444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Saudi Arabia contract logistics market represents a rapidly expanding sector within the Kingdom’s comprehensive economic transformation agenda. Contract logistics services encompass comprehensive supply chain management solutions, including warehousing, distribution, transportation, and value-added services provided by third-party logistics providers. The market has experienced remarkable growth, driven by Vision 2030 initiatives, increasing e-commerce penetration, and the Kingdom’s strategic position as a regional logistics hub.

Market dynamics indicate substantial expansion opportunities as Saudi Arabia continues diversifying its economy away from oil dependency. The contract logistics sector benefits from significant government investments in infrastructure development, including the development of NEOM logistics zones, expansion of King Abdulaziz Port, and construction of advanced distribution centers. Growth projections suggest the market will maintain a robust 8.5% CAGR through the forecast period, supported by increasing demand from retail, healthcare, automotive, and manufacturing sectors.

Regional positioning plays a crucial role in market development, with Saudi Arabia serving as a gateway between Europe, Asia, and Africa. The Kingdom’s strategic location along major trade routes, combined with substantial infrastructure investments, positions it as a preferred destination for international logistics companies seeking regional expansion. Digital transformation initiatives and adoption of advanced technologies further enhance the market’s growth potential.

The Saudi Arabia contract logistics market refers to the comprehensive ecosystem of outsourced supply chain management services provided by specialized third-party logistics companies to businesses across various industries within the Kingdom. Contract logistics encompasses integrated solutions including warehousing operations, inventory management, order fulfillment, transportation services, and value-added activities such as packaging, labeling, and reverse logistics.

Service providers in this market operate under long-term contractual agreements with clients, managing entire supply chain segments or specific logistics functions. These arrangements typically involve multi-year partnerships where logistics companies assume responsibility for optimizing supply chain efficiency, reducing operational costs, and improving service quality. The market includes both international logistics giants and domestic providers offering specialized regional expertise.

Value proposition centers on enabling businesses to focus on core competencies while leveraging specialized logistics expertise and infrastructure. Contract logistics providers offer scalable solutions that adapt to seasonal demand fluctuations, market expansion requirements, and evolving customer expectations. Technology integration forms a critical component, with providers implementing warehouse management systems, transportation management platforms, and real-time tracking capabilities.

Market leadership in Saudi Arabia’s contract logistics sector reflects the Kingdom’s ambitious economic diversification strategy and commitment to becoming a regional logistics powerhouse. The market demonstrates exceptional growth momentum, supported by government initiatives, infrastructure development, and increasing adoption of outsourced logistics solutions across multiple industry verticals.

Key growth drivers include the rapid expansion of e-commerce platforms, which has increased demand for sophisticated fulfillment capabilities by approximately 45% annually. The healthcare sector’s modernization efforts, retail market evolution, and manufacturing sector development contribute significantly to contract logistics demand. Vision 2030 objectives emphasize logistics sector development as a cornerstone of economic transformation.

Competitive landscape features a mix of international logistics leaders and emerging domestic providers, creating a dynamic market environment. Technology adoption rates have accelerated, with 65% of providers implementing advanced warehouse automation systems and digital tracking capabilities. Investment flows into logistics infrastructure and technology platforms continue strengthening market foundations.

Future prospects remain highly favorable, with market expansion expected across traditional and emerging sectors. The integration of artificial intelligence, robotics, and IoT technologies will drive operational efficiency improvements and service quality enhancements. Sustainability initiatives and green logistics practices are becoming increasingly important differentiators in the competitive landscape.

Strategic insights reveal several critical factors shaping the Saudi Arabia contract logistics market trajectory:

Market maturation indicators suggest the sector is transitioning from basic transportation and warehousing services toward comprehensive supply chain solutions. Value-added services including packaging, assembly, and reverse logistics are becoming standard offerings. The integration of predictive analytics and machine learning capabilities enables proactive supply chain optimization.

Economic diversification serves as the primary catalyst driving Saudi Arabia’s contract logistics market expansion. The Kingdom’s Vision 2030 strategy emphasizes reducing oil dependency through developing non-oil sectors, creating substantial demand for sophisticated logistics support across emerging industries. This transformation requires advanced supply chain capabilities that many businesses prefer to outsource to specialized providers.

E-commerce proliferation represents another significant growth driver, with online retail adoption accelerating dramatically following the pandemic. Digital commerce requires sophisticated fulfillment capabilities, including same-day delivery options, reverse logistics for returns, and multi-channel distribution strategies. Contract logistics providers offer the infrastructure and expertise necessary to support these complex requirements.

Infrastructure investments create enabling conditions for market expansion. The development of King Salman International Airport, expansion of Jeddah Islamic Port, and construction of specialized logistics zones provide world-class facilities that attract international businesses and logistics providers. These investments reduce operational costs and improve service quality across the supply chain.

Regulatory reforms facilitate foreign investment and business establishment, encouraging international logistics companies to establish regional operations in Saudi Arabia. Ease of doing business improvements, streamlined customs procedures, and investment incentives create favorable conditions for market entry and expansion.

Skilled workforce availability presents ongoing challenges for contract logistics market development. The sector requires specialized expertise in supply chain management, technology systems, and customer service. Talent shortages in areas such as warehouse automation, data analytics, and logistics planning can constrain growth and operational efficiency improvements.

Initial investment requirements for establishing comprehensive logistics operations can be substantial, particularly for advanced automation systems and technology platforms. Capital intensity may limit market entry for smaller providers and require significant financial resources for expansion and modernization initiatives.

Cultural adaptation challenges affect international providers entering the Saudi market. Understanding local business practices, regulatory requirements, and customer expectations requires time and investment. Localization efforts including language capabilities, cultural sensitivity, and relationship building are essential for success.

Technology integration complexities can create implementation challenges, particularly when connecting with existing client systems or legacy infrastructure. System compatibility issues, data security concerns, and integration timelines may impact service delivery and customer satisfaction during transition periods.

Healthcare logistics presents exceptional growth opportunities as Saudi Arabia modernizes its healthcare system and expands pharmaceutical distribution capabilities. The sector requires specialized handling, temperature-controlled storage, and regulatory compliance expertise. Medical device distribution and pharmaceutical supply chains offer high-value service opportunities for specialized providers.

Cross-border trade facilitation represents a significant opportunity as Saudi Arabia strengthens its position as a regional logistics hub. Trade route optimization between Asia, Europe, and Africa creates demand for comprehensive logistics services including customs clearance, warehousing, and distribution across multiple countries.

Sustainability services are becoming increasingly important as businesses focus on environmental responsibility and carbon footprint reduction. Green logistics solutions including electric vehicle fleets, renewable energy-powered facilities, and circular economy practices create differentiation opportunities for forward-thinking providers.

Technology-enabled services offer substantial growth potential through artificial intelligence, robotics, and IoT integration. Predictive analytics for demand forecasting, automated inventory management, and real-time supply chain visibility create value-added service opportunities that command premium pricing.

Competitive intensity in the Saudi Arabia contract logistics market continues escalating as both international and domestic providers vie for market share. Service differentiation increasingly focuses on technology capabilities, industry specialization, and value-added services rather than basic transportation and warehousing functions. This evolution drives continuous innovation and investment in advanced capabilities.

Customer expectations are rising rapidly, influenced by global e-commerce standards and digital transformation initiatives. Businesses demand real-time visibility, flexible service options, and seamless integration with their operations. Contract logistics providers must invest in technology platforms and service capabilities to meet these evolving requirements.

Consolidation trends are emerging as larger providers acquire specialized companies to expand service capabilities and geographic coverage. Strategic partnerships between international logistics giants and local providers create comprehensive service networks that leverage global expertise with regional market knowledge.

Regulatory evolution continues shaping market dynamics as the government implements new policies supporting logistics sector development. Trade facilitation measures, customs modernization, and investment incentives create favorable operating conditions while establishing quality and compliance standards.

Comprehensive analysis of the Saudi Arabia contract logistics market employs multiple research methodologies to ensure accuracy and depth of insights. Primary research includes extensive interviews with industry executives, logistics providers, and key stakeholders across various sectors utilizing contract logistics services. This approach provides firsthand insights into market trends, challenges, and opportunities.

Secondary research encompasses analysis of government publications, industry reports, company financial statements, and regulatory documents. Data triangulation from multiple sources ensures reliability and validates key findings. Market sizing and growth projections utilize econometric modeling based on historical trends and forward-looking indicators.

Industry expert consultations provide specialized insights into technology trends, regulatory developments, and competitive dynamics. Stakeholder feedback from customers, suppliers, and industry associations offers comprehensive market perspective. According to MarkWide Research analysis, this multi-faceted approach ensures robust and actionable market intelligence.

Quantitative analysis includes statistical modeling of market drivers, correlation analysis of economic indicators, and trend analysis of sector-specific demand patterns. Qualitative assessment covers competitive positioning, strategic initiatives, and market development strategies employed by leading providers.

Riyadh region dominates the Saudi Arabia contract logistics market, accounting for approximately 40% market share due to its role as the political and economic capital. The region benefits from extensive government and corporate headquarters, driving demand for sophisticated supply chain solutions. Industrial development in Riyadh creates additional opportunities for manufacturing logistics and distribution services.

Eastern Province represents the second-largest market segment, leveraging its industrial base and proximity to major ports. Petrochemical industries, manufacturing facilities, and international trade activities generate substantial contract logistics demand. The region’s infrastructure advantages include advanced port facilities and transportation networks supporting efficient logistics operations.

Western Region including Jeddah and Mecca benefits from religious tourism, international trade through Jeddah Islamic Port, and growing commercial activities. Seasonal demand fluctuations during Hajj and Umrah periods require flexible logistics solutions that contract providers are well-positioned to deliver.

Emerging regions including NEOM and other planned cities represent future growth opportunities as these developments progress. Strategic positioning of these new urban centers emphasizes logistics and trade facilitation, creating demand for advanced contract logistics services from the initial development phases.

Market leadership in Saudi Arabia’s contract logistics sector features a diverse mix of international logistics giants and specialized regional providers. The competitive environment emphasizes service excellence, technology innovation, and industry expertise as key differentiators.

Competitive strategies increasingly focus on technology differentiation, industry specialization, and strategic partnerships. Investment priorities include automation systems, digital platforms, and sustainability initiatives that enhance operational efficiency and service quality.

By Service Type:

By Industry Vertical:

By Technology Integration:

Warehousing and distribution represents the largest segment within Saudi Arabia’s contract logistics market, driven by increasing demand for sophisticated inventory management and order fulfillment capabilities. Modern facilities incorporate advanced warehouse management systems, automated sorting equipment, and real-time inventory tracking. The segment benefits from e-commerce growth and retail sector expansion requiring flexible storage solutions.

Transportation management services are experiencing rapid growth as businesses seek to optimize delivery networks and reduce logistics costs. Last-mile delivery capabilities have become particularly important with e-commerce expansion, requiring sophisticated routing optimization and customer communication systems. Cross-border transportation services benefit from Saudi Arabia’s strategic location and trade facilitation initiatives.

Value-added services represent the highest-margin segment, offering specialized capabilities including product customization, packaging, and reverse logistics. Service differentiation in this category enables providers to command premium pricing while building stronger customer relationships. Healthcare and automotive sectors drive demand for specialized value-added services requiring industry expertise and compliance capabilities.

