444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The South America electric vehicle battery materials market represents a rapidly evolving sector that has gained significant momentum as the region embraces sustainable transportation solutions. This dynamic market encompasses critical materials essential for electric vehicle battery production, including lithium, cobalt, nickel, graphite, and various cathode and anode materials. South America’s strategic position as a major supplier of lithium resources, particularly from the renowned lithium triangle comprising Argentina, Bolivia, and Chile, positions the region as a crucial player in the global electric vehicle supply chain.

Market dynamics indicate substantial growth potential driven by increasing electric vehicle adoption rates across major South American economies. The region’s abundant natural resources, combined with growing government support for clean energy initiatives, create favorable conditions for market expansion. Brazil and Argentina lead the regional market development, with significant investments in battery material processing facilities and mining operations. The market demonstrates a compound annual growth rate of 18.5%, reflecting the accelerating transition toward electric mobility solutions.

Regional advantages include proximity to key raw material sources, established mining infrastructure, and increasing foreign direct investment in battery material processing capabilities. The market benefits from strategic partnerships between local mining companies and international battery manufacturers, fostering technology transfer and capacity building initiatives throughout the supply chain.

The South America electric vehicle battery materials market refers to the comprehensive ecosystem of raw materials, processed components, and specialized chemicals required for manufacturing electric vehicle batteries within the South American region. This market encompasses the extraction, processing, refining, and distribution of critical battery materials including lithium compounds, cobalt sulfates, nickel hydroxides, natural and synthetic graphite, and advanced cathode materials such as lithium iron phosphate and nickel manganese cobalt compounds.

Market scope extends beyond traditional mining activities to include value-added processing, chemical refinement, and the development of battery-grade materials that meet stringent automotive industry specifications. The market represents the intersection of mining, chemical processing, and advanced manufacturing sectors, creating integrated supply chains that support both domestic electric vehicle production and global export markets.

South America’s electric vehicle battery materials market stands at a pivotal juncture, leveraging the region’s exceptional natural resource endowments to capture growing global demand for sustainable transportation solutions. The market demonstrates robust growth fundamentals supported by increasing electric vehicle penetration rates, government policy initiatives promoting clean energy adoption, and substantial infrastructure investments in battery material processing capabilities.

Key market drivers include the region’s dominant position in global lithium reserves, accounting for approximately 58% of worldwide lithium resources, and growing recognition of South America as a strategic supplier for international battery manufacturers. Brazil’s automotive sector leads regional electric vehicle adoption, while Chile and Argentina focus on upstream material extraction and processing activities.

Investment trends show significant capital allocation toward battery material refinement facilities, with major international companies establishing processing operations to capture value-added opportunities. The market benefits from favorable regulatory frameworks, competitive production costs, and established logistics infrastructure supporting both regional consumption and global export activities.

Strategic market positioning reveals South America’s critical role in global electric vehicle battery supply chains, with the region emerging as a preferred destination for battery material investments. MarkWide Research analysis indicates several key insights driving market development:

Global electric vehicle adoption serves as the primary catalyst driving South America’s battery materials market expansion. Increasing consumer acceptance of electric vehicles worldwide creates sustained demand for battery materials, positioning South American suppliers advantageously due to their resource abundance and competitive production costs. International automotive manufacturers increasingly recognize the strategic importance of securing reliable battery material supply chains, leading to substantial investments in South American operations.

Government policy initiatives across the region actively promote electric vehicle adoption and battery material industry development. Brazil’s national electric mobility program includes incentives for domestic battery production, while Chile’s lithium strategy focuses on maximizing value creation from natural resource extraction. These supportive policy frameworks create favorable business environments encouraging private sector investment and international partnerships.

Technological advancement in battery chemistry and manufacturing processes drives demand for higher-quality, specialized battery materials. South American suppliers invest in advanced processing technologies to meet evolving specifications for next-generation battery systems, including solid-state batteries and high-energy-density formulations. Research and development initiatives supported by regional universities and international collaborations enhance local technical capabilities and innovation capacity.

Supply chain diversification strategies adopted by global battery manufacturers create opportunities for South American suppliers to capture market share. Concerns about supply chain concentration and geopolitical risks motivate companies to establish alternative sourcing relationships, benefiting South American producers offering reliable, cost-competitive battery materials with established mining and processing infrastructure.

Infrastructure limitations present significant challenges for South America’s battery materials market development, particularly in remote mining regions where transportation costs and logistics complexity impact competitiveness. Limited processing capacity for battery-grade materials forces many regional suppliers to export raw materials rather than capturing value-added opportunities, reducing profit margins and economic benefits for local communities.

Environmental concerns associated with mining and processing operations create regulatory uncertainties and community opposition that can delay project development and increase operational costs. Water usage requirements for lithium extraction in arid regions raise sustainability questions, while waste management and environmental remediation obligations add complexity to project economics and social acceptance.

Technical expertise gaps in advanced battery material processing limit the region’s ability to produce high-specification products required by leading battery manufacturers. Skilled workforce shortages in specialized areas such as electrochemistry, materials science, and advanced manufacturing constrain industry growth and technology adoption rates.

Capital intensity of battery material processing facilities requires substantial upfront investments that may be challenging for smaller regional companies to secure. Market volatility in battery material prices creates uncertainty for long-term investment planning, while currency fluctuations and political risks in some countries may deter international investment in regional operations.

Value-added processing expansion represents the most significant opportunity for South American battery materials suppliers to capture higher margins and strengthen their competitive positions. Downstream integration into battery-grade material production, cathode manufacturing, and even complete battery assembly creates opportunities for regional companies to move up the value chain and develop closer relationships with automotive customers.

Circular economy initiatives in battery recycling and material recovery present emerging opportunities as electric vehicle adoption increases and first-generation batteries reach end-of-life. Regional recycling facilities can process spent batteries to recover valuable materials, reducing dependence on primary extraction while creating sustainable business models that align with environmental objectives.

Strategic partnerships with international battery manufacturers and automotive companies offer opportunities for technology transfer, capacity building, and long-term supply agreements that provide revenue stability and growth potential. Joint venture arrangements can combine South American resource advantages with international technical expertise and market access, creating mutually beneficial relationships that strengthen global supply chains.

Research and development collaborations with universities, government research institutions, and international partners can accelerate innovation in battery materials and processing technologies. Innovation hubs focused on battery technology development can attract investment, develop local expertise, and position South America as a center for battery material innovation rather than simply raw material extraction.

Supply and demand dynamics in South America’s battery materials market reflect the complex interplay between regional resource availability, global electric vehicle growth, and evolving battery technology requirements. Lithium supply dynamics demonstrate the region’s strategic importance, with South American producers accounting for substantial portions of global lithium carbonate and lithium hydroxide production capacity.

Price volatility in battery materials markets creates both opportunities and challenges for South American suppliers. Commodity price cycles influence investment decisions and production planning, while long-term supply agreements provide stability for both suppliers and customers. Market consolidation trends see larger international companies acquiring regional assets to secure supply chain control and capture integration benefits.

Technological evolution in battery chemistry drives changing material requirements and specifications, creating opportunities for suppliers who can adapt quickly to new formulations and quality standards. Next-generation battery technologies such as solid-state systems may require different material compositions, potentially disrupting existing supply relationships and creating new market opportunities.

Competitive dynamics intensify as global battery material demand growth attracts new entrants and encourages capacity expansion by existing suppliers. Regional competition among South American countries for battery material investments drives policy improvements and infrastructure development, ultimately benefiting the entire regional market ecosystem.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into South America’s electric vehicle battery materials market. Primary research activities include structured interviews with industry executives, mining company representatives, government officials, and academic researchers across major South American markets to gather firsthand insights on market trends, challenges, and opportunities.

Secondary research encompasses extensive analysis of industry reports, government statistics, trade publications, and academic studies to validate primary findings and provide comprehensive market context. Data triangulation techniques ensure information accuracy by cross-referencing multiple sources and identifying consistent trends and patterns across different data sets.

Market modeling utilizes statistical analysis and forecasting techniques to project market growth trends, segment performance, and regional dynamics. Scenario analysis examines various market development pathways under different assumptions about electric vehicle adoption rates, policy changes, and technology evolution to provide robust strategic insights for market participants.

Expert validation processes involve review and feedback from industry specialists, academic researchers, and market analysts to ensure research findings accurately reflect market realities and provide actionable intelligence for strategic decision-making. Continuous monitoring of market developments ensures research remains current and relevant to evolving industry conditions.

Brazil dominates South America’s electric vehicle battery materials market with approximately 42% regional market share, driven by its large automotive industry, growing electric vehicle adoption, and substantial investments in battery material processing capabilities. Brazilian companies focus on developing integrated supply chains from raw material extraction through battery-grade material production, supported by government incentives and international partnerships.

Chile maintains a strong position with 28% market share, leveraging its position as the world’s largest lithium producer and established mining infrastructure. Chilean lithium operations in the Atacama Desert supply global battery manufacturers, while recent investments in lithium hydroxide processing facilities add value-added capabilities to the country’s battery materials portfolio.

Argentina captures approximately 18% market share, benefiting from significant lithium reserves and growing international investment in extraction and processing operations. Argentine lithium projects in the Puna region attract major international battery companies seeking to secure long-term supply agreements and develop integrated production capabilities.

Other regional markets including Colombia, Peru, and Bolivia collectively represent 12% market share, with emerging opportunities in copper, nickel, and rare earth element production for battery applications. Regional cooperation initiatives promote technology sharing and joint development projects that strengthen the overall South American battery materials ecosystem.

Market leadership in South America’s electric vehicle battery materials sector features a mix of established mining companies, emerging battery material specialists, and international corporations investing in regional operations. The competitive landscape demonstrates increasing consolidation as larger players acquire strategic assets and develop integrated supply chain capabilities.

Strategic partnerships between regional suppliers and international battery manufacturers create competitive advantages through technology transfer, long-term supply agreements, and joint development initiatives. Vertical integration strategies see companies expanding along the value chain from mining through battery material processing to capture higher margins and strengthen customer relationships.

By Material Type: The South American market segments into distinct material categories, each with unique characteristics and growth dynamics. Lithium compounds represent the largest segment, including lithium carbonate, lithium hydroxide, and specialized lithium salts used in various battery chemistries. Cathode materials encompass lithium iron phosphate, nickel manganese cobalt, and emerging high-nickel formulations that offer improved energy density and performance characteristics.

By Application: Market segmentation by application reveals diverse end-use categories driving demand growth. Passenger electric vehicles constitute the primary application segment, supported by increasing consumer adoption and expanding model availability from major automotive manufacturers. Commercial electric vehicles including buses, delivery trucks, and industrial equipment represent growing market opportunities as fleet operators embrace electric mobility solutions.

By Processing Stage: Value chain segmentation distinguishes between different processing levels and value-added activities. Raw material extraction includes mining and initial processing of lithium brines, hard rock deposits, and other battery material sources. Intermediate processing covers conversion to battery-grade chemicals and compounds meeting automotive industry specifications.

By End-User: Customer segmentation reflects the diverse range of companies utilizing South American battery materials. Battery manufacturers represent the primary customer segment, including both regional producers and international companies with South American operations. Automotive companies increasingly engage directly with material suppliers to secure supply chain control and ensure quality standards.

Lithium Materials Category: This dominant category benefits from South America’s exceptional lithium resource endowments and established production infrastructure. Lithium carbonate production leads regional output, primarily serving Asian battery manufacturers, while lithium hydroxide capacity expands to meet growing demand from high-nickel battery chemistries. Quality improvements focus on reducing impurities and achieving battery-grade specifications that command premium pricing in global markets.

Cathode Materials Category: Emerging opportunities in cathode material production represent significant value-added potential for South American suppliers. Lithium iron phosphate production benefits from abundant iron ore resources and growing demand for cost-effective, safe battery chemistries. Advanced cathode formulations require sophisticated processing capabilities and technical expertise that regional companies are developing through international partnerships and technology transfer agreements.

Anode Materials Category: Natural graphite resources in Brazil and other regional countries support anode material production for battery applications. Graphite processing capabilities focus on achieving spherical graphite specifications required for high-performance batteries. Synthetic graphite production represents emerging opportunities as battery manufacturers seek consistent quality and supply security for critical anode materials.

Electrolyte Materials Category: Specialized chemical production for battery electrolytes creates niche opportunities for South American suppliers with advanced chemical processing capabilities. Lithium salts for electrolyte applications require high purity levels and specialized handling procedures. Solvent production leverages regional petrochemical infrastructure to support integrated battery material supply chains.

Mining Companies benefit from sustained demand growth and premium pricing for battery-grade materials compared to traditional industrial applications. Revenue diversification opportunities reduce dependence on commodity cycles while long-term supply agreements provide revenue stability and support investment planning. Technology partnerships with battery manufacturers enable access to advanced processing technologies and market intelligence that enhance competitive positioning.

Battery Manufacturers gain access to cost-competitive, reliable material supplies that support production cost optimization and supply chain security. Regional sourcing reduces transportation costs and supply chain complexity while strategic partnerships with South American suppliers provide preferential access to high-quality materials and potential joint development opportunities.

Automotive Companies benefit from diversified supply chains that reduce geopolitical risks and ensure material availability for electric vehicle production programs. Cost advantages from South American suppliers support competitive electric vehicle pricing while sustainability credentials from responsible mining practices align with corporate environmental objectives and consumer expectations.

Government Stakeholders realize economic development benefits through job creation, export revenue generation, and technology transfer that builds local industrial capabilities. Tax revenue from mining and processing operations supports public investment while infrastructure development associated with battery material projects benefits broader regional economic development initiatives.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability Integration emerges as a dominant trend shaping South America’s battery materials market, with companies increasingly adopting environmentally responsible mining practices and pursuing sustainability certifications. Water management innovations address environmental concerns while renewable energy adoption in mining operations reduces carbon footprints and aligns with global sustainability objectives. Community engagement programs ensure social license to operate while creating shared value for local stakeholders.

Vertical Integration Strategies see regional companies expanding along the value chain from raw material extraction through battery-grade processing and potentially into battery manufacturing. Downstream investments capture higher margins while strategic partnerships with international battery manufacturers provide technology access and market development opportunities. Supply chain optimization focuses on reducing costs and improving quality throughout integrated operations.

Technology Advancement drives continuous improvement in extraction and processing methods, with companies investing in advanced technologies that improve efficiency, reduce environmental impact, and enhance product quality. Direct lithium extraction technologies offer potential advantages over traditional evaporation methods while automated processing systems improve consistency and reduce operational costs.

Market Diversification strategies reduce dependence on single material types or customer segments through expansion into complementary battery materials and applications. Energy storage systems for grid applications create additional demand channels while emerging battery chemistries require new material formulations and processing capabilities that create growth opportunities for adaptable suppliers.

Major Investment Announcements demonstrate growing confidence in South America’s battery materials market potential, with international companies committing substantial capital to regional operations. Processing facility expansions increase battery-grade material production capacity while technology transfer agreements enhance local capabilities and product quality standards. Strategic acquisitions consolidate market positions and create integrated supply chain advantages.

Government Policy Initiatives across the region promote battery material industry development through tax incentives, infrastructure investments, and regulatory framework improvements. National lithium strategies in Chile and Argentina focus on maximizing value creation from natural resources while electric vehicle promotion programs in Brazil create domestic demand for battery materials and support local industry development.

Technology Partnerships between South American suppliers and international battery manufacturers accelerate capability development and market access. Joint venture formations combine regional resource advantages with international technical expertise while research collaborations with universities and research institutions advance innovation in battery materials and processing technologies.

Infrastructure Development Projects improve market accessibility and reduce operational costs through transportation network upgrades, port facility expansions, and logistics optimization initiatives. Power infrastructure investments support energy-intensive processing operations while water management projects address sustainability concerns and ensure operational continuity.

Strategic Focus recommendations emphasize the importance of value-added processing investments to capture higher margins and strengthen competitive positions in global battery materials markets. MWR analysis suggests that companies prioritizing battery-grade material production capabilities will achieve superior long-term performance compared to those focused solely on raw material extraction activities.

Partnership Development strategies should emphasize building relationships with international battery manufacturers and automotive companies to secure long-term supply agreements and access advanced technologies. Technology transfer initiatives provide opportunities to enhance processing capabilities while joint development projects create competitive advantages through customized material solutions and integrated supply chain relationships.

Sustainability Leadership becomes increasingly important as automotive companies and battery manufacturers prioritize responsible sourcing practices and environmental stewardship. Certification programs for sustainable mining and processing operations create market differentiation while community engagement initiatives ensure social license to operate and support long-term business sustainability.

Market Diversification strategies reduce risk exposure through expansion into complementary materials and applications beyond traditional automotive battery markets. Energy storage applications provide additional demand channels while emerging battery technologies create opportunities for companies with flexible processing capabilities and strong research and development programs.

Long-term growth prospects for South America’s electric vehicle battery materials market remain highly favorable, supported by the region’s exceptional natural resource endowments, improving processing capabilities, and growing global demand for sustainable transportation solutions. Market expansion is projected to continue at robust rates, with annual growth exceeding 15% through the next decade as electric vehicle adoption accelerates worldwide.

Technology evolution will drive changing material requirements and create opportunities for suppliers who can adapt to next-generation battery chemistries and specifications. Solid-state battery development may require different material compositions while recycling technologies create circular economy opportunities that reduce dependence on primary extraction and support sustainable industry development.

Regional integration initiatives will strengthen South America’s position in global battery materials supply chains through improved cooperation, shared infrastructure development, and coordinated market development strategies. Cross-border partnerships optimize resource utilization while regional trade agreements facilitate market access and reduce operational complexity for international customers.

Investment trends indicate continued capital allocation toward value-added processing capabilities, with processing capacity expected to increase by 45% over the next five years. International partnerships will accelerate technology transfer and capability development while government support continues to provide favorable business environments for industry growth and development.

South America’s electric vehicle battery materials market represents a compelling investment opportunity characterized by abundant natural resources, growing global demand, and increasing recognition of the region’s strategic importance in sustainable transportation supply chains. The market benefits from established mining infrastructure, competitive production costs, and supportive government policies that create favorable conditions for continued growth and development.

Strategic advantages including resource abundance, geographic positioning, and emerging processing capabilities position South American suppliers advantageously in global battery materials markets. Value-added processing investments offer opportunities to capture higher margins while international partnerships provide access to advanced technologies and market development support that strengthen competitive positions.

Future success will depend on continued investment in processing capabilities, technology advancement, and sustainability leadership that addresses environmental and social concerns while meeting growing demand for high-quality battery materials. Regional cooperation and strategic partnerships will be essential for maximizing the collective potential of South America’s battery materials ecosystem and establishing the region as a global leader in sustainable battery material production.

What is Electric Vehicle Battery Materials?

Electric Vehicle Battery Materials refer to the various components and substances used in the production of batteries for electric vehicles, including lithium, cobalt, nickel, and graphite. These materials are essential for the performance, efficiency, and sustainability of electric vehicle batteries.

What are the key players in the South America Electric Vehicle Battery Materials Market?

Key players in the South America Electric Vehicle Battery Materials Market include companies like SQM, Livent Corporation, and Vale S.A. These companies are involved in the extraction and processing of critical materials used in electric vehicle batteries, among others.

What are the growth factors driving the South America Electric Vehicle Battery Materials Market?

The South America Electric Vehicle Battery Materials Market is driven by the increasing demand for electric vehicles, government incentives for clean energy, and advancements in battery technology. Additionally, the push for sustainable transportation solutions is further fueling market growth.

What challenges does the South America Electric Vehicle Battery Materials Market face?

Challenges in the South America Electric Vehicle Battery Materials Market include supply chain disruptions, fluctuating raw material prices, and environmental concerns related to mining practices. These factors can impact the availability and cost of essential battery materials.

What opportunities exist in the South America Electric Vehicle Battery Materials Market?

Opportunities in the South America Electric Vehicle Battery Materials Market include the potential for local sourcing of materials, investments in recycling technologies, and partnerships between manufacturers and technology firms. These developments can enhance sustainability and reduce dependency on imports.

What trends are shaping the South America Electric Vehicle Battery Materials Market?

Trends in the South America Electric Vehicle Battery Materials Market include the growing focus on sustainable sourcing of materials, innovations in battery chemistry, and the rise of solid-state batteries. These trends are expected to influence the future landscape of electric vehicle battery production.

South America Electric Vehicle Battery Materials Market

| Segmentation Details | Description |

|---|---|

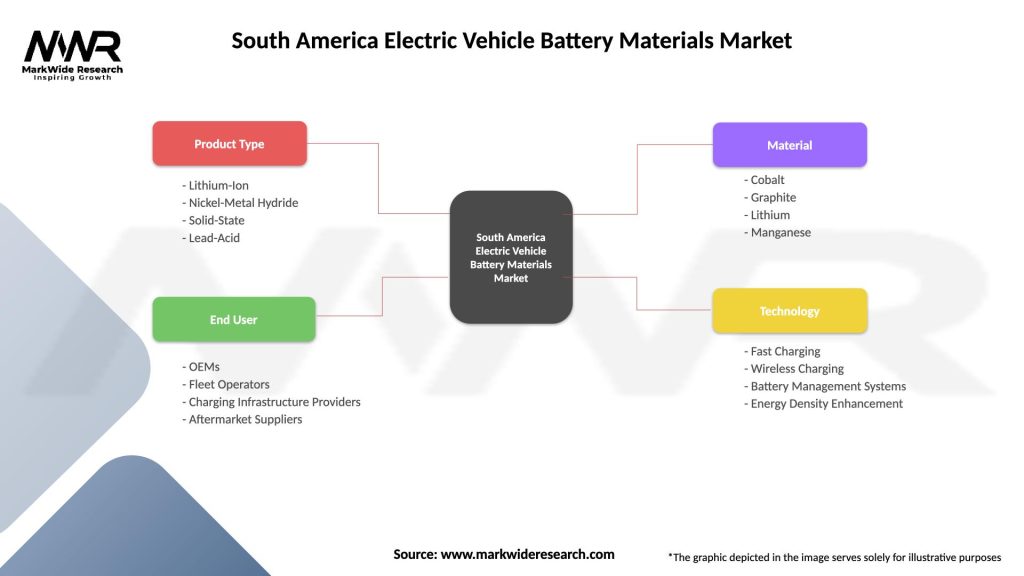

| Product Type | Lithium-Ion, Nickel-Metal Hydride, Solid-State, Lead-Acid |

| End User | OEMs, Fleet Operators, Charging Infrastructure Providers, Aftermarket Suppliers |

| Material | Cobalt, Graphite, Lithium, Manganese |

| Technology | Fast Charging, Wireless Charging, Battery Management Systems, Energy Density Enhancement |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the South America Electric Vehicle Battery Materials Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.