444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Spain plastic packaging films market represents a dynamic and rapidly evolving sector within the country’s broader packaging industry landscape. Market dynamics indicate substantial growth potential driven by increasing consumer demand for convenient packaging solutions across multiple industries including food and beverage, pharmaceuticals, personal care, and industrial applications. The market demonstrates robust expansion with projected growth rates of 6.2% CAGR over the forecast period, reflecting Spain’s position as a key manufacturing hub in Southern Europe.

Industry transformation is being driven by technological advancements in film manufacturing processes, sustainability initiatives, and evolving consumer preferences for flexible packaging solutions. The Spanish market benefits from its strategic location, providing access to both European and North African markets, while domestic consumption continues to grow across various end-use sectors. Manufacturing capabilities have expanded significantly, with local producers investing in advanced extrusion technologies and multi-layer film production facilities.

Regional distribution shows concentrated activity in industrial centers including Catalonia, Madrid, and Valencia, where major packaging manufacturers have established production facilities. The market encompasses various film types including polyethylene, polypropylene, polyester, and specialty barrier films, each serving specific application requirements. Innovation trends focus on developing sustainable alternatives, improving barrier properties, and enhancing recyclability to meet evolving regulatory requirements and consumer expectations.

The Spain plastic packaging films market refers to the comprehensive ecosystem of manufacturing, distribution, and consumption of flexible plastic films used for packaging applications across various industries within Spanish territory. These films encompass a wide range of polymer-based materials including polyethylene, polypropylene, polyester, and specialty multilayer structures designed to protect, preserve, and present products effectively.

Market scope includes various film categories such as shrink films, stretch films, barrier films, and specialty functional films used in applications ranging from food packaging to industrial wrapping. The definition encompasses both domestic production capabilities and import activities that serve the Spanish market demand. Value chain participants include raw material suppliers, film manufacturers, converters, brand owners, and end consumers, creating a complex network of interdependent relationships.

Technological aspects involve advanced manufacturing processes including blown film extrusion, cast film production, and specialized coating techniques that enhance film properties. The market definition also includes emerging sustainable alternatives such as bio-based films and recyclable formulations that address environmental concerns while maintaining performance standards required by various applications.

Strategic analysis reveals that Spain’s plastic packaging films market is experiencing significant transformation driven by sustainability mandates, technological innovation, and changing consumer behaviors. The market demonstrates strong growth momentum with increasing adoption of flexible packaging solutions across multiple sectors, particularly in food and beverage applications where convenience and shelf-life extension are critical factors.

Key market drivers include the growing e-commerce sector, which has increased demand for protective packaging films by 34% annually, and the food industry’s shift toward flexible packaging formats that offer superior barrier properties and reduced material usage. Sustainability initiatives are reshaping market dynamics as manufacturers invest in recyclable and bio-based film alternatives to meet circular economy objectives.

Competitive landscape features both international players and domestic manufacturers competing on innovation, sustainability, and cost-effectiveness. Market consolidation trends are evident as companies seek to achieve economies of scale and expand their technological capabilities. Future prospects indicate continued growth supported by infrastructure development, regulatory support for sustainable packaging, and increasing industrial automation that drives demand for specialized packaging films.

Market intelligence reveals several critical insights that define the current state and future trajectory of Spain’s plastic packaging films sector:

Primary growth catalysts propelling the Spain plastic packaging films market include the accelerating shift toward flexible packaging solutions across multiple industries. Food industry transformation represents the most significant driver, as manufacturers increasingly adopt flexible films to extend product shelf life, reduce packaging weight, and improve consumer convenience. The sector benefits from Spain’s strong agricultural base and food processing industry, which generates substantial demand for protective packaging solutions.

E-commerce expansion has emerged as a critical market driver, with online retail growth creating unprecedented demand for protective packaging films. Consumer behavior changes toward online shopping have increased requirements for durable, lightweight packaging that can withstand shipping stresses while maintaining product integrity. This trend has driven innovation in puncture-resistant and tear-resistant film formulations.

Sustainability mandates from both regulatory bodies and consumer preferences are driving investment in eco-friendly film alternatives. Circular economy initiatives supported by Spanish and European Union policies are encouraging development of recyclable and bio-based packaging films. Manufacturing efficiency improvements through automation and advanced process control systems are reducing production costs and improving product consistency, making flexible packaging more competitive against rigid alternatives.

Industrial automation across various sectors is increasing demand for specialized packaging films used in automated packaging lines. Pharmaceutical industry growth in Spain is generating demand for high-barrier films that provide superior protection for sensitive medical products and comply with stringent regulatory requirements.

Significant challenges facing the Spain plastic packaging films market include increasing environmental concerns and regulatory pressures targeting single-use plastics. Legislative restrictions on certain plastic packaging applications are creating compliance costs and forcing manufacturers to invest in alternative materials and technologies. Public perception issues regarding plastic waste and marine pollution are influencing consumer preferences and corporate sustainability policies.

Raw material volatility presents ongoing challenges as petroleum-based polymer prices fluctuate based on global oil markets and supply chain disruptions. Cost pressures from rising energy prices and transportation costs are impacting manufacturing economics and forcing companies to optimize operations and seek efficiency improvements. Competition from alternative packaging materials including paper, metal, and glass is intensifying in certain applications.

Technical limitations of current recycling infrastructure restrict the circular economy potential of plastic films, creating challenges for manufacturers seeking to develop fully recyclable products. Quality consistency requirements from brand owners and regulatory bodies demand significant investments in quality control systems and process monitoring technologies. Labor shortages in manufacturing sectors are affecting production capacity and driving automation investments.

International competition from low-cost producers in emerging markets creates pricing pressures on domestic manufacturers. Technology transition costs associated with adopting sustainable alternatives and advanced manufacturing processes require substantial capital investments that may strain smaller market participants.

Emerging opportunities in the Spain plastic packaging films market center around sustainable innovation and advanced functionality development. Bio-based film development represents a significant growth opportunity as companies invest in plant-based polymers and biodegradable formulations that meet performance requirements while addressing environmental concerns. Research partnerships with universities and technology institutes are accelerating breakthrough developments in this area.

Smart packaging integration offers substantial potential as Internet of Things (IoT) technologies enable development of intelligent films with embedded sensors for temperature monitoring, freshness indication, and supply chain tracking. Active packaging solutions incorporating antimicrobial properties and oxygen scavenging capabilities are creating new market segments in food and pharmaceutical applications.

Export market expansion presents opportunities for Spanish manufacturers to leverage their technological capabilities and strategic location to serve North African and Latin American markets. Circular economy initiatives supported by government incentives are creating opportunities for companies developing closed-loop recycling systems and take-back programs for used packaging films.

Specialty applications in agriculture, construction, and industrial sectors offer higher-margin opportunities for manufacturers capable of developing customized solutions. Digital printing compatibility is creating opportunities for films that support high-quality graphics and variable data printing for personalized packaging applications. Barrier technology advancement enables development of ultra-thin films with superior protection properties, reducing material usage while maintaining performance.

Complex interactions between supply and demand factors are shaping the Spain plastic packaging films market landscape. Demand dynamics reflect changing consumer preferences toward convenience packaging, sustainability requirements, and performance expectations across various applications. Supply-side factors include manufacturing capacity expansion, technology adoption rates, and raw material availability that influence market equilibrium.

Price dynamics are influenced by raw material costs, energy prices, and competitive pressures from both domestic and international suppliers. Innovation cycles drive market evolution as new technologies enable improved performance characteristics and sustainable alternatives. Regulatory dynamics create both challenges and opportunities as environmental policies shape market requirements and investment priorities.

Competitive dynamics involve ongoing consolidation trends, strategic partnerships, and technology licensing agreements that reshape market structure. Customer dynamics reflect evolving requirements from brand owners seeking differentiated packaging solutions that enhance product appeal and meet sustainability objectives. According to MarkWide Research analysis, market efficiency improvements of 23% annually are being achieved through advanced manufacturing technologies and process optimization.

Investment dynamics show increasing capital allocation toward sustainable technologies and automation systems that improve operational efficiency. Trade dynamics are influenced by international agreements, tariff policies, and currency fluctuations that affect import-export balances and competitive positioning in global markets.

Comprehensive research approach employed for analyzing the Spain plastic packaging films market combines primary and secondary research methodologies to ensure data accuracy and market insight reliability. Primary research includes structured interviews with industry executives, manufacturing specialists, technology providers, and end-user representatives across various sectors including food and beverage, pharmaceuticals, and industrial applications.

Secondary research encompasses analysis of industry reports, government statistics, trade association data, and academic publications to establish market context and validate primary findings. Data triangulation methods ensure consistency across multiple information sources and enhance the reliability of market projections and trend analysis.

Market sizing methodology utilizes bottom-up and top-down approaches to establish comprehensive market scope and segmentation analysis. Quantitative analysis includes statistical modeling, trend extrapolation, and correlation analysis to identify key market drivers and forecast future developments. Qualitative assessment incorporates expert opinions, industry best practices, and strategic analysis to provide context for quantitative findings.

Validation processes include peer review by industry experts, cross-referencing with multiple data sources, and sensitivity analysis to test assumption validity. Continuous monitoring of market developments ensures research findings remain current and relevant to evolving market conditions and stakeholder requirements.

Geographic distribution of Spain’s plastic packaging films market reveals significant concentration in key industrial regions with distinct characteristics and growth patterns. Catalonia region dominates market activity with approximately 35% market share, driven by its strong manufacturing base, proximity to European markets, and concentration of packaging companies in the Barcelona metropolitan area. The region benefits from excellent transportation infrastructure and established supply chains.

Madrid region represents the second-largest market segment with 22% market share, supported by its role as the national economic center and headquarters location for many multinational companies. Consumer goods concentration in the Madrid area drives demand for various packaging film applications, particularly in food and personal care sectors.

Valencia region accounts for 18% market share and serves as a critical manufacturing hub with strong connections to Mediterranean markets. Agricultural industry presence in Valencia creates substantial demand for agricultural films and food packaging applications. The region’s port facilities facilitate both raw material imports and finished product exports.

Andalusia region represents 12% market share with growing industrial development and increasing packaging demand from agricultural and food processing sectors. Basque Country contributes 8% market share with focus on high-value specialty films and industrial applications. Remaining regions collectively account for 5% market share but show potential for growth as industrial development expands across Spain.

Market structure in Spain’s plastic packaging films sector features a mix of international corporations, regional players, and specialized manufacturers competing across different market segments. Leading companies have established strong positions through technological innovation, strategic acquisitions, and comprehensive product portfolios that serve diverse application requirements.

Competitive strategies include investment in sustainable technologies, expansion of production capabilities, and development of specialized products for niche applications. Market consolidation trends are evident as companies seek to achieve economies of scale and expand their technological capabilities through strategic acquisitions and partnerships.

Market segmentation analysis reveals diverse categories within Spain’s plastic packaging films market, each serving specific application requirements and customer needs. By Material Type: The market encompasses polyethylene films, polypropylene films, polyester films, and specialty polymer films, with each category offering distinct performance characteristics and cost profiles.

By Technology: Manufacturing technologies include blown film extrusion, cast film production, and specialty coating processes that determine film properties and application suitability. By Thickness: Film thickness categories range from ultra-thin films for lightweight applications to heavy-duty films for industrial use, with each segment serving specific performance requirements.

By Application: Key application segments include:

By End-User Industry: Market segmentation includes food and beverage, healthcare, agriculture, consumer goods, and industrial sectors, each with specific requirements for film properties and performance characteristics.

Polyethylene films represent the largest category within Spain’s plastic packaging films market, driven by versatility, cost-effectiveness, and wide application range. Low-density polyethylene (LDPE) films dominate food packaging applications due to excellent sealability and moisture barrier properties. High-density polyethylene (HDPE) films serve industrial applications requiring higher strength and chemical resistance.

Polypropylene films constitute the second-largest category, valued for superior clarity, stiffness, and heat resistance properties. Biaxially oriented polypropylene (BOPP) films are extensively used in food packaging and labeling applications. Cast polypropylene (CPP) films serve as sealant layers in multilayer structures and heat-sealable applications.

Polyester films represent a growing category driven by demand for high-performance barrier properties and temperature resistance. Polyethylene terephthalate (PET) films are increasingly used in food packaging applications requiring excellent gas barrier properties and dimensional stability. Specialty polyester films serve niche applications in electronics and industrial sectors.

Specialty films including bio-based and biodegradable alternatives are emerging as significant growth categories. Barrier films with enhanced oxygen and moisture protection properties are gaining market share in food and pharmaceutical applications. Metallized films provide superior barrier properties and aesthetic appeal for premium packaging applications.

Manufacturers in Spain’s plastic packaging films market benefit from growing demand across multiple sectors, enabling capacity utilization optimization and revenue growth. Technology advancement opportunities allow manufacturers to differentiate their products through innovation and command premium pricing for specialized solutions. Sustainability initiatives create competitive advantages for companies developing eco-friendly alternatives and circular economy solutions.

Brand owners benefit from flexible packaging films through improved product protection, extended shelf life, and enhanced consumer appeal. Cost optimization opportunities arise from reduced packaging weight, improved logistics efficiency, and decreased product waste. Marketing advantages include superior printability, design flexibility, and ability to incorporate smart packaging features that enhance consumer engagement.

Retailers gain advantages through improved product presentation, reduced handling costs, and enhanced inventory management capabilities. Supply chain efficiency improvements result from lightweight packaging that reduces transportation costs and storage requirements. Consumer satisfaction increases through convenient packaging formats and improved product freshness.

End consumers benefit from enhanced product quality, improved convenience, and better value proposition through extended product life and reduced waste. Environmental benefits emerge from lightweight packaging that reduces carbon footprint and sustainable alternatives that support environmental objectives. Safety improvements result from superior barrier properties that protect product integrity and consumer health.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability transformation represents the most significant trend reshaping Spain’s plastic packaging films market, with companies investing heavily in bio-based materials, recyclable formulations, and circular economy solutions. Consumer awareness of environmental issues is driving demand for sustainable packaging alternatives that maintain performance while reducing environmental impact.

Smart packaging integration is emerging as a key trend with development of films incorporating sensors, indicators, and connectivity features that enhance supply chain visibility and consumer engagement. Active packaging solutions with antimicrobial properties and freshness indicators are gaining traction in food and pharmaceutical applications.

Lightweighting initiatives continue to drive innovation in film thickness reduction while maintaining barrier properties and mechanical strength. Advanced barrier technologies enable development of ultra-thin films with superior protection characteristics, reducing material usage and transportation costs.

Customization trends reflect growing demand for specialized films tailored to specific application requirements, driving investment in flexible manufacturing systems and rapid product development capabilities. Digital printing compatibility is becoming increasingly important as brands seek high-quality graphics and variable data printing capabilities. MWR data indicates that customization demand has grown by 28% annually across various application segments.

Recent developments in Spain’s plastic packaging films market reflect ongoing transformation toward sustainability and advanced functionality. Major investments in recycling infrastructure and closed-loop systems are enabling circular economy implementation across the packaging value chain. Technology partnerships between film manufacturers and research institutions are accelerating development of bio-based alternatives and advanced barrier solutions.

Regulatory developments including extended producer responsibility programs and plastic waste reduction targets are reshaping market dynamics and investment priorities. Industry consolidation continues with strategic acquisitions and partnerships aimed at achieving scale economies and technology integration.

Innovation breakthroughs in nanotechnology applications are enabling development of films with enhanced barrier properties and functional characteristics. Digitalization initiatives including Industry 4.0 implementation are improving manufacturing efficiency and quality control capabilities across the sector.

Export market expansion efforts are gaining momentum as Spanish manufacturers leverage their technological capabilities to serve international markets. Sustainability certifications and eco-labeling programs are becoming standard requirements for market participation and brand differentiation.

Strategic recommendations for market participants include prioritizing investment in sustainable technologies and circular economy solutions to address regulatory requirements and consumer preferences. Innovation focus should emphasize development of bio-based materials, advanced barrier properties, and smart packaging capabilities that create competitive differentiation.

Operational excellence initiatives should target manufacturing efficiency improvements, quality consistency, and supply chain optimization to maintain cost competitiveness. Partnership strategies with technology providers, research institutions, and value chain participants can accelerate innovation and market development.

Market expansion opportunities should be pursued through export development, particularly in North African and Latin American markets where Spanish companies can leverage their technological capabilities and cultural connections. Sustainability positioning should be central to brand strategy and product development initiatives.

Investment priorities should include automation technologies, recycling capabilities, and digital systems that enhance operational efficiency and market responsiveness. Talent development in sustainability technologies and advanced manufacturing processes will be critical for long-term competitiveness. According to MarkWide Research projections, companies implementing comprehensive sustainability strategies achieve 15% higher profitability compared to traditional approaches.

Long-term prospects for Spain’s plastic packaging films market remain positive despite environmental challenges, with growth driven by innovation in sustainable materials and expanding application areas. Market evolution will be characterized by transition toward circular economy models, advanced functionality integration, and increased customization capabilities.

Technology advancement will continue to drive market development with breakthrough innovations in bio-based polymers, nanotechnology applications, and smart packaging systems. Regulatory landscape evolution will create both challenges and opportunities as environmental policies shape market requirements and investment priorities.

Competitive dynamics will intensify as global players expand their presence while domestic companies strengthen their technological capabilities and market positions. Sustainability leadership will become increasingly important for market success and brand differentiation.

Growth projections indicate continued market expansion with annual growth rates of 5.8% expected over the next decade, driven by innovation, sustainability initiatives, and expanding applications. Export opportunities will provide additional growth avenues as Spanish manufacturers leverage their competitive advantages in international markets. Investment flows toward sustainable technologies and advanced manufacturing capabilities will reshape the competitive landscape and create new market leaders.

Spain’s plastic packaging films market stands at a critical juncture where traditional growth drivers intersect with sustainability imperatives and technological innovation opportunities. Market fundamentals remain strong with diverse application areas, established manufacturing capabilities, and strategic geographic positioning supporting continued expansion.

Transformation challenges related to environmental concerns and regulatory pressures are driving innovation and creating opportunities for companies capable of developing sustainable alternatives while maintaining performance standards. Competitive success will increasingly depend on sustainability leadership, technological innovation, and operational excellence rather than traditional cost-based competition.

Future market development will be characterized by circular economy implementation, smart packaging integration, and expanded international market participation. Industry participants that successfully navigate the sustainability transition while investing in advanced technologies and market expansion will be best positioned for long-term success in this evolving market landscape. The Spain plastic packaging films market represents a dynamic sector with significant potential for growth and innovation in the years ahead.

What is Plastic Packaging Films?

Plastic packaging films are thin layers of plastic used to wrap, protect, and preserve products. They are commonly utilized in various industries, including food and beverage, pharmaceuticals, and consumer goods.

What are the key players in the Spain Plastic Packaging Films Market?

Key players in the Spain Plastic Packaging Films Market include companies like Amcor, Sealed Air Corporation, and Berry Global, among others. These companies are known for their innovative packaging solutions and extensive product offerings.

What are the growth factors driving the Spain Plastic Packaging Films Market?

The Spain Plastic Packaging Films Market is driven by factors such as the increasing demand for convenient packaging solutions, the growth of the e-commerce sector, and the rising focus on food safety and preservation.

What challenges does the Spain Plastic Packaging Films Market face?

Challenges in the Spain Plastic Packaging Films Market include environmental concerns regarding plastic waste, regulatory pressures for sustainable packaging, and competition from alternative materials like biodegradable films.

What opportunities exist in the Spain Plastic Packaging Films Market?

Opportunities in the Spain Plastic Packaging Films Market include the development of eco-friendly packaging solutions, advancements in film technology, and the expansion of applications in sectors like healthcare and personal care.

What trends are shaping the Spain Plastic Packaging Films Market?

Trends in the Spain Plastic Packaging Films Market include the increasing adoption of smart packaging technologies, the shift towards recyclable materials, and the growing demand for customized packaging solutions tailored to specific consumer needs.

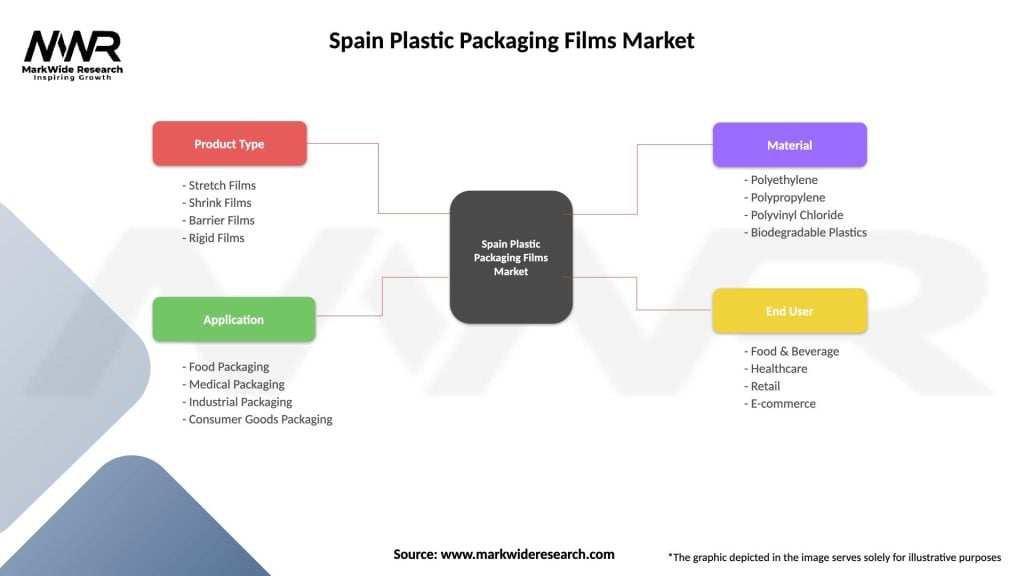

Spain Plastic Packaging Films Market

| Segmentation Details | Description |

|---|---|

| Product Type | Stretch Films, Shrink Films, Barrier Films, Rigid Films |

| Application | Food Packaging, Medical Packaging, Industrial Packaging, Consumer Goods Packaging |

| Material | Polyethylene, Polypropylene, Polyvinyl Chloride, Biodegradable Plastics |

| End User | Food & Beverage, Healthcare, Retail, E-commerce |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Spain Plastic Packaging Films Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.