Technology integration across all service categories is accelerating, with 75% of providers investing in digital transformation initiatives. Advanced analytics, artificial intelligence, and automation technologies enhance operational efficiency while improving service quality and customer satisfaction.

Cost optimization represents the primary benefit for businesses utilizing contract logistics services, with companies typically achieving 15-25% reduction in total logistics costs through outsourcing arrangements. Economies of scale achieved by specialized providers, combined with operational expertise and technology investments, deliver significant cost advantages compared to in-house logistics operations.

Scalability and flexibility enable businesses to adapt quickly to market changes, seasonal demand fluctuations, and growth opportunities. Contract logistics providers offer variable cost structures and scalable capacity that align with business requirements without requiring substantial capital investments in infrastructure and equipment.

Technology access provides businesses with advanced logistics capabilities without direct investment in expensive systems and platforms. Shared technology costs across multiple clients make sophisticated warehouse management systems, transportation optimization tools, and real-time tracking capabilities accessible to businesses of all sizes.

Risk mitigation benefits include regulatory compliance, insurance coverage, and operational risk management provided by experienced logistics professionals. Specialized expertise in areas such as hazardous materials handling, international trade regulations, and industry-specific requirements reduces compliance risks and operational challenges.

Focus enhancement allows businesses to concentrate resources on core competencies while leveraging specialized logistics expertise. Strategic advantage emerges from improved supply chain performance, enhanced customer service, and faster market responsiveness enabled by professional logistics support.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation represents the most significant trend reshaping Saudi Arabia’s contract logistics market. Technology adoption includes artificial intelligence for demand forecasting, robotics for warehouse automation, and IoT sensors for real-time supply chain visibility. These innovations enhance operational efficiency while improving service quality and customer satisfaction.

Sustainability initiatives are gaining momentum as businesses and consumers increasingly prioritize environmental responsibility. Green logistics practices include electric vehicle fleets, renewable energy-powered facilities, and circular economy principles. Providers implementing comprehensive sustainability programs gain competitive advantages and attract environmentally conscious clients.

Omnichannel fulfillment capabilities are becoming essential as retailers adopt integrated online and offline strategies. Unified inventory management across multiple channels requires sophisticated technology platforms and flexible distribution networks. Contract logistics providers offer the expertise and infrastructure necessary to support complex omnichannel requirements.

Specialized sector focus is emerging as providers develop deep expertise in specific industries such as healthcare, automotive, and e-commerce. Industry specialization enables providers to offer tailored solutions, regulatory compliance expertise, and value-added services that generic providers cannot match.

Regional integration trends reflect Saudi Arabia’s ambition to become a Middle East logistics hub. Cross-border services and regional distribution networks create opportunities for providers to offer comprehensive solutions spanning multiple countries and markets.

Infrastructure investments continue transforming Saudi Arabia’s logistics landscape with major projects enhancing capacity and capabilities. The King Salman International Airport development will create one of the world’s largest logistics hubs, while port expansions increase maritime cargo handling capacity. These investments attract international logistics providers and enable service quality improvements.

Technology partnerships between logistics providers and technology companies are accelerating innovation adoption. Strategic alliances focus on developing AI-powered optimization systems, blockchain-based tracking platforms, and automated warehouse solutions. These collaborations enhance competitive positioning while reducing individual investment requirements.

Regulatory reforms streamline business establishment procedures and improve trade facilitation processes. Customs modernization initiatives reduce clearance times and administrative burdens, while investment incentives encourage foreign logistics companies to establish regional operations in Saudi Arabia.

Merger and acquisition activities are reshaping the competitive landscape as companies seek to expand capabilities and market coverage. Strategic acquisitions enable rapid market entry, technology access, and specialized expertise acquisition. According to MWR analysis, consolidation trends are expected to continue as the market matures.

Sustainability commitments by major providers include carbon neutrality targets, renewable energy adoption, and circular economy initiatives. Environmental programs respond to increasing stakeholder expectations while creating operational efficiencies and cost savings.

Technology investment should be prioritized by contract logistics providers seeking competitive advantage in the Saudi market. Digital platforms including warehouse management systems, transportation optimization tools, and customer portals are essential for meeting evolving client expectations. Providers should focus on scalable solutions that can adapt to future technological developments.

Talent development initiatives are crucial for addressing skill shortages and building local expertise. Training programs should focus on supply chain management, technology systems, and customer service capabilities. Partnerships with educational institutions and government training programs can help develop the skilled workforce necessary for market expansion.

Industry specialization offers opportunities for differentiation and premium pricing. Sector expertise in areas such as healthcare, automotive, or e-commerce enables providers to offer tailored solutions and value-added services. Deep industry knowledge creates barriers to entry and strengthens customer relationships.

Strategic partnerships with local companies can facilitate market entry and expansion for international providers. Joint ventures or acquisition strategies provide access to local market knowledge, regulatory expertise, and established customer relationships. These partnerships can accelerate growth while reducing market entry risks.

Sustainability programs should be integrated into core business strategies rather than treated as optional initiatives. Environmental responsibility increasingly influences customer selection criteria and regulatory requirements. Providers implementing comprehensive sustainability programs gain competitive advantages and future-proof their operations.

Growth trajectory for Saudi Arabia’s contract logistics market remains highly positive, supported by continued economic diversification, infrastructure development, and technology adoption. Market expansion is expected to accelerate as Vision 2030 initiatives progress and new economic sectors develop. The integration of advanced technologies will drive operational efficiency improvements and service innovation.

Sector diversification will create new opportunities as healthcare modernization, renewable energy development, and tourism expansion generate specialized logistics requirements. Emerging industries including biotechnology, advanced manufacturing, and digital services will require sophisticated supply chain support that contract logistics providers are well-positioned to deliver.

Technology evolution will continue reshaping service delivery models, with artificial intelligence, robotics, and IoT integration becoming standard capabilities. Predictive analytics will enable proactive supply chain management, while automation will improve efficiency and reduce operational costs. Providers investing in technology leadership will capture disproportionate market share.

Regional integration opportunities will expand as Saudi Arabia strengthens its position as a Middle East logistics hub. Cross-border services and regional distribution networks will create substantial growth opportunities for providers with comprehensive geographic coverage and international expertise.

Sustainability requirements will become increasingly important as environmental regulations strengthen and customer expectations evolve. Green logistics capabilities will transition from competitive advantages to market requirements, driving continued investment in sustainable technologies and practices.

The Saudi Arabia contract logistics market presents exceptional growth opportunities driven by economic diversification, infrastructure development, and technology adoption. Market fundamentals remain strong, supported by government initiatives, increasing e-commerce penetration, and the Kingdom’s strategic positioning as a regional logistics hub. The sector’s transformation from basic transportation and warehousing services toward comprehensive supply chain solutions reflects market maturation and evolving customer requirements.

Competitive dynamics favor providers that invest in technology capabilities, develop industry expertise, and build strategic partnerships. The integration of artificial intelligence, robotics, and sustainability practices will define market leadership in the coming years. Success factors include operational excellence, customer service quality, and the ability to adapt to rapidly changing market conditions.

Future prospects indicate continued market expansion across traditional and emerging sectors, with particular opportunities in healthcare, e-commerce, and cross-border trade facilitation. The Saudi Arabia contract logistics market is well-positioned to support the Kingdom’s economic transformation while creating substantial value for businesses, investors, and stakeholders throughout the supply chain ecosystem.

What is Contract Logistics?

Contract logistics refers to the outsourcing of logistics services to a third-party provider, which manages the entire supply chain process. This includes transportation, warehousing, and distribution, tailored to meet the specific needs of businesses in various sectors.

What are the key players in the Saudi Arabia Contract Logistics Market?

