444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The South America data center market represents a rapidly expanding segment of the region’s digital infrastructure landscape, driven by increasing digitalization, cloud adoption, and growing demand for data processing capabilities. Market dynamics indicate substantial growth potential across key countries including Brazil, Argentina, Chile, and Colombia, with enterprises and service providers investing heavily in modern data center facilities.

Regional expansion has been particularly pronounced in major metropolitan areas such as São Paulo, Buenos Aires, Santiago, and Bogotá, where businesses are establishing state-of-the-art facilities to support their digital transformation initiatives. The market encompasses various facility types, from hyperscale data centers operated by global cloud providers to enterprise-specific installations and colocation facilities serving multiple tenants.

Growth trajectories across South America show promising development, with the region experiencing a 12.8% CAGR in data center capacity expansion over recent years. This growth reflects increasing demand from sectors including financial services, telecommunications, e-commerce, and government agencies seeking reliable, secure, and scalable data processing solutions.

Infrastructure development initiatives throughout the region have created favorable conditions for data center investments, with improved power grid reliability, enhanced telecommunications networks, and supportive regulatory frameworks encouraging both domestic and international players to establish operations in key South American markets.

The South America data center market refers to the comprehensive ecosystem of facilities, services, and technologies that provide data storage, processing, and management capabilities across South American countries. These facilities serve as critical infrastructure supporting digital services, cloud computing, enterprise applications, and internet connectivity for businesses and consumers throughout the region.

Data center facilities in South America encompass various configurations including enterprise data centers owned and operated by individual organizations, colocation facilities that house equipment for multiple clients, and hyperscale installations operated by major cloud service providers and internet companies.

Service offerings within this market include infrastructure as a service (IaaS), platform as a service (PaaS), software as a service (SaaS), disaster recovery solutions, managed hosting services, and specialized applications supporting industries such as banking, telecommunications, healthcare, and government operations.

Market expansion across South America’s data center sector demonstrates robust growth driven by digital transformation initiatives, increasing internet penetration, and growing demand for cloud-based services. The region’s strategic position as a gateway between North American and global markets has attracted significant investment from international data center operators and cloud service providers.

Key growth drivers include the rapid adoption of digital banking services, expansion of e-commerce platforms, increasing smartphone penetration reaching 78% across major markets, and government initiatives promoting digital infrastructure development. These factors have created substantial demand for reliable, high-performance data center services throughout the region.

Investment patterns show increasing focus on sustainable data center operations, with operators implementing advanced cooling technologies, renewable energy integration, and energy-efficient designs to reduce operational costs and environmental impact while meeting growing capacity requirements.

Competitive dynamics feature a mix of global hyperscale operators, regional service providers, and local enterprises developing data center capabilities to support their specific market requirements and customer bases across diverse South American economies.

Strategic positioning of South America’s data center market reveals several critical insights that define current and future development patterns:

Digital transformation initiatives across South American enterprises represent the primary catalyst driving data center market expansion. Organizations are modernizing their IT infrastructure to support cloud-first strategies, implement advanced analytics capabilities, and enable remote work environments that became essential during recent global disruptions.

E-commerce growth throughout the region has created substantial demand for scalable data center services, with online retail platforms requiring robust infrastructure to handle transaction processing, inventory management, and customer data analytics. The expansion of digital payment systems and fintech services further amplifies this demand.

Government digitalization programs across multiple South American countries are driving significant investments in data center infrastructure to support e-government services, digital identity systems, and citizen service platforms. These initiatives require secure, reliable data processing capabilities with high availability requirements.

Telecommunications sector expansion continues to fuel data center demand as mobile network operators deploy 5G infrastructure, expand fiber optic networks, and implement network function virtualization technologies that require substantial data processing and storage capabilities.

Content delivery requirements from streaming services, gaming platforms, and social media companies are driving edge data center deployments closer to end users, improving performance while reducing bandwidth costs and latency issues that affect user experience quality.

