444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

Smart fleet management refers to the use of advanced technologies and software applications to optimize the operation and management of commercial vehicle fleets. It involves the integration of various technologies such as GPS tracking, telematics, and data analytics to improve fleet efficiency, reduce costs, enhance driver safety, and ensure regulatory compliance. Smart fleet management solutions provide real-time visibility into fleet operations, enabling fleet managers to make informed decisions and streamline their operations effectively.

Meaning

Smart fleet management encompasses a range of applications and technologies designed to enhance the performance and productivity of fleet operations. It includes features such as vehicle tracking, route optimization, fuel management, maintenance scheduling, driver behavior monitoring, and more. These solutions leverage the power of data and analytics to provide actionable insights and enable efficient fleet management.

Executive Summary

The global smart fleet management market has witnessed significant growth in recent years, driven by the increasing need for operational efficiency, the rising demand for real-time tracking and monitoring, and the growing focus on reducing carbon emissions. The market is characterized by the presence of numerous solution providers offering a wide range of innovative products and services.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The smart fleet management market is highly dynamic and driven by several factors. Technological advancements, changing customer expectations, and government regulations play a crucial role in shaping the market dynamics. The market is witnessing intense competition, with key players focusing on product innovation, strategic partnerships, and mergers and acquisitions to gain a competitive edge. Additionally, the increasing demand for integrated solutions that offer end-to-end fleet management capabilities is driving market growth.

Regional Analysis

The smart fleet management market is geographically segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. North America holds a significant market share, driven by the early adoption of advanced technologies, stringent regulatory norms, and the presence of major solution providers. Europe is also a prominent market, characterized by the growing demand for sustainable transportation solutions and the presence of well-established automotive and transportation industries. The Asia Pacific region is expected to witness rapid growth, fueled by increasing investments in infrastructure development, rising disposable income, and the growing need for efficient fleet management solutions.

Competitive Landscape

Leading Companies in the Smart Fleet Management Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

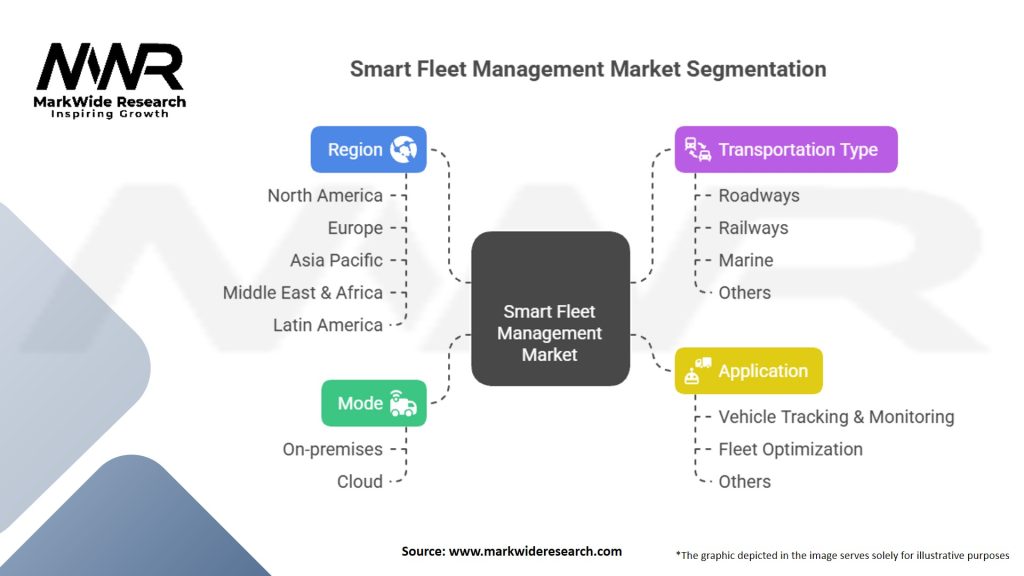

The smart fleet management market can be segmented based on solution type, connectivity, vehicle type, and end-use industry. The solution type segment includes tracking and monitoring, optimization, predictive maintenance, and others. Based on connectivity, the market can be categorized into cellular and satellite connectivity. Vehicle type segmentation includes commercial vehicles, passenger cars, and others. The end-use industry segment comprises transportation and logistics, government, automotive, and others.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact

The COVID-19 pandemic has had a significant impact on the smart fleet management market. The restrictions imposed to curb the spread of the virus disrupted supply chains, reduced transportation activities, and impacted fleet operations globally. However, the pandemic also highlighted the importance of efficient fleet management and real-time visibility into operations. As businesses recover and adapt to the new normal, the demand for smart fleet management solutions is expected to rebound, driven by the need for operational efficiency, cost optimization, and improved safety measures.

Key Industry Developments

Analyst Suggestions

Future Outlook

The future of the smart fleet management market looks promising, with continued growth expected in the coming years. Advancements in technology, increasing adoption of connected vehicles, and the rising need for operational efficiency are key factors driving market growth. The market is likely to witness further consolidation as larger players acquire smaller ones to expand their product portfolios and customer base. Additionally, the integration of AI, IoT, and blockchain technologies is expected to revolutionize fleet management practices and open up new avenues of growth.

Conclusion

The smart fleet management market is experiencing significant growth, driven by the need for operational efficiency, real-time tracking and monitoring, and cost optimization. The integration of advanced technologies such as IoT, AI, and data analytics is transforming the way fleet operations are managed. Fleet operators are increasingly adopting smart fleet management solutions to enhance productivity, reduce costs, improve driver safety, and comply with regulations. With the market evolving rapidly, stakeholders need to stay abreast of the latest trends, invest in innovation, and collaborate to capitalize on the immense opportunities offered by smart fleet management.

What is Smart Fleet Management?

Smart Fleet Management refers to the use of technology and data analytics to optimize the operation and maintenance of vehicle fleets. It encompasses various applications such as route optimization, vehicle tracking, and maintenance scheduling to enhance efficiency and reduce costs.

Who are the key players in the Smart Fleet Management Market?

Key players in the Smart Fleet Management Market include companies like Geotab, Verizon Connect, and Fleet Complete, which provide solutions for vehicle tracking and fleet optimization, among others.

What are the main drivers of growth in the Smart Fleet Management Market?

The main drivers of growth in the Smart Fleet Management Market include the increasing demand for operational efficiency, the rise in fuel prices, and the need for compliance with regulations regarding vehicle emissions and safety.

What challenges does the Smart Fleet Management Market face?

Challenges in the Smart Fleet Management Market include data privacy concerns, the high initial investment for technology implementation, and the complexity of integrating new systems with existing fleet operations.

What future opportunities exist in the Smart Fleet Management Market?

Future opportunities in the Smart Fleet Management Market include the integration of artificial intelligence for predictive maintenance, the expansion of electric vehicle fleets, and the development of more sophisticated telematics solutions.

What trends are shaping the Smart Fleet Management Market?

Trends shaping the Smart Fleet Management Market include the increasing adoption of cloud-based solutions, the use of big data analytics for decision-making, and the growing emphasis on sustainability and reducing carbon footprints in fleet operations.

Smart Fleet Management Market

| Segmentation | Details |

|---|---|

| Mode | On-premises, Cloud |

| Transportation Type | Roadways, Railways, Marine, Others |

| Application | Vehicle Tracking & Monitoring, Fleet Optimization, Others |

| Region | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Smart Fleet Management Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA