444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Software-Defined Networking (SDN) market represents a transformative shift in network infrastructure management, enabling organizations to centrally control and program network behavior through software applications. This revolutionary approach separates the network control plane from the data plane, providing unprecedented flexibility, scalability, and cost-effectiveness in network operations. The market has experienced remarkable growth momentum, driven by increasing demand for cloud computing, virtualization technologies, and the need for dynamic network management capabilities.

Market dynamics indicate robust expansion across multiple industry verticals, with enterprises increasingly adopting SDN solutions to address complex networking challenges. The technology enables organizations to achieve 45% reduction in operational costs while improving network agility and performance. Key market segments include data centers, telecommunications, enterprises, and cloud service providers, each contributing to the overall market momentum through diverse implementation strategies and use cases.

Regional adoption patterns show significant variation, with North America leading in early adoption and innovation, followed by Europe and Asia-Pacific regions experiencing rapid growth. The market demonstrates strong potential for continued expansion, supported by ongoing digital transformation initiatives and the increasing complexity of modern network infrastructures requiring more sophisticated management solutions.

The Software-Defined Networking (SDN) market refers to the comprehensive ecosystem of technologies, solutions, and services that enable centralized network control through software-based management systems, separating network intelligence from underlying hardware infrastructure to create more flexible, programmable, and efficient networking environments.

SDN architecture fundamentally transforms traditional networking by introducing a centralized controller that maintains a global view of the network topology and makes intelligent routing decisions. This approach enables network administrators to programmatically configure, manage, and optimize network resources through software applications rather than manual hardware configuration. The technology encompasses various components including SDN controllers, southbound and northbound APIs, and network virtualization platforms.

Core functionalities of SDN include network programmability, centralized management, dynamic resource allocation, and automated policy enforcement. Organizations leverage these capabilities to implement sophisticated traffic engineering, security policies, and quality of service measures while reducing dependency on proprietary hardware solutions. The technology enables rapid deployment of new services and applications while maintaining optimal network performance and security standards.

Market expansion in the Software-Defined Networking sector reflects the growing need for agile, scalable network infrastructure solutions across diverse industry segments. Organizations worldwide are recognizing the strategic value of SDN implementations in achieving operational efficiency, cost optimization, and enhanced network performance. The market encompasses a broad spectrum of solutions including SDN controllers, network virtualization platforms, orchestration tools, and professional services.

Technology adoption has accelerated significantly, with enterprises reporting 60% improvement in network provisioning speed following SDN implementation. Key market drivers include the proliferation of cloud computing, increasing data traffic volumes, and the need for more responsive network management capabilities. The market benefits from strong vendor ecosystem development, with established networking companies and emerging technology providers contributing innovative solutions.

Competitive landscape features a mix of traditional networking giants and innovative software companies, creating a dynamic environment for technological advancement and market growth. Strategic partnerships, acquisitions, and collaborative development initiatives continue to shape market evolution, while customer demand for integrated, comprehensive SDN solutions drives vendor innovation and service expansion.

Market intelligence reveals several critical insights that define the current and future trajectory of the SDN market:

Digital transformation initiatives serve as the primary catalyst for SDN market growth, with organizations seeking to modernize network infrastructure to support evolving business requirements. The increasing complexity of modern applications and services demands more sophisticated network management capabilities that traditional networking approaches cannot adequately address. SDN technologies provide the flexibility and programmability necessary to support dynamic workload requirements and rapid service deployment.

Cloud computing proliferation significantly drives SDN adoption as organizations migrate workloads to public, private, and hybrid cloud environments. These deployments require seamless connectivity, consistent policy enforcement, and dynamic resource allocation capabilities that SDN solutions effectively provide. The technology enables organizations to maintain network performance and security standards across distributed infrastructure while reducing operational complexity.

Cost reduction pressures motivate organizations to explore SDN implementations as a means of optimizing network infrastructure investments. The technology enables more efficient utilization of network resources, reduces dependency on expensive proprietary hardware, and streamlines operational processes. Organizations typically achieve significant cost savings through reduced hardware requirements, simplified management processes, and improved resource utilization efficiency.

Network agility requirements continue to drive market demand as businesses need to rapidly adapt network configurations to support changing operational requirements. SDN solutions enable programmatic network changes, automated policy implementation, and dynamic service provisioning that traditional networking approaches cannot match. This agility becomes increasingly critical as organizations adopt DevOps practices and implement continuous integration and deployment methodologies.

Implementation complexity represents a significant barrier to SDN adoption, particularly for organizations with limited networking expertise or complex legacy infrastructure. The technology requires substantial planning, testing, and validation efforts to ensure successful deployment without disrupting existing network operations. Many organizations struggle with the technical challenges associated with integrating SDN solutions into established network environments.

Security concerns continue to influence adoption decisions, as centralized network control introduces potential single points of failure and new attack vectors. Organizations express concerns about the security implications of software-based network management and the potential risks associated with centralized controller architectures. These concerns require careful security planning and implementation of robust protection measures.

Skills shortage poses ongoing challenges for organizations seeking to implement and manage SDN solutions effectively. The technology requires specialized knowledge and expertise that many IT teams currently lack, creating barriers to successful deployment and ongoing operations. Organizations must invest in training programs or external expertise to address these skill gaps.

Vendor lock-in risks concern organizations evaluating SDN solutions, as proprietary implementations may limit future flexibility and increase long-term costs. The lack of complete standardization across SDN platforms creates potential compatibility issues and reduces vendor negotiating power. Organizations must carefully evaluate vendor strategies and solution architectures to minimize these risks.

5G network deployment creates substantial opportunities for SDN market expansion, as telecommunications providers require sophisticated network management capabilities to support next-generation wireless services. The technology enables dynamic network slicing, quality of service optimization, and efficient resource allocation necessary for 5G implementations. SDN solutions provide the programmability and flexibility required to support diverse 5G use cases and service requirements.

Edge computing growth presents significant market opportunities as organizations deploy computing resources closer to end users and data sources. SDN technologies enable efficient management of distributed edge infrastructure, providing centralized control while maintaining local processing capabilities. The technology supports dynamic workload placement, traffic optimization, and security policy enforcement across edge deployments.

Internet of Things expansion drives demand for SDN solutions capable of managing massive numbers of connected devices and diverse traffic patterns. The technology enables intelligent traffic routing, device segmentation, and policy enforcement necessary for large-scale IoT deployments. Organizations require sophisticated network management capabilities to support IoT initiatives while maintaining security and performance standards.

Network function virtualization integration offers opportunities for comprehensive software-defined infrastructure solutions that combine SDN with virtualized network functions. This convergence enables organizations to achieve greater operational efficiency, reduced costs, and improved service agility through integrated software-based networking approaches.

Technology evolution continues to shape SDN market dynamics, with ongoing innovations in controller architectures, programmability interfaces, and integration capabilities. Vendors consistently enhance solution capabilities to address emerging customer requirements and competitive pressures. The market benefits from continuous technological advancement that expands use case applicability and improves solution effectiveness.

Competitive intensity drives innovation and market expansion as vendors compete for market share through differentiated offerings and strategic partnerships. The market features both established networking companies leveraging existing customer relationships and innovative software companies introducing disruptive technologies. This competition benefits customers through improved solutions, competitive pricing, and expanded service offerings.

Customer maturity influences market dynamics as organizations develop greater understanding of SDN technologies and implementation best practices. Early adopters share experiences and lessons learned, accelerating broader market adoption and reducing implementation risks for subsequent deployers. MarkWide Research indicates that organizations with SDN experience demonstrate 85% satisfaction rates with deployment outcomes.

Ecosystem development strengthens market foundations through partnerships, integrations, and collaborative initiatives among vendors, service providers, and technology partners. These relationships enable comprehensive solution offerings and reduce customer implementation complexity while expanding market reach for participating organizations.

Primary research forms the foundation of comprehensive SDN market analysis, incorporating extensive interviews with industry executives, technology leaders, and end-user organizations across diverse market segments. Research methodologies include structured surveys, in-depth interviews, and focus group discussions to gather qualitative and quantitative insights about market trends, adoption patterns, and future requirements.

Secondary research supplements primary data collection through analysis of industry reports, vendor documentation, academic research, and regulatory filings. This approach provides comprehensive market context and validates primary research findings while identifying emerging trends and technological developments that influence market evolution.

Market modeling employs sophisticated analytical techniques to project market trends, segment performance, and competitive dynamics. Research methodologies incorporate statistical analysis, trend extrapolation, and scenario modeling to develop accurate market forecasts and identify key growth opportunities.

Expert validation ensures research accuracy and reliability through consultation with industry experts, technology specialists, and market analysts. This validation process confirms research findings, identifies potential biases, and enhances the overall quality and credibility of market analysis and projections.

North America maintains market leadership in SDN adoption, driven by strong technology infrastructure, early adopter organizations, and robust vendor ecosystem presence. The region demonstrates 40% market share globally, supported by significant investments in data center modernization, cloud computing initiatives, and digital transformation programs. Major technology companies and service providers in the region continue to drive innovation and market development.

Europe represents a rapidly growing market segment, with organizations increasingly recognizing the strategic value of SDN implementations for operational efficiency and competitive advantage. The region shows strong adoption in telecommunications, financial services, and manufacturing sectors, supported by regulatory initiatives promoting digital infrastructure modernization. European organizations demonstrate particular interest in open-source SDN solutions and vendor-neutral implementations.

Asia-Pacific exhibits the highest growth potential, driven by rapid economic development, infrastructure modernization initiatives, and increasing technology adoption across diverse industry sectors. The region benefits from substantial investments in telecommunications infrastructure, data center development, and cloud computing services. Countries including China, Japan, and India lead regional adoption through government initiatives and private sector investments.

Latin America and other emerging markets show increasing interest in SDN technologies as organizations seek to modernize network infrastructure and improve operational efficiency. These regions benefit from technology transfer, vendor expansion initiatives, and growing awareness of SDN benefits for cost optimization and network agility.

Market leadership is distributed among several key categories of vendors, each bringing distinct capabilities and market approaches to SDN solutions:

Competitive strategies vary significantly among market participants, with established vendors leveraging existing customer relationships and channel partnerships while innovative companies focus on technological differentiation and specialized use cases. Strategic acquisitions, partnerships, and collaborative development initiatives continue to reshape competitive dynamics and market positioning.

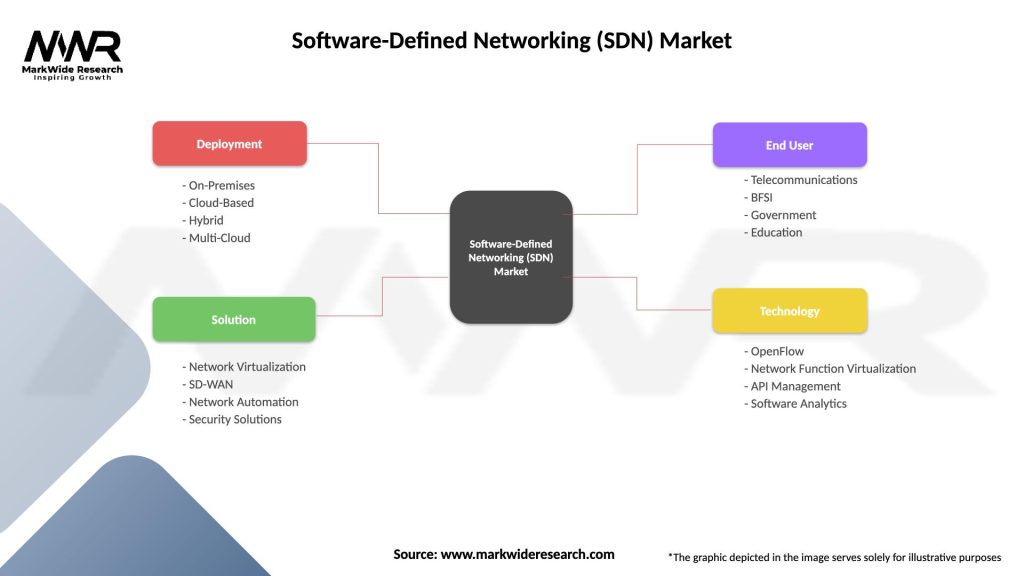

By Component:

By Deployment Model:

By Organization Size:

By Industry Vertical:

Data Center SDN represents the largest and most mature market segment, with organizations implementing SDN solutions to improve data center efficiency, scalability, and management capabilities. This category demonstrates strong growth driven by cloud computing adoption, virtualization initiatives, and the need for dynamic resource allocation. Data center SDN solutions typically achieve 50% reduction in provisioning time while improving network utilization and operational efficiency.

Campus Networking SDN shows increasing adoption as organizations seek to modernize traditional campus network infrastructure with centralized management and policy enforcement capabilities. Educational institutions, corporate campuses, and healthcare facilities represent key customer segments for campus SDN solutions. These implementations focus on user mobility, security policy enforcement, and simplified network management.

Wide Area Network SDN emerges as a high-growth category, driven by organizations requiring dynamic connectivity between distributed locations and cloud services. SD-WAN solutions provide centralized management, traffic optimization, and cost reduction benefits for organizations with multiple locations. This category benefits from increasing cloud adoption and the need for application-aware networking capabilities.

Service Provider SDN focuses on telecommunications companies implementing SDN for network function virtualization, service orchestration, and operational efficiency improvements. This category enables service providers to reduce operational costs, accelerate service deployment, and improve network agility while supporting diverse customer requirements and service level agreements.

Network Administrators benefit significantly from SDN implementations through centralized management capabilities, automated configuration processes, and improved visibility into network operations. The technology reduces manual configuration tasks, minimizes human errors, and enables more efficient troubleshooting and optimization processes. Administrators can implement network changes more quickly and consistently across distributed infrastructure.

IT Executives realize strategic value through reduced operational costs, improved network agility, and enhanced security capabilities. SDN solutions enable organizations to respond more quickly to business requirements while optimizing infrastructure investments and reducing vendor dependencies. The technology supports digital transformation initiatives and enables more efficient resource utilization.

Application Developers gain access to programmable network capabilities that enable application-aware networking, quality of service optimization, and dynamic resource allocation. SDN APIs provide developers with network control capabilities that were previously unavailable, enabling innovative applications and services that leverage network programmability.

Business Leaders benefit from improved operational efficiency, reduced costs, and enhanced competitive capabilities enabled by SDN implementations. The technology supports business agility, enables rapid service deployment, and provides the network foundation necessary for digital business initiatives and customer experience improvements.

Strengths:

Weaknesses:

Opportunities:

Threats:

Intent-Based Networking emerges as a significant trend, with SDN solutions incorporating artificial intelligence and machine learning capabilities to automatically translate business intent into network policies and configurations. This evolution reduces manual configuration requirements and enables more intelligent network management through automated decision-making and policy enforcement.

Multi-Cloud Networking drives SDN innovation as organizations require seamless connectivity and consistent policy enforcement across diverse cloud platforms and on-premises infrastructure. SDN solutions increasingly focus on providing unified management and control across hybrid and multi-cloud environments while maintaining security and performance standards.

Network Security Integration becomes increasingly important as organizations seek to embed security capabilities directly into SDN architectures. Micro-segmentation, zero-trust networking, and automated threat response capabilities are becoming standard features in SDN solutions, providing enhanced security posture and compliance capabilities.

Open Source Adoption continues to influence market development, with organizations increasingly evaluating open-source SDN solutions for cost optimization and vendor independence. Projects like OpenDaylight, ONOS, and Kubernetes networking continue to mature and gain enterprise adoption, particularly among organizations with strong technical capabilities.

Strategic acquisitions continue to reshape the competitive landscape, with major networking vendors acquiring specialized SDN companies to enhance solution portfolios and market capabilities. Recent acquisitions focus on expanding SDN controller capabilities, network analytics, and security integration features that address evolving customer requirements.

Partnership initiatives strengthen vendor ecosystems through collaborative development programs, integration partnerships, and joint go-to-market strategies. These partnerships enable comprehensive solution offerings while reducing customer implementation complexity and expanding market reach for participating organizations.

Standards development progresses through industry organizations and consortiums working to improve interoperability and reduce vendor lock-in risks. MWR analysis indicates that 70% of enterprises consider standards compliance a critical factor in SDN vendor selection decisions, driving continued standardization efforts.

Technology integration advances through initiatives combining SDN with complementary technologies including network function virtualization, artificial intelligence, and edge computing platforms. These integrations create more comprehensive solutions that address broader customer requirements and use cases.

Implementation Planning requires organizations to conduct thorough network assessments, develop comprehensive migration strategies, and establish clear success metrics before beginning SDN deployments. Successful implementations typically involve phased approaches that minimize disruption while demonstrating value through pilot projects and gradual expansion.

Vendor Selection should focus on solution compatibility with existing infrastructure, long-term vendor viability, and alignment with organizational technical capabilities and strategic objectives. Organizations should evaluate vendor roadmaps, support capabilities, and ecosystem partnerships to ensure sustainable long-term relationships.

Skills Development represents a critical success factor for SDN implementations, requiring organizations to invest in training programs, certification initiatives, and potentially external expertise to ensure successful deployment and ongoing operations. Building internal SDN capabilities reduces long-term operational risks and costs.

Security Considerations must be integrated throughout SDN planning and implementation processes, including controller security, network segmentation, and policy enforcement capabilities. Organizations should implement comprehensive security frameworks that address the unique risks and opportunities associated with software-defined networking architectures.

Market evolution will continue to be driven by increasing demand for network agility, cost optimization, and support for emerging technologies including 5G, edge computing, and artificial intelligence applications. The market is expected to maintain strong growth momentum as organizations recognize the strategic value of programmable network infrastructure for competitive advantage and operational efficiency.

Technology advancement will focus on improving automation capabilities, enhancing security integration, and expanding support for diverse deployment models including cloud-native and edge computing environments. MarkWide Research projects that organizations implementing advanced SDN capabilities will achieve 65% improvement in network operational efficiency over the next five years.

Industry adoption will expand beyond early adopter segments to include mainstream enterprises and smaller organizations as solutions become more accessible and implementation complexity decreases. Managed service offerings and cloud-based SDN solutions will enable broader market adoption by reducing technical barriers and implementation costs.

Ecosystem development will strengthen through continued vendor partnerships, standards advancement, and integration with complementary technologies. The market will benefit from improved interoperability, reduced vendor lock-in risks, and more comprehensive solution offerings that address diverse customer requirements and use cases.

The Software-Defined Networking market represents a fundamental transformation in network infrastructure management, providing organizations with unprecedented flexibility, control, and efficiency in network operations. The market demonstrates strong growth potential driven by digital transformation initiatives, cloud computing adoption, and the increasing complexity of modern network requirements that traditional networking approaches cannot adequately address.

Strategic implementation of SDN solutions enables organizations to achieve significant operational benefits including cost reduction, improved agility, and enhanced security capabilities. Success requires careful planning, appropriate vendor selection, and investment in necessary skills and expertise to realize the full potential of software-defined networking technologies.

Future market development will be shaped by emerging technologies, evolving customer requirements, and continued innovation from vendors and technology partners. Organizations that strategically adopt SDN solutions will be better positioned to support digital business initiatives, respond to changing market conditions, and maintain competitive advantage in an increasingly connected world.

What is Software-Defined Networking (SDN)?

Software-Defined Networking (SDN) is an approach to computer networking that allows network administrators to manage network services through abstraction of lower-level functionality. It separates the control plane from the data plane, enabling more flexible and efficient network management.

What are the key companies in the Software-Defined Networking (SDN) Market?

Key companies in the Software-Defined Networking (SDN) Market include Cisco Systems, VMware, Arista Networks, and Juniper Networks, among others.

What are the main drivers of growth in the Software-Defined Networking (SDN) Market?

The main drivers of growth in the Software-Defined Networking (SDN) Market include the increasing demand for network automation, the need for improved network management efficiency, and the rise of cloud computing and virtualization technologies.

What challenges does the Software-Defined Networking (SDN) Market face?

Challenges in the Software-Defined Networking (SDN) Market include security concerns related to centralized control, the complexity of integration with existing infrastructure, and the need for skilled personnel to manage SDN environments.

What opportunities exist in the Software-Defined Networking (SDN) Market?

Opportunities in the Software-Defined Networking (SDN) Market include the expansion of IoT applications, the growing demand for enhanced network security solutions, and the potential for innovative service delivery models in various industries.

What trends are shaping the Software-Defined Networking (SDN) Market?

Trends shaping the Software-Defined Networking (SDN) Market include the adoption of artificial intelligence for network management, the integration of SDN with edge computing, and the increasing focus on network slicing for improved service delivery.

Software-Defined Networking (SDN) Market

| Segmentation Details | Description |

|---|---|

| Deployment | On-Premises, Cloud-Based, Hybrid, Multi-Cloud |

| Solution | Network Virtualization, SD-WAN, Network Automation, Security Solutions |

| End User | Telecommunications, BFSI, Government, Education |

| Technology | OpenFlow, Network Function Virtualization, API Management, Software Analytics |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Software-Defined Networking (SDN) Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA