444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Singapore Intensive Care Unit (ICU) beds and surfaces market represents a critical component of the nation’s healthcare infrastructure, experiencing significant transformation driven by technological advancement and evolving patient care requirements. Singapore’s healthcare system, renowned for its excellence and innovation, continues to invest heavily in advanced ICU equipment to maintain its position as a regional medical hub. The market encompasses specialized hospital beds, mattresses, overlays, and support surfaces designed specifically for critical care environments.

Market dynamics indicate robust growth potential, with the sector expanding at a compound annual growth rate (CAGR) of 6.8% over the forecast period. This growth trajectory reflects Singapore’s commitment to healthcare excellence and the increasing demand for sophisticated critical care solutions. The integration of smart technologies, pressure redistribution systems, and infection control features has become paramount in modern ICU bed design.

Healthcare infrastructure development across Singapore’s public and private sectors continues to drive demand for premium ICU beds and surfaces. The market benefits from government initiatives supporting healthcare modernization, aging population demographics, and the country’s strategic positioning as a medical tourism destination. Advanced features such as automated positioning, integrated monitoring systems, and antimicrobial surfaces are increasingly becoming standard requirements.

The Singapore Intensive Care Unit (ICU) beds and surfaces market refers to the comprehensive ecosystem of specialized medical equipment designed to provide optimal support and care for critically ill patients within Singapore’s healthcare facilities. This market encompasses a wide range of products including electric hospital beds, therapeutic mattresses, pressure-relieving overlays, and advanced support surfaces specifically engineered for intensive care environments.

ICU beds and surfaces serve as fundamental infrastructure components that directly impact patient outcomes, comfort, and recovery rates in critical care settings. These specialized products incorporate advanced technologies such as pressure mapping, temperature regulation, moisture management, and integrated patient monitoring capabilities. The market includes both replacement and new installation segments across public hospitals, private healthcare facilities, and specialized medical centers throughout Singapore.

Singapore’s ICU beds and surfaces market demonstrates strong growth momentum, driven by healthcare system modernization and increasing critical care capacity requirements. The market benefits from Singapore’s position as a regional healthcare leader, with approximately 78% of healthcare facilities planning equipment upgrades within the next three years. Government healthcare spending and private sector investments continue to fuel market expansion.

Key market characteristics include the dominance of electric and semi-electric bed segments, growing adoption of smart mattress technologies, and increasing emphasis on infection prevention features. The market serves diverse end-users including public hospitals, private medical centers, and specialized critical care facilities. Technological integration remains a primary differentiator, with facilities prioritizing beds offering comprehensive patient monitoring and automated adjustment capabilities.

Competitive landscape analysis reveals a mix of international manufacturers and local distributors serving Singapore’s market. The sector benefits from strong regulatory frameworks ensuring product quality and safety standards. Market growth is supported by demographic trends, medical tourism expansion, and continuous healthcare infrastructure development across the island nation.

Strategic market insights reveal several critical factors shaping Singapore’s ICU beds and surfaces landscape:

Primary market drivers propelling Singapore’s ICU beds and surfaces sector include demographic shifts, healthcare infrastructure expansion, and technological advancement. The aging population represents a fundamental driver, with citizens aged 65 and above projected to comprise 25% of the population by 2030, significantly increasing critical care demand.

Healthcare system modernization initiatives continue driving market growth, as Singapore maintains its commitment to world-class medical care standards. Government healthcare spending increases support facility upgrades and equipment replacement cycles. The nation’s strategic focus on becoming a regional medical hub attracts international patients requiring advanced critical care services.

Technological innovation serves as a crucial market driver, with healthcare facilities seeking beds offering integrated monitoring, automated positioning, and data connectivity features. Patient safety regulations and quality improvement initiatives mandate advanced bed technologies capable of reducing complications and improving outcomes. The growing emphasis on patient experience and comfort drives demand for premium ICU surfaces and support systems.

Medical tourism expansion creates additional demand for high-quality ICU beds and surfaces, as international patients expect premium care environments. Private healthcare sector growth contributes to market expansion, with facilities investing in state-of-the-art equipment to maintain competitive advantages.

Market constraints affecting Singapore’s ICU beds and surfaces sector include high capital investment requirements, complex procurement processes, and space limitations within existing healthcare facilities. The substantial upfront costs associated with premium ICU beds and advanced surface technologies can strain healthcare budgets, particularly for smaller private facilities.

Regulatory compliance challenges present ongoing constraints, as manufacturers must navigate Singapore’s stringent medical device approval processes. The complexity of integrating new bed systems with existing hospital infrastructure creates implementation barriers. Staff training requirements and change management processes can delay adoption of advanced ICU bed technologies.

Space constraints within Singapore’s urban healthcare environment limit expansion possibilities, requiring careful planning for ICU bed installations. The need for specialized maintenance and technical support capabilities can restrict product choices to manufacturers with established local presence. Competition for healthcare funding across multiple priorities may impact ICU bed replacement schedules.

Supply chain considerations occasionally affect product availability and delivery timelines, particularly for specialized or customized ICU bed configurations. The requirement for comprehensive validation and testing procedures can extend implementation timelines for new bed technologies.

Significant market opportunities exist within Singapore’s ICU beds and surfaces sector, driven by healthcare expansion plans, technological advancement, and regional market positioning. The development of new healthcare facilities and expansion of existing hospitals creates substantial demand for modern ICU equipment. MarkWide Research analysis indicates that facility expansion projects represent approximately 40% of market opportunity over the next five years.

Smart healthcare initiatives present opportunities for ICU bed manufacturers offering connected devices and data analytics capabilities. The integration of artificial intelligence and machine learning technologies into bed systems creates new value propositions for healthcare providers. Telemedicine expansion and remote patient monitoring trends support demand for beds with advanced connectivity features.

Regional market expansion opportunities emerge as Singapore-based healthcare providers extend services throughout Southeast Asia. The growing medical tourism sector creates demand for premium ICU beds and surfaces that meet international patient expectations. Sustainability initiatives and green healthcare trends open opportunities for environmentally friendly bed technologies.

Specialized care segments including pediatric ICU, cardiac care, and neurological intensive care units require customized bed solutions, creating niche market opportunities. The development of home-based intensive care services presents emerging opportunities for portable and adaptable ICU bed technologies.

Market dynamics within Singapore’s ICU beds and surfaces sector reflect the interplay between healthcare policy, technological innovation, and patient care requirements. The competitive landscape features established international manufacturers competing alongside specialized medical equipment distributors. Price sensitivity varies significantly between public and private healthcare sectors, with public facilities emphasizing value-based procurement while private facilities prioritize premium features.

Innovation cycles drive continuous product development, with manufacturers introducing enhanced features approximately every 18-24 months. The market demonstrates strong correlation between technological advancement and adoption rates, particularly for beds offering measurable patient outcome improvements. Healthcare facility decision-making processes typically involve multidisciplinary teams evaluating clinical, financial, and operational factors.

Regulatory environment stability supports market growth, with clear guidelines facilitating product approvals and market entry. The emphasis on evidence-based purchasing decisions drives demand for ICU beds with documented clinical benefits and outcome improvements. Market consolidation trends among distributors create opportunities for direct manufacturer relationships with healthcare facilities.

Customer preferences increasingly favor comprehensive solutions including beds, surfaces, and ongoing support services. The market benefits from strong relationships between suppliers and healthcare providers, facilitating collaborative product development and customization initiatives.

Comprehensive research methodology employed for analyzing Singapore’s ICU beds and surfaces market incorporates multiple data collection and analysis techniques. Primary research includes structured interviews with healthcare facility administrators, ICU department heads, and procurement specialists across Singapore’s public and private healthcare sectors. Survey methodologies capture quantitative data regarding purchasing patterns, technology preferences, and future investment plans.

