444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Russia data center construction market represents a rapidly expanding sector within the nation’s digital infrastructure landscape. As Russia continues its digital transformation journey, the demand for robust data center facilities has intensified significantly, driven by increasing cloud adoption, digital services proliferation, and government digitization initiatives. The market encompasses the construction of hyperscale facilities, enterprise data centers, and colocation facilities across major metropolitan areas including Moscow, St. Petersburg, and emerging regional hubs.

Market dynamics indicate substantial growth potential, with the sector experiencing a compound annual growth rate (CAGR) of 12.3% as organizations increasingly recognize the critical importance of reliable digital infrastructure. The construction activities span various facility types, from small-scale edge computing centers to large hyperscale facilities designed to support cloud service providers and major enterprises. Regional distribution shows Moscow accounting for approximately 45% of construction activity, while St. Petersburg and other major cities contribute significantly to the overall market expansion.

Investment patterns reveal increasing interest from both domestic and international players, with construction projects incorporating advanced cooling technologies, renewable energy integration, and enhanced security features. The market benefits from Russia’s strategic focus on data sovereignty and digital independence, creating favorable conditions for local data center development and reducing reliance on international facilities.

The Russia data center construction market refers to the comprehensive ecosystem of planning, designing, building, and commissioning data center facilities within the Russian Federation. This market encompasses all aspects of data center development, from initial site selection and architectural design to mechanical and electrical systems installation, cooling infrastructure deployment, and final commissioning of operational facilities.

Construction activities include the development of various facility types such as enterprise data centers built for specific organizations, colocation facilities designed to house multiple tenants, hyperscale data centers supporting cloud service providers, and edge computing facilities positioned closer to end users. The market involves specialized contractors, technology vendors, equipment suppliers, and consulting firms working collaboratively to deliver state-of-the-art digital infrastructure.

Key components of data center construction include structural engineering, power and cooling systems, fire suppression technologies, security infrastructure, and network connectivity solutions. The market also encompasses renovation and expansion projects of existing facilities, reflecting the evolving needs of digital service providers and enterprises requiring enhanced capacity and capabilities.

Russia’s data center construction market demonstrates remarkable resilience and growth potential despite global economic uncertainties. The sector benefits from strong domestic demand for digital services, government support for technological sovereignty, and increasing adoption of cloud computing across various industries. Construction activities focus primarily on major urban centers, with Moscow and St. Petersburg leading development initiatives.

Market drivers include the rapid digitization of business processes, growing e-commerce activities, increased demand for data storage and processing capabilities, and regulatory requirements for data localization. The construction sector has adapted to incorporate advanced technologies such as liquid cooling systems, renewable energy integration, and modular construction approaches to enhance efficiency and reduce environmental impact.

Investment trends show significant capital allocation toward hyperscale facilities capable of supporting major cloud service providers and telecommunications companies. The market benefits from government digitization spending increasing by approximately 18% annually, creating substantial opportunities for data center construction companies and technology vendors. Regional expansion beyond traditional metropolitan areas presents additional growth opportunities as digital services penetrate smaller cities and rural areas.

Strategic insights reveal several critical factors shaping the Russia data center construction market landscape:

Market maturation indicators suggest the sector is transitioning from basic infrastructure development to sophisticated, technology-driven facilities incorporating artificial intelligence, automation, and predictive maintenance capabilities. This evolution reflects the growing sophistication of Russian enterprises and their digital infrastructure requirements.

Digital transformation initiatives across Russian enterprises serve as the primary catalyst for data center construction demand. Organizations increasingly recognize the strategic importance of reliable, secure, and scalable digital infrastructure to support their business operations and competitive positioning. The accelerated adoption of cloud computing, big data analytics, and artificial intelligence applications creates substantial demand for modern data center facilities.

Government digitization programs significantly contribute to market growth through substantial investments in digital infrastructure and services. Federal and regional authorities prioritize technological sovereignty and data security, creating favorable conditions for domestic data center development. Regulatory requirements for data localization ensure that sensitive information remains within Russian borders, driving demand for local facilities.

E-commerce expansion and digital services proliferation generate increasing requirements for data storage, processing, and delivery capabilities. The growth of online retail, digital banking, streaming services, and social media platforms creates substantial demand for robust data center infrastructure. Telecommunications modernization and 5G network deployment further amplify the need for edge computing facilities and enhanced connectivity infrastructure.

Enterprise modernization efforts drive demand for colocation services and private data center facilities as organizations seek to replace aging infrastructure with modern, efficient solutions. The increasing complexity of business applications and data management requirements necessitates sophisticated data center environments capable of supporting diverse workloads and ensuring high availability.

Economic uncertainties and geopolitical tensions create challenges for data center construction projects, particularly regarding international technology procurement and financing arrangements. Sanctions and trade restrictions may limit access to certain advanced technologies and equipment, potentially impacting construction timelines and project costs.

Skilled workforce shortages present significant challenges for the data center construction industry, as projects require specialized expertise in areas such as electrical systems, cooling technologies, and network infrastructure. The limited availability of qualified technicians, engineers, and project managers can constrain market growth and increase labor costs.

Energy infrastructure limitations in certain regions may restrict data center development opportunities, particularly for large-scale facilities requiring substantial power capacity. Grid reliability concerns and power cost variations across different regions influence site selection decisions and project feasibility assessments.

Regulatory complexities and lengthy approval processes can delay construction projects and increase development costs. Compliance requirements for environmental standards, building codes, and security regulations may extend project timelines and require additional resources for documentation and certification processes.

Capital intensity of data center construction projects requires significant upfront investments, potentially limiting market participation to well-funded organizations and creating barriers for smaller players seeking to enter the market.

Edge computing expansion presents substantial opportunities for data center construction companies as organizations seek to deploy smaller facilities closer to end users. The growing demand for low-latency applications, IoT deployments, and real-time data processing creates requirements for distributed data center infrastructure across various geographic locations.

Renewable energy integration offers significant opportunities for construction companies specializing in sustainable data center solutions. The increasing focus on environmental responsibility and energy cost optimization drives demand for facilities incorporating solar panels, wind power, and advanced energy management systems.

Regional expansion beyond traditional metropolitan areas presents growth opportunities as digital services penetrate smaller cities and rural regions. Government initiatives to improve digital connectivity and economic development in regional areas create demand for local data center infrastructure.

Retrofit and modernization projects offer substantial market potential as existing facilities require upgrades to meet evolving performance, efficiency, and security standards. Many older data centers need comprehensive renovations to support modern workloads and comply with current regulations.

Specialized facility development creates opportunities for niche construction services, including high-performance computing centers, research facilities, and industry-specific data centers designed for sectors such as healthcare, finance, and government services. These specialized requirements often command premium pricing and long-term contracts.

Supply chain evolution significantly impacts the Russia data center construction market, with increasing emphasis on domestic suppliers and technology providers. The shift toward local sourcing creates opportunities for Russian manufacturers while potentially affecting project costs and timelines. Construction companies adapt their procurement strategies to ensure reliable access to critical components and materials.

Technology advancement drives continuous evolution in data center design and construction methodologies. Innovations in cooling technologies, power management systems, and building materials enable more efficient and sustainable facilities. Liquid cooling adoption increases by 32% annually in high-density computing environments, reflecting the industry’s response to evolving performance requirements.

Competitive landscape dynamics show increasing collaboration between construction companies, technology vendors, and service providers to deliver comprehensive solutions. Strategic partnerships enable companies to offer end-to-end services from initial design through ongoing operations and maintenance.

Customer expectations continue to evolve, with clients demanding faster construction timelines, enhanced energy efficiency, and greater flexibility in facility design. Modular construction approaches and prefabricated solutions gain popularity as methods to accelerate project delivery while maintaining quality standards.

Regulatory environment changes influence construction practices and technology choices, with increasing emphasis on environmental compliance, energy efficiency standards, and security requirements. Construction companies must stay current with evolving regulations to ensure project compliance and avoid costly modifications.

Comprehensive market analysis employed multiple research methodologies to ensure accurate and reliable insights into the Russia data center construction market. Primary research activities included extensive interviews with industry executives, construction company leaders, technology vendors, and end-user organizations to gather firsthand perspectives on market trends, challenges, and opportunities.

Secondary research encompassed detailed analysis of industry reports, government publications, company financial statements, and regulatory documents to establish market context and validate primary research findings. Data collection focused on construction activity levels, project pipelines, technology adoption patterns, and competitive landscape dynamics.

Market sizing methodology utilized bottom-up and top-down approaches to estimate market dimensions and growth projections. Analysis considered factors such as construction project values, facility capacity additions, regional development patterns, and technology investment levels to develop comprehensive market assessments.

Validation processes included cross-referencing multiple data sources, conducting follow-up interviews with key stakeholders, and applying statistical analysis techniques to ensure data accuracy and reliability. Expert panels provided additional validation of key findings and market projections.

Analytical framework incorporated quantitative and qualitative assessment methods to evaluate market drivers, restraints, opportunities, and competitive dynamics. Scenario analysis examined potential market developments under various economic and regulatory conditions to provide robust insights for stakeholders.

Moscow region dominates the Russia data center construction market, accounting for approximately 45% of total construction activity. The capital region benefits from concentrated business activity, excellent connectivity infrastructure, and proximity to major enterprises and government organizations. Large-scale hyperscale facilities and enterprise data centers represent the primary construction focus, with several major projects under development or recently completed.

St. Petersburg emerges as the second-largest market, capturing roughly 20% of construction activity. The city’s strategic location, skilled workforce availability, and growing technology sector create favorable conditions for data center development. Both colocation facilities and enterprise data centers experience strong demand, supported by the region’s industrial base and proximity to European markets.

Regional centers including Novosibirsk, Yekaterinburg, and Kazan demonstrate increasing construction activity as digital services expand beyond traditional metropolitan areas. These markets benefit from government initiatives to improve regional digital infrastructure and growing local demand for data center services. Regional market growth reaches 18% annually, outpacing traditional metropolitan areas.

Southern regions including Rostov-on-Don and Krasnodar show emerging potential for data center construction, driven by economic development initiatives and improving connectivity infrastructure. These markets typically focus on smaller-scale facilities serving local enterprises and government organizations.

Siberian markets present unique opportunities due to favorable climate conditions for natural cooling and competitive energy costs. Several construction projects leverage these advantages to develop energy-efficient facilities serving both domestic and international clients seeking cost-effective data center solutions.

Market leadership in Russia’s data center construction sector includes both domestic and international companies offering comprehensive construction and engineering services. The competitive environment emphasizes technical expertise, project execution capabilities, and understanding of local regulatory requirements.

Competitive strategies focus on technological innovation, energy efficiency, and comprehensive service offerings spanning design, construction, and ongoing operations. Companies increasingly emphasize sustainability credentials and advanced cooling technologies to differentiate their offerings in the competitive marketplace.

Partnership arrangements between construction companies, technology vendors, and service providers create comprehensive solutions for clients seeking turnkey data center development. These collaborations enable companies to offer specialized expertise while sharing project risks and expanding market reach.

By Facility Type:

By Construction Type:

By End User:

Hyperscale facility construction represents the fastest-growing segment, driven by cloud service provider expansion and increasing demand for large-scale computing resources. These projects typically require substantial capital investment and specialized expertise in areas such as advanced cooling systems, high-density power distribution, and automated management systems. Construction timelines often extend 18-24 months due to complexity and scale requirements.

Enterprise data center development focuses on customized solutions meeting specific organizational requirements for security, compliance, and performance. These facilities often incorporate specialized features such as enhanced physical security, redundant systems, and integration with existing enterprise infrastructure. Construction approaches emphasize flexibility and future expansion capabilities.

Colocation facility construction requires careful planning to accommodate multiple tenants with varying requirements while maintaining security and operational efficiency. Design considerations include flexible space allocation, diverse connectivity options, and scalable power and cooling infrastructure. These facilities often feature modular designs enabling rapid tenant deployment and configuration changes.

Edge computing center development emphasizes rapid deployment and cost-effective construction approaches. These smaller facilities typically utilize prefabricated components and standardized designs to minimize construction time and costs. Location selection focuses on proximity to end users and existing network infrastructure.

Retrofit construction projects present unique challenges requiring creative engineering solutions to adapt existing buildings for data center use. These projects often involve significant structural modifications, power infrastructure upgrades, and cooling system installations while working within existing architectural constraints.

