444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Spain smart home market represents one of Europe’s most dynamic and rapidly evolving technology sectors, characterized by increasing consumer adoption of connected devices and intelligent home automation systems. Spanish households are experiencing a significant transformation as traditional homes evolve into interconnected ecosystems powered by Internet of Things (IoT) technology, artificial intelligence, and advanced connectivity solutions.

Market dynamics in Spain reflect a growing consumer preference for energy-efficient solutions, enhanced security systems, and convenient lifestyle technologies. The market encompasses various product categories including smart lighting, intelligent thermostats, security cameras, voice assistants, smart appliances, and comprehensive home automation platforms. Consumer adoption rates have accelerated significantly, with penetration reaching approximately 32% of Spanish households actively using at least one smart home device.

Regional variations across Spain demonstrate distinct adoption patterns, with metropolitan areas like Madrid, Barcelona, and Valencia leading in smart home technology integration. The market benefits from robust telecommunications infrastructure, government initiatives promoting digital transformation, and increasing awareness of energy conservation benefits. Growth projections indicate the Spanish smart home sector will expand at a compound annual growth rate (CAGR) of 18.5% through the forecast period, driven by technological advancements and changing consumer lifestyles.

The Spain smart home market refers to the comprehensive ecosystem of connected devices, intelligent systems, and automated technologies designed to enhance residential living experiences through digital integration and remote control capabilities. This market encompasses hardware components, software platforms, installation services, and ongoing support systems that enable homeowners to monitor, control, and optimize various aspects of their living environments.

Smart home technology in Spain includes interconnected devices that communicate through wireless networks, enabling centralized control via smartphones, tablets, or voice commands. These systems integrate lighting control, climate management, security monitoring, entertainment systems, and energy management solutions into unified platforms that learn user preferences and adapt automatically to household routines.

Market scope extends beyond individual device sales to include comprehensive home automation solutions, professional installation services, cloud-based management platforms, and subscription-based monitoring services. The Spanish market particularly emphasizes energy efficiency, security enhancement, and convenience features that align with European Union sustainability directives and local consumer preferences for technology-driven lifestyle improvements.

Spain’s smart home market demonstrates exceptional growth momentum, positioning itself as a leading European market for residential automation and connected device adoption. The sector benefits from strong government support for digital transformation initiatives, robust telecommunications infrastructure, and increasing consumer awareness of smart home benefits including energy savings, enhanced security, and improved quality of life.

Key market segments show varied growth patterns, with security systems and energy management solutions leading adoption rates. Smart lighting represents the most penetrated category, present in approximately 45% of connected Spanish homes, followed by intelligent thermostats and security cameras. The market structure includes both international technology giants and emerging Spanish companies developing localized solutions for domestic consumers.

Consumer behavior analysis reveals strong preference for integrated solutions over standalone devices, with 68% of Spanish smart home users expressing interest in comprehensive automation platforms. Price sensitivity remains a consideration, though willingness to invest in energy-saving technologies has increased significantly following recent energy cost fluctuations and environmental awareness campaigns.

Future market trajectory indicates continued expansion across all product categories, with particular growth expected in artificial intelligence-powered systems, voice control interfaces, and integrated renewable energy management solutions. The market’s evolution reflects broader European trends toward sustainable living and digital lifestyle integration.

Strategic market insights reveal several critical factors driving Spain’s smart home market development and shaping future growth opportunities:

Primary market drivers propelling Spain’s smart home market expansion include technological advancement, changing consumer lifestyles, and supportive regulatory environments that encourage digital transformation and energy efficiency improvements.

Energy cost concerns represent a fundamental driver, as Spanish households seek solutions to manage rising utility expenses through intelligent consumption monitoring and automated optimization systems. Smart thermostats and energy management platforms enable users to achieve significant cost reductions while maintaining comfort levels, creating compelling value propositions for technology adoption.

Government initiatives supporting digital transformation and sustainability goals provide additional market momentum. Spanish authorities promote smart home technology through incentive programs, building code updates, and public awareness campaigns highlighting environmental benefits. These policies align with European Union directives on energy efficiency and carbon emission reduction targets.

Telecommunications infrastructure improvements, including widespread 5G deployment and fiber optic network expansion, enable more sophisticated smart home applications requiring high-speed, low-latency connectivity. Enhanced network capabilities support real-time device communication, cloud-based processing, and advanced features like video streaming and artificial intelligence integration.

Demographic shifts toward younger, technology-savvy homeowners drive market demand as millennials and Generation Z consumers prioritize connected living experiences. These demographics demonstrate higher willingness to invest in smart home technology and integrate digital solutions into daily routines, creating sustainable market growth foundations.

Market restraints affecting Spain’s smart home sector include cost considerations, technical complexity, privacy concerns, and interoperability challenges that may limit adoption rates among certain consumer segments.

Initial investment costs remain a significant barrier for many Spanish households, particularly for comprehensive automation systems requiring multiple devices and professional installation. While individual smart devices have become more affordable, complete home automation solutions still represent substantial upfront investments that may deter price-sensitive consumers.

Technical complexity associated with system setup, configuration, and ongoing maintenance creates adoption hesitancy among less tech-savvy consumers. Many potential users express concerns about their ability to properly install, configure, and troubleshoot smart home systems without professional assistance, limiting market penetration in certain demographic segments.

Privacy and security concerns regarding data collection, storage, and potential unauthorized access to home systems influence consumer decision-making. Spanish consumers demonstrate increasing awareness of cybersecurity risks associated with connected devices, leading to careful evaluation of manufacturer security practices and data handling policies.

Interoperability challenges between different manufacturers’ devices and platforms create fragmentation concerns for consumers seeking integrated solutions. Lack of universal standards may result in compatibility issues, limiting system expansion possibilities and creating vendor lock-in situations that reduce consumer confidence in long-term investments.

Significant market opportunities exist within Spain’s smart home sector, driven by emerging technologies, evolving consumer needs, and supportive market conditions that favor continued expansion and innovation.

Artificial intelligence integration presents substantial opportunities for developing more sophisticated automation systems that learn user preferences and optimize home operations automatically. AI-powered solutions can enhance energy efficiency, improve security responses, and provide personalized experiences that differentiate products in competitive markets.

Renewable energy integration opportunities align with Spain’s strong solar energy potential and government sustainability initiatives. Smart home systems that optimize solar panel output, manage battery storage, and coordinate with grid systems can provide compelling value propositions while supporting national renewable energy goals.

Aging population services represent an emerging opportunity as Spain’s demographic profile shifts toward older residents who may benefit from smart home technologies designed for health monitoring, emergency response, and independent living support. These applications can address growing healthcare costs while improving quality of life for elderly residents.

Small and medium enterprise (SME) market expansion opportunities exist as smart home technologies adapt for small business applications including retail stores, restaurants, and professional offices. These markets may adopt residential-grade smart technologies for cost-effective automation and monitoring solutions.

Service sector development opportunities include installation, maintenance, monitoring, and consulting services that support smart home adoption. Professional service providers can address technical complexity barriers while creating recurring revenue streams through ongoing support and system optimization services.

Market dynamics within Spain’s smart home sector reflect complex interactions between technological advancement, consumer behavior evolution, competitive pressures, and regulatory influences that shape market development patterns and growth trajectories.

Supply chain dynamics demonstrate increasing localization as European manufacturers establish regional production and distribution capabilities to serve Spanish markets more effectively. This trend reduces dependency on Asian suppliers while improving delivery times and customer service quality, though it may impact pricing structures in certain product categories.

Competitive dynamics intensify as traditional electronics manufacturers, telecommunications companies, and technology startups compete for market share through product differentiation, pricing strategies, and partnership development. Market consolidation trends indicate larger companies acquiring specialized smart home technology firms to expand product portfolios and technical capabilities.

Consumer behavior dynamics show evolution from early adopter enthusiasm toward mainstream acceptance, with purchasing decisions increasingly influenced by practical benefits rather than novelty factors. This shift demands more sophisticated value propositions emphasizing tangible returns on investment, reliability, and long-term support.

Technology dynamics accelerate as 5G networks, edge computing, and artificial intelligence capabilities enable more advanced smart home applications. These technological improvements create opportunities for enhanced functionality while potentially obsoleting older systems, requiring careful product lifecycle management strategies.

Comprehensive research methodology employed for analyzing Spain’s smart home market incorporates multiple data collection approaches, analytical frameworks, and validation processes to ensure accurate market assessment and reliable forecasting.

Primary research activities include structured interviews with industry executives, technology manufacturers, distribution partners, installation service providers, and end-user consumers across major Spanish metropolitan areas. These interviews provide qualitative insights into market trends, competitive dynamics, consumer preferences, and emerging opportunities that quantitative data alone cannot capture.

Secondary research sources encompass industry reports, government statistics, trade association publications, patent filings, and company financial disclosures that provide quantitative market data and historical trend analysis. This information establishes baseline market conditions and enables trend projection modeling for future market scenarios.

Market sizing methodology utilizes bottom-up analysis combining product category sales data, adoption rate surveys, and demographic analysis to estimate total addressable market and serviceable addressable market segments. Cross-validation through top-down analysis ensures consistency and accuracy in market size calculations.

Forecasting models incorporate multiple variables including economic indicators, technology adoption curves, demographic trends, and regulatory policy impacts to project market growth scenarios. Sensitivity analysis testing validates forecast reliability under different assumption sets, providing confidence intervals for projected outcomes.

Regional market analysis reveals significant variations in smart home adoption patterns across Spain’s autonomous communities, reflecting differences in economic development, demographic profiles, housing characteristics, and local market conditions.

Madrid region leads national smart home adoption with approximately 42% household penetration, driven by high disposable incomes, technology-forward demographics, and extensive telecommunications infrastructure. The capital region demonstrates strong demand for comprehensive automation systems and premium smart home solutions, making it a primary market for international technology companies entering Spain.

Catalonia region, centered around Barcelona, represents the second-largest smart home market with 38% adoption rates and particular strength in energy management solutions. The region’s focus on sustainability and innovation creates favorable conditions for smart home technologies that deliver environmental benefits alongside convenience features.

Valencia and Andalusia regions show growing smart home markets with adoption rates reaching 29% and 26% respectively, driven by tourism industry influence and increasing urbanization. These regions demonstrate strong interest in security systems and climate control solutions that address local environmental conditions and lifestyle preferences.

Northern regions including Basque Country and Galicia exhibit more conservative adoption patterns but show accelerating growth in energy efficiency applications. These markets prioritize practical benefits over convenience features, creating opportunities for solutions that deliver measurable utility cost reductions and environmental improvements.

Competitive landscape within Spain’s smart home market features diverse participants ranging from global technology giants to specialized local companies, creating dynamic market conditions with varied competitive strategies and positioning approaches.

Market positioning strategies vary significantly among competitors, with some emphasizing ecosystem integration while others focus on specialized product excellence. Price competition intensifies in commodity categories like smart bulbs and basic sensors, while premium segments maintain higher margins through advanced features and professional service offerings.

