444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview:

The servo motors and drives market is witnessing significant growth due to the rising demand for automation across various industries. Servo motors and drives play a crucial role in precision control systems, offering high torque, accuracy, and rapid response. These devices find extensive applications in industries such as manufacturing, automotive, aerospace, robotics, and healthcare. The market is expected to experience substantial growth in the coming years, driven by technological advancements, increasing industrial automation, and the growing adoption of robotics.

Meaning:

Servo motors and drives are electromechanical systems designed to provide precise control over the movement and position of mechanical components. They consist of a motor that converts electrical energy into mechanical energy and a drive that controls the motor’s speed, torque, and position. Servo motors and drives offer superior performance compared to traditional motors, making them ideal for applications requiring accurate motion control.

Executive Summary:

The servo motors and drives market is witnessing robust growth, driven by the increasing need for automation and precision control in various industries. This report provides a comprehensive analysis of the market, including key market insights, drivers, restraints, opportunities, and market dynamics. Additionally, it offers a regional analysis, competitive landscape, segmentation, and category-wise insights. The report also discusses the impact of COVID-19 on the market and provides future outlook and analyst suggestions.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights:

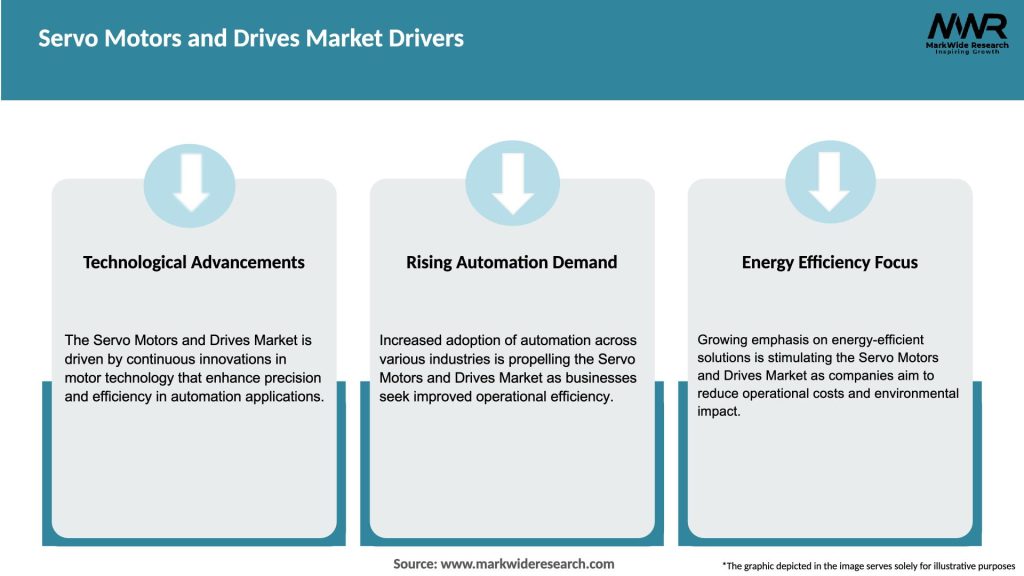

Market Drivers:

Market Restraints:

Market Opportunities:

Market Dynamics:

The servo motors and drives market is driven by several factors, including the demand for automation, technological advancements, and energy efficiency requirements. The market is highly competitive, with key players focusing on product innovations and strategic collaborations to gain a competitive edge. However, challenges such as high initial costs and a shortage of skilled professionals can hinder market growth.

Regional Analysis:

Competitive Landscape:

Leading Companies in Servo Motors and Drives Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation:

The market can be segmented based on motor type, drive type, voltage range, application, and end-use industry. Motor types include AC servo motors and DC servo motors. Drive types include analog drives and digital drives. The voltage range includes low voltage and medium/high voltage. Applications of servo motors and drives are found in robotics, machine tools, packaging, material handling, and others. End-use industries include manufacturing, automotive, aerospace, healthcare, and others.

Category-wise Insights:

Key Benefits for Industry Participants and Stakeholders:

SWOT Analysis:

Market Key Trends:

Covid-19 Impact:

The COVID-19 pandemic had a mixed impact on the servo motors and drives market. While the market experienced a temporary slowdown due to supply chain disruptions and reduced industrial activities, the need for automation and robotics in healthcare and other essential industries increased. The market has gradually recovered as industries resumed operations, and the demand for automation solutions grew.

Key Industry Developments:

Analyst Suggestions:

Future Outlook:

The servo motors and drives market is poised for significant growth in the coming years. Technological advancements, increasing automation, and the demand for precision control systems will drive market expansion. The integration of servo motors and drives with IoT, AI, and cloud computing technologies will open up new opportunities. The market is expected to witness a shift towards energy-efficient and lightweight servo motor and drive systems.

Conclusion:

The servo motors and drives market is experiencing steady growth due to the increasing demand for automation and precision control in various industries. Technological advancements, such as the integration of IoT and AI, are enhancing the capabilities of servo motors and drives. The market offers significant opportunities for industry participants, but challenges such as high initial costs and a shortage of skilled professionals need to be addressed. With continuous innovation and strategic collaborations, the servo motors and drives market is expected to thrive in the future.

What is Servo Motors and Drives?

Servo motors and drives are electromechanical devices that provide precise control of angular or linear position, velocity, and acceleration. They are widely used in applications such as robotics, CNC machinery, and automated manufacturing systems.

What are the key players in the Servo Motors and Drives Market?

Key players in the Servo Motors and Drives Market include Siemens, Mitsubishi Electric, and Rockwell Automation, among others. These companies are known for their innovative solutions and extensive product portfolios in motion control technology.

What are the growth factors driving the Servo Motors and Drives Market?

The growth of the Servo Motors and Drives Market is driven by the increasing demand for automation in manufacturing processes, the rise of robotics in various industries, and advancements in technology that enhance performance and efficiency.

What challenges does the Servo Motors and Drives Market face?

The Servo Motors and Drives Market faces challenges such as high initial costs of advanced systems, the complexity of integration with existing machinery, and the need for skilled personnel to operate and maintain these systems.

What opportunities exist in the Servo Motors and Drives Market?

Opportunities in the Servo Motors and Drives Market include the growing adoption of Industry Four Point Zero technologies, the expansion of electric vehicles requiring precise motion control, and the increasing demand for energy-efficient solutions across various sectors.

What trends are shaping the Servo Motors and Drives Market?

Trends in the Servo Motors and Drives Market include the integration of IoT technology for real-time monitoring and control, the development of more compact and efficient motor designs, and the increasing focus on sustainability and energy efficiency in manufacturing processes.

Servo Motors and Drives Market

| Segmentation Details | Description |

|---|---|

| Motor Type | AC Servo Motors, DC Servo Motors |

| Drive Type | Servo Drives, Servo Amplifiers |

| Voltage Range | Low Voltage, Medium Voltage |

| Application | Automotive, Industrial Machinery, Electronics, Healthcare, Others |

| Region | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in Servo Motors and Drives Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA