Singapore’s fintech market has experienced rapid growth and transformation in recent years. Fintech, short for financial technology, refers to the application of technology to innovate and improve financial services. In Singapore, the fintech industry has emerged as a dynamic and thriving sector, fueled by a combination of government support, a robust regulatory framework, and a supportive business environment.

Meaning

Fintech encompasses a wide range of technological innovations that aim to enhance financial services. These innovations include mobile payments, digital banking, blockchain technology, peer-to-peer lending, robo-advisory services, and more. Fintech solutions are designed to streamline processes, increase efficiency, and provide customers with convenient and accessible financial services.

Executive Summary

The Singapore fintech market has witnessed significant growth over the years, driven by various factors such as increased smartphone penetration, a young and tech-savvy population, supportive government initiatives, and a favorable regulatory environment. This growth has attracted both local and international players, leading to a highly competitive landscape.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Singapore has positioned itself as a global fintech hub, attracting significant investments and fostering innovation. The country’s strategic location, strong financial infrastructure, and pro-business policies have contributed to its prominence in the fintech space.

The government of Singapore has been proactive in promoting fintech through various initiatives, including the establishment of regulatory sandboxes, fintech-friendly regulations, and financial incentives. These measures have created an environment conducive to experimentation and growth.

The adoption of fintech solutions by consumers and businesses in Singapore has been on the rise. Digital payment platforms, online lending, and digital wealth management services have gained popularity, driven by their convenience and efficiency.

Collaboration between traditional financial institutions and fintech startups has become increasingly common. Established banks and financial institutions are partnering with fintech companies to leverage their technological capabilities and improve customer experience.

Singapore’s fintech market has attracted significant venture capital funding, with investments pouring into startups across various fintech verticals. This influx of funding has provided the necessary resources for fintech companies to scale their operations and expand into new markets.

Market Drivers

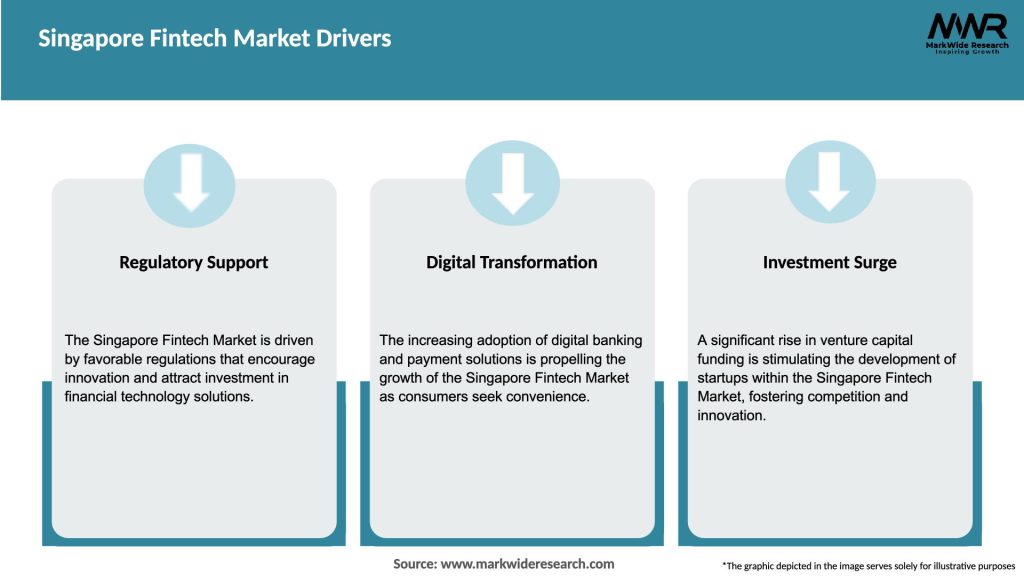

Supportive Government Initiatives: The Singapore government has introduced several initiatives to support the growth of the fintech sector. These include regulatory sandboxes, financial grants, tax incentives, and the establishment of innovation labs and accelerators.

Robust Digital Infrastructure: Singapore boasts a highly advanced digital infrastructure, including widespread internet connectivity, high smartphone penetration, and secure digital payment systems. This infrastructure provides a solid foundation for the development and adoption of fintech solutions.

Rising Consumer Demand: Consumers in Singapore are increasingly embracing digital financial services due to their convenience and accessibility. The growing demand for seamless and user-friendly financial products and services is driving the development of innovative fintech solutions.

Shift towards Cashless Payments: The government’s push for a cashless society and the increasing popularity of mobile payment platforms have created opportunities for fintech companies to develop innovative payment solutions. Cashless transactions are now the norm in many sectors, including retail, food, and transportation.

Increasing Investor Interest: Singapore’s fintech market has attracted significant interest from investors, both locally and globally. The potential for high returns, coupled with the country’s supportive ecosystem, has led to a surge in venture capital funding and investments in fintech startups.

Market Restraints

Regulatory Challenges: While Singapore has a favorable regulatory environment for fintech, navigating the regulatory landscape can still be complex. Fintech companies must comply with various regulations, including those related to data privacy, cybersecurity, and financial licensing, which can pose challenges and increase compliance costs.

Cybersecurity Risks: As fintech solutions become more prevalent, the risk of cyber threats and data breaches increases. Fintech companies must invest in robust cybersecurity measures to protect sensitive customer information and maintain trust.

Talent Shortage: The demand for skilled professionals in the fintech sector exceeds the available supply. Finding and retaining top talent with expertise in areas such as data analytics, blockchain, and cybersecurity can be a challenge for companies operating in the Singapore fintech market.

Consumer Trust and Adoption: While the adoption of fintech solutions is increasing, some consumers may still have concerns about the security and reliability of digital financial services. Building trust and promoting widespread adoption are ongoing challenges for fintech companies.

Competition from Traditional Financial Institutions: Established banks and financial institutions are also investing in fintech and digital transformation, posing competition to fintech startups. These institutions have the advantage of existing customer bases and regulatory compliance, which can be barriers for new entrants.

Market Opportunities

Digital Banking: With the issuance of digital banking licenses by the Monetary Authority of Singapore (MAS), there are opportunities for fintech companies to enter the banking space and offer innovative digital banking services. This includes neobanks, digital wallets, and virtual banking solutions.

Blockchain and Distributed Ledger Technology (DLT): Singapore has been actively exploring the potential of blockchain and DLT in areas such as trade finance, supply chain management, and cross-border payments. Fintech companies specializing in blockchain technology have opportunities to collaborate with government agencies and businesses.

Insurtech: The insurance industry in Singapore is ripe for disruption. Fintech startups focusing on insurance technology (insurtech) can leverage advanced analytics, artificial intelligence, and digital platforms to offer personalized insurance products and streamline claims processes.

Wealth Management: Singapore is known as a global wealth management hub. Fintech companies offering robo-advisory services and digital wealth management platforms have the opportunity to tap into the growing demand for personalized investment solutions.

Open Banking: The MAS has introduced guidelines for open banking, which allows customers to securely share their financial data with third-party service providers. Fintech companies can leverage open banking APIs to create innovative solutions that provide customers with a comprehensive view of their finances and personalized financial advice.

Market Dynamics

The Singapore fintech market is characterized by intense competition, continuous innovation, and evolving customer expectations. Fintech companies need to stay agile and responsive to market dynamics to succeed in this highly dynamic industry. Key dynamics shaping the market include:

Technological Advancements: The rapid pace of technological advancements, such as artificial intelligence, machine learning, and blockchain, continues to drive innovation in the fintech sector. Companies that can harness these technologies effectively will gain a competitive edge.

Evolving Customer Expectations: As customers become more digitally savvy, their expectations for seamless, personalized, and convenient financial services are increasing. Fintech companies must continuously innovate to meet these evolving expectations and deliver exceptional customer experiences.

Collaboration and Partnerships: Collaboration between fintech startups, traditional financial institutions, and other ecosystem players is becoming increasingly common. Partnerships can provide fintech companies with access to established customer bases, resources, and expertise, enabling them to scale and expand more rapidly.

Regulatory Landscape: The regulatory landscape in Singapore continues to evolve to keep pace with fintech innovation. Fintech companies must closely monitor regulatory developments and ensure compliance to maintain trust and credibility.

Global Expansion: Many Singapore-based fintech companies are looking to expand beyond the domestic market. Southeast Asia, with its large unbanked and underbanked population, presents significant growth opportunities for fintech companies seeking to expand regionally.

Regional Analysis

The Singapore fintech market serves as a gateway to Southeast Asia, one of the fastest-growing regions in terms of digital adoption and economic development. The market’s regional analysis highlights the following trends:

Southeast Asia as a Fintech Hotspot: Singapore’s strategic location and connectivity make it an ideal launchpad for fintech companies looking to expand into Southeast Asia. The region’s large population, growing middle class, and increasing smartphone penetration provide a fertile ground for fintech innovation.

Regional Collaboration: Singapore actively promotes regional collaboration in the fintech space. Initiatives such as the ASEAN Financial Innovation Network (AFIN) and the ASEAN Financial Innovation Network APIX platform facilitate collaboration and knowledge-sharing among fintech players across Southeast Asia.

Market Differences: While Southeast Asia offers immense opportunities, fintech companies need to be mindful of the diverse market landscape across countries. Each country has its own regulatory framework, cultural nuances, and levels of digital adoption, requiring localized strategies and tailored solutions.

Competition and Partnerships: Fintech companies face competition from both local and international players in the Southeast Asian market. Understanding the competitive landscape and forging strategic partnerships with local incumbents can help fintech companies gain market share and establish a strong foothold.

Competitive Landscape

Leading Companies in the Singapore Fintech Market

Grab Holdings Inc.

Sea Group (ShopeePay)

Ant Group (Alipay)

GIC Private Limited

Razer Inc.

Revolut Ltd.

TransferWise Ltd. (Wise)

Nium Pte Ltd. (InstaReM)

PolicyPal Singapore Pte Ltd.

Validus Capital Pte. Ltd.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The Singapore fintech market can be segmented based on various parameters, including:

Fintech Verticals: This segmentation categorizes fintech companies based on the specific financial services they provide, such as payments, lending, wealth management, insurance, and blockchain.

Customer Segments: Fintech solutions can be tailored for specific customer segments, such as retail consumers, small and medium-sized enterprises (SMEs), or institutional clients.

Business Models: Fintech companies can adopt different business models, including business-to-consumer (B2C), business-to-business (B2B), or peer-to-peer (P2P) models.

Technology Focus: Fintech companies may focus on specific technologies, such as artificial intelligence, blockchain, or cybersecurity, to differentiate their offerings.

Segmentation allows fintech companies to identify their target markets, tailor their products and services to specific customer needs, and gain a competitive advantage.

Category-wise Insights

Payments: The payments segment is one of the most mature and competitive in the Singapore fintech market. Fintech companies in this category offer digital payment solutions, mobile wallets, and remittance services. The adoption of digital payment platforms has increased significantly, driven by the convenience and speed they offer.

Lending and Financing: Fintech companies in this category provide alternative lending solutions, including P2P lending, invoice financing, and SME lending. These platforms leverage technology to streamline loan approval processes, provide faster access to capital, and serve underserved segments of the market.

Wealth Management: Robo-advisory platforms and digital wealth management solutions are gaining traction in Singapore. These platforms use algorithms and data analytics to offer personalized investment advice, automated portfolio management, and low-cost investment options.

Insurance: Insurtech startups are disrupting the traditional insurance industry by leveraging technology to simplify the insurance buying process, offer personalized products, and streamline claims management. Digital platforms and AI-powered solutions are transforming the insurance value chain.

Blockchain and Cryptocurrency: Fintech companies focusing on blockchain technology and cryptocurrency-related services are exploring use cases in areas such as cross-border payments, supply chain management, and digital identity verification. Singapore is actively promoting blockchain adoption and fostering blockchain-based innovation.

Key Benefits for Industry Participants and Stakeholders

Enhanced Efficiency: Fintech solutions automate manual processes, reduce paperwork, and improve operational efficiency for financial institutions. This leads to cost savings and faster service delivery.

Expanded Market Reach: Fintech companies can tap into underserved customer segments, such as the unbanked and underbanked population, by offering inclusive and accessible financial services through digital platforms.

Improved Customer Experience: Fintech solutions focus on delivering seamless, user-friendly experiences to customers. Enhanced digital interfaces, personalized recommendations, and 24/7 accessibility contribute to improved customer satisfaction.

Access to Capital: Fintech startups can attract significant investments and funding, providing them with the necessary capital to fuel growth, expand their operations, and innovate.

Collaboration Opportunities: Traditional financial institutions can collaborate with fintech companies to leverage their technological capabilities and drive innovation. Partnerships can enable incumbents to stay competitive in the digital era and offer innovative solutions to their customers.

SWOT Analysis

A SWOT (Strengths, Weaknesses, Opportunities, and Threats) analysis of the Singapore fintech market provides insights into its internal and external factors:

Strengths:

Strong Government Support: Singapore’s government has been proactive in supporting the growth of the fintech sector through various initiatives and incentives.

Robust Regulatory Framework: Singapore has established a regulatory framework that promotes innovation while ensuring consumer protection and financial stability.

Well-Developed Financial Infrastructure: Singapore boasts a world-class financial infrastructure, including a secure payment system, advanced cybersecurity measures, and a robust digital ecosystem.

Weaknesses:

Talent Shortage: The demand for skilled fintech professionals exceeds the available talent pool, leading to competition for top talent.

Regulatory Complexity: While the regulatory environment is favorable, navigating the regulatory landscape can be complex and time-consuming for fintech startups.

Customer Trust and Adoption: Building trust and widespread adoption of fintech solutions among consumers can be a challenge, especially for newer players.

Opportunities:

Regional Expansion: Singapore’s strategic location and connectivity offer opportunities for fintech companies to expand into the larger Southeast Asian market.

Digital Banking: The issuance of digital banking licenses presents opportunities for fintech companies to disrupt the traditional banking sector and offer innovative banking solutions.

Open Banking: The implementation of open banking guidelines enables fintech companies to create new value-added services by leveraging customer data.

Threats:

Regulatory Compliance: Fintech companies must stay updated with changing regulations to ensure compliance and avoid penalties.

Cybersecurity Risks: The increasing reliance on technology and digital platforms exposes fintech companies to cybersecurity threats, including data breaches and cyber attacks.

Competition from Incumbents: Traditional financial institutions are investing in fintech and digital transformation, posing competition to fintech startups. Established players have the advantage of brand recognition and customer trust.

Market Key Trends

Digital Transformation in Traditional Financial Institutions: Established banks and financial institutions are embracing digital transformation and partnering with fintech startups to enhance their service offerings and improve customer experience.

Rise of Neobanks: Digital banks, also known as neobanks, are gaining popularity in Singapore. These banks operate entirely online, offering customers a seamless and user-friendly banking experience.

Artificial Intelligence and Machine Learning: Fintech companies are leveraging AI and machine learning algorithms to enhance fraud detection, credit scoring, customer support, and personalized financial advice.

Decentralized Finance (DeFi): The emergence of DeFi platforms, built on blockchain technology, is reshaping the traditional financial ecosystem. DeFi offers decentralized lending, liquidity pooling, and yield farming opportunities.

Sustainable Finance: Fintech companies are integrating sustainability and ESG (Environmental, Social, and Governance) considerations into their products and services. This includes offering green investment options, sustainable lending, and impact-focused solutions.

Covid-19 Impact

The Covid-19 pandemic has significantly impacted the Singapore fintech market, leading to both challenges and opportunities:

Accelerated Digital Adoption: The pandemic has accelerated the shift towards digital financial services as physical interactions were restricted. Consumers and businesses increasingly turned to fintech solutions for payments, remote banking, and online transactions.

Increased Demand for Contactless Payments: The fear of virus transmission through physical currency led to a surge in contactless payments and mobile wallet usage. Fintech companies offering digital payment solutions experienced a significant increase in transaction volumes.

Focus on Financial Inclusion: The pandemic highlighted the importance of financial inclusion, particularly for vulnerable populations. Fintech solutions that enable access to financial services for the unbanked and underbanked gained prominence.

Challenges in Funding: The pandemic disrupted global investment activity, impacting funding opportunities for fintech startups. However, certain sectors such as digital payments and online lending saw increased investor interest.

Heightened Cybersecurity Risks: The rapid adoption of digital solutions increased the risk of cyber attacks and data breaches. Fintech companies had to strengthen their cybersecurity measures to protect customer data and maintain trust.

Key Industry Developments

Digital Banking Licenses: The MAS issued digital banking licenses, allowing non-bank players to operate digital banks in Singapore. This move has attracted both local and international players to enter the digital banking space.

Blockchain Innovation: Singapore has been actively exploring blockchain technology in areas such as trade finance, supply chain management, and digital identity verification. Government initiatives and collaborations with industry players aim to position Singapore as a blockchain hub.

Expansion of Payments Infrastructure: The introduction of PayNow, an instant peer-to-peer funds transfer service, and the implementation of SGQR, a unified QR code system, have contributed to the growth of the digital payments ecosystem in Singapore.

Regulatory Sandboxes: The MAS established regulatory sandboxes to facilitate fintech experimentation and innovation. These sandboxes provide a controlled environment for fintech companies to test their solutions and navigate regulatory requirements.

Collaboration with Global Fintech Hubs: Singapore has forged partnerships and collaborations with other global fintech hubs, such as London and Hong Kong, to foster knowledge exchange, promote cross-border collaboration, and drive fintech innovation.

Analyst Suggestions

Foster Collaboration: Fintech companies should actively seek collaboration opportunities with traditional financial institutions, regulatory bodies, and industry players to leverage complementary strengths and drive innovation.

Focus on Customer Trust: Building trust and ensuring data privacy and security are critical for fintech companies. Implementing robust cybersecurity measures and transparent data practices will foster customer trust and loyalty.

Address Talent Shortage: Fintech companies should invest in talent acquisition and retention strategies, including partnerships with educational institutions, training programs, and initiatives to attract skilled professionals to the industry.

Embrace Regulation and Compliance: Staying updated with regulatory requirements is crucial for fintech companies to avoid penalties and maintain trust with customers and regulators. Engaging with regulatory authorities and seeking guidance can help navigate the complex regulatory landscape.

Explore Regional Expansion: Fintech companies should consider expanding their operations beyond Singapore to tap into the growing opportunities in the broader Southeast Asian market. Localizing solutions and understanding market-specific dynamics will be key to success.

Future Outlook

The future of the Singapore fintech market is promising, driven by technological advancements, government support, and evolving customer expectations. Key trends that will shape the market include digital transformation in traditional financial institutions, the rise of neobanks, increased adoption of AI and machine learning, and the integration of sustainability into financial services. The market will continue to witness collaboration and partnerships between fintech startups and traditional incumbents, fostering innovation and driving industry growth. Regional expansion into Southeast Asia will provide significant opportunities for fintech companies to tap into the region’s large unbanked and underbanked population. However, challenges such as talent shortage, regulatory compliance, and cybersecurity risks need to be addressed to sustain growth and ensure long-term success.

Conclusion

The Singapore fintech market is a vibrant and competitive landscape, offering immense opportunities for innovation and disruption. Fintech companies are leveraging technology to transform traditional financial services, enhance customer experiences, and drive financial inclusion. The market benefits from strong government support, a robust regulatory framework, and a well-developed financial infrastructure. While challenges such as talent shortage, regulatory compliance, and cybersecurity risks exist, the market’s future outlook remains positive. Collaboration, customer trust, and continuous innovation will be crucial for fintech companies to thrive in the dynamic Singapore fintech market and expand regionally.

What is Fintech?

Fintech refers to the integration of technology into offerings by financial services companies to improve their use of financial services. This includes innovations in areas such as mobile payments, online banking, and blockchain technology.

What are the key players in the Singapore Fintech Market?

The Singapore Fintech Market features several prominent companies, including Grab Financial Group, Razer Fintech, and DBS Bank, which are known for their innovative financial solutions and services, among others.

What are the growth factors driving the Singapore Fintech Market?

Key growth factors for the Singapore Fintech Market include the increasing adoption of digital payments, a supportive regulatory environment, and the rising demand for financial inclusion and accessibility among consumers.

What challenges does the Singapore Fintech Market face?

The Singapore Fintech Market faces challenges such as regulatory compliance complexities, cybersecurity threats, and competition from traditional financial institutions that are adapting to digital trends.

What opportunities exist in the Singapore Fintech Market?

Opportunities in the Singapore Fintech Market include the expansion of blockchain technology applications, the growth of insurtech solutions, and the potential for partnerships between fintech firms and established banks to enhance service offerings.

What trends are shaping the Singapore Fintech Market?

Trends in the Singapore Fintech Market include the rise of artificial intelligence in financial services, the increasing popularity of neobanks, and the focus on sustainable finance solutions that address environmental, social, and governance (ESG) criteria.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.