Key players in the Saudi Arabia Contract Logistics Market include DHL Supply Chain, Agility Logistics, and Kuehne + Nagel, among others. These companies provide a range of services, including freight forwarding, warehousing, and supply chain management.

What are the growth factors driving the Saudi Arabia Contract Logistics Market?

The growth of the Saudi Arabia Contract Logistics Market is driven by factors such as the increasing demand for efficient supply chain solutions, the rise of e-commerce, and government initiatives to enhance logistics infrastructure. Additionally, the focus on cost reduction and operational efficiency is propelling market expansion.

What challenges does the Saudi Arabia Contract Logistics Market face?

Challenges in the Saudi Arabia Contract Logistics Market include regulatory hurdles, fluctuating fuel prices, and the need for skilled labor. These factors can impact operational efficiency and service delivery in the logistics sector.

What opportunities exist in the Saudi Arabia Contract Logistics Market?

Opportunities in the Saudi Arabia Contract Logistics Market include the adoption of advanced technologies such as automation and IoT, which can enhance supply chain visibility and efficiency. Additionally, the growing trend of sustainability in logistics presents avenues for companies to innovate and reduce their environmental impact.

What trends are shaping the Saudi Arabia Contract Logistics Market?

Trends shaping the Saudi Arabia Contract Logistics Market include the increasing integration of technology in logistics operations, the rise of omnichannel distribution strategies, and a focus on sustainability practices. These trends are influencing how logistics providers operate and meet customer demands.

Saudi Arabia Contract Logistics Market

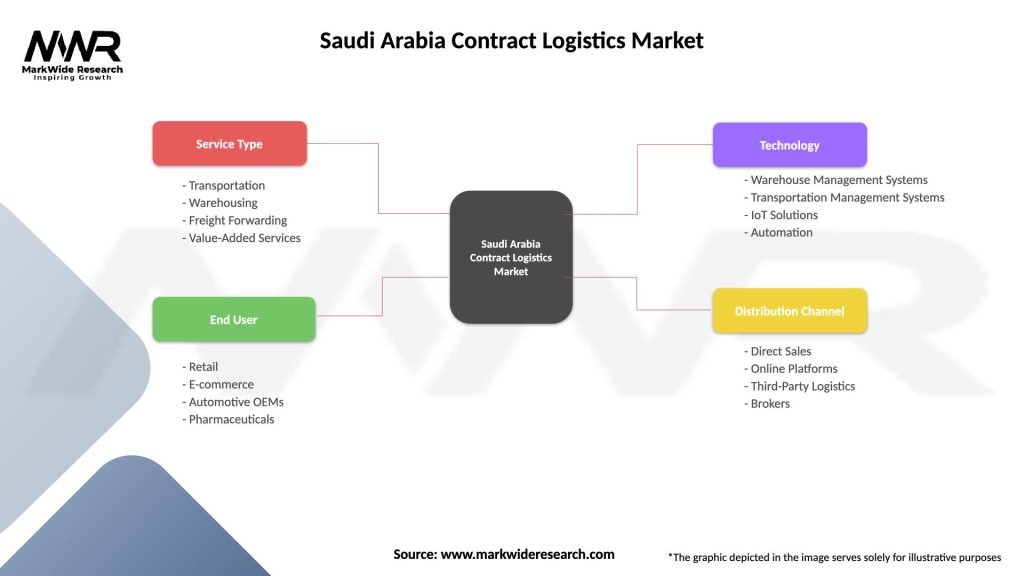

| Segmentation Details | Description |

|---|---|

| Service Type | Transportation, Warehousing, Freight Forwarding, Value-Added Services |

| End User | Retail, E-commerce, Automotive OEMs, Pharmaceuticals |

| Technology | Warehouse Management Systems, Transportation Management Systems, IoT Solutions, Automation |

| Distribution Channel | Direct Sales, Online Platforms, Third-Party Logistics, Brokers |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Saudi Arabia Contract Logistics Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.