444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Thailand data center processor market represents a rapidly expanding segment within the country’s digital infrastructure landscape, driven by increasing cloud adoption, digital transformation initiatives, and growing demand for high-performance computing solutions. Thailand’s strategic position as a digital hub in Southeast Asia has accelerated investments in data center infrastructure, creating substantial opportunities for processor manufacturers and technology providers.

Market dynamics indicate robust growth potential, with the sector experiencing significant expansion at a compound annual growth rate (CAGR) of 8.2% over the forecast period. This growth trajectory reflects Thailand’s commitment to becoming a regional digital economy leader, supported by government initiatives promoting digital infrastructure development and foreign investment in technology sectors.

Key market drivers include the proliferation of Internet of Things (IoT) applications, artificial intelligence workloads, and edge computing requirements. The increasing adoption of hybrid cloud architectures by Thai enterprises has created demand for diverse processor solutions, ranging from traditional x86 architectures to specialized AI accelerators and energy-efficient ARM-based processors.

Regional positioning shows Thailand capturing approximately 12% market share within the Southeast Asian data center processor landscape, positioning the country as a significant growth market for international processor manufacturers and local system integrators seeking to expand their presence in the region.

The Thailand data center processor market refers to the comprehensive ecosystem of central processing units, graphics processing units, and specialized computing chips deployed within data center facilities across Thailand to support various computational workloads, cloud services, and digital applications.

This market encompasses multiple processor categories including traditional server CPUs, GPU accelerators for AI and machine learning workloads, field-programmable gate arrays (FPGAs) for specialized applications, and emerging processor architectures designed for edge computing and energy-efficient operations. The market serves diverse end-users ranging from hyperscale cloud providers to enterprise data centers and colocation facilities.

Technological scope includes both established processor technologies and emerging solutions such as quantum processing units, neuromorphic chips, and application-specific integrated circuits (ASICs) designed for cryptocurrency mining and blockchain applications. The market also encompasses supporting technologies including cooling solutions, power management systems, and interconnect technologies that enable optimal processor performance.

Thailand’s data center processor market demonstrates exceptional growth momentum, driven by accelerating digital transformation across industries and increasing adoption of cloud-native technologies. The market benefits from Thailand’s strategic geographic location, favorable government policies, and growing foreign direct investment in digital infrastructure projects.

Key growth catalysts include the expansion of hyperscale data centers by major cloud service providers, increasing demand for AI and machine learning capabilities, and the proliferation of edge computing applications. The market shows particular strength in enterprise segments, where 65% of organizations are actively upgrading their data center infrastructure to support modern workloads.

Competitive landscape features a mix of international processor manufacturers and local system integrators, with increasing focus on energy-efficient solutions and specialized processors for emerging applications. The market demonstrates resilience and adaptability, with vendors successfully navigating supply chain challenges while maintaining growth trajectories.

Future prospects remain highly positive, supported by continued government investment in digital infrastructure, growing adoption of 5G technologies, and increasing demand for edge computing solutions across various industry verticals including manufacturing, healthcare, and financial services.

Strategic market analysis reveals several critical insights shaping the Thailand data center processor landscape:

Market maturation indicators suggest Thailand is transitioning from a primarily cost-focused market to one emphasizing performance, efficiency, and specialized capabilities, creating opportunities for premium processor solutions and value-added services.

Digital transformation initiatives across Thai enterprises serve as the primary catalyst for data center processor market expansion. Organizations are modernizing their IT infrastructure to support cloud-native applications, artificial intelligence workloads, and real-time analytics, driving demand for high-performance computing solutions.

Government digitalization programs including the Thailand 4.0 initiative and Digital Economy Promotion Agency (DEPA) projects have accelerated public sector adoption of advanced data center technologies. These initiatives create substantial demand for processors capable of handling large-scale data processing and analytics workloads.

Cloud service provider expansion represents another significant driver, with major international and regional cloud providers establishing data center presence in Thailand. This expansion requires substantial processor investments to support diverse customer workloads and maintain competitive service levels.

Artificial intelligence adoption across industries including healthcare, finance, and manufacturing drives demand for specialized processors such as GPUs and AI accelerators. The growing implementation of machine learning applications requires processors optimized for parallel processing and high-throughput computing.

Edge computing proliferation creates demand for processors designed for distributed computing environments. The deployment of 5G networks and IoT applications requires edge data centers equipped with energy-efficient processors capable of real-time processing.

High capital investment requirements for advanced processor technologies pose significant barriers for smaller organizations and local service providers. The substantial upfront costs associated with next-generation processors and supporting infrastructure can limit market adoption among price-sensitive segments.

Skills shortage in specialized areas such as AI processor optimization, high-performance computing, and advanced cooling technologies constrains market growth. The limited availability of qualified technical personnel affects deployment timelines and operational efficiency.

Supply chain vulnerabilities continue to impact processor availability and pricing, particularly for cutting-edge technologies. Global semiconductor shortages and geopolitical tensions affect procurement strategies and project timelines for data center operators.

Energy infrastructure limitations in certain regions of Thailand constrain the deployment of high-performance processors that require substantial power and cooling resources. Grid stability and power quality concerns affect data center location decisions and processor selection criteria.

Regulatory complexity surrounding data localization, cybersecurity requirements, and foreign investment restrictions creates uncertainty for international processor manufacturers and cloud service providers considering Thailand market entry or expansion.

Emerging technology adoption presents substantial opportunities for processor manufacturers specializing in quantum computing, neuromorphic processing, and advanced AI accelerators. Thailand’s growing research and development ecosystem creates demand for cutting-edge processor technologies.

Sustainability initiatives drive opportunities for energy-efficient processor solutions and green data center technologies. Organizations increasingly prioritize environmental responsibility, creating market demand for processors with superior performance-per-watt ratios.

Industry 4.0 transformation across Thailand’s manufacturing sector generates opportunities for edge computing processors and industrial IoT solutions. The integration of smart manufacturing technologies requires specialized processors for real-time control and analytics applications.

Financial services digitalization creates opportunities for high-security processors and specialized solutions for blockchain, cryptocurrency, and digital payment applications. The growing fintech sector requires processors optimized for cryptographic operations and secure computing.

Healthcare technology advancement presents opportunities for processors supporting medical imaging, genomics research, and telemedicine applications. The expansion of digital health initiatives requires specialized computing capabilities for medical data processing and analysis.

Competitive intensity in the Thailand data center processor market continues to increase as international manufacturers expand their presence and local partners develop specialized capabilities. This competition drives innovation and improves price-performance ratios for end customers.

Technology convergence trends show increasing integration between traditional CPUs, specialized accelerators, and emerging processor architectures. This convergence creates opportunities for comprehensive solutions while challenging vendors to develop broader technical expertise.

Customer requirements evolution demonstrates shift from purely performance-focused procurement to holistic evaluation including energy efficiency, total cost of ownership, and sustainability metrics. This evolution influences processor design priorities and market positioning strategies.

Partnership ecosystem development shows increasing collaboration between processor manufacturers, system integrators, and cloud service providers to deliver integrated solutions. These partnerships enable faster market penetration and improved customer support capabilities.

Market segmentation dynamics reveal growing differentiation between hyperscale, enterprise, and edge computing segments, each with distinct processor requirements and procurement patterns. This segmentation drives specialized product development and targeted marketing strategies.

Comprehensive market analysis employed multiple research methodologies to ensure accurate and reliable insights into the Thailand data center processor market. The research approach combined primary data collection, secondary research, and expert analysis to provide holistic market understanding.

Primary research activities included structured interviews with key market participants including processor manufacturers, system integrators, data center operators, and end-user organizations. These interviews provided insights into market trends, technology preferences, and future requirements.

Secondary research methodology encompassed analysis of industry reports, government publications, company financial statements, and technology specifications. This research provided quantitative data on market size, growth rates, and competitive positioning.

Expert consultation process involved engagement with technology specialists, industry analysts, and academic researchers to validate findings and provide additional market insights. Expert input enhanced the accuracy and depth of market analysis.

Data validation procedures included cross-referencing multiple sources, statistical analysis of quantitative data, and peer review of research findings. These procedures ensured research quality and reliability of market projections.

Bangkok metropolitan region dominates the Thailand data center processor market, accounting for approximately 58% of total market share due to its concentration of data centers, cloud service providers, and enterprise customers. The region benefits from superior telecommunications infrastructure, reliable power supply, and proximity to international connectivity hubs.

Eastern Economic Corridor (EEC) emerges as a significant growth region, capturing 22% market share through government-promoted industrial development and foreign investment initiatives. The EEC’s focus on advanced manufacturing and digital technologies creates substantial demand for edge computing processors and industrial IoT solutions.

Central Thailand region demonstrates steady growth with 12% market share, driven by manufacturing sector digitalization and expanding logistics operations. The region’s strategic location and transportation infrastructure support data center development and processor deployment.

Northern Thailand shows emerging potential with 5% market share, primarily driven by government digitalization initiatives and growing educational technology adoption. The region’s lower operational costs attract data center investments requiring cost-effective processor solutions.

Southern Thailand maintains 3% market share with growth potential in tourism technology, maritime logistics, and cross-border trade applications. The region’s connectivity to Malaysia and Singapore creates opportunities for regional data center services.

Market leadership in the Thailand data center processor segment features a combination of established international manufacturers and emerging regional players, each leveraging distinct competitive advantages and market positioning strategies.

Competitive strategies emphasize technology innovation, local partnership development, and comprehensive solution offerings. Market leaders invest significantly in research and development to maintain technological advantages while building strong relationships with local system integrators and service providers.

By Processor Type:

By Architecture:

By End-User:

CPU Segment Analysis: Traditional central processing units continue to dominate the market with 68% segment share, driven by widespread adoption in enterprise applications and cloud computing workloads. The segment shows steady growth with increasing demand for multi-core processors and advanced security features.

GPU Accelerator Growth: Graphics processing units experience rapid expansion, capturing 18% market share through increasing AI and machine learning adoption. The segment benefits from growing demand for parallel processing capabilities and specialized computing workloads.

Specialized Processor Emergence: FPGA and ASIC solutions gain traction with 8% combined market share, driven by requirements for customizable computing and application-specific optimization. These processors serve niche applications requiring specialized performance characteristics.

DPU Market Development: Data processing units represent an emerging category with 6% market share, focusing on infrastructure acceleration and offloading tasks from main processors. This segment shows strong growth potential as data centers optimize for efficiency and performance.

Architecture Evolution: x86 processors maintain 78% architecture share while ARM-based solutions grow rapidly at 15% share, driven by energy efficiency requirements and cloud-native applications. RISC-V and custom architectures represent emerging opportunities with 7% combined share.

Processor Manufacturers benefit from Thailand’s growing data center market through expanded revenue opportunities, strategic market positioning, and access to emerging technology segments. The market provides platforms for testing new processor architectures and building regional partnerships.

System Integrators gain opportunities to develop specialized expertise, expand service portfolios, and build long-term customer relationships. The market enables integrators to differentiate through technical capabilities and comprehensive solution offerings.

Data Center Operators benefit from improved processor performance, energy efficiency, and cost optimization opportunities. Advanced processors enable operators to enhance service quality while reducing operational expenses and environmental impact.

End-User Organizations gain access to advanced computing capabilities, improved application performance, and enhanced business agility. Modern processors enable organizations to implement digital transformation initiatives and competitive advantages.

Government Entities benefit from enhanced digital infrastructure capabilities, improved public service delivery, and economic development opportunities. Advanced processor technologies support smart city initiatives and digital government programs.

Research Institutions gain access to cutting-edge computing resources for scientific research, academic programs, and innovation development. High-performance processors enable advanced research capabilities and educational opportunities.

Strengths:

Weaknesses:

Opportunities:

Threats:

Energy Efficiency Focus emerges as a dominant trend, with organizations prioritizing processors offering superior performance-per-watt ratios. This trend drives adoption of advanced manufacturing processes, optimized architectures, and intelligent power management technologies.

AI-Optimized Processors gain significant traction as organizations implement machine learning and artificial intelligence applications. Specialized AI accelerators, neuromorphic processors, and quantum computing solutions represent growing market segments.

Edge Computing Integration drives demand for processors designed for distributed computing environments. These processors emphasize low latency, energy efficiency, and real-time processing capabilities for IoT and 5G applications.

Hybrid Cloud Architectures influence processor selection criteria, with organizations requiring flexible solutions supporting both on-premises and cloud workloads. This trend promotes processor standardization and workload portability.

Sustainability Initiatives impact procurement decisions, with organizations evaluating processors based on environmental impact, recyclability, and carbon footprint. Green computing becomes a competitive differentiator for processor manufacturers.

Security Enhancement drives adoption of processors with built-in security features, hardware-based encryption, and trusted execution environments. Cybersecurity concerns influence processor architecture design and market positioning.

Major cloud service providers announce significant data center investments in Thailand, driving substantial processor procurement and market expansion. These investments demonstrate confidence in Thailand’s digital infrastructure potential and create long-term growth opportunities.

Government digitalization initiatives accelerate with increased budget allocations for digital infrastructure projects. The MarkWide Research analysis indicates these initiatives will drive sustained processor demand growth across public sector applications.

International processor manufacturers establish local partnerships and distribution networks to better serve the Thai market. These partnerships enhance technical support capabilities and reduce procurement lead times for customers.

University research programs expand focus on advanced computing technologies, creating talent pipeline and innovation ecosystem. Academic partnerships with processor manufacturers drive technology transfer and market development.

Industry associations form to promote data center development and establish technical standards. These organizations facilitate knowledge sharing and coordinate industry development initiatives.

Sustainability certifications gain importance as organizations implement environmental responsibility programs. Green data center standards influence processor selection and market positioning strategies.

Market entry strategies should emphasize local partnership development and technical support capabilities. MarkWide Research recommends that international processor manufacturers establish strong relationships with system integrators and service providers to accelerate market penetration.

Technology positioning should focus on energy efficiency, performance optimization, and total cost of ownership benefits. Organizations should evaluate processors based on comprehensive value propositions rather than initial purchase price alone.

Skills development initiatives require immediate attention to address technical talent shortages. Industry participants should invest in training programs, certification courses, and academic partnerships to build local expertise.

Supply chain diversification becomes critical for ensuring processor availability and managing cost fluctuations. Organizations should develop multiple supplier relationships and consider regional sourcing strategies.

Sustainability integration should become standard practice in processor evaluation and procurement processes. Environmental considerations will increasingly influence purchasing decisions and vendor selection criteria.

Innovation investment in emerging technologies such as quantum computing, neuromorphic processing, and advanced AI accelerators will create competitive advantages and market differentiation opportunities.

Long-term growth prospects for the Thailand data center processor market remain highly positive, supported by continued digital transformation, government investment, and regional economic development. The market is positioned to benefit from Thailand’s strategic role as a Southeast Asian technology hub.

Technology evolution will drive market transformation with increasing adoption of specialized processors, AI accelerators, and energy-efficient architectures. The market will likely see continued growth at 8.5% CAGR through the forecast period, driven by emerging technology adoption and infrastructure expansion.

Market maturation will bring increased sophistication in processor selection criteria, with organizations emphasizing performance optimization, energy efficiency, and total cost of ownership. This maturation creates opportunities for premium processor solutions and value-added services.

Regional integration will strengthen Thailand’s position as a data center hub serving Southeast Asian markets. Cross-border data flows and regional cloud services will drive processor demand and market expansion.

Innovation ecosystem development will enhance Thailand’s capabilities in processor technologies and related fields. Academic research, industry partnerships, and government support will contribute to technology advancement and market growth.

The Thailand data center processor market presents exceptional growth opportunities driven by digital transformation, government support, and strategic geographic positioning. The market demonstrates strong fundamentals with diverse growth drivers across multiple industry segments and technology categories.

Key success factors for market participants include local partnership development, technical expertise building, and comprehensive solution offerings. Organizations that invest in understanding local market requirements and building strong support capabilities will achieve competitive advantages.

Future market development will be characterized by increasing technology sophistication, sustainability focus, and regional integration. The market’s evolution toward specialized processors and advanced computing capabilities creates opportunities for innovation and differentiation.

Strategic positioning in the Thailand data center processor market requires long-term commitment, continuous technology investment, and adaptive business strategies. Market participants who align with Thailand’s digital development vision and invest in local capabilities will benefit from sustained growth opportunities in this dynamic and expanding market.

What is Data Center Processor?

Data Center Processors are specialized computing units designed to handle the high-performance demands of data centers. They are optimized for tasks such as data processing, storage management, and virtualization, playing a crucial role in cloud computing and enterprise applications.

What are the key players in the Thailand Data Center Processor Market?

Key players in the Thailand Data Center Processor Market include Intel Corporation, AMD, and Huawei Technologies. These companies are known for their innovative processor solutions that cater to the growing demands of data centers, among others.

What are the growth factors driving the Thailand Data Center Processor Market?

The Thailand Data Center Processor Market is driven by the increasing demand for cloud services, the rise of big data analytics, and the need for enhanced processing power in enterprise applications. Additionally, the expansion of digital infrastructure is contributing to market growth.

What challenges does the Thailand Data Center Processor Market face?

Challenges in the Thailand Data Center Processor Market include the high costs associated with advanced processor technologies and the rapid pace of technological change. Additionally, competition from alternative computing solutions can impact market dynamics.

What opportunities exist in the Thailand Data Center Processor Market?

Opportunities in the Thailand Data Center Processor Market include the growing adoption of artificial intelligence and machine learning applications, which require powerful processing capabilities. Furthermore, the shift towards edge computing presents new avenues for processor development.

What trends are shaping the Thailand Data Center Processor Market?

Trends in the Thailand Data Center Processor Market include the increasing integration of AI capabilities into processors and the development of energy-efficient computing solutions. Additionally, the rise of hybrid cloud environments is influencing processor design and functionality.

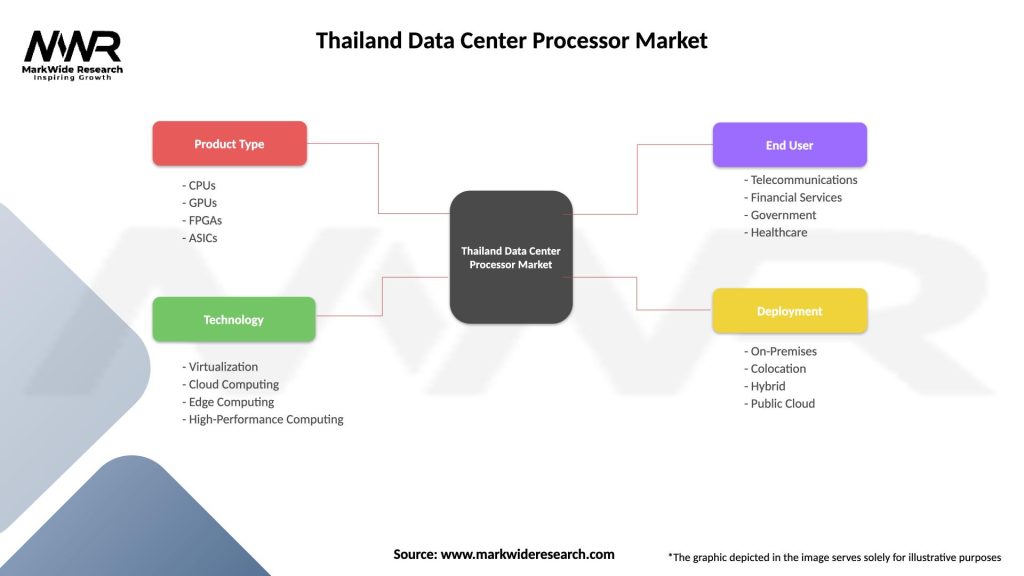

Thailand Data Center Processor Market

| Segmentation Details | Description |

|---|---|

| Product Type | CPUs, GPUs, FPGAs, ASICs |

| Technology | Virtualization, Cloud Computing, Edge Computing, High-Performance Computing |

| End User | Telecommunications, Financial Services, Government, Healthcare |

| Deployment | On-Premises, Colocation, Hybrid, Public Cloud |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Thailand Data Center Processor Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.