Market Overview Satellite broadband refers to high-speed internet access provided through satellite communication networks. Satellite broadband services offer broadband connectivity to remote and underserved areas where traditional terrestrial broadband infrastructure is unavailable or inadequate. With advancements in satellite technology and the growing demand for internet connectivity worldwide, the satellite broadband market is experiencing significant growth and innovation.

Meaning Satellite broadband is a telecommunications technology that delivers high-speed internet access to users via satellite communication systems. Unlike traditional terrestrial broadband services, which rely on physical cables and infrastructure, satellite broadband beams internet signals from satellites orbiting the Earth directly to satellite dishes installed at users’ premises. Satellite broadband enables reliable internet access in rural, remote, and maritime areas, bridging the digital divide and expanding broadband connectivity globally.

Executive Summary The satellite broadband market is witnessing rapid growth, driven by factors such as increasing demand for broadband connectivity, technological advancements in satellite systems, and government initiatives to bridge the digital divide. Key market players are investing in satellite constellation deployments, ground infrastructure upgrades, and service innovations to deliver high-speed internet access to underserved regions and emerging markets. However, the market faces challenges such as spectrum constraints, latency issues, and competition from terrestrial broadband technologies. To capitalize on growth opportunities, industry participants need to focus on improving service quality, expanding coverage, and addressing regulatory and technical challenges.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Global Connectivity Demand: The increasing demand for broadband connectivity, driven by trends such as remote work, e-learning, and digitalization, is fueling the growth of the satellite broadband market, particularly in rural and underserved areas.

Advancements in Satellite Technology: Technological advancements, such as high-throughput satellites (HTS), low Earth orbit (LEO) satellite constellations, and phased array antennas, are enabling satellite broadband providers to deliver faster speeds, lower latency, and expanded coverage.

Government Initiatives: Governments and regulatory authorities are implementing initiatives to promote satellite broadband deployment, improve digital infrastructure, and bridge the digital divide, particularly in rural and remote regions lacking access to terrestrial broadband services.

Market Drivers

Digital Inclusion: Satellite broadband plays a crucial role in bridging the digital divide by providing broadband connectivity to underserved and remote areas where traditional terrestrial infrastructure is unavailable or economically unfeasible to deploy.

Global Coverage: Satellite broadband offers global coverage, enabling connectivity in remote, rural, and maritime regions, as well as in areas affected by natural disasters or geopolitical conflicts where terrestrial infrastructure may be disrupted.

Scalability and Flexibility: Satellite broadband solutions are scalable and flexible, allowing service providers to rapidly deploy and expand coverage to new regions, respond to changing demand, and address temporary connectivity needs in disaster recovery scenarios.

Broadband Competition: In regions where terrestrial broadband services are limited or non-existent, satellite broadband providers offer competition and choice, driving innovation, improving service quality, and lowering prices for consumers.

Market Restraints

Latency and Bandwidth Constraints: Satellite broadband systems face inherent limitations, including latency issues due to the distance between satellites and Earth, as well as bandwidth constraints that can impact the quality of service, particularly for real-time applications such as online gaming and video conferencing.

Spectrum Allocation Challenges: The allocation of spectrum for satellite broadband services is subject to regulatory constraints and competition from other wireless technologies, posing challenges for satellite operators to secure sufficient spectrum resources for future growth and innovation.

Infrastructure Costs: The deployment and operation of satellite broadband systems require significant upfront investments in satellite manufacturing, launch services, ground infrastructure, and ongoing maintenance, limiting market entry and scalability for smaller satellite operators.

Competition from Terrestrial Technologies: Satellite broadband faces competition from terrestrial broadband technologies, such as fiber-optic networks, cable internet, and 5G wireless, which offer higher speeds, lower latency, and lower costs in densely populated urban areas.

Market Opportunities

LEO Satellite Constellations: The deployment of LEO satellite constellations, featuring hundreds or thousands of small satellites in low Earth orbit, presents opportunities for satellite broadband providers to offer faster speeds, lower latency, and expanded coverage compared to traditional geostationary satellites.

Urban and Mobility Markets: Satellite broadband providers can target urban markets, including apartment buildings, commercial complexes, and transportation hubs, as well as mobile and maritime applications such as aircraft, ships, and vehicles, to expand their customer base and revenue streams.

Emerging Markets and Verticals: Emerging markets in Asia, Africa, and Latin America, as well as vertical sectors such as agriculture, energy, and government, represent growth opportunities for satellite broadband providers to address unmet connectivity needs and deliver value-added services.

Market Dynamics The satellite broadband market is characterized by dynamic trends and factors that influence its growth and evolution. From technological innovations to regulatory reforms, these dynamics shape the market landscape and present both challenges and opportunities for industry participants. Understanding the market dynamics is essential for stakeholders to navigate the competitive landscape, capitalize on emerging trends, and sustain growth in the long term.

Regional Analysis The satellite broadband market exhibits regional variations in terms of market size, growth potential, regulatory environment, and competitive landscape. Key regions driving market growth include:

North America: North America is a leading market for satellite broadband, driven by factors such as rural connectivity initiatives, government funding programs, and partnerships between satellite operators and broadband providers to expand coverage in underserved areas.

Europe: Europe is a prominent market for satellite broadband, characterized by regulatory support for satellite communications, investments in satellite infrastructure, and partnerships between satellite operators and telecommunication companies to deliver broadband services to rural communities.

Asia Pacific: Asia Pacific is witnessing significant growth in satellite broadband adoption, fueled by increasing demand for broadband connectivity, government initiatives to bridge the digital divide, and investments in satellite technology and infrastructure across countries such as India, China, and Australia.

Latin America: Latin America represents an emerging market for satellite broadband, driven by factors such as remote geography, limited terrestrial infrastructure, and government efforts to improve connectivity in rural and remote regions.

Competitive Landscape

Leading Companies in the Satellite Broadband Market:

Viasat, Inc.

Hughes Network Systems, LLC

SpaceX

OneWeb

Telesat

Eutelsat Communications

SES S.A.

Inmarsat plc

O3b Networks (a subsidiary of SES S.A.)

Intelsat S.A.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

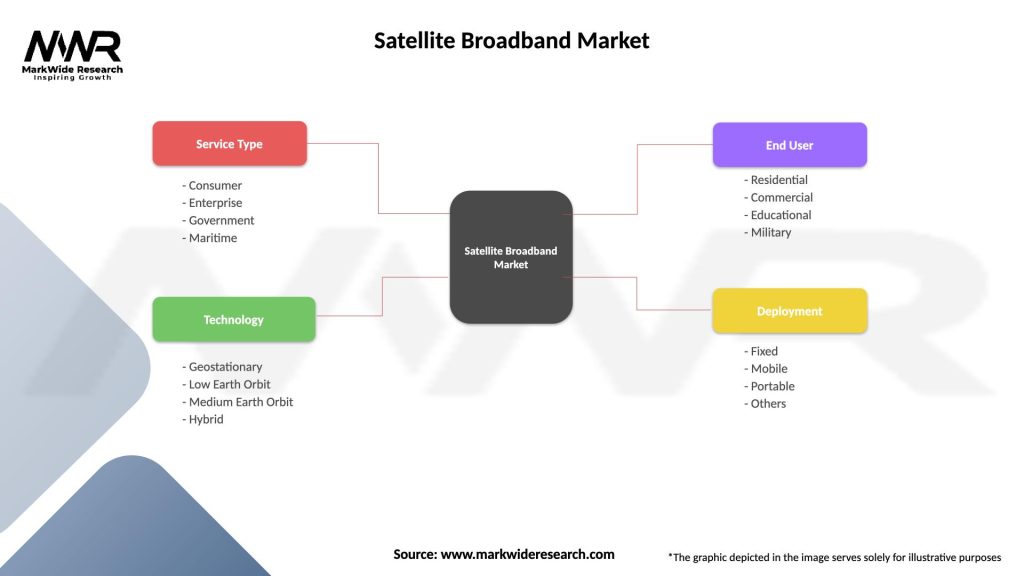

Segmentation The satellite broadband market can be segmented based on various factors, including:

Satellite Orbit: Geostationary orbit (GEO) satellites, medium Earth orbit (MEO) satellites, and low Earth orbit (LEO) satellites.

Service Type: Consumer broadband, enterprise broadband, government and military, maritime and aviation, and Internet of Things (IoT) applications.

End User: Residential users, commercial users, government agencies, maritime operators, and aviation companies.

Region: North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Segmentation provides insights into market dynamics, customer preferences, and growth opportunities, enabling satellite broadband providers to tailor their products and strategies to specific market segments and geographic regions.

Category-wise Insights

Consumer Broadband: Satellite broadband services for residential users, offering high-speed internet access, data allowances, and value-added features such as Wi-Fi hotspot access, bundled services, and equipment leasing options.

Enterprise Broadband: Satellite broadband solutions for businesses and organizations, providing reliable connectivity, dedicated bandwidth, and managed services for applications such as cloud computing, video conferencing, and remote office connectivity.

Government and Military: Satellite broadband services for government agencies, military forces, and emergency responders, offering secure, resilient, and interoperable communications for command and control, intelligence, surveillance, and reconnaissance (C4ISR) applications.

Maritime and Aviation: Satellite broadband solutions for maritime and aviation markets, including ships, aircraft, and offshore platforms, providing connectivity for crew welfare, passenger entertainment, operational efficiency, and safety communications.

Key Benefits for Industry Participants and Stakeholders

Universal Connectivity: Satellite broadband enables universal broadband connectivity, reaching remote, rural, and underserved areas where terrestrial infrastructure is unavailable or economically unfeasible to deploy.

Reliable Connectivity: Satellite broadband offers reliable internet access, providing backup and redundancy for terrestrial networks, as well as connectivity in disaster recovery scenarios and during network outages.

Scalable Solutions: Satellite broadband solutions are scalable and flexible, allowing service providers to rapidly deploy and expand coverage to new regions, respond to changing demand, and address temporary connectivity needs in disaster recovery scenarios.

Global Coverage: Satellite broadband offers global coverage, enabling connectivity in remote, rural, and maritime regions, as well as in areas affected by natural disasters or geopolitical conflicts where terrestrial infrastructure may be disrupted.

SWOT Analysis A SWOT analysis of the satellite broadband market provides insights into its strengths, weaknesses, opportunities, and threats:

Strengths:

Universal broadband connectivity.

Global coverage and resilience.

Scalable and flexible solutions.

Bridging the digital divide and enabling digital inclusion.

Weaknesses:

Latency and bandwidth limitations.

Spectrum constraints and regulatory challenges.

Infrastructure costs and investment requirements.

Competition from terrestrial broadband technologies.

Opportunities:

LEO satellite constellations and advanced satellite technologies.

Urban and mobility markets for satellite broadband services.

Government initiatives to bridge the digital divide and improve connectivity.

Threats:

Competition from terrestrial broadband technologies.

Regulatory constraints and spectrum allocation challenges.

Technology disruptions and market volatility.

Cybersecurity risks and vulnerabilities.

Understanding these factors through a SWOT analysis helps stakeholders identify strategic priorities, mitigate risks, and capitalize on growth opportunities in the satellite broadband market.

Market Key Trends

LEO Satellite Constellations: The deployment of LEO satellite constellations is a key trend in the satellite broadband market, enabling faster speeds, lower latency, and expanded coverage compared to traditional GEO satellites.

Advanced Satellite Technologies: Technological advancements such as high-throughput satellites (HTS), phased array antennas, and software-defined payloads are driving innovation in satellite broadband systems, enhancing performance, flexibility, and scalability.

Vertical Integration and Partnerships: Vertical integration among satellite operators, telecommunications companies, and technology providers, as well as partnerships with governments, industry stakeholders, and vertical sectors, are shaping the future of satellite broadband services.

Regulatory Reforms and Spectrum Allocation: Regulatory reforms and spectrum allocation initiatives by governments and regulatory authorities are driving market growth, facilitating satellite broadband deployment, and enabling innovation in satellite communications.

Covid-19 Impact The COVID-19 pandemic has had a significant impact on the satellite broadband market, affecting demand, supply chains, and industry dynamics. Key impacts of COVID-19 on the market include:

Increased Demand for Connectivity: The pandemic has led to increased demand for broadband connectivity, driven by trends such as remote work, e-learning, telemedicine, and digitalization, boosting demand for satellite broadband services in rural and underserved areas.

Supply Chain Disruptions: Disruptions in global supply chains, manufacturing operations, and launch schedules have impacted the availability of satellite components, ground infrastructure, and satellite launches, delaying deployment timelines and expansion plans for satellite operators.

Operational Challenges: Satellite operators and service providers have faced operational challenges, including increased network traffic, bandwidth demands, and customer support requirements, as well as logistical challenges related to site installations, equipment provisioning, and service activations.

Digital Divide Awareness: The pandemic has highlighted the digital divide and disparities in broadband access, prompting governments, regulators, and industry stakeholders to prioritize initiatives to bridge the digital divide, improve digital infrastructure, and expand broadband connectivity to underserved populations.

Key Industry Developments

LEO Satellite Constellations Deployment: Satellite operators are deploying LEO satellite constellations to deliver high-speed, low-latency broadband services to global markets, with companies such as SpaceX (Starlink), OneWeb, and Amazon (Project Kuiper) leading the way.

Advanced Ground Infrastructure: Investments in ground infrastructure upgrades, including gateway Earth stations, ground segment automation, and network management systems, are enhancing the performance, efficiency, and scalability of satellite broadband networks.

Satellite Technology Innovation: Technological innovations such as electronically steerable antennas, on-board processing, and optical inter-satellite links are driving innovation in satellite broadband systems, enabling higher throughput, lower latency, and improved service quality.

Regulatory Reforms and Spectrum Allocation: Governments and regulatory authorities are implementing reforms and spectrum allocation initiatives to support satellite broadband deployment, reduce regulatory barriers, and facilitate market entry for new satellite operators.

Analyst Suggestions

Invest in LEO Constellations: Satellite operators should invest in LEO satellite constellations to capitalize on opportunities for faster speeds, lower latency, and expanded coverage, while addressing challenges such as satellite manufacturing, launch services, and network scalability.

Focus on Service Quality: Satellite broadband providers should focus on improving service quality, reliability, and customer support to enhance user experience, reduce churn, and differentiate themselves in the competitive market landscape.

Address Regulatory Challenges: Satellite operators should engage with governments, regulators, and industry stakeholders to address regulatory challenges, spectrum constraints, and market entry barriers, while advocating for policies that support satellite broadband deployment and innovation.

Expand Market Reach: Satellite broadband providers should expand their market reach into urban, mobility, and emerging markets, as well as vertical sectors such as government, enterprise, and maritime, to diversify revenue streams and maximize market opportunities.

Future Outlook The satellite broadband market is poised for continued growth and innovation, driven by advancements in satellite technology, increasing demand for broadband connectivity, and government initiatives to bridge the digital divide. Despite challenges such as latency issues, spectrum constraints, and competition from terrestrial broadband technologies, the long-term outlook for the satellite broadband market remains positive, with opportunities for stakeholders to innovate, collaborate, and address emerging market needs.

Conclusion Satellite broadband plays a vital role in expanding broadband connectivity globally, reaching remote, rural, and underserved areas where traditional terrestrial infrastructure is unavailable or economically unfeasible to deploy. The market for satellite broadband is characterized by technological innovation, regulatory reforms, and industry collaboration, with key trends such as LEO satellite constellations, advanced satellite technologies, and vertical integration shaping its evolution. Despite challenges posed by the COVID-19 pandemic and market uncertainties, the satellite broadband market presents opportunities for stakeholders to drive innovation, enhance connectivity, and contribute to digital inclusion and economic development.

This comprehensive analysis provides insights into the aircraft control software and satellite broadband markets, covering market dynamics, trends, drivers, restraints, opportunities, competitive landscape, regional analysis, and future outlook. Understanding these insights is essential for industry stakeholders to navigate the competitive landscape, capitalize on growth opportunities, and shape the future of aviation and telecommunications.

What is Satellite Broadband?

Satellite broadband refers to high-speed internet access provided through satellite technology, enabling connectivity in remote and rural areas where traditional broadband services may be unavailable. It utilizes satellites in geostationary or low Earth orbit to transmit data to and from users.

What are the key players in the Satellite Broadband Market?

Key players in the Satellite Broadband Market include companies like SpaceX, Hughes Network Systems, and Viasat, which are known for their innovative satellite technologies and services. These companies are competing to expand their coverage and improve service quality, among others.

What are the main drivers of growth in the Satellite Broadband Market?

The main drivers of growth in the Satellite Broadband Market include the increasing demand for high-speed internet in underserved areas, advancements in satellite technology, and the rising adoption of IoT applications that require reliable connectivity. Additionally, the expansion of telecommunication infrastructure is contributing to market growth.

What challenges does the Satellite Broadband Market face?

The Satellite Broadband Market faces challenges such as high latency compared to terrestrial broadband, weather-related disruptions, and the significant costs associated with satellite deployment and maintenance. These factors can hinder service reliability and user satisfaction.

What opportunities exist in the Satellite Broadband Market?

Opportunities in the Satellite Broadband Market include the potential for partnerships with telecommunications companies to enhance service offerings and the growing demand for connectivity in sectors like agriculture, healthcare, and education. The rise of low Earth orbit satellites also presents new avenues for service expansion.

What trends are shaping the Satellite Broadband Market?

Trends shaping the Satellite Broadband Market include the deployment of low Earth orbit satellite constellations, which aim to provide lower latency and higher speeds, and the increasing integration of satellite services with mobile networks. Additionally, there is a growing focus on sustainability and reducing the environmental impact of satellite launches.

Leading Companies in the Satellite Broadband Market:

Viasat, Inc.

Hughes Network Systems, LLC

SpaceX

OneWeb

Telesat

Eutelsat Communications

SES S.A.

Inmarsat plc

O3b Networks (a subsidiary of SES S.A.)

Intelsat S.A.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.