The Sweden Life and Non-Life Insurance Market has experienced steady growth over the years, driven by the country’s robust economy, increasing awareness about insurance products, and the rising focus on financial security. Insurance is an essential aspect of Sweden’s socio-economic landscape, offering protection against various risks for individuals, businesses, and assets. This market overview provides insights into the current state of the Life and Non-Life Insurance sector in Sweden, analyzing its meaning, key market insights, drivers, restraints, opportunities, dynamics, regional analysis, competitive landscape, segmentation, and category-wise insights.

Meaning:

Life insurance is a contract between an individual and an insurance company, wherein the insured pays regular premiums, and in return, the insurer provides financial protection to the policyholder’s beneficiaries upon their death. On the other hand, Non-Life insurance, also known as general insurance, covers various risks that do not involve life or death, such as health, property, vehicles, travel, and more. These insurance products are designed to safeguard individuals and businesses against potential losses, providing peace of mind and financial security.

Executive Summary:

The executive summary of the Sweden Life and Non-Life Insurance Market provides a concise overview of the market’s key highlights, growth prospects, and significant trends. It gives readers an insight into the major opportunities and challenges faced by the industry, along with the latest developments and the potential impact of Covid-19 on the market.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

The Sweden Life and Non-Life Insurance Market is shaped by a dynamic blend of socio-economic factors, technological innovation, and regulatory influences. In Sweden, a mature insurance market, both life and non-life insurance segments are evolving to meet the changing needs of individuals, businesses, and the public sector. With high digital literacy, a stable economic environment, and robust consumer protection laws, the Swedish insurance industry is well-positioned to offer innovative products and services. The market benefits from advanced underwriting processes, risk management tools, and tailored policies that respond to emerging risks such as cyber threats, climate change, and evolving demographic trends.

Evolving Consumer Expectations: Swedish policyholders increasingly demand digital, personalized, and transparent insurance solutions.

Regulatory Rigor and Consumer Protection: Stringent regulatory frameworks and strong consumer protection measures enhance market stability and trust.

Technological Advancements: Digital transformation, including AI, big data analytics, and online distribution channels, is revolutionizing underwriting, claims processing, and customer engagement.

Economic Stability and Wealth Management: A stable economic environment coupled with high per capita income drives demand for both life and non-life insurance products.

Focus on Sustainability: Environmental, social, and governance (ESG) factors are influencing product development and underwriting practices, particularly in non-life segments.

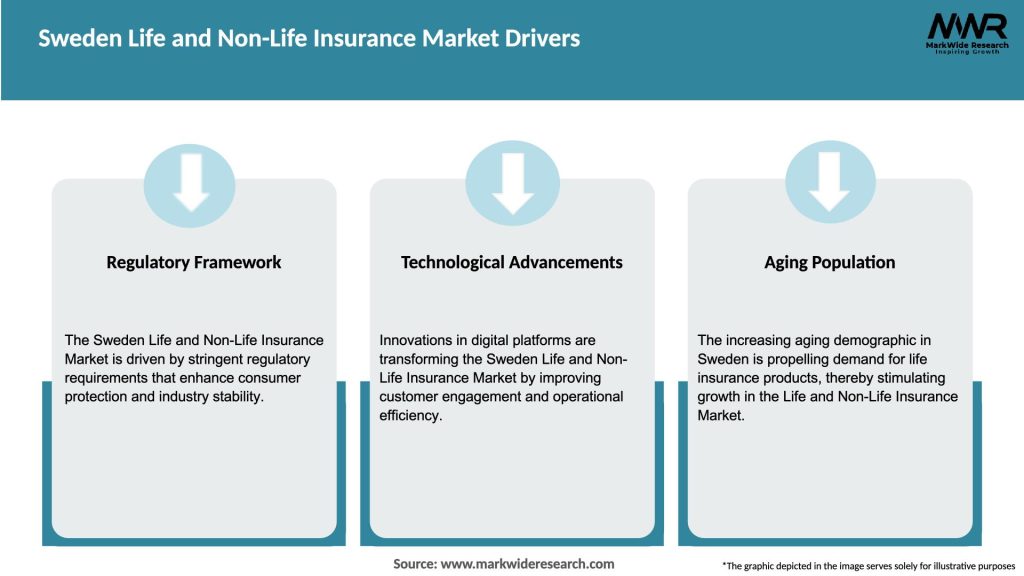

Market Drivers

Several factors are propelling the growth of the Sweden Life and Non-Life Insurance Market:

Increasing Digital Adoption: The rapid uptake of digital technologies by consumers and insurers is driving efficiency, reducing costs, and enhancing customer experience.

Rising Health and Longevity Awareness: In the life insurance segment, greater awareness of health issues and longevity planning is boosting demand for comprehensive life policies and pension products.

Economic and Demographic Shifts: An aging population combined with stable economic growth creates a strong need for retirement planning, life coverage, and tailored non-life policies.

Innovation in Product Offerings: The development of innovative insurance products, including usage-based and microinsurance solutions, is expanding market reach and attracting new customer segments.

Risk Mitigation and Loss Prevention: In the non-life segment, increased awareness of risks such as cyber incidents, natural disasters, and business interruptions is driving demand for specialized insurance products.

Market Restraints

Despite its mature market status, the Sweden Life and Non-Life Insurance Market faces several challenges:

Competitive Pricing Pressure: High competition among established players leads to pricing pressures, affecting profit margins.

Regulatory Complexity: Constantly evolving regulations, especially concerning data privacy (e.g., GDPR) and solvency requirements, add to operational complexities.

Digital Transformation Challenges: While digital adoption offers benefits, legacy systems and the need for significant capital investment in new technology can slow progress.

Low Interest Rate Environment: Persistently low interest rates challenge the investment returns of insurers, particularly affecting the life insurance segment.

Changing Risk Profiles: Emerging risks, such as cyber threats and climate change, require rapid adaptation in product offerings and risk assessment models.

Market Opportunities

The Sweden Life and Non-Life Insurance Market presents numerous opportunities for growth and innovation:

Expansion of Digital Platforms: Further development of online sales, claims processing, and customer service platforms can enhance efficiency and attract tech-savvy customers.

Integration of AI and Big Data: Leveraging advanced analytics and artificial intelligence to optimize underwriting, risk management, and fraud detection can lead to improved profitability.

Customized and On-Demand Products: The rising demand for personalized insurance solutions opens opportunities for insurers to offer bespoke products tailored to individual risk profiles.

Cross-Selling and Bundling: Opportunities exist to bundle life and non-life products, offering comprehensive risk management solutions to both individual and corporate customers.

Sustainability and Green Insurance: With growing environmental awareness, developing green insurance products that incentivize sustainable practices can capture a new market segment.

Collaborative Ecosystems: Partnerships with insurtech startups, technology providers, and financial institutions can drive innovation and open new channels for distribution.

Market Dynamics

The dynamics of the Sweden Life and Non-Life Insurance Market are influenced by a complex interplay of internal and external factors:

Supply Side Factors:

Technological Advancements: Insurers are investing in modern IT infrastructures and analytics capabilities, enhancing product offerings and operational efficiencies.

Product Innovation: Ongoing research and development in insurance products drive differentiation and cater to evolving consumer needs.

Talent and Expertise: The availability of skilled professionals in data science, risk management, and digital transformation plays a critical role in market performance.

Demand Side Factors:

Changing Consumer Preferences: Modern Swedish consumers prioritize digital accessibility, transparency, and personalized services in their insurance choices.

Economic Environment: Stable economic growth, high household incomes, and low unemployment rates support increased discretionary spending on insurance.

Awareness of Risks: Rising awareness of personal, property, and business risks is fueling demand for comprehensive non-life insurance policies.

Economic and Regulatory Influences:

Solvency and Capital Requirements: Adherence to Solvency II and other regulatory frameworks ensures market stability but requires ongoing investment in risk management.

Interest Rate Environment: A persistently low interest rate scenario affects insurers’ investment income, prompting a need for innovative risk-adjusted pricing models.

Regulatory Innovations: Progressive regulatory reforms aimed at promoting digitalization and consumer protection continue to shape market strategies.

Regional Analysis

While Sweden is a relatively small but highly developed market, regional variations within the country offer insights into the market dynamics:

Stockholm Region:

Economic and Financial Hub: As the capital and financial center, Stockholm is home to a significant share of life and non-life insurance business, characterized by advanced technology adoption and high customer expectations.

Corporate Market: A large number of multinational corporations and high-net-worth individuals drive demand for specialized insurance products.

Gothenburg and Malmö:

Industrial and Commercial Centers: These regions are critical for non-life insurance, with strong demand from manufacturing, logistics, and service sectors.

Innovation and Startups: Growing clusters of insurtech startups in these cities are fostering innovation and competitive product offerings.

Rural and Peripheral Areas:

Tailored Local Solutions: Smaller towns and rural areas demand customized insurance solutions, particularly in property and agriculture-related risks.

Digital Penetration: Increasing internet penetration in these regions is driving adoption of digital insurance services, although traditional channels still play a role.

Competitive Landscape

Leading Companies in the Sweden Life and Non-Life Insurance Market:

Folksam Group

If P&C Insurance Ltd.

Länsförsäkringar AB

Tryg Forsikring A/S

Svedea AB

Skandia Group

BNP Paribas Cardif

Alecta Pensionsförsäkring, ömsesidigt

Gjensidige Forsikring ASA

AMF Pension

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

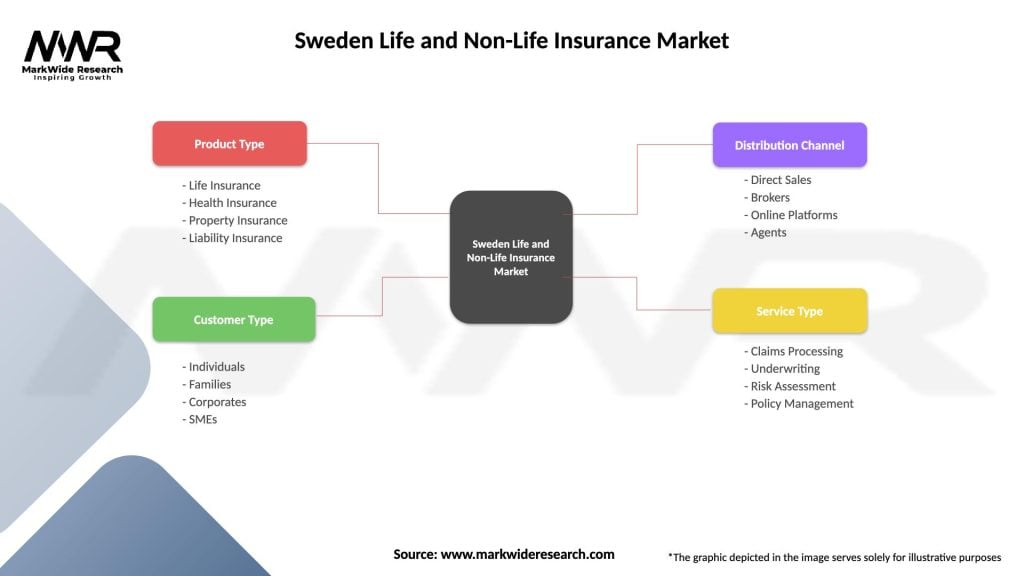

Segmentation

The Sweden Life and Non-Life Insurance Market can be segmented based on various criteria to offer a comprehensive view of its structure:

By Product Type:

Life Insurance:

Term Life Insurance: Policies providing coverage for a specific period.

Whole Life Insurance: Policies offering lifetime coverage along with cash value accumulation.

Endowment Policies: Products that combine life coverage with savings or investment components.

Pension and Annuity Products: Solutions designed to secure retirement income.

Non-Life Insurance:

Property Insurance: Coverage for residential and commercial properties.

Motor Insurance: Policies covering private and commercial vehicles.

Health and Accident Insurance: Products addressing medical expenses, disability, and accidental injuries.

Liability Insurance: Coverage to protect against claims related to legal liabilities.

Specialty Insurance: Policies for niche markets such as cyber, travel, and marine insurance.

By Distribution Channel:

Direct Sales: Online platforms and company websites offering digital quotes and policy management.

Agency and Broker Networks: Traditional channels where agents and brokers provide personalized advice and product bundling.

Partnerships and Bancassurance: Collaborations with banks and financial institutions to distribute insurance products to a broader customer base.

By Customer Type:

Individual Consumers: Tailored solutions addressing personal, family, and retirement needs.

Small and Medium Enterprises (SMEs): Business-focused products that cover property, liability, and employee benefits.

Large Corporations: Comprehensive risk management and group insurance solutions for multinational companies.

Public Sector: Specialized insurance products designed for government agencies and public institutions.

Category-wise Insights

Each segment within the Sweden Life and Non-Life Insurance Market offers unique features and value propositions:

Life Insurance: Products are increasingly focused on offering not just protection but also long-term savings, investment growth, and retirement planning. Digital tools enable personalized underwriting, while partnerships with healthcare providers enhance wellness benefits.

Non-Life Insurance: With a strong emphasis on risk prevention and claims efficiency, non-life products are evolving to incorporate innovative technologies such as telematics in motor insurance and real-time risk monitoring in property and liability segments.

Key Benefits for Industry Participants and Stakeholders

The Sweden Life and Non-Life Insurance Market provides numerous benefits for insurers, intermediaries, and policyholders:

Enhanced Customer Trust: Robust regulatory frameworks and strong consumer protection laws build confidence and long-term loyalty among policyholders.

Digital Efficiency: Adoption of digital technologies leads to streamlined processes, reduced operational costs, and faster claims settlements.

Revenue Growth and Diversification: Innovative product offerings and cross-selling opportunities drive revenue streams, while tailored solutions address diverse customer needs.

Risk Mitigation: Advanced risk assessment and data analytics improve underwriting accuracy and reduce exposure to unforeseen losses.

Competitive Differentiation: Insurers that invest in technology and personalized service can distinguish themselves in a competitive market.

SWOT Analysis

Strengths:

Mature and Stable Market: A well-established insurance industry with high consumer trust and consistent regulatory support.

High Digital Penetration: Extensive use of digital platforms facilitates improved customer engagement and operational efficiencies.

Innovative Product Offerings: Continuous innovation in product design and distribution channels meets evolving consumer needs.

Strong Economic Fundamentals: A stable economy with high disposable incomes supports sustained demand for both life and non-life insurance products.

Weaknesses:

Pricing Pressures: High competition results in thin profit margins, necessitating constant cost optimization.

Legacy Systems: Some traditional insurers face challenges in modernizing legacy IT infrastructures.

Low Interest Rates: A persistently low interest rate environment affects investment returns, particularly for life insurers.

Regulatory Burdens: Compliance with evolving regulatory standards requires ongoing investments in risk management and digital transformation.

Opportunities:

Expansion into Niche Segments: Growth opportunities exist in specialized areas such as cyber insurance, health tech integration, and green insurance products.

Technological Integration: Further adoption of AI, big data, and IoT for underwriting and claims processing can drive efficiency.

Partnership and Collaboration: Strategic alliances with insurtech startups and financial institutions offer avenues for market expansion.

Customer-Centric Innovations: Enhanced personalization and on-demand product offerings can attract younger, tech-savvy consumers.

Threats:

Intense Market Competition: Fierce competition among established players and new entrants could lead to market saturation.

Economic Uncertainty: Global economic fluctuations and potential shifts in consumer spending may impact premium growth.

Cybersecurity Risks: Increasing digitalization raises concerns over data breaches and cyber-attacks, necessitating robust security measures.

Regulatory Changes: Rapid changes in regulatory landscapes may increase operational costs and disrupt market dynamics.

Market Key Trends

Several key trends are shaping the Sweden Life and Non-Life Insurance Market:

Digital Transformation: Insurers are increasingly investing in digital platforms for customer service, underwriting, and claims management.

Personalization and Customization: Data analytics and AI enable insurers to offer tailored products and pricing models that match individual risk profiles.

Omnichannel Distribution: A blended approach combining online platforms, agency networks, and bancassurance is expanding market reach.

Sustainability Focus: Environmental and social responsibility are influencing product development, with a growing emphasis on green insurance solutions.

Preventive Risk Management: Increased adoption of telematics, wearable technology, and IoT devices helps in early risk detection and proactive loss prevention.

Covid-19 Impact

The Covid-19 pandemic has influenced the Sweden Life and Non-Life Insurance Market in several ways:

Accelerated Digital Adoption: The crisis accelerated the transition to digital channels, with more customers preferring online policy management and claims processing.

Shift in Consumer Priorities: Health and life insurance products have seen increased demand as individuals reassess personal risk and future uncertainties.

Operational Adjustments: Insurers have adapted their risk assessment and underwriting processes to account for the pandemic’s impact on mortality, morbidity, and economic stability.

Market Stabilization Efforts: Government stimulus packages and regulatory relief measures have helped stabilize the market amid economic challenges.

Increased Focus on Business Interruption: Non-life insurance segments, particularly business interruption and liability, are reassessing coverage terms and risk exposures in a post-pandemic world.

Key Industry Developments

The Sweden Life and Non-Life Insurance Market has witnessed several significant developments:

Technological Upgrades: Insurers are investing in advanced IT systems, digital underwriting, and AI-driven claims processing to improve efficiency.

Strategic Collaborations: Partnerships between traditional insurers and insurtech startups are driving product innovation and expanding distribution channels.

Product Diversification: New products tailored to emerging risks—such as cyber, climate-related, and pandemic-related coverages—are gaining traction.

Regulatory Enhancements: Continuous improvements in regulatory frameworks ensure robust consumer protection and market stability.

Sustainability Initiatives: Companies are integrating ESG principles into their underwriting and investment strategies, aligning with global sustainability trends.

Analyst Suggestions

Based on current market trends and challenges, industry analysts suggest the following strategies for stakeholders in the Sweden Life and Non-Life Insurance Market:

Invest in Digital Transformation: Prioritize modernizing IT infrastructures and adopting advanced analytics to enhance customer engagement and operational efficiency.

Enhance Product Innovation: Develop flexible, customized products that address emerging risks and cater to evolving consumer needs.

Focus on Data Security: Strengthen cybersecurity measures and data governance frameworks to protect sensitive customer information.

Expand Omnichannel Strategies: Leverage a combination of digital channels, traditional agency networks, and bancassurance partnerships to broaden market reach.

Monitor Regulatory Trends: Stay abreast of regulatory changes and proactively adjust business models to ensure compliance and maintain competitive advantage.

Future Outlook

The future outlook for the Sweden Life and Non-Life Insurance Market is positive, with sustained growth anticipated in the coming years. Key factors shaping the market’s future include:

Ongoing Digital Disruption: Continued investment in digital technologies will further streamline operations and enhance the customer experience.

Increasing Demand for Personalized Solutions: A shift toward customer-centric models and tailored products is expected to drive premium growth.

Emerging Risk Opportunities: New risk areas such as cyber threats, climate change, and evolving health challenges will spur the development of innovative insurance products.

Enhanced Distribution Channels: The convergence of digital and traditional distribution methods will create a more resilient and accessible market.

Regulatory Support: Ongoing government and regulatory support for consumer protection and market stability will provide a solid foundation for growth.

Conclusion

The Sweden Life and Non-Life Insurance Market is a mature and dynamic industry marked by a strong digital orientation, innovative product offerings, and robust consumer protection. With evolving consumer expectations, technological advancements, and a focus on sustainability, insurers in Sweden are well-equipped to meet future challenges and capitalize on emerging opportunities. Despite competitive pressures and regulatory complexities, the market continues to offer significant growth potential for stakeholders committed to digital transformation, risk management, and customer-centric innovation. As Sweden’s insurance landscape evolves in response to global trends and local needs, the integration of advanced technologies and personalized services will be key to maintaining a competitive edge and ensuring long-term success.

What is Life and Non-Life Insurance?

Life and Non-Life Insurance refers to the two main categories of insurance products. Life insurance provides financial protection to beneficiaries upon the policyholder’s death, while non-life insurance covers various risks such as property damage, liability, and health-related expenses.

What are the key players in the Sweden Life and Non-Life Insurance Market?

Key players in the Sweden Life and Non-Life Insurance Market include companies like Folksam, Länsförsäkringar, and Trygg-Hansa, which offer a range of insurance products from life coverage to property and casualty insurance, among others.

What are the growth factors driving the Sweden Life and Non-Life Insurance Market?

The growth of the Sweden Life and Non-Life Insurance Market is driven by factors such as increasing consumer awareness of insurance products, a growing aging population requiring life insurance, and rising demand for comprehensive health and property coverage.

What challenges does the Sweden Life and Non-Life Insurance Market face?

Challenges in the Sweden Life and Non-Life Insurance Market include regulatory changes that affect product offerings, competition from insurtech companies, and the need to adapt to changing consumer preferences and digital transformation.

What opportunities exist in the Sweden Life and Non-Life Insurance Market?

Opportunities in the Sweden Life and Non-Life Insurance Market include the potential for innovative insurance products tailored to specific demographics, the integration of technology for better customer service, and the expansion of coverage options in emerging sectors.

What trends are shaping the Sweden Life and Non-Life Insurance Market?

Trends in the Sweden Life and Non-Life Insurance Market include the rise of digital insurance platforms, increased focus on sustainability and ESG factors, and the growing importance of personalized insurance solutions to meet diverse consumer needs.

Leading Companies in the Sweden Life and Non-Life Insurance Market:

Folksam Group

If P&C Insurance Ltd.

Länsförsäkringar AB

Tryg Forsikring A/S

Svedea AB

Skandia Group

BNP Paribas Cardif

Alecta Pensionsförsäkring, ömsesidigt

Gjensidige Forsikring ASA

AMF Pension

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.