444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Thailand data center construction market represents a rapidly expanding sector within Southeast Asia’s digital infrastructure landscape. Thailand’s strategic position as a regional technology hub has attracted significant investment in data center facilities, driven by increasing digitalization across industries and growing cloud adoption. The market encompasses construction of hyperscale facilities, colocation centers, and enterprise data centers designed to support the country’s digital transformation initiatives.

Market growth is accelerated by Thailand’s robust telecommunications infrastructure, favorable government policies, and strategic location connecting major Asian markets. The construction sector focuses on building energy-efficient, scalable facilities that meet international standards while addressing local climate challenges. Investment patterns show increasing preference for sustainable construction practices and advanced cooling technologies optimized for Thailand’s tropical environment.

Regional dynamics indicate Thailand’s emergence as a preferred destination for multinational corporations establishing Southeast Asian data center operations. The market benefits from competitive land costs, reliable power infrastructure, and skilled construction workforce. Growth projections suggest the market will expand at a compound annual growth rate of 12.5% through the forecast period, reflecting strong demand from cloud service providers and enterprise customers.

The Thailand data center construction market refers to the comprehensive sector encompassing planning, design, and construction of specialized facilities housing computer systems, networking equipment, and supporting infrastructure within Thailand’s borders. These facilities serve as critical backbone infrastructure for digital services, cloud computing, and data storage operations across various industries.

Construction activities include development of purpose-built structures featuring advanced power systems, cooling infrastructure, security measures, and connectivity solutions. The market covers both new construction projects and major renovation or expansion of existing facilities to meet evolving technological requirements and capacity demands.

Scope encompasses various facility types from small enterprise data centers to large hyperscale facilities, each requiring specialized construction approaches, materials, and technologies adapted to Thailand’s unique environmental and regulatory conditions.

Thailand’s data center construction market demonstrates exceptional growth momentum driven by accelerating digital transformation across Southeast Asia. The market benefits from Thailand’s strategic geographic position, stable political environment, and comprehensive digital infrastructure development programs. Construction demand is primarily fueled by international cloud service providers, telecommunications companies, and enterprises seeking regional data center presence.

Key market characteristics include increasing focus on sustainable construction practices, adoption of modular construction techniques, and integration of advanced cooling technologies. The market shows strong preference for facilities designed with Power Usage Effectiveness (PUE) ratios below 1.4, reflecting industry commitment to energy efficiency. Investment trends indicate growing interest in edge computing facilities and hybrid cloud infrastructure supporting Thailand’s smart city initiatives.

Competitive landscape features both international construction firms and local contractors specializing in data center projects. Market growth is supported by favorable government policies, including the Thailand 4.0 economic model and Eastern Economic Corridor development program, which prioritize digital infrastructure expansion.

Strategic insights reveal several critical factors shaping Thailand’s data center construction market dynamics:

Digital transformation acceleration serves as the primary catalyst driving Thailand’s data center construction market expansion. Organizations across industries are migrating operations to cloud platforms, creating substantial demand for locally-hosted data center facilities. E-commerce growth and digital payment adoption further amplify requirements for robust data infrastructure supporting transaction processing and customer data management.

Government digitalization initiatives including smart city projects, digital government services, and Industry 4.0 programs generate significant data center capacity requirements. The Eastern Economic Corridor development specifically targets digital infrastructure as a key economic driver, attracting international investment in data center construction projects.

Cloud service expansion by major international providers necessitates local data center presence to serve Thai and regional markets effectively. Data sovereignty regulations and latency requirements drive demand for in-country data storage and processing capabilities. 5G network deployment creates additional infrastructure requirements supporting edge computing applications and low-latency services.

Foreign investment flows into Thailand’s technology sector bring associated data center construction requirements. Multinational corporations establishing regional headquarters or manufacturing operations require dedicated data infrastructure supporting their operations across Southeast Asia.

High capital requirements for data center construction projects present significant barriers for smaller market participants. Construction costs have increased due to specialized equipment requirements, advanced cooling systems, and stringent security specifications. Land availability in prime locations near major cities and connectivity hubs creates supply constraints affecting project development timelines.

Regulatory complexity surrounding foreign ownership restrictions and investment approval processes can delay project implementation. Environmental regulations require comprehensive impact assessments and mitigation measures, adding complexity to construction planning and execution phases.

Skilled labor shortages in specialized data center construction trades limit project execution capacity. Supply chain dependencies on imported specialized equipment and materials create potential delays and cost fluctuations affecting project economics.

Climate challenges including monsoon seasons, high humidity, and temperature extremes require specialized construction approaches and materials, increasing project complexity and costs. Power grid limitations in certain regions may constrain large-scale data center development opportunities.

Edge computing expansion presents substantial opportunities for distributed data center construction across Thailand’s urban centers. 5G network rollout creates demand for edge facilities supporting ultra-low latency applications in autonomous vehicles, industrial IoT, and augmented reality services.

Sustainable construction practices offer differentiation opportunities for contractors specializing in green building techniques and renewable energy integration. LEED certification and other sustainability standards are becoming increasingly important for attracting environmentally-conscious tenants and investors.

Modular construction technologies enable faster project delivery and reduced construction costs, creating competitive advantages for early adopters. Prefabricated components manufactured locally can reduce import dependencies while supporting domestic manufacturing capabilities.

Regional expansion opportunities exist as Thailand serves as a construction base for data center projects across Southeast Asia. Cross-border connectivity initiatives and regional digital integration programs create additional market opportunities for Thai-based construction companies.

Retrofit and modernization of existing facilities present ongoing opportunities as older data centers require upgrades to meet current efficiency and capacity standards. Hybrid cloud infrastructure development creates demand for specialized construction approaches supporting both public and private cloud deployments.

Supply and demand dynamics in Thailand’s data center construction market reflect strong underlying growth fundamentals balanced against capacity constraints. Demand drivers include accelerating digital adoption, cloud migration trends, and regulatory requirements for local data storage. Construction capacity is expanding through workforce development programs and international contractor participation.

Pricing dynamics show upward pressure due to specialized material requirements and skilled labor premiums. Competition intensity varies by project scale, with hyperscale facilities attracting international contractors while smaller projects remain dominated by local firms. Technology integration requirements are driving construction methodology evolution toward more sophisticated project management and execution approaches.

Market maturation is evident in increasing standardization of construction practices and growing emphasis on operational efficiency optimization. Customer sophistication has increased significantly, with clients demanding detailed performance guarantees and sustainability commitments from construction partners.

Innovation adoption in construction techniques, materials, and project management systems continues accelerating, driven by competitive pressures and client requirements. Partnership strategies between international and local firms are becoming more common to combine global expertise with local market knowledge.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into Thailand’s data center construction market. Primary research includes extensive interviews with construction companies, data center operators, real estate developers, and government officials involved in digital infrastructure planning.

Secondary research encompasses analysis of government publications, industry reports, construction permits data, and investment announcements. Market sizing utilizes bottom-up analysis of individual projects combined with top-down validation through industry capacity assessments and growth projections.

Data validation processes include cross-referencing multiple sources, expert interviews, and statistical analysis to ensure accuracy and consistency. MarkWide Research employs proprietary analytical frameworks specifically designed for infrastructure market analysis, incorporating both quantitative metrics and qualitative insights.

Forecasting methodology combines historical trend analysis with forward-looking indicators including planned investments, regulatory changes, and technology adoption patterns. Regional analysis considers local market conditions, competitive dynamics, and infrastructure development plans across different provinces and economic zones.

Bangkok Metropolitan Region dominates Thailand’s data center construction market, accounting for approximately 65% of total construction activity. The region benefits from superior connectivity infrastructure, proximity to international submarine cables, and concentration of major enterprises. Construction projects in Bangkok focus on hyperscale facilities and premium colocation centers serving multinational clients.

Eastern Economic Corridor represents the fastest-growing regional market, with construction activity increasing by 45% annually as government investment programs attract international data center operators. Chonburi and Rayong provinces are emerging as preferred locations for large-scale facilities due to available land, industrial infrastructure, and government incentives.

Northern regions including Chiang Mai are experiencing growing construction activity driven by edge computing requirements and distributed cloud infrastructure development. Southern provinces benefit from submarine cable landing points and tourism-related digital infrastructure requirements.

Regional connectivity improvements through high-speed rail and fiber optic networks are expanding viable construction locations beyond traditional metropolitan areas. Provincial governments are increasingly offering incentives and streamlined approval processes to attract data center construction projects.

Market leadership is distributed among several categories of construction companies, each bringing distinct capabilities and market positioning:

Competitive differentiation focuses on construction speed, energy efficiency achievements, and sustainability certifications. Market consolidation trends show increasing collaboration between international firms and local contractors to combine global expertise with local market knowledge and relationships.

By Facility Type:

By Construction Type:

By End User:

Hyperscale construction represents the highest-value segment, with individual projects often exceeding substantial investment thresholds. These facilities require specialized construction approaches including modular design, advanced cooling systems, and high-density power distribution. Construction timelines typically range from 18-24 months, with phased delivery approaches enabling faster time-to-market.

Colocation facility construction emphasizes flexibility and scalability, with designs accommodating diverse tenant requirements. Multi-tenant considerations require sophisticated security systems, separate utility metering, and flexible space configurations. Construction standards focus on achieving high uptime guarantees and operational efficiency.

Enterprise data center construction allows for more customized approaches tailored to specific organizational requirements. Security considerations often drive design decisions, with enhanced physical security measures and specialized access control systems. Integration requirements with existing corporate infrastructure influence construction planning and execution.

Edge computing facility construction represents the fastest-growing segment, with construction activity increasing 60% annually. These smaller facilities require standardized, cost-effective construction approaches while maintaining high reliability standards. Distributed deployment strategies create opportunities for local contractors and specialized edge facility designs.

Construction companies benefit from stable, long-term project pipelines with premium pricing for specialized data center expertise. Skill development in data center construction creates competitive advantages and opportunities for regional expansion. Technology partnerships with equipment vendors and system integrators enhance service offerings and market positioning.

Real estate developers gain access to high-value, long-term tenants with stable rental income streams. Land utilization optimization through data center development often generates superior returns compared to traditional commercial real estate. Infrastructure investments in power and connectivity enhance overall property values and development potential.

Government stakeholders benefit from increased foreign investment, job creation, and enhanced digital infrastructure supporting economic development goals. Tax revenue from data center construction and operations provides sustainable funding for public services and infrastructure improvements.

Technology companies gain access to world-class data center facilities supporting their digital transformation initiatives and regional expansion strategies. Cost optimization through local data center presence reduces operational expenses and improves service delivery performance.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainable construction practices are becoming standard requirements rather than optional features, with clients demanding LEED certification and carbon-neutral construction approaches. Green building materials and renewable energy integration are increasingly specified in project requirements, driving innovation in construction methodologies and supplier partnerships.

Modular construction adoption is accelerating, with prefabricated components accounting for 35% of construction elements in new projects. Factory-built modules reduce on-site construction time while improving quality control and cost predictability. Standardization efforts across the industry are enabling greater efficiency and reduced customization costs.

Artificial intelligence integration in construction planning and project management is improving efficiency and reducing errors. Building Information Modeling (BIM) adoption has reached 80% penetration in major data center construction projects, enabling better coordination and reduced construction waste.

Edge computing architecture is driving demand for smaller, distributed facilities requiring different construction approaches than traditional centralized data centers. Micro data centers and containerized solutions are creating new market segments with distinct construction requirements and opportunities.

Major investment announcements continue shaping Thailand’s data center construction landscape, with several international cloud service providers committing to large-scale facility development. Government infrastructure programs including the Digital Economy Promotion Agency initiatives are accelerating market development through policy support and funding mechanisms.

Technology partnerships between construction companies and data center equipment manufacturers are becoming more strategic, with integrated solution offerings becoming competitive differentiators. Sustainability certifications are increasingly required for major projects, driving adoption of green construction practices and renewable energy systems.

Workforce development programs launched by industry associations and government agencies are addressing skilled labor shortages through specialized training and certification programs. International collaboration initiatives are bringing global best practices and advanced construction technologies to the Thai market.

Regulatory updates including streamlined permitting processes and updated building codes are reducing project approval timelines and providing greater clarity for construction planning. MarkWide Research analysis indicates these developments are contributing to improved market confidence and increased investment activity.

Construction companies should invest in specialized data center construction capabilities and certifications to capture premium market opportunities. Partnership strategies with international firms can provide access to advanced technologies and global best practices while leveraging local market knowledge and relationships.

Sustainability expertise development is essential for long-term competitiveness, with green building certifications becoming standard client requirements. Modular construction capabilities should be developed to improve project efficiency and meet client demands for faster delivery timelines.

Government stakeholders should continue developing supportive policy frameworks while addressing infrastructure constraints that may limit market growth. Workforce development initiatives should be expanded to ensure adequate skilled labor availability for projected market expansion.

Investors should focus on projects with strong sustainability credentials and strategic locations near major connectivity hubs. Risk management strategies should address climate-related construction challenges and potential regulatory changes affecting project economics.

Market expansion is expected to continue at robust pace, driven by ongoing digital transformation and increasing cloud adoption across Southeast Asia. Construction activity will likely shift toward more distributed edge computing facilities while maintaining strong demand for hyperscale central facilities.

Technology evolution will drive continuous adaptation in construction approaches, with artificial intelligence, automation, and advanced materials becoming standard elements of data center construction projects. Sustainability requirements will become more stringent, with carbon-neutral construction and operations becoming competitive necessities rather than differentiators.

Regional integration initiatives will likely enhance Thailand’s position as a data center hub, with cross-border connectivity improvements and regulatory harmonization supporting market growth. MWR projections indicate the market will maintain strong growth momentum through the forecast period, with construction activity expanding beyond traditional metropolitan areas.

Innovation adoption in construction technologies and project delivery methods will accelerate, driven by competitive pressures and client demands for improved efficiency and reduced environmental impact. Market maturation will bring increased standardization and specialization, with construction companies developing distinct competitive positions based on technology expertise, sustainability capabilities, or regional presence.

Thailand’s data center construction market represents a dynamic and rapidly expanding sector with substantial growth potential driven by digital transformation trends and strategic geographic advantages. The market benefits from strong government support, reliable infrastructure, and increasing international investment in Southeast Asian digital capabilities.

Key success factors for market participants include developing specialized construction expertise, embracing sustainable building practices, and adapting to evolving technology requirements. Market opportunities span multiple segments from hyperscale facilities to edge computing centers, each requiring distinct construction approaches and capabilities.

Future growth prospects remain positive, supported by continued digitalization, cloud adoption, and Thailand’s emergence as a regional technology hub. Strategic positioning and capability development in specialized data center construction will be essential for capturing the substantial opportunities ahead in this dynamic and evolving market.

What is Data Center Construction?

Data Center Construction refers to the process of building facilities that house computer systems and associated components, such as telecommunications and storage systems. These facilities are designed to support the operational needs of data processing and storage for various industries.

What are the key players in the Thailand Data Center Construction Market?

Key players in the Thailand Data Center Construction Market include companies like STT GDC, Digital Realty, and NTT Communications, which are involved in developing and managing data center facilities. These companies focus on providing robust infrastructure to support growing data demands, among others.

What are the growth factors driving the Thailand Data Center Construction Market?

The Thailand Data Center Construction Market is driven by increasing demand for cloud services, the rise of big data analytics, and the expansion of e-commerce. Additionally, the government’s push for digital transformation and smart city initiatives further fuels market growth.

What challenges does the Thailand Data Center Construction Market face?

Challenges in the Thailand Data Center Construction Market include high construction costs, regulatory hurdles, and the need for skilled labor. Environmental concerns and the impact of climate change also pose significant challenges for sustainable construction practices.

What opportunities exist in the Thailand Data Center Construction Market?

Opportunities in the Thailand Data Center Construction Market include the potential for green data centers, advancements in energy-efficient technologies, and the increasing adoption of edge computing. These trends can lead to innovative construction methods and enhanced operational efficiencies.

What trends are shaping the Thailand Data Center Construction Market?

Trends shaping the Thailand Data Center Construction Market include the integration of artificial intelligence for operational efficiency, the rise of modular data centers, and a focus on sustainability. These trends reflect the industry’s response to evolving technological demands and environmental considerations.

Thailand Data Center Construction Market

| Segmentation Details | Description |

|---|---|

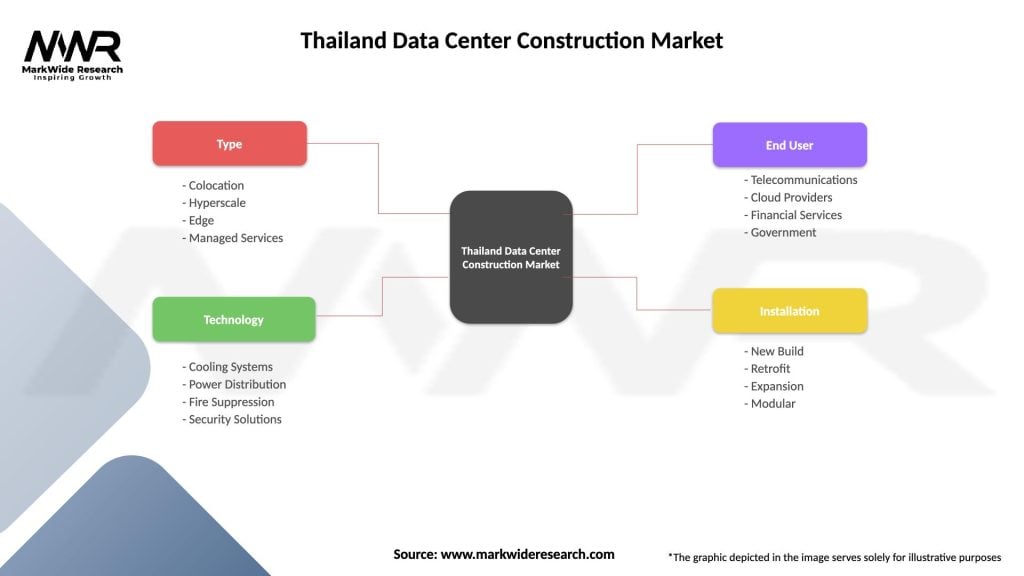

| Type | Colocation, Hyperscale, Edge, Managed Services |

| Technology | Cooling Systems, Power Distribution, Fire Suppression, Security Solutions |

| End User | Telecommunications, Cloud Providers, Financial Services, Government |

| Installation | New Build, Retrofit, Expansion, Modular |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Thailand Data Center Construction Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.