444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Sweden data center networking market represents a dynamic and rapidly evolving sector within the Nordic region’s technology landscape. Sweden’s strategic position as a digital innovation hub, combined with its robust infrastructure and commitment to sustainability, has positioned the country as a leading destination for data center investments. The market encompasses a comprehensive range of networking solutions, including switches, routers, network security appliances, and software-defined networking technologies that enable efficient data transmission and management within data center environments.

Market dynamics indicate substantial growth momentum, driven by increasing digitalization across industries and the rising demand for cloud services. The Swedish market benefits from favorable government policies supporting digital transformation, abundant renewable energy resources, and a highly skilled workforce. Data center operators in Sweden are increasingly focusing on advanced networking solutions that offer enhanced performance, scalability, and energy efficiency to meet the growing demands of modern applications and services.

Growth projections suggest the market will experience a compound annual growth rate of 8.2% over the forecast period, reflecting the strong underlying demand for data center services and the continuous evolution of networking technologies. The market’s expansion is further supported by Sweden’s position as a gateway to the broader European market and its reputation for technological innovation and environmental sustainability.

The Sweden data center networking market refers to the comprehensive ecosystem of networking hardware, software, and services specifically designed to facilitate data transmission, storage, and processing within data center facilities located in Sweden. This market encompasses all networking components that enable seamless connectivity, data flow management, and communication between servers, storage systems, and end-users within data center environments.

Core components of this market include ethernet switches, routers, load balancers, firewalls, network monitoring tools, and emerging technologies such as software-defined networking (SDN) and network function virtualization (NFV). These solutions work collectively to ensure optimal performance, security, and reliability of data center operations while supporting various applications ranging from enterprise computing to cloud services and content delivery networks.

Sweden’s data center networking market demonstrates remarkable resilience and growth potential, driven by the country’s strategic advantages in renewable energy, political stability, and advanced digital infrastructure. The market benefits from Sweden’s position as a preferred location for hyperscale data centers, with major international technology companies establishing significant operations in the region.

Key market drivers include the accelerating adoption of cloud computing services, which accounts for approximately 42% of enterprise IT spending in Sweden, and the increasing demand for edge computing solutions. The market is characterized by strong competition among established networking vendors and emerging technology providers, fostering innovation and driving down costs for end-users.

Sustainability initiatives play a crucial role in market development, with Swedish data centers achieving some of the world’s lowest power usage effectiveness (PUE) ratios. This environmental focus attracts environmentally conscious enterprises and supports the country’s carbon neutrality goals, creating additional demand for energy-efficient networking solutions.

Strategic market insights reveal several critical trends shaping the Sweden data center networking landscape:

Digital transformation initiatives across Swedish enterprises serve as the primary catalyst for data center networking market growth. Organizations are increasingly migrating their IT infrastructure to cloud-based solutions, requiring robust networking capabilities to support seamless data access and application performance. The accelerating pace of digitalization has created unprecedented demand for reliable, high-performance networking solutions.

Government support for digital infrastructure development provides significant momentum for market expansion. Swedish authorities have implemented favorable policies encouraging data center investments, including tax incentives and streamlined regulatory processes. These initiatives have attracted major international technology companies to establish operations in Sweden, driving substantial demand for advanced networking equipment.

Renewable energy availability represents a unique competitive advantage for Swedish data centers, attracting environmentally conscious organizations seeking sustainable IT solutions. The abundance of clean energy sources enables data center operators to offer carbon-neutral services, creating additional demand for energy-efficient networking technologies that complement these sustainability objectives.

5G network deployment is generating substantial demand for edge computing infrastructure, requiring sophisticated networking solutions to support low-latency applications and real-time data processing. Swedish telecommunications operators are investing heavily in 5G infrastructure, creating new opportunities for data center networking providers.

High initial capital requirements for advanced networking infrastructure can limit market adoption, particularly among smaller organizations with constrained IT budgets. The complexity and cost of implementing cutting-edge networking solutions may deter some potential customers from upgrading their existing infrastructure, slowing overall market growth.

Skills shortage in specialized networking technologies presents a significant challenge for market expansion. The rapid evolution of networking technologies requires highly skilled professionals capable of designing, implementing, and managing complex data center networks. The limited availability of qualified personnel can constrain deployment timelines and increase operational costs.

Regulatory compliance requirements related to data protection and privacy can complicate networking infrastructure decisions. Organizations must ensure their networking solutions comply with GDPR and other regulatory frameworks, potentially limiting technology choices and increasing implementation complexity.

Technology obsolescence risks create uncertainty for long-term infrastructure investments. The rapid pace of technological advancement in networking equipment may render current solutions outdated, causing organizations to delay major networking investments until technology standards stabilize.

Edge computing expansion presents substantial growth opportunities as organizations seek to reduce latency and improve application performance. The deployment of edge data centers across Sweden creates demand for specialized networking solutions designed to support distributed computing architectures and real-time data processing requirements.

Artificial intelligence integration offers significant potential for networking solution providers. AI-powered network management tools can optimize performance, predict failures, and automate routine maintenance tasks, creating value-added opportunities for vendors willing to invest in intelligent networking technologies.

Sustainability-focused solutions represent a growing market segment as organizations prioritize environmental responsibility. Networking vendors that develop energy-efficient products and provide comprehensive sustainability reporting capabilities can capture additional market share from environmentally conscious customers.

Industry 4.0 initiatives in Swedish manufacturing create new networking requirements for industrial data centers supporting IoT devices, robotics, and automated production systems. These specialized applications require robust, low-latency networking solutions capable of handling diverse data types and communication protocols.

Competitive dynamics in the Sweden data center networking market are characterized by intense rivalry among established vendors and emerging technology providers. Traditional networking equipment manufacturers face increasing competition from software-defined networking specialists and cloud-native solution providers, driving innovation and competitive pricing strategies.

Technology convergence is reshaping market dynamics as networking, security, and computing functions become increasingly integrated. This convergence creates opportunities for vendors offering comprehensive solutions while challenging traditional product boundaries and vendor relationships.

Customer expectations continue to evolve toward more flexible, scalable, and automated networking solutions. Data center operators demand networking infrastructure that can adapt quickly to changing requirements while minimizing operational complexity and maintenance overhead.

Supply chain considerations have gained prominence following recent global disruptions, with customers prioritizing vendors that can ensure reliable product availability and support services. This focus on supply chain resilience is influencing vendor selection criteria and long-term partnership strategies.

Comprehensive market analysis was conducted using a multi-faceted research approach combining primary and secondary data sources to ensure accuracy and reliability of findings. The methodology incorporated quantitative analysis of market trends, competitive positioning, and technology adoption patterns across the Swedish data center networking landscape.

Primary research activities included structured interviews with key industry stakeholders, including data center operators, networking vendors, system integrators, and end-user organizations. These interviews provided valuable insights into market dynamics, customer requirements, and emerging technology trends shaping the industry.

Secondary research encompassed analysis of industry reports, vendor financial statements, government publications, and technology research studies. This comprehensive data collection approach ensured a thorough understanding of market conditions and competitive dynamics.

Data validation processes were implemented to verify research findings through multiple independent sources and expert consultations. This rigorous validation approach enhances the reliability and credibility of market insights and projections presented in this analysis.

Stockholm region dominates the Swedish data center networking market, accounting for approximately 58% of total market activity. The capital region benefits from excellent connectivity infrastructure, proximity to major enterprises, and favorable government policies supporting technology investments. Major international data center operators have established significant facilities in the Stockholm area, driving substantial demand for advanced networking solutions.

Gothenburg area represents the second-largest market segment, capturing roughly 22% of market share. The region’s strategic location on Sweden’s west coast provides excellent connectivity to European markets, making it an attractive location for data centers serving international customers. The presence of major manufacturing companies also creates demand for industrial data center networking solutions.

Northern Sweden is emerging as a significant growth region, particularly in areas with abundant renewable energy resources and favorable climate conditions for data center cooling. The region’s 15% market share is expected to grow as more hyperscale operators establish facilities to take advantage of low-cost renewable energy and natural cooling capabilities.

Other regions collectively represent the remaining 5% of market activity, primarily consisting of smaller enterprise data centers and edge computing deployments serving local markets. These regions show potential for growth as edge computing requirements expand and 5G networks are deployed nationwide.

Market leadership in the Sweden data center networking sector is characterized by a mix of global technology giants and specialized networking vendors. The competitive environment fosters innovation and drives continuous improvement in product offerings and service capabilities.

By Product Type: The market segmentation reveals distinct categories based on networking equipment and solution types, each serving specific data center requirements and applications.

By End-User Industry: Market segmentation by industry vertical demonstrates diverse application requirements and adoption patterns across different sectors.

High-Performance Computing segment demonstrates exceptional growth potential, driven by increasing demand for AI and machine learning applications requiring specialized networking infrastructure. These applications demand ultra-low latency and high-bandwidth connectivity, creating opportunities for advanced networking solutions.

Software-Defined Networking category shows rapid adoption rates, with 46% of new data center projects incorporating SDN technologies. This trend reflects the industry’s shift toward more flexible, programmable networking architectures that can adapt quickly to changing business requirements.

Network Security segment continues to expand as cyber threats become more sophisticated and frequent. Organizations are investing heavily in integrated security solutions that provide comprehensive protection without compromising network performance or operational efficiency.

Edge Computing category represents the fastest-growing segment, driven by 5G deployment and IoT applications requiring real-time data processing. Edge data centers require specialized networking solutions optimized for distributed architectures and remote management capabilities.

Data Center Operators benefit from advanced networking solutions that improve operational efficiency, reduce energy consumption, and enhance service quality. Modern networking infrastructure enables operators to offer differentiated services while maintaining competitive cost structures and meeting stringent performance requirements.

Enterprise Customers gain access to more reliable, scalable, and secure data center services through improved networking infrastructure. Enhanced networking capabilities enable better application performance, reduced latency, and improved user experiences across various business applications and services.

Technology Vendors can capitalize on growing market demand by developing innovative solutions that address evolving customer requirements. The expanding market provides opportunities for revenue growth, market share expansion, and technology leadership in emerging areas such as AI-powered networking and edge computing.

System Integrators benefit from increased demand for professional services related to network design, implementation, and management. The complexity of modern data center networks creates opportunities for specialized consulting and integration services that add value for end customers.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial Intelligence integration is transforming data center networking through intelligent automation, predictive maintenance, and self-optimizing network configurations. AI-powered networking solutions can automatically adjust performance parameters, detect anomalies, and prevent potential issues before they impact operations.

Sustainability focus continues to intensify, with data center operators implementing comprehensive environmental strategies including energy-efficient networking equipment, renewable energy sourcing, and carbon footprint reduction initiatives. This trend is driving demand for networking solutions that minimize power consumption while maximizing performance.

Edge computing proliferation is creating new networking requirements as applications move closer to end-users and data sources. Edge data centers require networking solutions optimized for distributed architectures, remote management, and integration with centralized cloud infrastructure.

Network automation advancement is reducing operational complexity and improving efficiency through software-defined networking, intent-based networking, and automated configuration management. These technologies enable data center operators to manage increasingly complex networks with fewer manual interventions.

Security integration is becoming more sophisticated as networking and security functions converge into unified platforms. Modern data center networks incorporate advanced threat detection, automated response capabilities, and comprehensive security analytics to protect against evolving cyber threats.

Major infrastructure investments by international technology companies have significantly expanded Sweden’s data center capacity and created substantial demand for advanced networking solutions. These investments demonstrate confidence in Sweden’s long-term potential as a data center hub and drive continuous market growth.

5G network deployment across Sweden is creating new opportunities for edge computing and mobile edge networking solutions. Telecommunications operators are investing heavily in infrastructure upgrades that require sophisticated data center networking capabilities to support next-generation services.

Government digitalization initiatives are accelerating public sector adoption of cloud services and digital platforms, creating additional demand for secure, reliable data center networking infrastructure. These initiatives support broader digital transformation objectives and stimulate market growth.

Sustainability certifications and environmental standards are becoming increasingly important for data center operations, influencing networking equipment selection and operational practices. Industry organizations are developing comprehensive sustainability frameworks that guide technology choices and operational procedures.

Strategic partnerships between networking vendors and data center operators are fostering innovation and accelerating technology adoption. These collaborations enable rapid deployment of cutting-edge solutions and create competitive advantages for participating organizations.

MarkWide Research recommends that data center operators prioritize networking solutions that offer both immediate performance benefits and long-term scalability. The rapid evolution of applications and services requires networking infrastructure that can adapt to changing requirements without major architectural overhauls.

Investment focus should emphasize software-defined networking technologies that provide flexibility and automation capabilities. These solutions enable more efficient resource utilization and reduce operational complexity, delivering both cost savings and improved service quality.

Sustainability considerations should be integrated into all networking infrastructure decisions, as environmental responsibility becomes increasingly important for customer attraction and regulatory compliance. Energy-efficient networking solutions provide both operational cost benefits and competitive advantages.

Skills development programs should be implemented to address the shortage of qualified networking professionals. Organizations that invest in training and development will be better positioned to leverage advanced networking technologies and maintain competitive advantages.

Strategic partnerships with technology vendors can provide access to cutting-edge solutions and specialized expertise. Collaborative relationships enable faster technology adoption and more effective implementation of complex networking projects.

Market growth prospects remain highly positive, with continued expansion expected across all major segments of the Sweden data center networking market. The combination of favorable market conditions, technological advancement, and strong customer demand creates a robust foundation for sustained growth over the forecast period.

Technology evolution will continue to drive market transformation, with emerging technologies such as quantum networking, advanced AI integration, and next-generation security solutions creating new opportunities and challenges. Organizations that stay ahead of technological trends will be best positioned to capitalize on future market developments.

Sustainability leadership will become increasingly important as global environmental concerns intensify and regulatory requirements evolve. Swedish data centers’ renewable energy advantages position them well to meet growing demand for environmentally responsible technology services.

Market consolidation may occur as smaller players struggle to compete with larger organizations that can invest in advanced technologies and comprehensive service offerings. This consolidation could create opportunities for strategic acquisitions and partnerships that strengthen market positions.

International expansion opportunities will continue to develop as Swedish data center operators leverage their expertise and environmental advantages to serve broader European and global markets. The projected growth rate of 8.2% CAGR reflects strong underlying demand and favorable market conditions supporting continued expansion.

Sweden’s data center networking market represents a dynamic and rapidly evolving sector with exceptional growth potential driven by favorable market conditions, technological innovation, and strong customer demand. The market benefits from Sweden’s unique advantages in renewable energy, political stability, and advanced infrastructure, positioning it as a leading destination for data center investments and networking technology deployment.

Key success factors for market participants include embracing sustainability initiatives, investing in advanced technologies such as software-defined networking and AI-powered solutions, and developing strategic partnerships that enhance competitive capabilities. The market’s evolution toward more automated, intelligent, and environmentally responsible networking solutions creates opportunities for organizations willing to innovate and adapt to changing requirements.

Future market development will be shaped by continued technological advancement, increasing sustainability focus, and growing demand for edge computing and 5G-enabled services. Organizations that position themselves effectively to capitalize on these trends while addressing market challenges such as skills shortages and regulatory compliance will be best positioned for long-term success in this dynamic and promising market.

What is Data Center Networking?

Data Center Networking refers to the technologies and solutions that facilitate communication and data transfer within and between data centers. This includes hardware and software components such as switches, routers, and network management tools that ensure efficient data flow and connectivity.

What are the key players in the Sweden Data Center Networking Market?

Key players in the Sweden Data Center Networking Market include companies like Cisco Systems, Arista Networks, and Juniper Networks, which provide a range of networking solutions for data centers. These companies focus on enhancing network performance, scalability, and security, among others.

What are the main drivers of growth in the Sweden Data Center Networking Market?

The main drivers of growth in the Sweden Data Center Networking Market include the increasing demand for cloud services, the rise of big data analytics, and the need for enhanced network security. Additionally, the expansion of IoT applications is also contributing to market growth.

What challenges does the Sweden Data Center Networking Market face?

The Sweden Data Center Networking Market faces challenges such as the high cost of advanced networking equipment and the complexity of network management. Additionally, the rapid pace of technological change can make it difficult for companies to keep up with the latest innovations.

What opportunities exist in the Sweden Data Center Networking Market?

Opportunities in the Sweden Data Center Networking Market include the growing adoption of software-defined networking (SDN) and network function virtualization (NFV). These technologies offer improved flexibility and efficiency, making them attractive to data center operators.

What trends are shaping the Sweden Data Center Networking Market?

Trends shaping the Sweden Data Center Networking Market include the shift towards automation and AI-driven network management, as well as the increasing focus on energy efficiency and sustainability. Additionally, the integration of edge computing is becoming more prevalent in data center networking strategies.

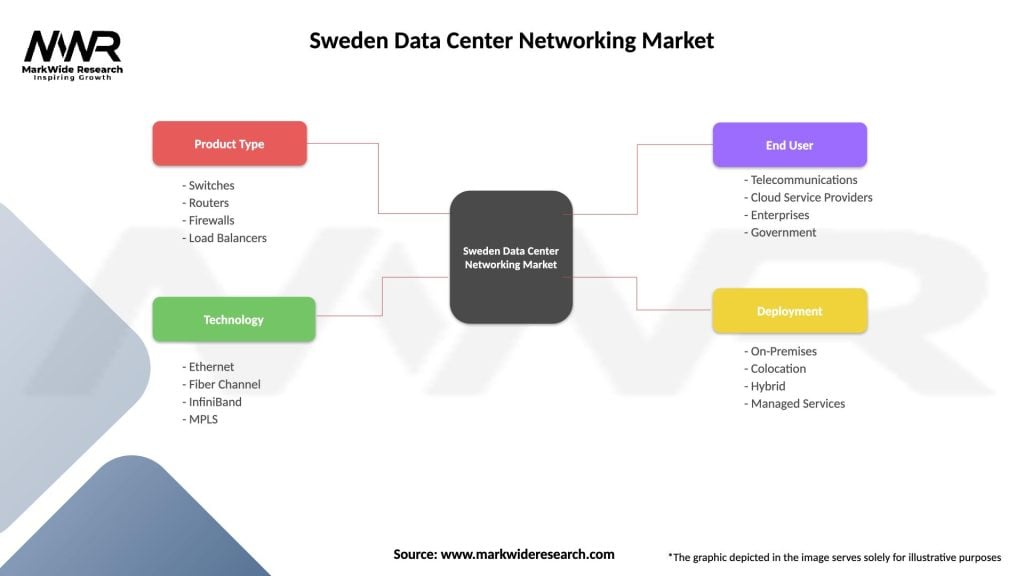

Sweden Data Center Networking Market

| Segmentation Details | Description |

|---|---|

| Product Type | Switches, Routers, Firewalls, Load Balancers |

| Technology | Ethernet, Fiber Channel, InfiniBand, MPLS |

| End User | Telecommunications, Cloud Service Providers, Enterprises, Government |

| Deployment | On-Premises, Colocation, Hybrid, Managed Services |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Sweden Data Center Networking Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.