444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview The secondary smelting and alloying of aluminum market involves the process of recycling and reusing aluminum scrap to produce alloys with specific properties. This market plays a vital role in the aluminum industry’s sustainability efforts by reducing the need for primary aluminum production and conserving resources. The market has witnessed steady growth due to the increasing demand for recycled aluminum and the focus on environmental sustainability.

Meaning Secondary smelting and alloying of aluminum refer to the process of melting and refining aluminum scrap to create new alloys that meet specific performance requirements. This process involves the collection, sorting, and recycling of aluminum scrap from various sources, such as manufacturing waste, used beverage cans, and automotive parts. The recycled aluminum is then melted, refined, and alloyed to produce high-quality alloys used in various industries.

Executive Summary The secondary smelting and alloying of aluminum market has experienced significant growth in recent years, driven by factors such as the increasing demand for recycled aluminum, environmental regulations promoting sustainability, and the cost advantages of using recycled materials. The market offers opportunities for aluminum scrap recyclers, smelters, alloy manufacturers, and end-users seeking sustainable and cost-effective aluminum solutions.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics The secondary smelting and alloying of aluminum market is influenced by factors such as aluminum scrap availability, metal prices, government regulations, and the demand from end-use industries. The market is characterized by a strong focus on sustainability, quality control, and innovation in recycling processes.

Regional Analysis The demand for secondary smelting and alloying of aluminum varies across regions, influenced by factors such as industrialization, scrap collection infrastructure, recycling rates, and the presence of end-use industries. Regions with robust recycling systems and a strong manufacturing base, such as North America and Europe, have a significant market share.

Competitive Landscape

Leading Companies in Secondary Smelting and Alloying of Aluminum Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

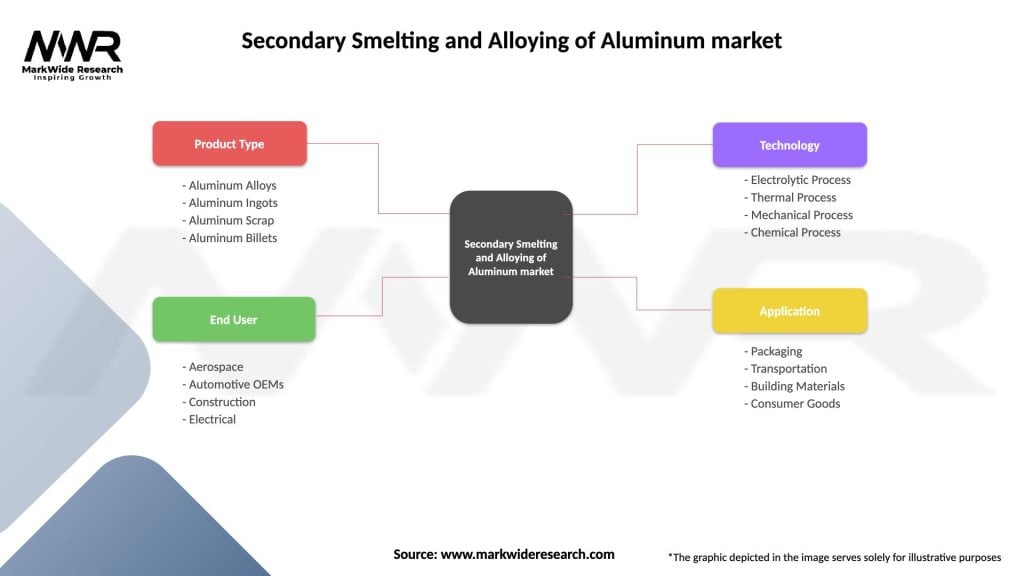

Segmentation The secondary smelting and alloying of aluminum market can be segmented based on the source of aluminum scrap (industrial scrap, post-consumer scrap), alloy type (wrought alloys, cast alloys), and end-use industries (automotive, construction, packaging).

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Market Key Trends

Covid-19 Impact The Covid-19 pandemic disrupted supply chains and affected aluminum demand across various industries. However, the focus on sustainability and the circular economy remained intact, driving the long-term growth of the secondary smelting and alloying of aluminum market.

Key Industry Developments

Analyst Suggestions

Future Outlook The secondary smelting and alloying of aluminum market is expected to witness steady growth in the coming years as industries focus on sustainable practices and resource conservation. Technological advancements, collaboration, and innovation in recycling processes will drive the market’s future growth. The circular economy initiatives and the increasing demand for recycled materials will create opportunities for market players to expand their operations and develop high-quality alloys.

Conclusion The secondary smelting and alloying of aluminum market plays a critical role in sustainable resource management and environmental conservation. The market offers cost-effective solutions for industries seeking recycled aluminum alloys while reducing the demand for primary aluminum. Despite challenges related to quality control and competition from primary aluminum, the market presents opportunities for technological advancements, collaboration, and growth in various end-use industries. With the increasing focus on sustainability and circular economy practices, the secondary smelting and alloying of aluminum market is expected to witness a positive outlook in the coming years.

What is Secondary Smelting and Alloying of Aluminum?

Secondary smelting and alloying of aluminum refers to the process of recycling aluminum scrap to produce new aluminum products. This process involves melting down scrap aluminum and adding alloying elements to achieve desired properties for various applications.

What are the key players in the Secondary Smelting and Alloying of Aluminum market?

Key players in the Secondary Smelting and Alloying of Aluminum market include companies like Novelis Inc., Hydro Aluminium, and Constellium, among others. These companies are involved in the production and recycling of aluminum, catering to various industries such as automotive and construction.

What are the growth factors driving the Secondary Smelting and Alloying of Aluminum market?

The growth of the Secondary Smelting and Alloying of Aluminum market is driven by increasing demand for recycled aluminum due to its environmental benefits and cost-effectiveness. Additionally, the automotive and aerospace industries are increasingly adopting aluminum for lightweight applications, further boosting market growth.

What challenges does the Secondary Smelting and Alloying of Aluminum market face?

The Secondary Smelting and Alloying of Aluminum market faces challenges such as fluctuating scrap aluminum prices and stringent environmental regulations. These factors can impact the profitability and operational efficiency of recycling facilities.

What opportunities exist in the Secondary Smelting and Alloying of Aluminum market?

Opportunities in the Secondary Smelting and Alloying of Aluminum market include advancements in recycling technologies and increasing investments in sustainable practices. The growing emphasis on circular economy principles also presents new avenues for growth in aluminum recycling.

What trends are shaping the Secondary Smelting and Alloying of Aluminum market?

Trends in the Secondary Smelting and Alloying of Aluminum market include the rising adoption of electric arc furnaces for more efficient melting processes and the development of new aluminum alloys with enhanced properties. Additionally, there is a growing focus on reducing carbon emissions in aluminum production.

Secondary Smelting and Alloying of Aluminum market

| Segmentation Details | Description |

|---|---|

| Product Type | Aluminum Alloys, Aluminum Ingots, Aluminum Scrap, Aluminum Billets |

| End User | Aerospace, Automotive OEMs, Construction, Electrical |

| Technology | Electrolytic Process, Thermal Process, Mechanical Process, Chemical Process |

| Application | Packaging, Transportation, Building Materials, Consumer Goods |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in Secondary Smelting and Alloying of Aluminum Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA