4 inhibitors, and SGLT-2 inhibitors, each serving distinct patient populations with varying clinical needs.

Market dynamics indicate robust growth potential, with the sector experiencing a compound annual growth rate (CAGR) of 6.2% over recent years. This expansion reflects Thailand’s commitment to addressing the diabetes epidemic through comprehensive pharmaceutical interventions. Healthcare infrastructure improvements and government initiatives supporting diabetes care have created favorable conditions for market development, positioning Thailand as a significant player in the Southeast Asian pharmaceutical landscape.

Regional healthcare policies emphasize preventive care and early intervention strategies, contributing to increased demand for oral antidiabetic medications. The market benefits from Thailand’s strategic location as a healthcare hub in Southeast Asia, attracting both domestic and international pharmaceutical companies seeking to establish manufacturing and distribution networks. Patient demographics show approximately 65% of diabetic patients rely on oral medications as their primary treatment modality, highlighting the market’s fundamental importance in diabetes management protocols.

The Thailand oral antidiabetic drug market refers to the comprehensive ecosystem of pharmaceutical products, distribution networks, and healthcare services dedicated to managing diabetes mellitus through oral medication therapies within Thailand’s borders. This market encompasses prescription medications designed to regulate blood glucose levels, improve insulin sensitivity, and prevent diabetic complications through non-injectable treatment approaches.

Market scope includes various drug classifications such as biguanides, thiazolidinediones, alpha-glucosidase inhibitors, and newer therapeutic classes like SGLT-2 inhibitors and GLP-1 receptor agonists available in oral formulations. The definition extends beyond mere pharmaceutical products to include regulatory frameworks, pricing mechanisms, insurance coverage policies, and healthcare provider networks that facilitate patient access to these essential medications.

Healthcare integration within this market involves collaboration between pharmaceutical manufacturers, healthcare providers, regulatory authorities, and patient advocacy groups to ensure optimal diabetes management outcomes. The market’s meaning encompasses both therapeutic efficacy and economic accessibility, reflecting Thailand’s commitment to providing comprehensive diabetes care across diverse socioeconomic populations while maintaining sustainable healthcare financing models.

Thailand’s oral antidiabetic drug market demonstrates remarkable resilience and growth potential, driven by increasing diabetes prevalence and evolving treatment paradigms. The market landscape features diverse therapeutic options catering to varying patient needs, from traditional metformin-based therapies to innovative combination treatments offering enhanced glycemic control and reduced side effect profiles.

Key market drivers include rising diabetes incidence rates, aging population demographics, and improved healthcare accessibility through universal coverage schemes. Government initiatives supporting diabetes prevention and management have created favorable regulatory environments, encouraging pharmaceutical investment and innovation. The market benefits from Thailand’s position as a regional manufacturing hub, with local production accounting for approximately 45% of domestic consumption.

Competitive dynamics reveal a balanced mix of multinational pharmaceutical companies and domestic manufacturers, fostering healthy competition and price optimization. Market segmentation shows metformin-based products maintaining dominant market share, while newer therapeutic classes experience rapid adoption rates among healthcare providers seeking improved patient outcomes. Future projections indicate sustained growth momentum, supported by ongoing research and development initiatives and expanding healthcare infrastructure across rural and urban regions.

Market intelligence reveals several critical insights shaping Thailand’s oral antidiabetic drug landscape. Patient preferences increasingly favor combination therapies offering simplified dosing regimens and improved compliance rates, driving pharmaceutical companies to develop innovative formulations addressing multiple therapeutic targets simultaneously.

Demographic analysis indicates that approximately 72% of patients prefer oral medications over injectable alternatives, emphasizing the market’s fundamental role in diabetes management strategies. Healthcare providers report increased confidence in prescribing newer oral antidiabetic agents due to improved safety profiles and clinical evidence supporting their efficacy in diverse patient populations.

Primary market drivers propelling Thailand’s oral antidiabetic drug market include the escalating diabetes epidemic, demographic transitions, and healthcare system modernization. Epidemiological data reveals diabetes prevalence rates increasing annually, creating sustained demand for effective oral therapeutic interventions across all age groups and socioeconomic segments.

Lifestyle factors contributing to market growth include urbanization trends, dietary pattern changes, and reduced physical activity levels among Thailand’s population. These societal shifts have resulted in increased type 2 diabetes incidence, particularly among younger demographics previously considered low-risk populations. Healthcare awareness campaigns have improved early diabetes detection rates, leading to earlier treatment initiation and prolonged medication therapy requirements.

Government healthcare policies supporting universal health coverage have significantly expanded patient access to oral antidiabetic medications, removing financial barriers that previously limited treatment options. Pharmaceutical industry investment in research and development has accelerated the introduction of innovative therapeutic options, providing healthcare providers with enhanced tools for personalized diabetes management. Economic development and rising disposable incomes enable patients to afford newer, more effective medications, driving market expansion toward premium therapeutic segments.

Healthcare infrastructure improvements including expanded pharmacy networks, improved cold chain logistics, and enhanced medication distribution systems have increased product availability across urban and rural regions. Medical education initiatives have improved healthcare provider knowledge regarding optimal prescribing practices, leading to more appropriate medication selection and improved patient outcomes.

Market constraints affecting Thailand’s oral antidiabetic drug sector include regulatory challenges, pricing pressures, and healthcare system limitations. Regulatory approval processes for new medications can be lengthy and complex, delaying market entry for innovative therapeutic options and limiting patient access to cutting-edge treatments.

Economic factors such as healthcare budget constraints and insurance coverage limitations restrict patient access to newer, more expensive oral antidiabetic medications. Generic competition intensifies pricing pressures on branded products, potentially limiting pharmaceutical companies’ investment in research and development activities. Healthcare provider education gaps may result in suboptimal prescribing practices, affecting market growth for newer therapeutic classes.

Patient compliance challenges including medication adherence issues, side effect concerns, and complex dosing regimens can limit market expansion and therapeutic effectiveness. Rural healthcare access limitations may restrict medication availability in remote regions, creating geographic disparities in treatment options. Cultural factors and traditional medicine preferences among certain population segments may influence acceptance of modern pharmaceutical interventions.

Supply chain vulnerabilities including raw material shortages, manufacturing disruptions, and distribution challenges can affect product availability and market stability. Counterfeit medication concerns pose risks to patient safety and market integrity, requiring enhanced regulatory oversight and authentication systems.

Emerging opportunities within Thailand’s oral antidiabetic drug market include technological innovations, market expansion initiatives, and strategic partnerships. Digital health integration offers possibilities for developing smart medication management systems, improving patient adherence, and enhancing therapeutic outcomes through real-time monitoring and feedback mechanisms.

Pharmaceutical innovation opportunities include developing combination therapies targeting multiple pathophysiological pathways, creating personalized medicine approaches based on genetic markers, and formulating extended-release preparations improving dosing convenience. Market expansion into underserved rural regions presents significant growth potential, supported by government initiatives improving healthcare infrastructure and medication accessibility.

Strategic partnerships between international pharmaceutical companies and local manufacturers can facilitate technology transfer, reduce production costs, and accelerate market penetration. Export opportunities to neighboring Southeast Asian countries leverage Thailand’s manufacturing capabilities and regulatory expertise, creating additional revenue streams for domestic pharmaceutical companies.

Healthcare technology integration including telemedicine platforms, electronic prescribing systems, and patient monitoring applications creates opportunities for comprehensive diabetes management solutions. Educational program development targeting healthcare providers and patients can improve treatment outcomes and expand market acceptance of newer therapeutic options. Research collaboration with academic institutions and international organizations can accelerate clinical development and regulatory approval processes for innovative oral antidiabetic medications.

Market dynamics within Thailand’s oral antidiabetic drug sector reflect complex interactions between supply and demand factors, regulatory influences, and competitive pressures. Demand patterns show increasing preference for combination therapies and once-daily formulations, driving pharmaceutical companies to prioritize convenience-focused product development strategies.

Supply chain dynamics emphasize local manufacturing capabilities, with domestic production facilities achieving international quality standards and serving both local and export markets. Competitive dynamics feature intense rivalry between multinational corporations and local pharmaceutical companies, resulting in continuous innovation and competitive pricing strategies benefiting patients and healthcare systems.

Regulatory dynamics influence market entry timelines, pricing mechanisms, and quality standards, with authorities balancing innovation encouragement and patient safety protection. Economic dynamics including currency fluctuations, raw material costs, and healthcare spending patterns affect market profitability and investment decisions. Technological dynamics drive product differentiation through advanced drug delivery systems, improved formulations, and enhanced therapeutic profiles.

Healthcare provider dynamics show increasing adoption of evidence-based prescribing practices, with clinical guidelines emphasizing individualized treatment approaches and combination therapy strategies. Patient dynamics reveal growing awareness of diabetes management importance and increased willingness to invest in effective therapeutic options, supporting market growth for premium products.

Research methodology employed for analyzing Thailand’s oral antidiabetic drug market incorporates comprehensive primary and secondary research approaches, ensuring robust data collection and analysis. Primary research includes structured interviews with healthcare providers, pharmaceutical industry executives, regulatory officials, and patient advocacy representatives to gather firsthand insights into market dynamics and trends.

Secondary research encompasses analysis of government health statistics, pharmaceutical industry reports, clinical trial databases, and academic publications to establish market baseline data and identify growth patterns. Data validation processes involve cross-referencing multiple sources and conducting expert interviews to ensure accuracy and reliability of market intelligence.

Quantitative analysis utilizes statistical modeling techniques to project market trends, assess competitive positioning, and evaluate growth opportunities. Qualitative analysis examines market dynamics, regulatory influences, and strategic implications affecting industry participants and stakeholders. Market segmentation analysis categorizes products by therapeutic class, distribution channel, and patient demographics to identify specific growth opportunities and competitive advantages.

Competitive intelligence gathering involves monitoring pharmaceutical company activities, product launches, pricing strategies, and market share developments. Regulatory analysis tracks policy changes, approval processes, and compliance requirements affecting market operations. Technology assessment evaluates emerging innovations and their potential impact on market dynamics and competitive positioning.

Regional analysis of Thailand’s oral antidiabetic drug market reveals significant geographic variations in consumption patterns, healthcare infrastructure, and market penetration rates. Bangkok metropolitan region dominates market consumption, accounting for approximately 35% of total market volume, driven by concentrated healthcare facilities, higher income levels, and superior medication accessibility.

Northern regions including Chiang Mai and surrounding provinces demonstrate growing market potential, supported by healthcare infrastructure improvements and increasing diabetes awareness programs. Northeastern regions show rapid market expansion, with government initiatives targeting rural healthcare access contributing to increased medication availability and patient enrollment in diabetes management programs.

Southern regions benefit from established pharmaceutical distribution networks and medical tourism infrastructure, creating opportunities for premium product positioning and specialized diabetes care services. Central regions surrounding Bangkok experience spillover effects from metropolitan healthcare developments, resulting in improved medication access and treatment options for diabetic patients.

Rural market penetration remains challenging but presents significant growth opportunities, with government healthcare initiatives targeting underserved populations through mobile clinics, telemedicine programs, and community health worker training. Regional healthcare disparities influence prescribing patterns and medication preferences, with rural areas showing higher reliance on generic formulations and basic therapeutic options.

Distribution network analysis reveals regional variations in pharmacy density, with urban areas maintaining comprehensive coverage while rural regions require innovative delivery solutions including online pharmacies and community health centers.

Competitive landscape within Thailand’s oral antidiabetic drug market features diverse participants ranging from multinational pharmaceutical corporations to domestic manufacturers and generic drug producers. Market leadership positions are determined by product portfolio breadth, distribution network strength, and clinical evidence supporting therapeutic efficacy.

Competitive strategies emphasize product differentiation through advanced formulations, strategic pricing, and comprehensive patient support programs. Market share distribution shows relatively balanced competition, with no single company dominating more than 25% of total market volume. Innovation focus drives companies toward developing combination therapies, extended-release formulations, and personalized medicine approaches addressing specific patient populations and clinical needs.

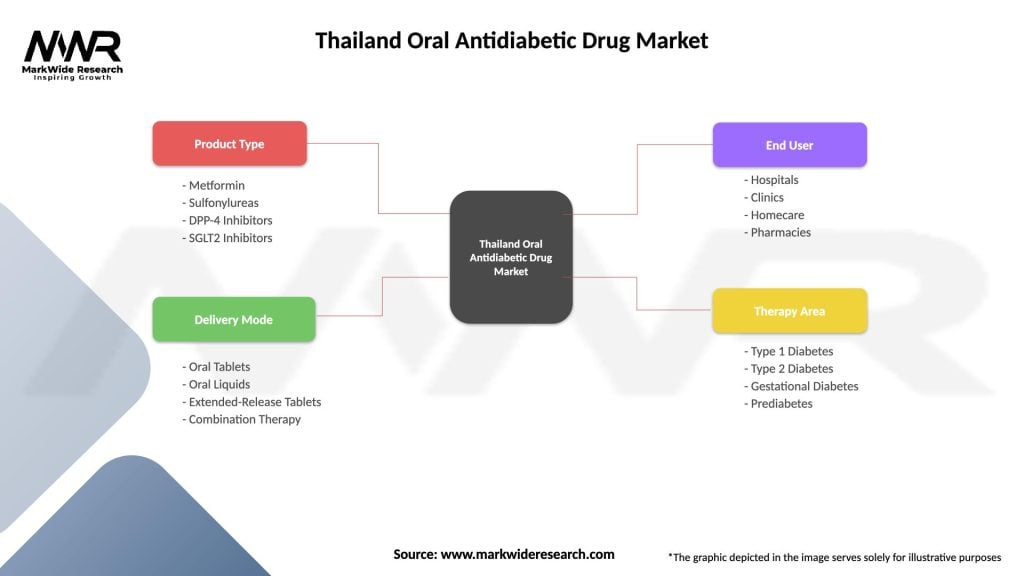

Market segmentation of Thailand’s oral antidiabetic drug market reveals distinct categories based on therapeutic class, distribution channel, patient demographics, and geographic regions. Therapeutic segmentation represents the primary classification method, with each drug class serving specific patient populations and clinical indications.

By Therapeutic Class:

By Distribution Channel:

By Patient Demographics:

Category-wise analysis provides detailed insights into specific therapeutic segments within Thailand’s oral antidiabetic drug market, revealing unique growth patterns, competitive dynamics, and clinical adoption trends. Metformin-based products maintain market leadership due to established clinical evidence, favorable safety profiles, and cost-effectiveness advantages supporting widespread prescribing practices.

DPP-4 inhibitor category demonstrates robust growth momentum, with healthcare providers increasingly prescribing these medications due to low hypoglycemia risk and weight-neutral effects. Clinical adoption rates for DPP-4 inhibitors show annual growth of approximately 12%, reflecting physician confidence and patient acceptance of this therapeutic class.

SGLT-2 inhibitor segment represents the fastest-growing category, driven by emerging clinical evidence supporting cardiovascular and renal protection benefits beyond glucose control. Market penetration for SGLT-2 inhibitors remains relatively low but shows accelerating adoption among specialists and informed primary care providers.

Combination therapy category experiences significant expansion, with fixed-dose combinations offering improved patient compliance and simplified treatment regimens. Healthcare providers increasingly favor combination products for patients requiring multiple therapeutic mechanisms to achieve glycemic targets. Generic competition intensifies across established categories, particularly metformin and sulfonylurea segments, driving price optimization and market accessibility improvements.

Premium therapeutic segments including newer drug classes command higher prices but demonstrate superior clinical outcomes, creating value-based prescribing opportunities for healthcare providers seeking optimal patient management solutions.

Industry participants within Thailand’s oral antidiabetic drug market benefit from diverse opportunities including market expansion, technological innovation, and strategic partnerships. Pharmaceutical manufacturers gain access to growing patient populations, supportive regulatory environments, and established distribution networks facilitating market penetration and revenue growth.

Healthcare providers benefit from expanded therapeutic options, improved patient outcomes, and enhanced clinical decision-making tools supporting evidence-based diabetes management. Educational programs and clinical support services provided by pharmaceutical companies improve prescribing confidence and patient counseling effectiveness.

Patients experience significant benefits including improved medication access, enhanced therapeutic options, and better clinical outcomes through advanced oral antidiabetic formulations. Insurance coverage expansion reduces financial barriers, enabling patients to access newer, more effective medications previously considered unaffordable.

Healthcare systems benefit from improved diabetes management outcomes, reduced long-term complications, and optimized resource utilization through effective oral therapeutic interventions. Economic benefits include reduced hospitalization rates, decreased emergency department visits, and improved productivity among diabetic patients achieving better glycemic control.

Regulatory authorities benefit from enhanced pharmaceutical industry collaboration, improved drug safety monitoring, and strengthened healthcare infrastructure supporting national diabetes management objectives. Research institutions gain opportunities for clinical collaboration, technology transfer, and academic advancement through partnerships with pharmaceutical companies developing innovative oral antidiabetic medications.

Strengths:

Weaknesses:

Opportunities:

Threats:

Key trends shaping Thailand’s oral antidiabetic drug market include personalized medicine adoption, digital health integration, and combination therapy preferences. Personalized medicine approaches gain momentum as healthcare providers increasingly consider genetic factors, comorbidities, and individual patient characteristics when selecting optimal therapeutic regimens.

Digital health integration transforms medication management through smartphone applications, continuous glucose monitoring systems, and telemedicine platforms supporting remote patient care. Healthcare providers report improved patient engagement rates of approximately 40% when utilizing digital health tools for diabetes management support.

Combination therapy trends show increasing preference for fixed-dose combinations offering simplified dosing regimens and improved patient compliance. Clinical evidence supporting combination approaches drives prescribing pattern shifts toward multi-mechanism therapeutic strategies addressing diverse pathophysiological targets simultaneously.

Sustainability trends influence pharmaceutical manufacturing processes, with companies adopting environmentally responsible production methods and packaging solutions. Patient-centric trends emphasize convenience, safety, and affordability, driving product development toward user-friendly formulations and accessible pricing structures.

Regulatory trends focus on expedited approval processes for essential medications, biosimilar development support, and enhanced post-market surveillance systems ensuring patient safety and therapeutic effectiveness. Market access trends emphasize value-based pricing models and outcomes-based reimbursement systems aligning pharmaceutical costs with clinical benefits achieved.

Recent industry developments within Thailand’s oral antidiabetic drug market include regulatory approvals, strategic partnerships, and technological innovations advancing diabetes care capabilities. Regulatory authorities have streamlined approval processes for generic medications, reducing market entry timelines and increasing competition benefiting patients through improved affordability.

Strategic partnerships between international pharmaceutical companies and local manufacturers have accelerated technology transfer, enhanced production capabilities, and expanded market access for innovative therapeutic options. MarkWide Research analysis indicates these collaborations have resulted in improved market penetration rates of approximately 18% for newer therapeutic classes.

Technological innovations include development of extended-release formulations, combination products, and patient-friendly dosing systems improving medication adherence and therapeutic outcomes. Manufacturing investments in advanced production facilities have strengthened Thailand’s position as a regional pharmaceutical hub serving both domestic and export markets.

Clinical research initiatives involving local healthcare institutions and international pharmaceutical companies have generated valuable real-world evidence supporting optimal prescribing practices and patient management strategies. Digital health developments include integration of electronic health records, prescription management systems, and patient monitoring platforms enhancing healthcare delivery efficiency.

Market access improvements through insurance coverage expansion and government healthcare initiatives have increased patient access to essential diabetes medications across diverse socioeconomic populations.

Market analysts recommend strategic approaches for maximizing opportunities within Thailand’s oral antidiabetic drug market while addressing existing challenges and competitive pressures. Product differentiation strategies should focus on developing innovative formulations, combination therapies, and patient-centric solutions addressing unmet clinical needs and improving therapeutic outcomes.

Market expansion recommendations emphasize rural healthcare penetration through innovative distribution models, telemedicine integration, and community health worker programs extending medication access to underserved populations. Partnership strategies should prioritize collaborations with local healthcare providers, academic institutions, and government agencies supporting market development and clinical evidence generation.

Investment priorities should include research and development capabilities, manufacturing infrastructure, and digital health technologies enhancing competitive positioning and market responsiveness. Regulatory engagement recommendations emphasize proactive collaboration with authorities supporting favorable policy development and streamlined approval processes.

Pricing strategies should balance affordability requirements with innovation investment needs, utilizing value-based pricing models demonstrating clinical and economic benefits. Educational initiatives targeting healthcare providers and patients should emphasize evidence-based prescribing practices and optimal medication management approaches.

Quality assurance recommendations include implementation of robust manufacturing standards, supply chain security measures, and post-market surveillance systems ensuring patient safety and market integrity. Sustainability initiatives should address environmental concerns while maintaining cost-effectiveness and therapeutic efficacy standards.

Future outlook for Thailand’s oral antidiabetic drug market indicates sustained growth momentum driven by demographic trends, healthcare infrastructure improvements, and therapeutic innovation. Market projections suggest continued expansion with annual growth rates maintaining 5-7% CAGR over the next decade, supported by increasing diabetes prevalence and improved medication access.

Technological advancement will reshape market dynamics through personalized medicine approaches, digital health integration, and innovative drug delivery systems enhancing patient outcomes and treatment convenience. Regulatory evolution toward value-based healthcare models will influence pricing mechanisms and market access strategies, emphasizing clinical effectiveness and economic efficiency.

Competitive landscape evolution will feature increased collaboration between multinational corporations and local manufacturers, fostering innovation while maintaining market accessibility. Patient demographics show aging population trends creating sustained demand for diabetes medications, with MWR projections indicating patient population growth of approximately 8% annually over the next five years.

Healthcare system development will support market expansion through improved infrastructure, enhanced provider education, and integrated care models optimizing diabetes management outcomes. Export opportunities will leverage Thailand’s manufacturing capabilities and regulatory expertise, positioning the country as a regional pharmaceutical hub serving Southeast Asian markets.

Innovation focus will emphasize combination therapies, extended-release formulations, and personalized treatment approaches addressing diverse patient needs and clinical scenarios. Market maturation will drive consolidation among smaller players while creating opportunities for specialized niche products and premium therapeutic segments.

The Thailand oral antidiabetic drug market represents a dynamic and rapidly evolving healthcare sector characterized by robust growth potential, diverse therapeutic options, and increasing patient accessibility. Market fundamentals remain strong, supported by rising diabetes prevalence, supportive government policies, and continuous pharmaceutical innovation addressing unmet clinical needs.

Strategic opportunities abound for industry participants willing to invest in research and development, market expansion initiatives, and patient-centric solutions. Competitive advantages will increasingly depend on product differentiation, clinical evidence generation, and comprehensive patient support programs enhancing therapeutic outcomes and medication adherence.

Healthcare system integration will continue driving market development through improved infrastructure, enhanced provider education, and digital health adoption supporting optimal diabetes management. Regulatory environment evolution toward value-based healthcare models will create opportunities for innovative companies demonstrating superior clinical and economic outcomes.

Future success in Thailand’s oral antidiabetic drug market will require balanced approaches addressing affordability, accessibility, and innovation while maintaining high quality standards and patient safety priorities. Market participants who effectively navigate these complex dynamics while delivering meaningful value to patients and healthcare systems will achieve sustainable competitive advantages and long-term growth in this essential therapeutic market.

What is Oral Antidiabetic Drug?

Oral antidiabetic drugs are medications used to manage blood sugar levels in individuals with diabetes. They work by various mechanisms, including increasing insulin sensitivity, stimulating insulin secretion, or reducing glucose production in the liver.

What are the key players in the Thailand Oral Antidiabetic Drug Market?

Key players in the Thailand Oral Antidiabetic Drug Market include companies like Sanofi, Novo Nordisk, and Merck, which offer a range of antidiabetic medications. These companies focus on developing innovative treatments to improve diabetes management, among others.

What are the growth factors driving the Thailand Oral Antidiabetic Drug Market?

The growth of the Thailand Oral Antidiabetic Drug Market is driven by increasing diabetes prevalence, rising awareness about diabetes management, and advancements in drug formulations. Additionally, the growing aging population contributes to the demand for effective antidiabetic therapies.

What challenges does the Thailand Oral Antidiabetic Drug Market face?

The Thailand Oral Antidiabetic Drug Market faces challenges such as high treatment costs, potential side effects of medications, and competition from alternative therapies. Furthermore, regulatory hurdles can impact the speed of new drug approvals.

What opportunities exist in the Thailand Oral Antidiabetic Drug Market?

Opportunities in the Thailand Oral Antidiabetic Drug Market include the development of new drug classes, personalized medicine approaches, and increasing investment in diabetes research. There is also potential for expanding access to medications in rural areas.

What trends are shaping the Thailand Oral Antidiabetic Drug Market?

Trends in the Thailand Oral Antidiabetic Drug Market include the rise of combination therapies, the use of digital health technologies for diabetes management, and a focus on patient-centered care. These trends aim to enhance treatment outcomes and improve patient adherence.

Thailand Oral Antidiabetic Drug Market

| Segmentation Details | Description |

|---|---|

| Product Type | Metformin, Sulfonylureas, DPP-4 Inhibitors, SGLT2 Inhibitors |

| Delivery Mode | Oral Tablets, Oral Liquids, Extended-Release Tablets, Combination Therapy |

| End User | Hospitals, Clinics, Homecare, Pharmacies |

| Therapy Area | Type 1 Diabetes, Type 2 Diabetes, Gestational Diabetes, Prediabetes |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Thailand Oral Antidiabetic Drug Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.