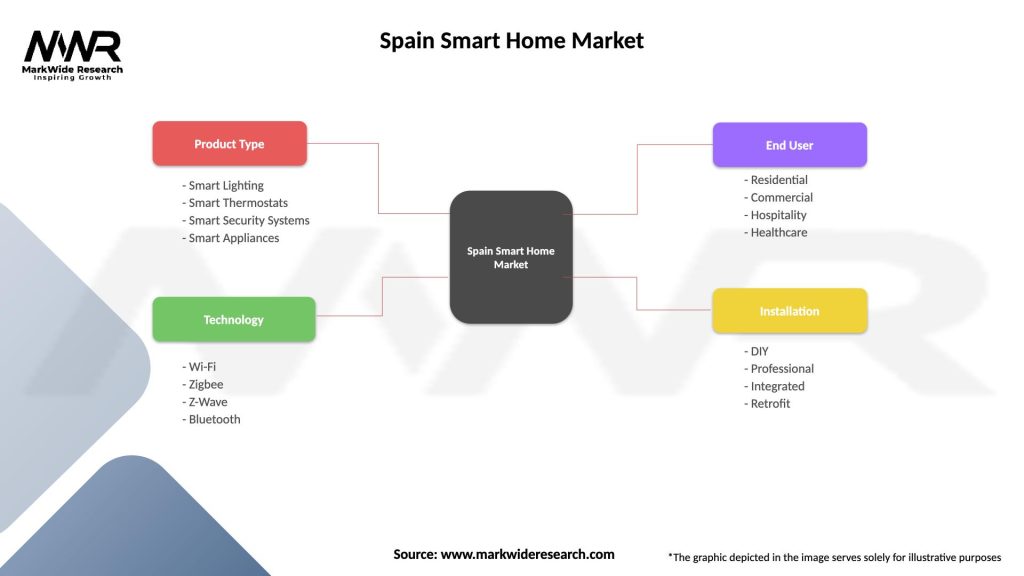

Market segmentation analysis reveals distinct categories within Spain’s smart home market, each characterized by unique growth patterns, consumer preferences, and competitive dynamics that influence strategic positioning and investment decisions.

By Product Category:

By Technology Platform:

By End-User Segment:

Smart lighting category maintains market leadership through combination of affordability, ease of installation, and immediate user benefits. LED smart bulbs represent the most accessible entry point for smart home adoption, with Spanish consumers appreciating energy savings and customization capabilities. Advanced lighting systems incorporating circadian rhythm optimization and integration with other smart home devices show growing adoption among premium market segments.

Security systems category demonstrates exceptional growth momentum driven by urbanization trends and increasing security awareness. Video doorbells and security cameras lead adoption within this segment, offering immediate security benefits and remote monitoring capabilities that appeal to Spanish homeowners. Professional monitoring services show strong acceptance rates, creating recurring revenue opportunities for service providers.

Climate control category benefits from Spain’s diverse climate conditions and energy cost concerns, with smart thermostats delivering measurable utility savings. Zoned heating and cooling systems gain popularity in larger homes, while simple programmable thermostats serve entry-level market segments. Integration with renewable energy systems creates additional value propositions for environmentally conscious consumers.

Entertainment systems category evolves rapidly with streaming service integration and voice control capabilities driving adoption. Smart speakers and displays serve as central control hubs while providing entertainment value, making them attractive gateway devices for broader smart home adoption. Multi-room audio systems appeal to premium market segments seeking comprehensive entertainment solutions.

Smart appliances category shows emerging growth as replacement cycles drive adoption of connected refrigerators, washing machines, and kitchen appliances. Energy monitoring capabilities and remote control features provide practical benefits that justify premium pricing for technology-enhanced appliances.

Manufacturers and technology companies benefit from Spain’s smart home market through access to sophisticated European consumers willing to invest in premium technology solutions. The market provides opportunities for product differentiation, premium pricing strategies, and development of localized solutions that address specific Spanish consumer preferences and regulatory requirements.

Retailers and distribution partners gain advantages through expanding product categories, higher-margin technology sales, and opportunities for value-added services including installation and technical support. Smart home products typically generate higher revenues per square foot compared to traditional electronics, improving overall retail profitability.

Service providers and installers benefit from growing demand for professional installation, system integration, and ongoing maintenance services. The technical complexity of comprehensive smart home systems creates sustainable competitive advantages for companies developing specialized expertise and certification programs.

Telecommunications companies leverage smart home adoption to increase broadband service value propositions, reduce customer churn, and develop new revenue streams through device sales and managed services. Smart home applications drive increased bandwidth consumption, supporting premium service tier adoption.

Energy utilities benefit from smart home technologies that enable demand response programs, peak load management, and grid optimization initiatives. Smart meters and energy management systems provide valuable consumption data while supporting renewable energy integration and grid stability objectives.

Real estate developers and property managers use smart home features as differentiation tools in competitive markets, potentially commanding premium pricing and faster sales cycles. Smart home integration can reduce property management costs while improving tenant satisfaction and retention rates.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial intelligence integration emerges as a dominant trend transforming Spain’s smart home market through machine learning algorithms that optimize energy consumption, predict maintenance needs, and personalize user experiences. AI-powered systems learn household patterns and automatically adjust settings to maximize efficiency while maintaining comfort levels, creating compelling value propositions for energy-conscious Spanish consumers.

Voice control adoption accelerates rapidly as Spanish-language support improves and consumers become comfortable with voice-activated home automation. Natural language processing advances enable more sophisticated voice commands and conversational interactions, making smart home control more intuitive and accessible to diverse demographic groups.

Energy management focus intensifies as utility costs rise and environmental awareness increases among Spanish households. Smart energy systems that integrate solar panels, battery storage, and intelligent load management gain popularity, particularly in regions with high solar potential and supportive renewable energy policies.

Professional installation services show growing demand as consumers seek reliable system setup and ongoing support for complex smart home installations. Certified installer networks develop to address technical complexity concerns while ensuring proper system configuration and optimal performance.

Subscription service models gain acceptance as consumers appreciate ongoing software updates, cloud storage, and professional monitoring services. Monthly service fees provide predictable revenue streams for companies while ensuring continuous system optimization and security updates for consumers.

Interoperability standards receive increased attention as consumers demand seamless integration between devices from different manufacturers. Matter protocol adoption and other universal standards initiatives aim to address fragmentation concerns and improve consumer confidence in smart home investments.

Recent industry developments within Spain’s smart home market demonstrate accelerating innovation, strategic partnerships, and market expansion initiatives that shape competitive dynamics and growth opportunities.

Major telecommunications providers expand smart home service offerings through partnerships with device manufacturers and development of integrated platforms that combine connectivity, devices, and professional services. These initiatives aim to increase customer lifetime value while reducing churn in competitive broadband markets.

Retail distribution expansion occurs as traditional electronics retailers, home improvement stores, and online platforms increase smart home product selections and develop specialized sales expertise. Demonstration areas and experience centers help consumers understand smart home benefits and overcome technical complexity concerns.

Government incentive programs launch to promote energy-efficient smart home technologies as part of broader sustainability and digital transformation initiatives. These programs provide financial incentives for smart thermostat installations, energy monitoring systems, and renewable energy integration solutions.

Local startup ecosystem development accelerates as Spanish entrepreneurs identify market opportunities for specialized smart home solutions addressing local consumer needs and preferences. Innovation hubs and accelerator programs support technology development while attracting international investment in Spanish smart home companies.

Security and privacy enhancements receive increased attention as manufacturers implement stronger encryption, local data processing, and transparent privacy policies to address consumer concerns about connected device security risks.

Market entry strategies for companies targeting Spain’s smart home market should prioritize localization efforts including Spanish-language support, local customer service capabilities, and partnerships with established distribution channels. MarkWide Research analysis indicates that companies demonstrating commitment to Spanish market needs achieve higher adoption rates and customer satisfaction scores.

Product development focus should emphasize energy efficiency features, security applications, and ease of installation to address primary Spanish consumer concerns. Value proposition communication must clearly articulate tangible benefits including utility cost savings, security improvements, and convenience enhancements rather than focusing solely on technological sophistication.

Distribution strategy optimization requires multi-channel approaches combining online sales, traditional retail partnerships, and professional installer networks. Consumer education initiatives through demonstration centers, educational content, and hands-on experiences help overcome technical complexity barriers and accelerate adoption decisions.

Pricing strategies should consider Spanish consumer price sensitivity while maintaining adequate margins for sustainable business growth. Financing options and subscription models may improve accessibility for price-conscious consumers while creating recurring revenue opportunities for manufacturers and service providers.

Partnership development with local telecommunications companies, energy utilities, and security service providers can accelerate market penetration while providing credible third-party endorsements for smart home solutions. These partnerships also enable integrated service offerings that address multiple consumer needs through single vendor relationships.

Future market trajectory for Spain’s smart home sector indicates continued robust growth driven by technological advancement, changing consumer lifestyles, and supportive market conditions that favor widespread adoption across demographic segments.

Technology evolution will enable more sophisticated applications including predictive maintenance, health monitoring, and autonomous home management systems that require minimal user intervention. 5G network deployment and edge computing capabilities will support real-time processing and advanced artificial intelligence applications that enhance smart home functionality and user experiences.

Market maturation patterns suggest evolution from early adopter enthusiasm toward mainstream acceptance, with purchasing decisions increasingly influenced by practical benefits and return on investment considerations. Consumer expectations will shift toward seamless integration, reliable performance, and comprehensive support services rather than novelty features alone.

Industry consolidation trends may accelerate as larger companies acquire specialized technology firms to expand product portfolios and technical capabilities. This consolidation could improve interoperability while potentially reducing innovation diversity in certain market segments.

Regulatory developments will likely address privacy protection, cybersecurity standards, and energy efficiency requirements that influence product design and market positioning strategies. European Union initiatives promoting digital transformation and sustainability will continue supporting smart home adoption through policy frameworks and incentive programs.

Market penetration projections indicate Spanish household adoption could reach 55-60% by 2028, driven by declining device costs, improved user experiences, and growing awareness of smart home benefits. This growth will create substantial opportunities for manufacturers, service providers, and technology companies committed to Spanish market development.

Spain’s smart home market represents a compelling growth opportunity characterized by favorable demographic trends, supportive government policies, and increasing consumer acceptance of connected home technologies. The market demonstrates strong fundamentals including robust telecommunications infrastructure, growing environmental awareness, and rising energy costs that create compelling value propositions for smart home solutions.

Market dynamics indicate continued expansion across all product categories, with particular strength in energy management, security systems, and integrated automation platforms. Consumer behavior evolution from early adopter enthusiasm toward mainstream acceptance creates opportunities for companies that prioritize practical benefits, reliable performance, and comprehensive support services over technological novelty alone.

Competitive landscape development will likely favor companies that successfully balance global technology capabilities with local market understanding, Spanish-language support, and partnerships with established distribution channels. Success factors include clear value proposition communication, competitive pricing strategies, and commitment to ongoing customer support and system optimization services.

Future market potential remains substantial as technological advancement, demographic shifts, and policy support continue driving smart home adoption throughout Spain. Companies that establish strong market positions during this growth phase will benefit from first-mover advantages and customer loyalty as the market matures toward widespread mainstream adoption across Spanish households.

What is Smart Home?

Smart Home refers to a residential setup where appliances and devices are interconnected and can be controlled remotely, enhancing convenience, security, and energy efficiency. This includes systems like smart lighting, thermostats, and security cameras.

What are the key players in the Spain Smart Home Market?

Key players in the Spain Smart Home Market include companies like Amazon, Google, and Philips, which offer a range of smart home devices and solutions. These companies are known for their innovative technologies and extensive product lines, among others.

What are the main drivers of growth in the Spain Smart Home Market?

The main drivers of growth in the Spain Smart Home Market include increasing consumer demand for energy-efficient solutions, advancements in IoT technology, and the rising trend of home automation. Additionally, the growing awareness of home security is propelling market expansion.

What challenges does the Spain Smart Home Market face?

The Spain Smart Home Market faces challenges such as concerns over data privacy and security, high installation costs, and the complexity of integrating various devices. These factors can hinder consumer adoption and market growth.

What opportunities exist in the Spain Smart Home Market?

Opportunities in the Spain Smart Home Market include the potential for growth in smart energy management systems, increased demand for home security solutions, and the expansion of smart appliances. As technology evolves, new applications and services are likely to emerge.

What trends are shaping the Spain Smart Home Market?

Trends shaping the Spain Smart Home Market include the rise of voice-activated devices, the integration of AI for enhanced automation, and a growing focus on sustainability in smart home products. These trends are influencing consumer preferences and driving innovation.

Spain Smart Home Market

| Segmentation Details | Description |

|---|---|

| Product Type | Smart Lighting, Smart Thermostats, Smart Security Systems, Smart Appliances |

| Technology | Wi-Fi, Zigbee, Z-Wave, Bluetooth |

| End User | Residential, Commercial, Hospitality, Healthcare |

| Installation | DIY, Professional, Integrated, Retrofit |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Spain Smart Home Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.