444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Thailand data center market represents a rapidly expanding sector within Southeast Asia’s digital infrastructure landscape, driven by increasing digitalization, cloud adoption, and growing demand for data storage solutions. Thailand’s strategic position as a regional hub for digital services has positioned the country as a critical player in the Asia-Pacific data center ecosystem. The market encompasses various facility types, from hyperscale data centers to edge computing facilities, serving both domestic and international clients across multiple industries.

Digital transformation initiatives across Thai enterprises have accelerated demand for reliable, scalable data center services. The market benefits from government support through the Thailand 4.0 initiative, which emphasizes digital economy development and smart city implementations. Major international cloud service providers and colocation operators have established significant presence in Thailand, recognizing the country’s potential as a gateway to the broader Southeast Asian market.

Growth projections indicate the Thailand data center market is experiencing robust expansion, with analysts forecasting a compound annual growth rate of 8.2% over the next five years. This growth trajectory reflects increasing enterprise cloud adoption, rising internet penetration rates, and expanding e-commerce activities throughout the region.

The Thailand data center market refers to the comprehensive ecosystem of facilities, services, and infrastructure designed to house, manage, and distribute digital data and computing resources within Thailand’s borders. This market encompasses colocation services, managed hosting solutions, cloud infrastructure, and edge computing facilities that support the country’s growing digital economy and serve as a regional hub for Southeast Asian operations.

Data centers in Thailand provide critical infrastructure for businesses ranging from local enterprises to multinational corporations, offering services including server hosting, data storage, disaster recovery, and cloud computing solutions. The market includes various deployment models such as enterprise data centers, colocation facilities, hyperscale cloud data centers, and emerging edge computing nodes that support low-latency applications and IoT implementations.

Thailand’s data center market has emerged as one of Southeast Asia’s most dynamic digital infrastructure sectors, characterized by strong government support, strategic geographic positioning, and increasing enterprise digitalization. The market demonstrates exceptional growth potential, supported by Thailand’s role as a regional business hub and gateway to emerging Southeast Asian economies.

Key market drivers include accelerating cloud adoption rates, with enterprise cloud utilization growing by 35% annually, expanding e-commerce activities, and increasing demand for data sovereignty solutions. The market benefits from substantial foreign investment, with international data center operators establishing major facilities to serve both local and regional markets.

Infrastructure development has focused on building world-class facilities that meet international standards for reliability, security, and energy efficiency. The market shows strong diversification across multiple segments, including colocation services, managed hosting, cloud infrastructure, and emerging edge computing solutions that support Thailand’s smart city initiatives and Industry 4.0 implementations.

Strategic market insights reveal several critical factors driving Thailand’s data center market expansion and positioning within the regional digital infrastructure landscape:

Digital transformation acceleration across Thai enterprises represents the primary driver of data center market growth, with organizations increasingly migrating to cloud-based infrastructure and digital service delivery models. The Thailand 4.0 economic strategy has created substantial momentum for digital infrastructure investment, encouraging both domestic and international companies to establish data center operations within the country.

Cloud adoption rates continue to surge, with small and medium enterprises showing particularly strong growth in cloud service utilization. This trend has created increased demand for colocation services and managed hosting solutions that enable businesses to access enterprise-grade infrastructure without significant capital investment. The growing popularity of hybrid cloud deployments has further expanded market opportunities for data center operators.

E-commerce expansion throughout Thailand and the broader Southeast Asian region has generated substantial data center demand, as online retailers require robust infrastructure to support transaction processing, inventory management, and customer data analytics. The rise of digital payment systems and fintech services has created additional requirements for secure, compliant data center facilities.

Government digitalization initiatives including smart city projects, digital government services, and e-governance implementations have created significant public sector demand for data center services. These initiatives require reliable, secure infrastructure capable of supporting citizen services and government operations at scale.

High capital requirements for data center development represent a significant barrier to market entry, particularly for smaller operators seeking to compete with established international providers. The substantial investment needed for land acquisition, facility construction, and equipment procurement can limit market participation and consolidation opportunities.

Skilled workforce shortage poses ongoing challenges for data center operators, as the specialized technical expertise required for facility management, cybersecurity, and cloud operations remains in limited supply. This talent gap can impact operational efficiency and service quality, potentially constraining market growth rates.

Regulatory complexity surrounding data protection, cross-border data transfers, and foreign investment in critical infrastructure creates uncertainty for international operators. Evolving compliance requirements and data sovereignty regulations may impact operational flexibility and investment decisions.

Energy costs and availability concerns affect data center economics, particularly for energy-intensive hyperscale facilities. While Thailand’s electricity infrastructure is generally reliable, rising energy costs and environmental sustainability requirements create operational challenges that must be carefully managed.

Edge computing deployment presents substantial growth opportunities as Thailand advances smart city initiatives and IoT implementations across various sectors. The need for low-latency computing solutions to support autonomous vehicles, industrial automation, and real-time analytics creates demand for distributed data center infrastructure throughout urban and industrial areas.

Regional expansion potential offers significant opportunities for Thailand-based data center operators to serve neighboring markets in Cambodia, Laos, Myanmar, and Vietnam. Thailand’s superior infrastructure and connectivity position it as an ideal hub for cross-border digital services and regional cloud deployments.

Sustainability initiatives create opportunities for operators to differentiate through renewable energy adoption, energy-efficient cooling systems, and green building certifications. Growing corporate focus on environmental responsibility drives demand for sustainable data center solutions that align with ESG objectives.

Industry-specific solutions present opportunities for specialized data center services targeting healthcare, financial services, manufacturing, and government sectors. Each industry has unique compliance, security, and performance requirements that create demand for tailored infrastructure solutions and managed services.

Competitive dynamics in Thailand’s data center market reflect a healthy balance between established international operators and emerging local providers, creating diverse service offerings and competitive pricing structures. Market consolidation trends show increasing collaboration between global cloud providers and local colocation operators to deliver comprehensive solutions.

Technology evolution continues to reshape market dynamics, with artificial intelligence, machine learning, and advanced analytics driving demand for high-performance computing infrastructure. The integration of 5G networks is creating new requirements for edge computing facilities and ultra-low latency services that support next-generation applications.

Customer behavior patterns show increasing preference for hybrid and multi-cloud deployments, requiring data center operators to provide flexible, interoperable infrastructure solutions. Service level expectations continue to rise, with customers demanding 99.99% uptime guarantees and comprehensive security measures.

Investment flows into Thailand’s data center market remain strong, with both domestic and international capital supporting facility expansion and technology upgrades. MarkWide Research analysis indicates sustained investor confidence in Thailand’s long-term digital infrastructure potential and regional market position.

Comprehensive market analysis for Thailand’s data center sector employs multiple research methodologies to ensure accurate, reliable insights into market trends, competitive dynamics, and growth projections. The research approach combines quantitative data analysis with qualitative industry expertise to provide holistic market understanding.

Primary research activities include extensive interviews with data center operators, cloud service providers, enterprise customers, and government officials involved in digital infrastructure planning. These discussions provide firsthand insights into market challenges, opportunities, and strategic priorities that shape industry development.

Secondary research analysis incorporates government statistics, industry reports, financial disclosures, and regulatory filings to establish comprehensive market baselines and validate primary research findings. This approach ensures data accuracy and provides historical context for market trend analysis.

Market modeling techniques utilize advanced analytical frameworks to project future market scenarios, assess competitive positioning, and evaluate the impact of various market drivers and restraints on industry growth trajectories.

Bangkok metropolitan area dominates Thailand’s data center market, accounting for approximately 75% of total market capacity due to its concentration of businesses, government agencies, and international connectivity infrastructure. The capital region offers optimal access to submarine cables, fiber optic networks, and skilled technical workforce, making it the preferred location for major data center investments.

Eastern Economic Corridor (EEC) represents an emerging growth region for data center development, supported by government investment in digital infrastructure and industrial development. The EEC’s focus on advanced manufacturing and technology creates demand for specialized data center services supporting Industry 4.0 applications and smart factory implementations.

Chiang Mai and northern regions show increasing data center activity, particularly for disaster recovery and backup operations that benefit from geographic separation from Bangkok facilities. The region’s cooler climate conditions provide natural cooling advantages that reduce operational costs for data center operators.

Southern Thailand regions including Phuket and Hat Yai are experiencing growing data center demand driven by tourism industry digitalization and cross-border connectivity to Malaysia and Singapore. These areas offer strategic positioning for regional service delivery and backup operations.

Market leadership in Thailand’s data center sector reflects a diverse ecosystem of international hyperscale operators, regional colocation providers, and specialized service companies that collectively serve the country’s growing digital infrastructure needs.

By Service Type: The Thailand data center market segments into distinct service categories, each addressing specific customer requirements and use cases across various industries and applications.

By Deployment Model: Market segmentation reflects diverse infrastructure approaches tailored to different organizational requirements and technical specifications.

Colocation services represent the largest market segment, driven by enterprise demand for flexible, cost-effective infrastructure solutions that provide access to carrier-neutral connectivity and professional facility management. This segment shows particular strength among small and medium enterprises seeking to avoid capital expenditure while accessing enterprise-grade infrastructure.

Managed hosting solutions demonstrate strong growth as organizations seek to outsource complex infrastructure management while maintaining control over their applications and data. The segment benefits from increasing demand for 24/7 technical support and proactive monitoring services that ensure optimal system performance.

Cloud infrastructure services show the highest growth rates, with public cloud adoption increasing by 42% annually among Thai enterprises. This segment encompasses Infrastructure-as-a-Service offerings that provide scalable computing resources without requiring physical infrastructure investment.

Edge computing facilities represent the fastest-emerging segment, driven by IoT implementations, smart city projects, and applications requiring ultra-low latency performance. This category shows particular promise for supporting autonomous vehicle systems and industrial automation applications.

Enterprise customers benefit from access to world-class infrastructure without significant capital investment, enabling focus on core business activities while ensuring reliable, secure data management. Cost optimization opportunities through shared infrastructure and professional management services provide substantial operational advantages.

Data center operators benefit from Thailand’s strategic regional position, government support for digital infrastructure development, and growing enterprise demand for cloud services. The market offers attractive return potential supported by stable regulatory environment and increasing digitalization trends.

Technology vendors gain access to expanding market opportunities as data center operators invest in advanced cooling systems, security solutions, and automation technologies. The focus on energy efficiency and sustainability creates demand for innovative infrastructure solutions.

Government stakeholders benefit from enhanced digital infrastructure that supports economic development, attracts foreign investment, and enables delivery of digital government services. Job creation opportunities in high-skill technical roles contribute to workforce development objectives.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability initiatives are reshaping Thailand’s data center market, with operators increasingly adopting renewable energy sources, advanced cooling technologies, and green building certifications. Carbon neutrality commitments from major cloud providers are driving demand for environmentally responsible infrastructure solutions.

Edge computing deployment represents a transformative trend, with data center operators establishing distributed facilities to support IoT applications, autonomous systems, and real-time analytics. This trend is particularly evident in smart city implementations and industrial automation projects throughout Thailand.

Artificial intelligence integration is becoming standard across data center operations, with AI-powered systems optimizing cooling efficiency, predicting maintenance requirements, and enhancing security monitoring. Machine learning algorithms are improving operational efficiency by 15-20% in advanced facilities.

Hybrid cloud adoption continues to accelerate, with enterprises seeking flexible infrastructure solutions that combine public cloud services with private data center resources. This trend drives demand for interconnected data center ecosystems that enable seamless workload mobility.

Major infrastructure investments have characterized recent industry developments, with international operators committing substantial capital to expand Thailand data center capacity. Hyperscale facility construction projects are establishing Thailand as a regional hub for cloud service delivery across Southeast Asia.

Government policy initiatives including the Digital Economy Promotion Act and Thailand 4.0 strategy have created favorable conditions for data center investment and operation. Regulatory clarity regarding data protection and cross-border data transfers has enhanced investor confidence.

Technology partnerships between global cloud providers and local data center operators are expanding service capabilities and market reach. These collaborations enable comprehensive solution delivery that combines international expertise with local market knowledge.

Submarine cable investments have enhanced Thailand’s international connectivity, with new cable systems providing improved bandwidth and redundancy for data center operations. MarkWide Research indicates these infrastructure improvements are attracting additional international data center investments.

Strategic positioning recommendations emphasize the importance of establishing operations in Thailand’s growing data center market while the competitive landscape remains favorable for new entrants. Early market entry can provide significant advantages in securing prime locations and establishing customer relationships.

Investment focus should prioritize sustainability features, advanced automation systems, and edge computing capabilities that align with emerging market trends. Energy efficiency improvements and renewable energy adoption will become increasingly important competitive differentiators.

Partnership strategies with local telecommunications providers, system integrators, and cloud service providers can accelerate market penetration and enhance service delivery capabilities. Collaborative approaches enable access to established customer bases and local market expertise.

Talent development initiatives should address the skilled workforce shortage through training programs, partnerships with educational institutions, and competitive compensation packages. Human capital investment is essential for sustainable operational excellence and market growth.

Long-term growth prospects for Thailand’s data center market remain exceptionally positive, supported by continued digitalization, regional economic development, and government infrastructure investment. Market expansion is expected to accelerate as Thailand strengthens its position as Southeast Asia’s digital hub.

Technology evolution will continue driving market transformation, with quantum computing, advanced AI systems, and next-generation networking creating new infrastructure requirements. Innovation adoption rates in Thailand are projected to increase by 25% over the next three years.

Regional integration opportunities will expand as ASEAN digital economy initiatives progress, creating demand for cross-border data center services and regional cloud deployments. Thailand’s central location positions it to capture significant benefits from regional digital integration.

MWR projections indicate sustained market growth driven by enterprise cloud adoption, edge computing deployment, and increasing data sovereignty requirements. The market is expected to maintain its strong growth trajectory while evolving to meet changing customer needs and technological requirements.

Thailand’s data center market represents one of Southeast Asia’s most compelling digital infrastructure opportunities, characterized by strong fundamentals, government support, and strategic regional positioning. The market benefits from robust demand drivers including enterprise digitalization, cloud adoption, and Thailand’s emergence as a regional business hub.

Market dynamics favor continued expansion, with diverse growth opportunities spanning traditional colocation services, managed hosting solutions, hyperscale cloud infrastructure, and emerging edge computing applications. The competitive landscape remains healthy, with room for both established operators and innovative new entrants to succeed.

Strategic advantages including geographic location, infrastructure quality, and supportive regulatory environment position Thailand as an attractive destination for data center investment and operations. The market’s evolution toward sustainability, automation, and advanced technologies creates opportunities for operators to differentiate and capture premium value.

Future success in Thailand’s data center market will depend on operators’ ability to adapt to changing customer requirements, embrace technological innovation, and contribute to the country’s digital transformation objectives. The market outlook remains highly positive, with sustained growth expected across all major segments and service categories.

What is a Data Center?

A data center is a facility used to house computer systems and associated components, such as telecommunications and storage systems. It plays a crucial role in managing and storing data for various applications, including cloud computing, big data analytics, and enterprise IT operations.

What are the key players in the Thailand Data Center Market?

Key players in the Thailand Data Center Market include companies like Digital Realty, STT GDC, and True Internet Data Center. These companies provide a range of services, including colocation, cloud services, and managed hosting, among others.

What are the growth factors driving the Thailand Data Center Market?

The growth of the Thailand Data Center Market is driven by increasing demand for cloud services, the rise of e-commerce, and the need for data storage solutions. Additionally, the government’s push for digital transformation and smart city initiatives further fuels market expansion.

What challenges does the Thailand Data Center Market face?

The Thailand Data Center Market faces challenges such as high energy consumption, regulatory compliance issues, and the need for skilled labor. Additionally, competition from neighboring countries with more established data center infrastructures poses a challenge.

What opportunities exist in the Thailand Data Center Market?

Opportunities in the Thailand Data Center Market include the growing adoption of artificial intelligence and machine learning, which require robust data processing capabilities. Furthermore, the increasing focus on sustainability and green data centers presents avenues for innovation and investment.

What trends are shaping the Thailand Data Center Market?

Trends shaping the Thailand Data Center Market include the rise of edge computing, which brings data processing closer to the source of data generation, and the increasing use of hybrid cloud solutions. Additionally, advancements in cooling technologies and energy efficiency are becoming more prominent.

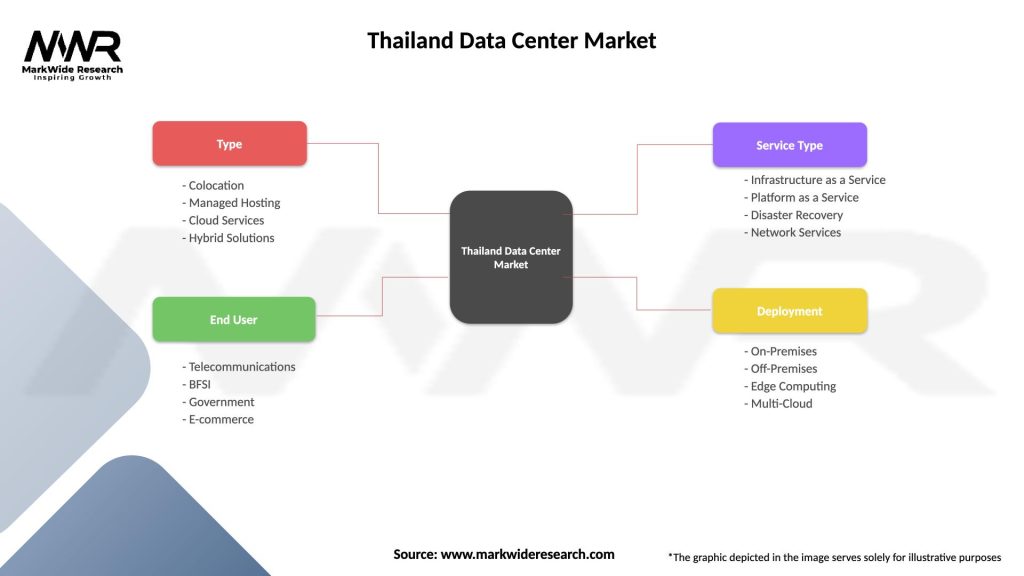

Thailand Data Center Market

| Segmentation Details | Description |

|---|---|

| Type | Colocation, Managed Hosting, Cloud Services, Hybrid Solutions |

| End User | Telecommunications, BFSI, Government, E-commerce |

| Service Type | Infrastructure as a Service, Platform as a Service, Disaster Recovery, Network Services |

| Deployment | On-Premises, Off-Premises, Edge Computing, Multi-Cloud |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Thailand Data Center Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.