444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Singapore data center networking market represents a critical infrastructure segment driving the nation’s digital transformation and smart city initiatives. As a leading financial and technological hub in Southeast Asia, Singapore has established itself as a premier destination for data center investments, with networking solutions forming the backbone of these sophisticated facilities. The market encompasses a comprehensive range of networking equipment, software solutions, and services designed to support high-performance data center operations.

Market dynamics indicate robust growth driven by increasing cloud adoption, digital transformation initiatives, and the proliferation of Internet of Things (IoT) applications across various industries. Singapore’s strategic location, coupled with its advanced telecommunications infrastructure and supportive government policies, has attracted major global technology companies to establish their regional data centers in the city-state. The market is experiencing significant expansion at a compound annual growth rate (CAGR) of 8.2%, reflecting the strong demand for advanced networking solutions.

Key market drivers include the rapid adoption of 5G technology, increasing demand for edge computing solutions, and the growing emphasis on artificial intelligence and machine learning applications. The market benefits from Singapore’s position as a regional gateway for international connectivity, with multiple submarine cables and terrestrial networks converging in the country. This strategic advantage has led to approximately 65% of multinational corporations in the Asia-Pacific region choosing Singapore as their primary data center location.

The Singapore data center networking market refers to the comprehensive ecosystem of networking infrastructure, equipment, software, and services that enable efficient data transmission, storage, and processing within data center facilities located in Singapore. This market encompasses various networking components including switches, routers, load balancers, firewalls, network management software, and related services that ensure optimal performance, security, and reliability of data center operations.

Data center networking in Singapore’s context involves the integration of advanced technologies such as software-defined networking (SDN), network function virtualization (NFV), and intent-based networking to create highly scalable and flexible infrastructure solutions. The market serves diverse sectors including financial services, telecommunications, government agencies, healthcare, and multinational corporations requiring robust data processing and storage capabilities.

Strategic importance of this market extends beyond traditional networking, encompassing cloud connectivity, hybrid infrastructure management, and edge computing solutions that support Singapore’s vision of becoming a smart nation. The networking infrastructure enables seamless connectivity between on-premises systems, public clouds, and edge locations, facilitating digital transformation initiatives across various industries.

Singapore’s data center networking market demonstrates exceptional growth potential, driven by the nation’s strategic position as a regional technology hub and its commitment to digital innovation. The market benefits from strong government support, world-class infrastructure, and a favorable regulatory environment that encourages investment in advanced networking technologies. Current market trends indicate increasing adoption of cloud-native networking solutions, with approximately 72% of enterprises implementing hybrid cloud strategies.

Key market segments include enterprise networking, service provider solutions, and hyperscale data center networking, each experiencing distinct growth patterns and technological requirements. The enterprise segment leads in terms of deployment diversity, while hyperscale facilities drive demand for high-performance, scalable networking solutions. Service providers focus on network function virtualization and software-defined networking to enhance service delivery capabilities.

Competitive landscape features a mix of global technology leaders and regional specialists, with companies investing heavily in research and development to address evolving customer requirements. The market is characterized by rapid technological advancement, with artificial intelligence and machine learning increasingly integrated into networking solutions to enable autonomous network management and optimization.

Primary market insights reveal several critical trends shaping Singapore’s data center networking landscape:

Market maturity varies across different segments, with traditional enterprise networking showing steady growth while emerging technologies like intent-based networking and network-as-a-service models experience rapid adoption rates.

Digital transformation initiatives across Singapore’s economy serve as the primary catalyst for data center networking market growth. Government-led smart nation projects, coupled with private sector digitalization efforts, create substantial demand for advanced networking infrastructure. The financial services sector, representing a significant portion of Singapore’s economy, drives demand for high-performance, low-latency networking solutions to support algorithmic trading and real-time transaction processing.

Cloud adoption acceleration continues to fuel market expansion, with organizations migrating workloads to public, private, and hybrid cloud environments. This trend necessitates sophisticated networking solutions capable of managing complex multi-cloud architectures while maintaining security and performance standards. The growing popularity of containerization and microservices architectures further amplifies the need for advanced networking capabilities.

Regulatory requirements in Singapore’s highly regulated environment drive investment in compliant networking solutions. Financial institutions, healthcare organizations, and government agencies require networking infrastructure that meets strict data protection, privacy, and security standards. These requirements often necessitate specialized networking equipment and software solutions designed for regulated environments.

Internet of Things proliferation across smart city initiatives, industrial automation, and consumer applications creates demand for networking infrastructure capable of handling massive device connectivity and data volumes. Edge computing requirements associated with IoT deployments drive demand for distributed networking solutions that can process data closer to the source.

High implementation costs associated with advanced networking solutions present significant barriers for smaller organizations and startups. The initial capital investment required for enterprise-grade networking equipment, software licenses, and professional services can be substantial, particularly for organizations requiring high-performance or specialized solutions. This cost barrier often delays adoption or forces organizations to compromise on functionality.

Skills shortage in networking expertise represents a critical challenge for market growth. The rapid evolution of networking technologies, including software-defined networking, network function virtualization, and intent-based networking, requires specialized skills that are in short supply. Organizations often struggle to find qualified personnel capable of designing, implementing, and managing advanced networking solutions.

Complexity challenges associated with modern networking solutions can overwhelm organizations lacking adequate technical expertise. The integration of multiple networking technologies, cloud platforms, and security solutions creates complex environments that require sophisticated management capabilities. This complexity can lead to implementation delays, performance issues, and increased operational costs.

Vendor lock-in concerns discourage some organizations from adopting proprietary networking solutions, particularly those requiring long-term commitments or extensive customization. Organizations prefer open, standards-based solutions that provide flexibility and avoid dependency on single vendors, which can limit market growth for proprietary technologies.

5G network deployment presents substantial opportunities for data center networking providers, as telecommunications companies and enterprises upgrade infrastructure to support next-generation wireless technologies. The low-latency requirements of 5G applications necessitate edge computing capabilities and specialized networking solutions, creating new market segments and revenue opportunities.

Artificial intelligence integration offers significant potential for networking solution providers to differentiate their offerings through intelligent automation, predictive analytics, and autonomous network management capabilities. AI-powered networking solutions can optimize performance, reduce operational costs, and enhance security, appealing to organizations seeking competitive advantages through technology innovation.

Sustainability initiatives create opportunities for energy-efficient networking solutions that help organizations reduce their environmental footprint while maintaining performance standards. Green data center initiatives and corporate sustainability commitments drive demand for networking equipment with improved power efficiency and reduced environmental impact.

Industry-specific solutions present opportunities for specialized networking providers to develop tailored solutions for specific sectors such as financial services, healthcare, manufacturing, and government. These vertical-specific solutions can command premium pricing while addressing unique regulatory, performance, and security requirements.

Technological evolution continues to reshape Singapore’s data center networking landscape, with software-defined networking and network function virtualization gaining widespread adoption. These technologies enable greater flexibility, scalability, and cost-effectiveness compared to traditional hardware-centric approaches. Organizations report achieving operational efficiency improvements of up to 40% through SDN implementation, driving continued market adoption.

Competitive intensity remains high as established networking vendors compete with emerging technology companies and cloud service providers offering networking-as-a-service solutions. This competition drives innovation while putting pressure on pricing, benefiting customers through improved value propositions and accelerated technology development.

Customer expectations continue to evolve, with organizations demanding greater automation, intelligence, and integration capabilities from their networking solutions. The shift toward outcome-based purchasing models and consumption-based pricing reflects changing customer preferences and market dynamics.

Partnership ecosystems play an increasingly important role in market dynamics, with networking vendors collaborating with cloud providers, system integrators, and technology partners to deliver comprehensive solutions. These partnerships enable vendors to address complex customer requirements while expanding their market reach and capabilities.

Comprehensive market analysis employed multiple research methodologies to ensure accuracy and reliability of findings. Primary research included structured interviews with industry executives, technology leaders, and end-users across various sectors in Singapore. Secondary research encompassed analysis of industry reports, financial statements, regulatory filings, and technology documentation from leading market participants.

Data collection processes involved systematic gathering of information from diverse sources including vendor briefings, customer case studies, industry conferences, and regulatory publications. Market sizing and forecasting utilized bottom-up and top-down approaches to validate findings and ensure consistency across different market segments and geographic regions.

Analytical frameworks incorporated quantitative and qualitative assessment techniques to evaluate market trends, competitive dynamics, and growth opportunities. Statistical analysis methods were applied to identify correlations, patterns, and significant market drivers while qualitative analysis provided context and strategic insights.

Validation procedures included cross-referencing findings with multiple sources, conducting follow-up interviews with key stakeholders, and reviewing preliminary findings with industry experts to ensure accuracy and completeness of the research outcomes.

Singapore’s unique position as a city-state creates a concentrated but highly sophisticated data center networking market. The entire country functions as a single metropolitan area with world-class infrastructure, making it an ideal location for hyperscale data centers and regional headquarters of multinational corporations. Geographic concentration enables efficient service delivery and maintenance while facilitating collaboration between market participants.

Infrastructure advantages include multiple submarine cable landing points, redundant power systems, and advanced telecommunications networks that support high-performance data center operations. Singapore’s strategic location at the intersection of major international trade routes makes it a natural hub for regional data center operations, with approximately 78% of regional internet traffic passing through Singapore-based facilities.

Government support through initiatives such as the Smart Nation program and Digital Government Blueprint creates a favorable environment for data center networking investments. Regulatory frameworks designed to attract foreign investment while maintaining high standards for data protection and cybersecurity provide stability and predictability for market participants.

Connectivity ecosystem benefits from Singapore’s role as a regional internet exchange point and telecommunications hub. The presence of multiple internet service providers, cloud service providers, and content delivery networks creates a rich ecosystem that supports diverse networking requirements and enhances the value proposition for data center operators.

Market leadership is distributed among several global technology companies and regional specialists, each bringing unique strengths and capabilities to Singapore’s data center networking market:

Competitive strategies vary among market participants, with some focusing on technology innovation while others emphasize service delivery, pricing competitiveness, or vertical market specialization. The market rewards companies that can demonstrate clear value propositions and successful customer outcomes.

Innovation focus areas include artificial intelligence integration, automation capabilities, security enhancements, and sustainability improvements. Companies investing in research and development to address emerging customer requirements maintain competitive advantages in this rapidly evolving market.

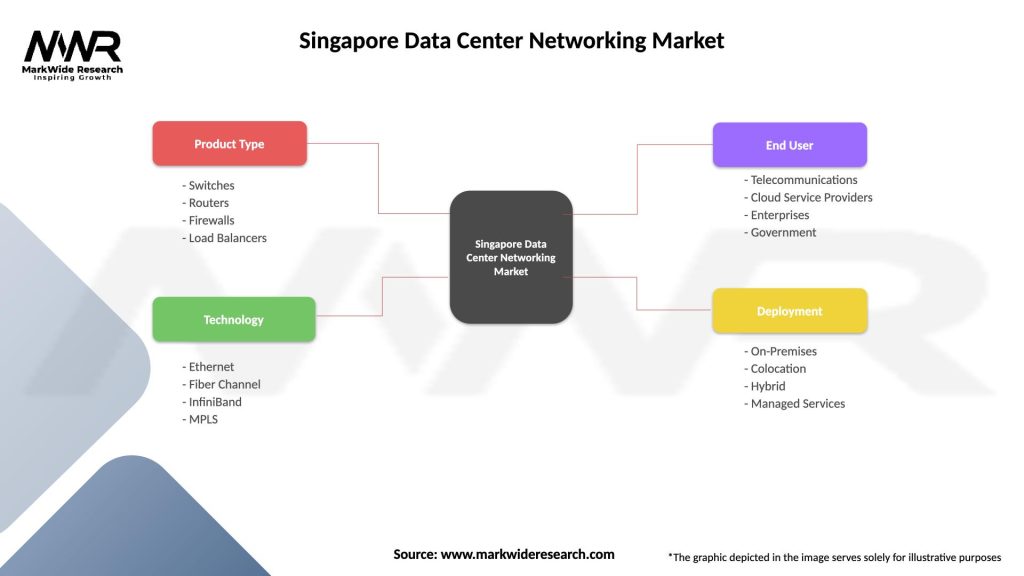

By Technology:

By Deployment Model:

By End-User:

Ethernet switching solutions represent the largest segment within Singapore’s data center networking market, driven by the fundamental requirement for high-speed, reliable connectivity within data center environments. Modern switching solutions incorporate advanced features such as software-defined networking capabilities, integrated security, and intelligent traffic management. The segment benefits from continuous technology advancement, with 25% of organizations upgrading their switching infrastructure annually to support growing bandwidth requirements.

Network security integration has become increasingly important as organizations face evolving cybersecurity threats. Integrated security solutions that combine networking and security functions in unified platforms gain popularity due to their operational efficiency and cost-effectiveness. This trend reflects the growing recognition that network security cannot be treated as an afterthought but must be built into the fundamental networking architecture.

Software-defined networking adoption continues to accelerate as organizations seek greater flexibility and automation in their networking infrastructure. SDN solutions enable centralized network management, policy enforcement, and rapid service provisioning, addressing the dynamic requirements of modern data center environments. The technology particularly appeals to organizations implementing cloud-first strategies and requiring seamless integration between on-premises and cloud resources.

Network management and analytics solutions gain importance as networking infrastructure becomes more complex and distributed. Advanced analytics capabilities enable proactive network optimization, predictive maintenance, and automated troubleshooting, reducing operational costs while improving performance and reliability.

Technology vendors benefit from Singapore’s position as a regional hub, enabling them to serve customers across Southeast Asia from a single location while leveraging world-class infrastructure and skilled workforce. The market provides opportunities for both established players and innovative startups to demonstrate their capabilities in a sophisticated, demanding environment.

End-user organizations gain access to cutting-edge networking technologies and services that enable digital transformation initiatives while maintaining high standards for security, reliability, and performance. Singapore’s competitive market environment ensures access to diverse solution options and competitive pricing.

System integrators and service providers benefit from strong demand for professional services, implementation support, and managed services as organizations seek to optimize their networking investments. The market rewards providers that can demonstrate expertise in emerging technologies and deliver measurable business outcomes.

Government and regulatory bodies benefit from a vibrant technology ecosystem that supports economic development, innovation, and competitiveness while maintaining high standards for security and compliance. The data center networking market contributes to Singapore’s position as a leading technology hub in the Asia-Pacific region.

Investment community finds attractive opportunities in a market characterized by steady growth, technological innovation, and strong fundamentals. Singapore’s stable political and economic environment, coupled with supportive regulatory frameworks, provides a favorable investment climate for technology companies and infrastructure providers.

Strengths:

Weaknesses:

Opportunities:

Threats:

Intent-based networking emerges as a transformative trend, enabling organizations to define desired network outcomes rather than managing individual network components. This approach leverages artificial intelligence and machine learning to automatically configure, monitor, and optimize network infrastructure based on business requirements and policies. Early adopters report network management efficiency improvements of 35% through intent-based networking implementation.

Edge computing proliferation drives demand for distributed networking solutions that can support processing and storage capabilities closer to end users and devices. This trend is particularly relevant for applications requiring ultra-low latency, such as autonomous vehicles, industrial automation, and augmented reality applications.

Network-as-a-Service adoption accelerates as organizations seek to reduce capital expenditure and operational complexity while accessing advanced networking capabilities. This consumption-based model appeals to organizations of all sizes, enabling them to scale networking resources based on actual requirements rather than peak capacity planning.

Zero-trust networking gains momentum as organizations recognize the limitations of traditional perimeter-based security models. This approach requires verification of every user and device attempting to access network resources, regardless of their location or previous authentication status.

Quantum-safe networking preparation begins as organizations anticipate the eventual impact of quantum computing on current cryptographic methods. Forward-thinking organizations are beginning to evaluate and implement quantum-resistant security measures to protect their networking infrastructure.

Major infrastructure investments by global cloud service providers continue to reshape Singapore’s data center landscape. Recent announcements include significant capacity expansions by leading cloud platforms, creating substantial demand for advanced networking solutions capable of supporting hyperscale operations.

Government initiatives such as the National AI Strategy and Digital Economy Framework for Action provide strategic direction and funding support for technology innovation, including advanced networking solutions. These initiatives create opportunities for local and international companies to collaborate on cutting-edge projects.

Strategic partnerships between networking vendors, system integrators, and cloud service providers enable comprehensive solution delivery and market expansion. Recent partnerships focus on areas such as multi-cloud connectivity, edge computing, and artificial intelligence integration.

Regulatory developments including updated data protection laws and cybersecurity frameworks impact networking solution requirements and create opportunities for compliant, secure networking technologies. Organizations must ensure their networking infrastructure meets evolving regulatory standards.

Technology acquisitions by major networking companies demonstrate the industry’s focus on innovation and capability expansion. Recent acquisitions target areas such as network analytics, security integration, and software-defined networking technologies.

MarkWide Research recommends that organizations prioritize networking solutions that provide flexibility, scalability, and future-readiness rather than focusing solely on current requirements. The rapid pace of technological change necessitates networking infrastructure that can adapt to evolving business needs and emerging technologies.

Investment in skills development should be a priority for organizations implementing advanced networking solutions. The complexity of modern networking technologies requires ongoing training and certification programs to ensure optimal performance and return on investment.

Security integration should be considered from the initial planning stages rather than as an add-on component. Organizations that incorporate security requirements into their networking architecture from the beginning achieve better outcomes and lower total cost of ownership.

Vendor evaluation should consider long-term viability, innovation capabilities, and ecosystem partnerships rather than focusing exclusively on current product features and pricing. The networking market’s rapid evolution makes vendor selection a strategic decision with long-term implications.

Pilot programs and proof-of-concept implementations can help organizations evaluate new networking technologies and approaches before making significant investments. This approach reduces risk while enabling organizations to gain experience with emerging technologies.

Market growth trajectory remains positive, with continued expansion expected across all major segments of Singapore’s data center networking market. The convergence of multiple technology trends, including 5G deployment, edge computing adoption, and artificial intelligence integration, creates a favorable environment for sustained market growth.

Technology evolution will continue to reshape the networking landscape, with software-defined approaches becoming increasingly prevalent across all market segments. Organizations can expect greater automation, intelligence, and integration capabilities in future networking solutions, with autonomous network management becoming a standard feature rather than a premium option.

MWR analysis indicates that the market will experience increasing consolidation as smaller vendors are acquired by larger companies seeking to expand their capabilities and market reach. This consolidation trend will likely accelerate innovation while potentially reducing the number of independent solution options available to customers.

Sustainability requirements will become increasingly important as organizations face pressure to reduce their environmental impact. Energy-efficient networking solutions and green data center initiatives will drive demand for innovative technologies that can deliver high performance while minimizing power consumption and environmental impact.

Regional integration opportunities will expand as Singapore strengthens its position as a hub for Southeast Asian digital infrastructure. Cross-border connectivity requirements and regional data center networks will create new market opportunities for networking solution providers capable of supporting distributed, multi-country operations.

Singapore’s data center networking market represents a dynamic and rapidly evolving sector that plays a crucial role in the nation’s digital economy and regional technology leadership. The market benefits from strong fundamentals including strategic location, world-class infrastructure, government support, and a sophisticated customer base with demanding requirements.

Growth prospects remain robust, driven by multiple converging trends including digital transformation acceleration, cloud adoption, 5G deployment, and emerging technologies such as artificial intelligence and edge computing. The market’s maturity and sophistication create opportunities for both established vendors and innovative newcomers to succeed through differentiated value propositions and superior customer outcomes.

Success factors for market participants include technological innovation, strong customer relationships, comprehensive service capabilities, and the ability to adapt quickly to changing market conditions. Organizations that can demonstrate clear business value and measurable outcomes will continue to thrive in this competitive environment.

Future market development will be shaped by ongoing technological advancement, evolving customer requirements, and Singapore’s continued evolution as a smart nation and regional technology hub. The Singapore data center networking market is well-positioned to maintain its growth trajectory while contributing to the broader digital transformation of the Asia-Pacific region.

What is Data Center Networking?

Data Center Networking refers to the technologies and infrastructure that connect servers, storage, and networking devices within a data center. It encompasses various components such as switches, routers, and cabling systems that facilitate data transfer and communication.

What are the key players in the Singapore Data Center Networking Market?

Key players in the Singapore Data Center Networking Market include companies like Cisco Systems, Arista Networks, and Juniper Networks, which provide essential networking solutions and services for data centers, among others.

What are the main drivers of growth in the Singapore Data Center Networking Market?

The growth of the Singapore Data Center Networking Market is driven by the increasing demand for cloud services, the rise of big data analytics, and the need for enhanced network security. These factors are pushing organizations to invest in advanced networking solutions.

What challenges does the Singapore Data Center Networking Market face?

Challenges in the Singapore Data Center Networking Market include the high costs associated with advanced networking technologies and the complexity of integrating new systems with existing infrastructure. Additionally, the rapid pace of technological change can make it difficult for companies to keep up.

What opportunities exist in the Singapore Data Center Networking Market?

Opportunities in the Singapore Data Center Networking Market include the growing adoption of edge computing and the expansion of Internet of Things (IoT) applications. These trends are creating demand for more efficient and scalable networking solutions.

What trends are shaping the Singapore Data Center Networking Market?

Trends shaping the Singapore Data Center Networking Market include the shift towards software-defined networking (SDN) and the increasing focus on energy-efficient networking solutions. Additionally, the rise of artificial intelligence in network management is transforming how data centers operate.

Singapore Data Center Networking Market

| Segmentation Details | Description |

|---|---|

| Product Type | Switches, Routers, Firewalls, Load Balancers |

| Technology | Ethernet, Fiber Channel, InfiniBand, MPLS |

| End User | Telecommunications, Cloud Service Providers, Enterprises, Government |

| Deployment | On-Premises, Colocation, Hybrid, Managed Services |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Singapore Data Center Networking Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.