Infrastructure limitations in certain South American markets present significant challenges for data center development, including inconsistent power grid reliability, limited high-speed internet connectivity in secondary markets, and inadequate transportation infrastructure for equipment delivery and maintenance operations.

Economic volatility across the region creates uncertainty for long-term data center investments, with currency fluctuations, inflation pressures, and changing regulatory environments affecting project financing and operational cost predictability for both domestic and international operators.

Skilled workforce shortages in specialized data center technologies limit expansion capabilities, as operators struggle to find qualified personnel for facility management, network operations, cybersecurity, and advanced technical support roles required for modern data center operations.

Regulatory complexity varies significantly across South American countries, creating challenges for multi-national data center operators seeking to establish consistent service offerings while complying with diverse data protection, tax, and operational requirements in different jurisdictions.

High initial capital requirements for data center development can limit market entry for smaller operators, while established players face challenges in securing financing for expansion projects in markets perceived as higher risk by international investors and lenders.

Edge computing deployment presents substantial opportunities as businesses seek to reduce latency and improve application performance through distributed data center architectures. This trend creates demand for smaller, strategically located facilities serving specific geographic regions or industry verticals.

Sustainability initiatives offer competitive advantages for data center operators implementing renewable energy sources, advanced cooling technologies, and energy-efficient designs. These approaches reduce operational costs while meeting corporate environmental responsibility requirements from enterprise customers.

Industry-specific solutions create opportunities for specialized data center services tailored to sectors such as healthcare, financial services, manufacturing, and government agencies with unique compliance, security, and performance requirements that generic facilities cannot adequately address.

Hybrid cloud adoption drives demand for data center services that seamlessly integrate with public cloud platforms, enabling enterprises to maintain sensitive data locally while leveraging cloud scalability for variable workloads and disaster recovery capabilities.

International connectivity expansion through new submarine cables and terrestrial fiber networks creates opportunities for data center operators to serve as regional hubs for global content distribution, data backup services, and international business operations requiring South American presence.

Supply and demand equilibrium in South America’s data center market shows increasing tension as demand growth outpaces new capacity additions in key metropolitan areas. This dynamic has led to rising colocation prices and longer lead times for enterprise data center space, creating opportunities for new facility development.

Technology evolution continues to reshape market dynamics, with operators investing in advanced cooling systems, high-density server configurations, and software-defined infrastructure that maximizes capacity utilization while reducing operational costs and environmental impact.

Customer requirements are becoming increasingly sophisticated, with enterprises demanding higher uptime guarantees, enhanced security measures, compliance certifications, and integrated managed services that extend beyond basic infrastructure provision to include application support and optimization.

Competitive pressures drive continuous innovation in service offerings, pricing models, and operational efficiency improvements. Operators are differentiating through specialized services, industry expertise, and strategic partnerships that provide comprehensive solutions for complex customer requirements.

Investment flows from international sources continue to support market expansion, with global data center operators, infrastructure funds, and technology companies establishing South American operations to capture growth opportunities and serve multinational clients requiring regional presence.

Comprehensive market analysis for the South America data center market employs multiple research methodologies to ensure accurate, reliable, and actionable insights for industry stakeholders, investors, and market participants seeking to understand current conditions and future opportunities.

Primary research activities include structured interviews with data center operators, enterprise customers, technology vendors, and industry experts across key South American markets. These discussions provide qualitative insights into market trends, customer requirements, operational challenges, and strategic planning considerations.

Secondary research sources encompass industry reports, government publications, regulatory filings, company financial statements, and trade association data that provide quantitative market metrics, competitive intelligence, and regulatory environment analysis across multiple South American countries.

Market validation processes involve cross-referencing multiple data sources, conducting follow-up interviews with key stakeholders, and applying statistical analysis techniques to ensure data accuracy and reliability while identifying potential biases or limitations in available information.

Analytical frameworks incorporate both quantitative modeling and qualitative assessment methodologies to develop comprehensive market insights that address current conditions, emerging trends, competitive dynamics, and future growth projections for various market segments and geographic regions.

Brazil dominates the South American data center landscape, accounting for approximately 52% of regional capacity and hosting major facilities from international operators including hyperscale cloud providers and colocation specialists. São Paulo serves as the primary hub, with Rio de Janeiro and other major cities supporting secondary data center deployments.

Argentina represents the second-largest market with 23% market share, centered primarily in Buenos Aires where financial services, telecommunications, and government sectors drive substantial demand for data center services. The country’s strategic location and established business infrastructure attract regional headquarters operations.

Chile’s market shows rapid growth with 12% regional share, benefiting from political stability, reliable infrastructure, and strategic position for serving Pacific Rim connectivity requirements. Santiago hosts major data center facilities supporting mining, financial services, and telecommunications sectors.

Colombia emerges as a growing market with 8% share, driven by Bogotá’s role as a regional business center and government digitalization initiatives. The country’s improving infrastructure and strategic location create opportunities for data center operators serving northern South American markets.

Other markets including Peru, Ecuador, Uruguay, and Paraguay collectively represent 5% of regional capacity but show promising growth potential as digital transformation initiatives expand and infrastructure development progresses across these emerging markets.

Market leadership in South America’s data center sector features a diverse mix of global hyperscale operators, regional service providers, and specialized colocation companies serving different customer segments and geographic markets throughout the region.

Competitive strategies focus on geographic expansion, service diversification, sustainability initiatives, and strategic partnerships that enable operators to serve evolving customer requirements while maintaining operational efficiency and competitive pricing structures.

By Facility Type:

By Service Type:

By Industry Vertical:

Hyperscale segment demonstrates the strongest growth trajectory, with major cloud providers establishing regional presence to serve enterprise customers migrating to cloud-based infrastructure. These facilities typically feature high-density configurations, advanced cooling systems, and renewable energy integration to optimize operational efficiency.

Colocation services remain popular among enterprises seeking to outsource data center operations while maintaining control over their IT infrastructure. This segment benefits from economies of scale, shared security investments, and professional facility management that many organizations cannot cost-effectively provide internally.

Edge computing facilities represent the fastest-growing category, driven by applications requiring ultra-low latency including gaming, video streaming, IoT data processing, and real-time analytics. These smaller facilities are strategically located to minimize distance between users and computing resources.

Enterprise data centers continue serving organizations with specific security, compliance, or performance requirements that cannot be adequately addressed through shared facilities. This segment includes financial institutions, government agencies, and companies handling sensitive intellectual property.

Managed services integration across all categories shows increasing demand, with customers seeking comprehensive solutions that include infrastructure provision, ongoing management, security monitoring, and performance optimization rather than basic facility rental arrangements.

Enterprise customers benefit from improved application performance, enhanced data security, regulatory compliance support, and reduced IT infrastructure management overhead through professional data center services. These advantages enable organizations to focus on core business activities while ensuring reliable technology infrastructure.

Data center operators gain opportunities for revenue growth, market expansion, and operational efficiency improvements through economies of scale, advanced technology deployment, and diversified customer portfolios that reduce dependency on individual clients or market segments.

Technology vendors access expanding markets for servers, storage systems, networking equipment, cooling solutions, and management software as data center operators invest in capacity expansion and infrastructure modernization projects throughout South America.

Government agencies achieve digital transformation objectives, improved citizen services, and enhanced operational efficiency through reliable data center infrastructure that supports e-government platforms, digital identity systems, and inter-agency data sharing initiatives.

Economic development benefits include job creation in high-skill technology sectors, increased foreign investment, improved digital infrastructure supporting business competitiveness, and enhanced connectivity that attracts international companies establishing regional operations.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability integration has become a defining trend, with data center operators implementing renewable energy sources, advanced cooling technologies, and energy-efficient designs to reduce environmental impact while controlling operational costs. Green certifications are increasingly important for enterprise customers with corporate sustainability commitments.

Edge computing deployment accelerates as applications require ultra-low latency and real-time processing capabilities. This trend drives development of smaller, distributed data centers located closer to end users, supporting applications including autonomous vehicles, industrial IoT, and augmented reality services.

Hybrid cloud adoption continues expanding as enterprises seek to balance public cloud scalability with private infrastructure control for sensitive workloads. This approach requires data center services that seamlessly integrate with major cloud platforms while providing local data processing capabilities.

Artificial intelligence integration transforms data center operations through predictive maintenance, automated resource optimization, and intelligent cooling management systems that improve efficiency while reducing operational costs and environmental impact.

Connectivity enhancement through new submarine cables, terrestrial fiber networks, and 5G infrastructure creates opportunities for data center operators to serve as regional connectivity hubs supporting international business operations and content distribution networks.

Major infrastructure investments from global cloud providers continue reshaping the South American data center landscape, with Amazon Web Services, Microsoft Azure, and Google Cloud establishing regional presence through substantial facility development and local partnership agreements.

Regulatory framework evolution across multiple South American countries has created more favorable conditions for data center investments, with governments recognizing digital infrastructure as critical for economic competitiveness and implementing supportive policies for facility development.

Submarine cable projects including new trans-Pacific and trans-Atlantic connections enhance South America’s position as a global connectivity hub, creating opportunities for data center operators to serve international content distribution and data backup requirements.

Sustainability initiatives gain momentum with operators implementing renewable energy projects, advanced cooling technologies, and circular economy principles in facility design and operations. These developments respond to both cost optimization objectives and corporate environmental responsibility requirements.

Strategic partnerships between international data center operators and local service providers enable market entry while leveraging regional expertise, regulatory knowledge, and established customer relationships that facilitate expansion into new geographic markets and industry verticals.

MarkWide Research analysis indicates that data center operators should prioritize geographic diversification across multiple South American markets to reduce concentration risk while capturing growth opportunities in emerging metropolitan areas beyond traditional hubs like São Paulo and Buenos Aires.

Investment strategies should emphasize sustainability and energy efficiency as key differentiators, with operators implementing renewable energy sources and advanced cooling technologies that provide both cost advantages and competitive positioning for environmentally conscious enterprise customers.

Service portfolio expansion into managed services, cloud integration, and industry-specific solutions will be essential for maintaining competitive advantages as the market matures and customers demand more comprehensive technology partnerships rather than basic infrastructure provision.

Partnership development with local telecommunications providers, system integrators, and technology vendors can accelerate market penetration while providing access to established customer relationships and regional expertise that international operators may lack.

Edge computing preparation should begin immediately, with operators developing strategies for distributed facility deployment that can support emerging applications requiring ultra-low latency while maintaining operational efficiency across multiple smaller locations.

Growth projections for South America’s data center market remain highly positive, with MWR forecasting continued expansion driven by digital transformation acceleration, cloud adoption growth, and increasing demand for edge computing capabilities across diverse industry sectors and geographic markets.

Technology evolution will continue reshaping facility requirements, with operators investing in high-density configurations, advanced cooling systems, and software-defined infrastructure that maximizes capacity utilization while supporting emerging workloads including artificial intelligence and machine learning applications.

Market consolidation is expected to accelerate as smaller operators seek partnerships or acquisition opportunities with larger players having the capital resources and technical expertise required for next-generation data center development and operations.

Regulatory harmonization across South American countries may create opportunities for more efficient multi-national operations, while data sovereignty requirements could drive increased demand for locally-hosted data center services from both domestic and international enterprises.

Sustainability requirements will become increasingly important, with operators needing to demonstrate measurable environmental impact reductions through renewable energy adoption, circular economy principles, and advanced efficiency technologies that meet both regulatory requirements and corporate customer expectations.

South America’s data center market presents substantial opportunities for growth and development, driven by accelerating digitalization, increasing cloud adoption, and expanding demand for edge computing capabilities across diverse industry sectors and geographic regions throughout the continent.

Market dynamics favor operators who can successfully navigate regulatory complexity, infrastructure challenges, and competitive pressures while delivering innovative services that meet evolving customer requirements for performance, security, sustainability, and cost-effectiveness.

Strategic success will require balanced approaches combining geographic diversification, technology innovation, sustainability integration, and comprehensive service portfolios that position operators as strategic partners rather than commodity infrastructure providers in an increasingly sophisticated marketplace.

Future growth prospects remain highly favorable for well-positioned operators who can capitalize on digital transformation trends, emerging technology requirements, and expanding connectivity infrastructure that positions South America as an increasingly important hub for global data center operations and services.

What is Data Center?

A data center is a facility used to house computer systems and associated components, such as telecommunications and storage systems. It plays a crucial role in managing and storing data for various applications across industries.

What are the key players in the South America Data Center Market?

Key players in the South America Data Center Market include Equinix, Digital Realty, and Ascenty, which provide various services such as colocation, cloud services, and managed hosting, among others.

What are the main drivers of growth in the South America Data Center Market?

The main drivers of growth in the South America Data Center Market include the increasing demand for cloud computing services, the rise in data consumption, and the need for enhanced data security and compliance solutions.

What challenges does the South America Data Center Market face?

Challenges in the South America Data Center Market include high operational costs, regulatory compliance issues, and the need for skilled workforce to manage advanced technologies.

What opportunities exist in the South America Data Center Market?

Opportunities in the South America Data Center Market include the expansion of edge computing, the growth of artificial intelligence applications, and the increasing investment in renewable energy sources for sustainable operations.

What trends are shaping the South America Data Center Market?

Trends shaping the South America Data Center Market include the adoption of hyper-converged infrastructure, the shift towards green data centers, and the integration of advanced cooling technologies to improve energy efficiency.

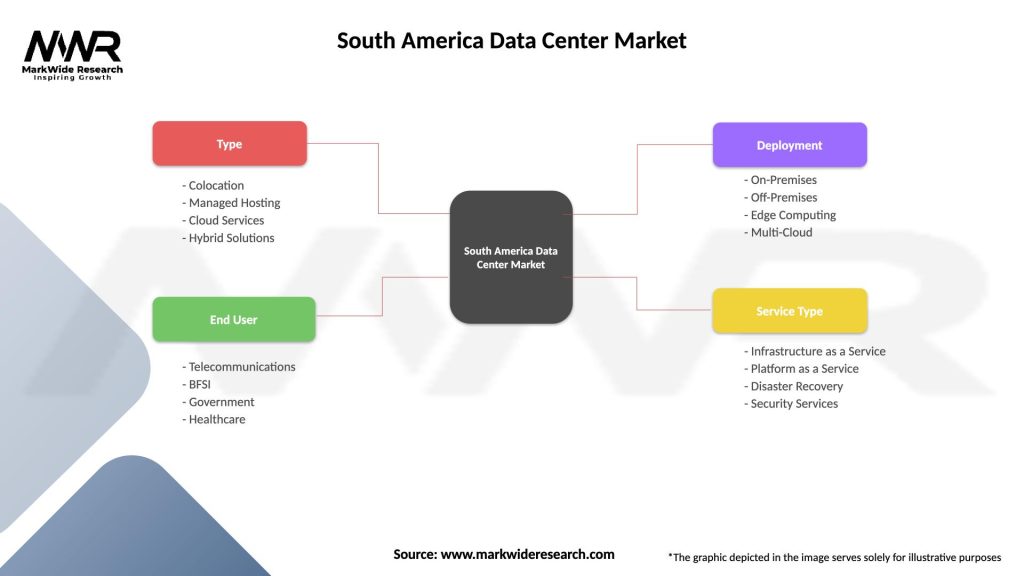

South America Data Center Market

| Segmentation Details | Description |

|---|---|

| Type | Colocation, Managed Hosting, Cloud Services, Hybrid Solutions |

| End User | Telecommunications, BFSI, Government, Healthcare |

| Deployment | On-Premises, Off-Premises, Edge Computing, Multi-Cloud |

| Service Type | Infrastructure as a Service, Platform as a Service, Disaster Recovery, Security Services |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the South America Data Center Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.