Secondary research components encompass analysis of government healthcare statistics, regulatory filings, and industry publications. Market sizing calculations utilize healthcare facility databases, bed capacity information, and replacement cycle analysis. Competitive intelligence gathering includes manufacturer product portfolios, pricing strategies, and market positioning analysis.

Data validation processes ensure research accuracy through triangulation of multiple information sources. Expert interviews with medical equipment specialists and healthcare technology consultants provide additional market insights. Financial analysis of healthcare facility budgets and capital expenditure plans supports market opportunity assessment.

Forecasting methodologies incorporate demographic projections, healthcare capacity expansion plans, and technology adoption curves. The research framework accounts for regulatory changes, policy initiatives, and economic factors affecting healthcare spending patterns in Singapore.

Singapore’s healthcare landscape demonstrates geographic concentration within key medical districts, with the Central Region accounting for approximately 55% of ICU bed capacity. The Singapore General Hospital campus and surrounding medical facilities represent the largest concentration of critical care beds, driving significant equipment demand. Private healthcare facilities in the Orchard Road and Novena areas contribute substantially to premium ICU bed market segments.

Regional distribution patterns reflect Singapore’s urban planning approach, with healthcare facilities strategically located to serve population centers. The Eastern Region, including Changi General Hospital and specialized medical centers, represents approximately 25% of market demand. Western Region facilities, including National University Hospital and associated medical complexes, account for the remaining market share.

Infrastructure development projects across different regions create varying market opportunities. The upcoming Woodlands Health Campus and other planned healthcare facilities will significantly impact regional demand patterns. Specialized medical centers focusing on cardiac care, oncology, and neurosciences drive demand for customized ICU bed solutions.

Accessibility considerations influence ICU bed specifications, with facilities serving diverse patient populations requiring adaptable and inclusive design features. The concentration of medical tourism activities in central Singapore creates demand for premium ICU beds meeting international patient expectations.

Competitive landscape analysis reveals a diverse ecosystem of international manufacturers, regional distributors, and specialized service providers serving Singapore’s ICU beds and surfaces market. The market features several key players with established presence and strong customer relationships:

Market competition centers on technological innovation, clinical outcomes, and comprehensive service support. Manufacturers differentiate through advanced features such as integrated patient monitoring, automated positioning systems, and pressure redistribution technologies. Local distribution partnerships and service capabilities significantly influence competitive positioning within Singapore’s market.

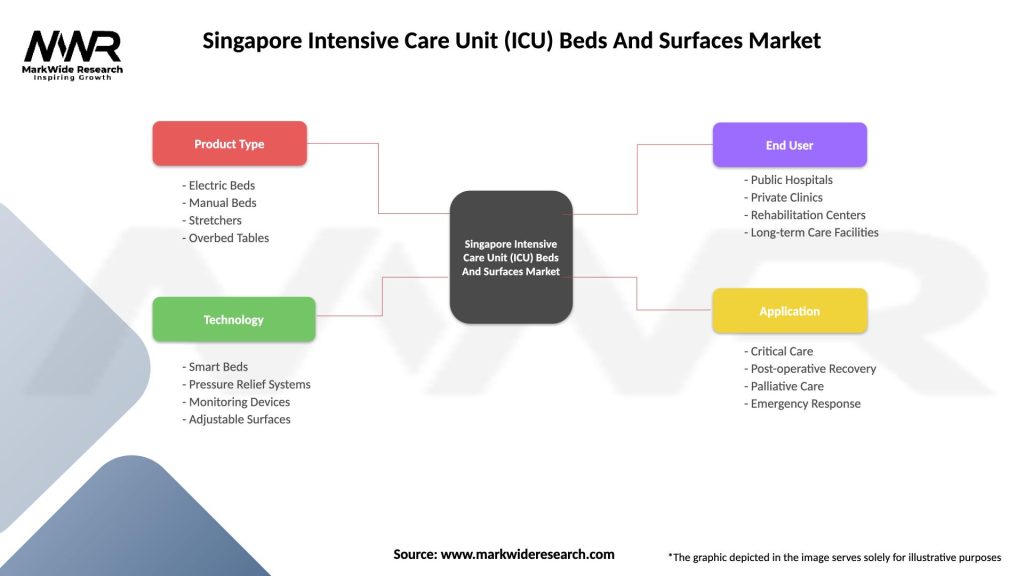

Market segmentation analysis reveals distinct categories based on product type, technology level, and end-user requirements. The ICU beds and surfaces market demonstrates clear segmentation patterns reflecting diverse healthcare facility needs and patient care protocols.

By Product Type:

By Technology Level:

By End User:

Electric ICU beds dominate Singapore’s market, representing approximately 70% of new installations due to their comprehensive functionality and clinical benefits. These beds offer advanced positioning capabilities, integrated patient monitoring, and automated adjustment features that improve patient outcomes and reduce caregiver workload. Healthcare facilities prioritize electric beds for their ability to support complex care protocols and enhance patient safety.

Therapeutic mattresses and surfaces constitute a rapidly growing segment, driven by increased awareness of pressure ulcer prevention and patient comfort requirements. Advanced materials and technologies including memory foam, gel systems, and alternating pressure capabilities create significant value for critical care applications. The integration of temperature regulation and moisture management features enhances patient comfort and clinical outcomes.

Smart bed technologies represent the fastest-growing category, with healthcare facilities increasingly adopting connected devices offering data analytics and remote monitoring capabilities. These systems provide valuable insights into patient movement, sleep patterns, and vital signs, supporting evidence-based care decisions. The integration with hospital information systems creates comprehensive patient care platforms.

Specialized ICU applications including pediatric, cardiac, and neurological intensive care units require customized bed solutions with specific features and capabilities. These niche segments command premium pricing and offer opportunities for manufacturers with specialized expertise and product portfolios.

Healthcare providers benefit significantly from advanced ICU beds and surfaces through improved patient outcomes, enhanced operational efficiency, and reduced complications. Modern bed technologies support evidence-based care protocols, reduce caregiver workload, and improve patient satisfaction scores. The integration of monitoring and data collection capabilities enables continuous quality improvement initiatives.

Patients and families experience enhanced comfort, safety, and care quality through advanced ICU bed technologies. Pressure redistribution systems reduce complications, while positioning capabilities improve respiratory function and circulation. The integration of communication and entertainment features enhances the patient experience during critical care stays.

Healthcare staff benefit from ergonomic design features, automated positioning capabilities, and integrated monitoring systems that reduce physical strain and improve workflow efficiency. Advanced bed technologies support safe patient handling practices and reduce the risk of workplace injuries. Training and education programs enhance staff competency and confidence in using advanced equipment.

Manufacturers and suppliers benefit from Singapore’s stable healthcare market, strong regulatory framework, and commitment to quality care standards. The market offers opportunities for innovation, premium pricing, and long-term customer relationships. MWR analysis indicates that successful suppliers achieve customer retention rates exceeding 85% through comprehensive service support.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation represents the most significant trend shaping Singapore’s ICU beds and surfaces market, with healthcare facilities increasingly adopting smart bed technologies offering connectivity, data analytics, and remote monitoring capabilities. The integration of Internet of Things (IoT) sensors and artificial intelligence creates comprehensive patient monitoring platforms that support evidence-based care decisions.

Infection prevention focus has intensified following global health challenges, driving demand for ICU beds with antimicrobial surfaces, easy-clean designs, and contactless operation features. Healthcare facilities prioritize beds offering superior infection control capabilities and supporting strict hygiene protocols. The development of self-sanitizing surfaces and UV-resistant materials represents emerging technological trends.

Patient-centered design trends emphasize comfort, dignity, and family involvement in critical care environments. Modern ICU beds incorporate features supporting patient communication, entertainment, and family interaction while maintaining clinical functionality. The integration of ambient lighting, noise reduction, and privacy features enhances the healing environment.

Sustainability initiatives influence ICU bed selection, with healthcare facilities increasingly considering environmental impact, energy efficiency, and recyclability factors. Manufacturers respond with eco-friendly materials, energy-efficient motors, and sustainable manufacturing processes. The development of modular designs supporting component replacement and upgrades extends product lifecycles.

Recent industry developments highlight the dynamic nature of Singapore’s ICU beds and surfaces market, with several significant announcements and innovations shaping the competitive landscape. Major healthcare facility expansions and modernization projects create substantial equipment procurement opportunities across both public and private sectors.

Technology partnerships between ICU bed manufacturers and healthcare technology companies accelerate innovation in connected devices and data analytics capabilities. The development of integrated platforms combining bed technologies with hospital information systems creates comprehensive patient care solutions. Artificial intelligence integration enables predictive analytics for patient monitoring and care optimization.

Regulatory updates from Singapore’s Health Sciences Authority continue refining medical device approval processes and quality standards. New guidelines addressing cybersecurity requirements for connected medical devices impact smart bed development and implementation strategies. The emphasis on clinical evidence and outcome measurement influences product development priorities.

Market consolidation activities among distributors and service providers create opportunities for direct manufacturer relationships with healthcare facilities. Strategic partnerships between international manufacturers and local service providers enhance market access and customer support capabilities. The development of comprehensive service networks supports complex ICU bed installations and maintenance requirements.

Strategic recommendations for stakeholders in Singapore’s ICU beds and surfaces market emphasize the importance of technology integration, comprehensive service support, and evidence-based value propositions. Healthcare facilities should prioritize beds offering measurable clinical benefits, operational efficiency improvements, and long-term cost effectiveness.

Manufacturers should focus on developing smart bed technologies with robust data analytics capabilities, seamless integration with hospital information systems, and comprehensive cybersecurity features. The ability to demonstrate clinical outcomes and return on investment becomes increasingly important for market success. Local service capabilities and rapid response times represent critical competitive advantages.

Healthcare providers are advised to adopt comprehensive evaluation frameworks considering clinical benefits, operational impact, and total cost of ownership when selecting ICU beds and surfaces. The integration of staff training programs and change management initiatives ensures successful technology adoption. Collaboration with manufacturers during product development creates customized solutions meeting specific facility requirements.

Investment in research and development remains crucial for manufacturers seeking to maintain competitive positioning in Singapore’s sophisticated healthcare market. The development of specialized solutions for niche applications and emerging care models creates differentiation opportunities. MarkWide Research recommends focusing on sustainability features and environmental considerations as increasingly important selection criteria.

Future market prospects for Singapore’s ICU beds and surfaces sector remain highly positive, supported by continued healthcare infrastructure development, demographic trends, and technological advancement. The market is projected to maintain robust growth momentum, with smart bed technologies and integrated monitoring systems driving premium segment expansion.

Demographic projections indicate sustained demand growth, with Singapore’s aging population requiring increased critical care capacity. The expansion of medical tourism and regional healthcare services creates additional market opportunities. Healthcare facility modernization programs and replacement cycles support consistent equipment demand over the forecast period.

Technology evolution will continue shaping market dynamics, with artificial intelligence, machine learning, and advanced sensors creating new capabilities for ICU beds and surfaces. The development of predictive analytics and personalized care protocols enhances the value proposition of smart bed technologies. Integration with telemedicine platforms and remote monitoring systems supports emerging care delivery models.

Market maturation is expected to drive consolidation among suppliers and increased emphasis on comprehensive service offerings. The development of outcome-based pricing models and performance guarantees may reshape commercial relationships between manufacturers and healthcare providers. Sustainability considerations and environmental impact assessments will become standard requirements for equipment procurement decisions.

Singapore’s ICU beds and surfaces market represents a dynamic and growing sector within the nation’s healthcare ecosystem, characterized by technological innovation, quality focus, and strong growth prospects. The market benefits from Singapore’s commitment to healthcare excellence, supportive regulatory environment, and strategic positioning as a regional medical hub.

Key success factors for market participants include technology leadership, comprehensive service support, and evidence-based value propositions. The integration of smart technologies, infection control features, and patient-centered design elements creates significant opportunities for differentiation and premium positioning. Healthcare facilities increasingly prioritize beds offering measurable clinical benefits and operational efficiency improvements.

Future market development will be shaped by demographic trends, healthcare expansion plans, and continued technological advancement. The emphasis on connected devices, data analytics, and integrated care platforms creates substantial opportunities for innovative manufacturers and service providers. Singapore’s ICU beds and surfaces market is well-positioned for sustained growth and continued evolution toward more sophisticated and effective critical care solutions.

What is Intensive Care Unit (ICU) Beds And Surfaces?

Intensive Care Unit (ICU) Beds And Surfaces refer to specialized medical equipment and materials designed for use in critical care settings. These include adjustable beds that provide comfort and support for patients, as well as surfaces that facilitate hygiene and infection control.

What are the key players in the Singapore Intensive Care Unit (ICU) Beds And Surfaces Market?

Key players in the Singapore Intensive Care Unit (ICU) Beds And Surfaces Market include companies like Hill-Rom, Stryker, and Getinge, which are known for their innovative healthcare solutions. These companies focus on developing advanced ICU beds and surfaces that enhance patient care and safety, among others.

What are the growth factors driving the Singapore Intensive Care Unit (ICU) Beds And Surfaces Market?

The growth of the Singapore Intensive Care Unit (ICU) Beds And Surfaces Market is driven by factors such as the increasing prevalence of chronic diseases, the rising number of surgical procedures, and advancements in healthcare technology. Additionally, the demand for improved patient comfort and safety in critical care settings contributes to market expansion.

What challenges does the Singapore Intensive Care Unit (ICU) Beds And Surfaces Market face?

The Singapore Intensive Care Unit (ICU) Beds And Surfaces Market faces challenges such as high costs associated with advanced medical equipment and the need for regular maintenance and training. Furthermore, regulatory compliance and the rapid pace of technological change can pose difficulties for manufacturers.

What opportunities exist in the Singapore Intensive Care Unit (ICU) Beds And Surfaces Market?

Opportunities in the Singapore Intensive Care Unit (ICU) Beds And Surfaces Market include the development of smart beds equipped with monitoring technology and the integration of telemedicine solutions. Additionally, increasing investments in healthcare infrastructure present avenues for growth.

What trends are shaping the Singapore Intensive Care Unit (ICU) Beds And Surfaces Market?

Trends shaping the Singapore Intensive Care Unit (ICU) Beds And Surfaces Market include the shift towards patient-centered care, the adoption of modular and flexible bed designs, and the emphasis on infection control materials. Innovations in bed technology, such as pressure-relieving surfaces, are also gaining traction.

Singapore Intensive Care Unit (ICU) Beds And Surfaces Market

| Segmentation Details | Description |

|---|---|

| Product Type | Electric Beds, Manual Beds, Stretchers, Overbed Tables |

| Technology | Smart Beds, Pressure Relief Systems, Monitoring Devices, Adjustable Surfaces |

| End User | Public Hospitals, Private Clinics, Rehabilitation Centers, Long-term Care Facilities |

| Application | Critical Care, Post-operative Recovery, Palliative Care, Emergency Response |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Singapore Intensive Care Unit (ICU) Beds And Surfaces Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.