444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Switzerland data center physical security market represents a critical component of the nation’s robust digital infrastructure ecosystem. As Switzerland continues to establish itself as a leading European hub for data center operations, the demand for comprehensive physical security solutions has experienced remarkable growth. The market encompasses various security technologies including biometric access controls, surveillance systems, perimeter security, fire suppression systems, and environmental monitoring solutions designed specifically for data center facilities.

Market dynamics indicate that Switzerland’s strategic position as a neutral country, combined with its stringent data protection laws and political stability, has attracted numerous international organizations to establish their data centers within its borders. This influx has driven the adoption of advanced physical security measures, with the market experiencing a compound annual growth rate of 8.2% over recent years. The integration of artificial intelligence and machine learning technologies into physical security systems has further accelerated market expansion.

Swiss data centers are increasingly implementing multi-layered security approaches that combine traditional physical barriers with cutting-edge technological solutions. The market benefits from Switzerland’s reputation for precision engineering and high-quality manufacturing, which extends to the physical security sector. Additionally, the country’s strict regulatory environment and compliance requirements have created a favorable landscape for advanced security solution providers.

The Switzerland data center physical security market refers to the comprehensive ecosystem of physical protection solutions, technologies, and services specifically designed to safeguard data center facilities across Switzerland. This market encompasses all tangible security measures that protect data center infrastructure from unauthorized access, environmental threats, theft, vandalism, and other physical risks that could compromise critical digital assets and operations.

Physical security solutions in this context include access control systems, video surveillance networks, intrusion detection systems, perimeter security measures, fire suppression technologies, environmental monitoring equipment, and security personnel services. These components work together to create multiple layers of protection around sensitive data center environments, ensuring the integrity and availability of stored information and computing resources.

The market scope extends beyond traditional security measures to include advanced technologies such as biometric authentication, artificial intelligence-powered threat detection, drone surveillance systems, and integrated security management platforms. This comprehensive approach reflects the evolving nature of physical threats and the increasing sophistication required to protect modern data center facilities in Switzerland’s competitive digital landscape.

Switzerland’s data center physical security market demonstrates exceptional resilience and growth potential, driven by the country’s position as a premier destination for secure data storage and processing. The market has evolved significantly over the past decade, transitioning from basic security measures to sophisticated, integrated security ecosystems that leverage cutting-edge technologies and methodologies.

Key market characteristics include the dominance of enterprise-grade security solutions, with approximately 72% of implementations focusing on high-security applications for financial services, healthcare, and government sectors. The market benefits from Switzerland’s stringent regulatory framework, which mandates comprehensive physical security measures for data centers handling sensitive information.

Technological advancement represents a primary growth driver, with artificial intelligence and machine learning integration showing particularly strong adoption rates. The market has witnessed increased investment in biometric access control systems, with adoption rates reaching 58% among tier-three data centers. Additionally, the integration of IoT-based environmental monitoring systems has become standard practice, contributing to overall market expansion.

Regional distribution shows concentration in major urban centers, particularly Zurich, Geneva, and Basel, which collectively account for significant market share. The competitive landscape features both international security technology providers and specialized Swiss companies that offer tailored solutions for the local market’s unique requirements and regulatory environment.

Market intelligence reveals several critical insights that shape the Switzerland data center physical security landscape. The following key observations provide comprehensive understanding of market dynamics and opportunities:

Market maturity indicators suggest that Switzerland’s data center physical security sector has reached a sophisticated development stage, with established procurement processes, standardized implementation methodologies, and mature vendor ecosystems. This maturity creates opportunities for innovative solutions while maintaining stability for existing market participants.

Primary market drivers propelling the Switzerland data center physical security market stem from multiple interconnected factors that create sustained demand for advanced security solutions. These drivers reflect both global trends and Switzerland-specific market conditions that favor continued expansion.

Regulatory compliance requirements serve as a fundamental driver, with Swiss data protection laws and international standards mandating comprehensive physical security measures. The implementation of GDPR and other privacy regulations has intensified focus on data center security, creating mandatory upgrade cycles that drive consistent market growth. Financial services regulations, particularly those governing banking and insurance sectors, require enhanced physical security measures that exceed basic industry standards.

Digital transformation initiatives across Swiss enterprises have accelerated data center construction and expansion projects, each requiring comprehensive physical security implementations. The shift toward hybrid cloud architectures and edge computing deployments has created new security requirements that traditional solutions cannot adequately address, driving demand for innovative security technologies.

Threat landscape evolution continues to drive security investment, with physical threats becoming more sophisticated and targeted. The increasing value of digital assets stored in data centers has attracted more determined adversaries, requiring correspondingly advanced security countermeasures. Additionally, the interconnected nature of modern data centers means that physical security breaches can have cascading effects across multiple systems and organizations.

Switzerland’s strategic positioning as a neutral country with strong privacy protections attracts international organizations seeking secure data storage solutions, creating sustained demand for high-security data center facilities. This positioning advantage drives premium security requirements that exceed typical market standards.

Market constraints affecting the Switzerland data center physical security sector present challenges that organizations must navigate while pursuing growth opportunities. These restraints reflect both technical limitations and market-specific factors that can impact adoption rates and implementation timelines.

High implementation costs represent a significant barrier, particularly for smaller data center operators and organizations with limited security budgets. Advanced physical security systems require substantial capital investment, ongoing maintenance expenses, and specialized personnel training, creating financial barriers that can delay or prevent adoption of optimal security solutions.

Technical complexity challenges arise from the integration requirements of modern security systems with existing data center infrastructure. Legacy systems often lack compatibility with newer security technologies, requiring costly upgrades or complete replacements that extend implementation timelines and increase project complexity. The need for seamless integration across multiple security layers can create technical challenges that require specialized expertise.

Skills shortage issues affect the market as demand for qualified security professionals exceeds available talent pools. The specialized knowledge required to design, implement, and maintain advanced physical security systems creates workforce constraints that can limit market growth. This shortage is particularly acute in areas requiring expertise in both physical security and data center operations.

Regulatory complexity can create implementation challenges as organizations must navigate multiple compliance frameworks simultaneously. The intersection of Swiss national regulations, international standards, and industry-specific requirements can create conflicting or overlapping mandates that complicate security system design and implementation processes.

Emerging opportunities within the Switzerland data center physical security market present significant potential for growth and innovation. These opportunities reflect evolving market needs, technological advancement, and changing regulatory landscapes that create new avenues for market expansion.

Artificial intelligence integration represents a transformative opportunity, with AI-powered security analytics offering enhanced threat detection capabilities and automated response systems. The integration of machine learning algorithms into surveillance systems enables predictive security measures that can identify potential threats before they materialize, creating substantial value propositions for data center operators.

Edge computing expansion creates new market segments as organizations deploy distributed data center architectures that require specialized security solutions. Edge facilities often operate in less controlled environments than traditional data centers, creating unique security challenges that drive demand for innovative protection technologies and monitoring systems.

Sustainability integration opportunities align physical security systems with Switzerland’s environmental objectives, creating market demand for energy-efficient security technologies. Solar-powered perimeter security systems, low-power surveillance equipment, and environmentally sustainable access control solutions represent growing market segments that appeal to environmentally conscious organizations.

Cloud-native security solutions offer opportunities to serve the growing hybrid and multi-cloud market segments. Organizations operating distributed data center environments require security solutions that can provide consistent protection across multiple locations and cloud platforms, creating demand for scalable, cloud-integrated security architectures.

Managed security services present opportunities for service providers to offer comprehensive security solutions without requiring organizations to maintain internal expertise. This model particularly appeals to smaller data center operators and organizations seeking to outsource non-core security functions while maintaining high protection levels.

Market dynamics shaping the Switzerland data center physical security landscape reflect complex interactions between technological advancement, regulatory requirements, competitive pressures, and evolving customer needs. Understanding these dynamics provides insight into market trajectory and strategic opportunities.

Supply chain considerations significantly impact market dynamics, with global component shortages and logistics challenges affecting security system availability and pricing. Swiss market participants have adapted by developing local supply relationships and maintaining strategic inventory levels to ensure consistent service delivery. The emphasis on supply chain resilience has created opportunities for domestic suppliers and regional distribution networks.

Technology convergence trends drive market evolution as physical security systems increasingly integrate with IT infrastructure and cybersecurity platforms. This convergence creates new market dynamics where traditional physical security vendors compete with IT security companies and integrated solution providers. The resulting market consolidation has led to more comprehensive offerings but also increased complexity in vendor selection processes.

Customer behavior evolution shows increasing preference for integrated security platforms that provide centralized management and analytics capabilities. Organizations seek solutions that can provide comprehensive visibility across all security layers while reducing operational complexity. This trend has driven development of unified security management platforms that combine multiple security functions into cohesive systems.

Competitive intensity continues to increase as new market entrants introduce innovative technologies and established vendors expand their solution portfolios. The market has witnessed efficiency improvements of up to 35% in security system performance through technological advancement and process optimization, creating pressure for continuous innovation among market participants.

Research methodology employed for analyzing the Switzerland data center physical security market incorporates comprehensive data collection techniques, analytical frameworks, and validation processes designed to ensure accuracy and reliability of market insights. The methodology combines quantitative analysis with qualitative research to provide holistic market understanding.

Primary research activities include structured interviews with key market participants, including data center operators, security solution providers, system integrators, and regulatory officials. These interviews provide firsthand insights into market trends, challenges, opportunities, and competitive dynamics that shape the Swiss market landscape. Survey methodologies capture quantitative data on adoption rates, investment patterns, and technology preferences across different market segments.

Secondary research components encompass analysis of industry reports, regulatory documents, company financial statements, technology specifications, and market intelligence databases. This research provides historical context, market sizing information, competitive landscape analysis, and trend identification that supports primary research findings.

Data validation processes ensure research accuracy through triangulation of multiple data sources, expert review panels, and statistical analysis techniques. Market data undergoes rigorous verification procedures to identify and correct potential inconsistencies or biases that could affect research conclusions.

Analytical frameworks applied include market segmentation analysis, competitive positioning assessment, technology adoption lifecycle modeling, and regulatory impact analysis. These frameworks provide structured approaches to understanding complex market dynamics and identifying strategic implications for market participants.

Regional distribution of the Switzerland data center physical security market reveals distinct patterns that reflect economic activity, regulatory requirements, and infrastructure development across different Swiss regions. MarkWide Research analysis indicates significant concentration in major urban centers while showing emerging growth in secondary markets.

Zurich region dominates the market landscape, accounting for approximately 42% of total market activity. This concentration reflects Zurich’s position as Switzerland’s financial capital and primary technology hub, attracting numerous multinational corporations and financial institutions that require high-security data center facilities. The region benefits from excellent infrastructure, skilled workforce availability, and proximity to major European markets.

Geneva area represents the second-largest regional market, capturing roughly 28% market share driven by its role as an international diplomatic center and headquarters location for numerous global organizations. The presence of United Nations agencies, international NGOs, and multinational corporations creates sustained demand for secure data center facilities with advanced physical security implementations.

Basel region accounts for approximately 18% of market activity, supported by its position as a major pharmaceutical and chemical industry center. The life sciences sector’s stringent data security requirements drive demand for specialized physical security solutions that can protect sensitive research data and intellectual property stored in data center facilities.

Emerging regional markets including Bern, Lausanne, and other secondary cities collectively represent the remaining market share, showing steady growth as organizations seek cost-effective alternatives to major urban centers while maintaining high security standards. These regions benefit from lower operational costs while still providing access to skilled workforce and reliable infrastructure.

Competitive dynamics within the Switzerland data center physical security market feature a diverse ecosystem of international technology providers, specialized security companies, and local system integrators. The market structure reflects the complex requirements of Swiss data center operators and the sophisticated security solutions needed to meet regulatory and operational demands.

Leading market participants include established security technology providers that offer comprehensive solution portfolios:

Regional specialists and system integrators play crucial roles in market delivery, providing localized expertise, customization capabilities, and ongoing support services. These organizations often partner with international technology providers to deliver complete solutions that meet specific Swiss market requirements and regulatory compliance needs.

Market positioning strategies vary among competitors, with some focusing on technology innovation, others emphasizing service excellence, and several pursuing vertical market specialization. The competitive landscape continues to evolve through mergers, acquisitions, and strategic partnerships that reshape market dynamics and solution offerings.

Market segmentation of the Switzerland data center physical security market reveals distinct categories based on technology type, application area, end-user industry, and deployment model. This segmentation provides detailed insight into market structure and growth opportunities across different market segments.

By Technology Type:

By Application Area:

By End-User Industry:

Category analysis reveals distinct characteristics and growth patterns across different segments of the Switzerland data center physical security market. Each category demonstrates unique drivers, challenges, and opportunities that shape overall market dynamics.

Access Control Systems Category represents the largest market segment, driven by regulatory requirements and increasing sophistication of authentication technologies. Biometric systems show particularly strong growth, with adoption rates increasing by 23% annually as organizations seek to enhance security while improving user experience. Multi-factor authentication implementations have become standard practice across tier-three data centers.

Video Surveillance Category benefits from artificial intelligence integration and advanced analytics capabilities that provide proactive threat detection. The transition from analog to IP-based systems continues, with smart cameras and video analytics software showing robust demand. Integration with access control and alarm systems creates comprehensive security ecosystems that appeal to sophisticated data center operators.

Environmental Security Category demonstrates rapid growth as organizations recognize the importance of protecting against environmental threats. Climate monitoring systems, power management solutions, and disaster prevention technologies have become essential components of comprehensive data center security strategies. The category benefits from increasing awareness of environmental risks and regulatory requirements for business continuity planning.

Intrusion Detection Category evolves toward more sophisticated sensor technologies and intelligent alarm management systems. The integration of machine learning algorithms enables reduction of false alarms while improving genuine threat detection capabilities. Perimeter security solutions increasingly incorporate multiple detection technologies to create layered protection approaches.

Industry participants and stakeholders in the Switzerland data center physical security market realize substantial benefits through participation in this dynamic and growing sector. These benefits extend across the entire value chain, from technology providers to end-user organizations.

For Technology Providers:

For Data Center Operators:

For System Integrators:

For End-User Organizations:

SWOT analysis provides comprehensive evaluation of the Switzerland data center physical security market’s internal strengths and weaknesses alongside external opportunities and threats that influence market development and strategic planning.

Strengths:

Weaknesses:

Opportunities:

Threats:

Key trends shaping the Switzerland data center physical security market reflect technological advancement, changing threat landscapes, and evolving customer requirements that drive market evolution and strategic decision-making.

Artificial Intelligence Integration represents the most significant trend, with AI-powered security analytics becoming standard features in new implementations. Machine learning algorithms enable predictive threat detection, automated response systems, and intelligent video analytics that substantially enhance security effectiveness. Organizations report security incident reduction of up to 45% through AI integration, driving widespread adoption across all market segments.

Cloud-Native Security Architectures gain momentum as organizations adopt hybrid and multi-cloud strategies that require consistent security across distributed environments. Cloud-based security management platforms provide centralized control and analytics capabilities while supporting scalable deployment models that align with modern data center architectures.

Biometric Authentication Advancement continues with more sophisticated technologies including facial recognition, iris scanning, and behavioral biometrics that provide enhanced security while improving user experience. Multi-modal biometric systems that combine multiple authentication factors show particularly strong adoption in high-security applications.

Environmental Security Focus intensifies as organizations recognize the critical importance of protecting against environmental threats. Advanced climate monitoring systems, predictive maintenance capabilities, and disaster prevention technologies become essential components of comprehensive security strategies.

Integration and Convergence trends drive demand for unified security platforms that combine multiple security functions into cohesive systems. Organizations increasingly prefer integrated solutions that provide comprehensive visibility and control while reducing operational complexity and vendor management requirements.

Sustainability Integration aligns security systems with environmental objectives through energy-efficient technologies, renewable power sources, and environmentally sustainable materials. This trend reflects Switzerland’s commitment to environmental responsibility and creates market opportunities for green security solutions.

Industry developments within the Switzerland data center physical security market demonstrate the dynamic nature of this sector and highlight significant events that shape market trajectory and competitive landscape.

Technology Innovation Initiatives have accelerated with major security providers investing heavily in artificial intelligence and machine learning capabilities. Recent developments include launch of AI-powered video analytics platforms that can identify potential security threats with accuracy rates exceeding 92%, significantly reducing false alarm incidents while improving genuine threat detection.

Regulatory Framework Updates continue to influence market development, with Swiss authorities implementing enhanced data protection requirements that mandate stronger physical security measures for data centers handling sensitive information. These regulatory changes create mandatory upgrade cycles that drive consistent market demand while raising security standards across the industry.

Strategic Partnerships and Acquisitions reshape the competitive landscape as companies seek to expand their solution portfolios and market reach. Recent consolidation activities have created more comprehensive solution providers while eliminating smaller competitors, leading to increased market concentration among leading vendors.

Infrastructure Investment Projects by major data center operators include significant physical security components that demonstrate market growth and sophistication. These projects often serve as showcase implementations that influence industry standards and drive adoption of advanced security technologies across the broader market.

International Expansion Activities by Swiss-based security companies leverage their domestic market success to pursue opportunities in neighboring European countries. This expansion demonstrates the strength of Swiss security expertise and creates additional growth opportunities for domestic market participants.

Sustainability Initiatives gain prominence as security providers develop environmentally friendly solutions that align with Switzerland’s environmental objectives. These initiatives include energy-efficient security systems, renewable power integration, and sustainable manufacturing processes that appeal to environmentally conscious customers.

Strategic recommendations for market participants in the Switzerland data center physical security sector focus on positioning for sustained growth while addressing evolving market challenges and opportunities. MWR analysis suggests several key strategic priorities for different stakeholder categories.

For Technology Providers: Focus on developing integrated security platforms that combine multiple security functions into unified solutions. Invest heavily in artificial intelligence and machine learning capabilities to differentiate offerings and provide enhanced value propositions. Establish strong local partnerships with system integrators and service providers to ensure effective market coverage and customer support.

For Data Center Operators: Implement comprehensive security strategies that address both current threats and future requirements. Prioritize solutions that provide scalability and flexibility to accommodate changing business needs and regulatory requirements. Consider managed security services to access specialized expertise while controlling operational costs.

For System Integrators: Develop specialized expertise in data center security implementations to differentiate from general security providers. Invest in training and certification programs to ensure technical competency with advanced security technologies. Build strategic partnerships with leading technology providers to access cutting-edge solutions and support resources.

For New Market Entrants: Focus on niche market segments or specialized technologies where established competitors may have limited presence. Leverage innovative technologies or unique value propositions to gain market traction. Consider partnership strategies with established market participants to accelerate market entry and credibility development.

For Investors: Evaluate opportunities in companies that demonstrate strong technology innovation capabilities and established market positions. Consider the long-term growth potential driven by digital transformation trends and regulatory requirements. Assess the sustainability of competitive advantages and market positioning strategies.

Future market trajectory for the Switzerland data center physical security market indicates continued growth driven by technological advancement, regulatory evolution, and expanding digital infrastructure requirements. The market outlook reflects both opportunities and challenges that will shape industry development over the coming years.

Growth projections suggest the market will maintain robust expansion with projected compound annual growth rates of 7.5% over the next five years. This growth reflects sustained demand from digital transformation initiatives, regulatory compliance requirements, and increasing sophistication of security threats that require advanced countermeasures.

Technology evolution will continue to drive market transformation, with artificial intelligence, machine learning, and IoT integration becoming standard features across all security categories. The emergence of quantum computing and advanced encryption technologies may create new security requirements that drive additional market opportunities.

Market consolidation trends are expected to continue as companies seek to expand their solution portfolios and market reach through strategic acquisitions and partnerships. This consolidation may reduce the number of independent vendors while creating more comprehensive solution providers with broader capabilities.

Regulatory landscape evolution will likely introduce additional compliance requirements that mandate enhanced security measures, creating sustained market demand while potentially increasing implementation complexity. Organizations must prepare for evolving regulatory frameworks that may require system upgrades or replacements.

Sustainability integration will become increasingly important as environmental considerations influence purchasing decisions and regulatory requirements. Security providers that can demonstrate environmental responsibility while maintaining high performance standards will gain competitive advantages in the evolving market landscape.

International market expansion opportunities will emerge as Swiss security expertise gains recognition in broader European markets, creating growth potential beyond domestic boundaries for successful market participants.

The Switzerland data center physical security market represents a dynamic and rapidly evolving sector that combines technological innovation with stringent security requirements to create substantial opportunities for market participants. The market benefits from Switzerland’s unique position as a secure, politically stable jurisdiction with strong regulatory frameworks that mandate comprehensive physical security measures for data center facilities.

Market fundamentals remain strong, supported by continued digital transformation initiatives, regulatory compliance requirements, and increasing sophistication of security threats that drive demand for advanced protection technologies. The integration of artificial intelligence, machine learning, and IoT technologies creates new capabilities while opening additional market segments for innovative solution providers.

Competitive dynamics favor organizations that can provide integrated security platforms combining multiple protection layers into unified, manageable systems. The market rewards innovation, technical expertise, and strong customer relationships while penalizing companies that fail to adapt to evolving technology and regulatory requirements.

Strategic success in this market requires understanding of local regulatory requirements, investment in advanced technologies, and development of comprehensive solution portfolios that address diverse customer needs. Organizations that can effectively balance innovation with reliability while providing exceptional customer service will capture the greatest market opportunities.

The future outlook for the Switzerland data center physical security market remains positive, with sustained growth expected across all major market segments. Success will increasingly depend on technological innovation, regulatory compliance capabilities, and the ability to provide integrated solutions that address the complex security challenges facing modern data center operations in Switzerland’s sophisticated digital infrastructure landscape.

What is Data Center Physical Security?

Data Center Physical Security refers to the measures and protocols implemented to protect data centers from physical threats such as unauthorized access, natural disasters, and vandalism. This includes surveillance systems, access controls, and environmental monitoring.

What are the key players in the Switzerland Data Center Physical Security Market?

Key players in the Switzerland Data Center Physical Security Market include companies like Schneider Electric, IBM, and Cisco Systems, which provide various security solutions and technologies for data centers, among others.

What are the main drivers of the Switzerland Data Center Physical Security Market?

The main drivers of the Switzerland Data Center Physical Security Market include the increasing need for data protection due to rising cyber threats, the growth of cloud computing, and the expansion of data center infrastructure to support digital transformation.

What challenges does the Switzerland Data Center Physical Security Market face?

Challenges in the Switzerland Data Center Physical Security Market include the high costs associated with implementing advanced security technologies, the complexity of integrating various security systems, and the evolving nature of security threats that require constant updates and adaptations.

What opportunities exist in the Switzerland Data Center Physical Security Market?

Opportunities in the Switzerland Data Center Physical Security Market include the adoption of AI and machine learning for enhanced security analytics, the increasing demand for compliance with data protection regulations, and the potential for innovative security solutions tailored to specific industry needs.

What trends are shaping the Switzerland Data Center Physical Security Market?

Trends shaping the Switzerland Data Center Physical Security Market include the integration of IoT devices for real-time monitoring, the shift towards remote management of security systems, and the growing emphasis on sustainability in security practices.

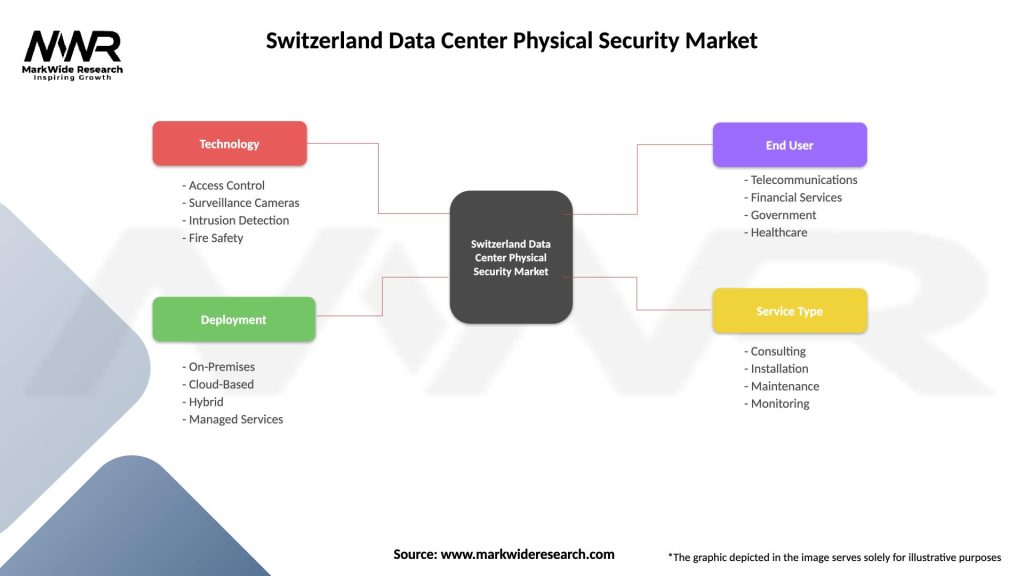

Switzerland Data Center Physical Security Market

| Segmentation Details | Description |

|---|---|

| Technology | Access Control, Surveillance Cameras, Intrusion Detection, Fire Safety |

| Deployment | On-Premises, Cloud-Based, Hybrid, Managed Services |

| End User | Telecommunications, Financial Services, Government, Healthcare |

| Service Type | Consulting, Installation, Maintenance, Monitoring |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Switzerland Data Center Physical Security Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.