Construction companies benefit from strong market demand and premium pricing for specialized data center construction services. The sector offers opportunities for long-term relationships with clients requiring ongoing expansion and modernization services. Technical expertise development in data center construction creates competitive advantages and barriers to entry for competitors.

Technology vendors gain access to growing markets for specialized equipment including cooling systems, power distribution units, monitoring solutions, and security technologies. The emphasis on energy efficiency and sustainability creates demand for innovative products and solutions. Partnership opportunities with construction companies enable comprehensive service offerings.

End-user organizations benefit from improved digital infrastructure supporting business growth and operational efficiency. Modern data center facilities provide enhanced reliability, security, and scalability compared to legacy infrastructure. Access to advanced technologies and professional management services reduces operational complexity and costs.

Regional economies benefit from substantial capital investment, job creation, and technology sector development associated with data center construction projects. These facilities often attract additional technology companies and service providers, creating economic multiplier effects in local communities.

Government stakeholders achieve strategic objectives related to digital sovereignty, economic development, and technological advancement through domestic data center infrastructure development. These facilities support government digitization initiatives while reducing dependence on international infrastructure providers.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability integration emerges as a dominant trend, with construction projects increasingly incorporating renewable energy sources, advanced cooling technologies, and green building materials. Energy efficiency improvements of 25-30% are commonly achieved through innovative design approaches and technology integration. This trend reflects both environmental consciousness and operational cost optimization objectives.

Modular construction adoption accelerates as organizations seek faster deployment timelines and greater flexibility in facility design. Prefabricated components and standardized modules enable construction time reductions while maintaining quality standards. This approach particularly benefits edge computing deployments and rapid capacity expansion projects.

Automation integration transforms data center construction and operations, with facilities incorporating artificial intelligence, machine learning, and automated management systems. These technologies enhance operational efficiency, reduce human error, and enable predictive maintenance capabilities. Construction projects increasingly include infrastructure to support these advanced technologies.

Edge computing proliferation drives demand for smaller, distributed facilities positioned closer to end users. This trend requires new construction approaches emphasizing rapid deployment, standardized designs, and remote management capabilities. Edge facility construction grows at 40% annually, reflecting the increasing importance of low-latency applications.

Security enhancement becomes increasingly critical, with construction projects incorporating advanced physical security measures, biometric access controls, and comprehensive monitoring systems. The emphasis on data protection and facility security drives demand for specialized construction expertise and security technology integration.

Major construction projects across Russia demonstrate the market’s growth trajectory and technological advancement. Several hyperscale facilities have commenced construction in the Moscow region, incorporating state-of-the-art cooling systems and renewable energy integration. These projects represent significant capital investments and showcase the industry’s commitment to modern, efficient infrastructure.

Technology partnerships between construction companies and international vendors enable access to advanced data center technologies despite global supply chain challenges. These collaborations focus on energy-efficient solutions, automated management systems, and sustainable construction materials. Strategic alliances help companies navigate regulatory requirements and technology transfer considerations.

Regulatory developments include updated building codes and environmental standards specifically addressing data center construction requirements. New regulations emphasize energy efficiency, environmental protection, and security standards while streamlining approval processes for qualified projects. These changes create more predictable regulatory environments for construction planning.

Investment announcements from major technology companies and telecommunications providers signal continued market expansion. Several organizations have announced substantial capital commitments for data center infrastructure development, creating substantial opportunities for construction companies and technology vendors.

Innovation initiatives focus on developing domestic capabilities in critical technology areas including cooling systems, power management, and monitoring solutions. Research and development programs aim to reduce dependence on international suppliers while creating competitive advantages for Russian construction companies.

MarkWide Research recommends that construction companies focus on developing specialized expertise in emerging technologies such as liquid cooling, renewable energy integration, and automated management systems. These capabilities will become increasingly important as clients demand more sophisticated and efficient facilities.

Strategic partnerships with technology vendors and service providers should be prioritized to offer comprehensive solutions spanning design, construction, and ongoing operations. These collaborations enable companies to differentiate their offerings while sharing risks and expanding market reach.

Regional expansion strategies should consider emerging markets beyond traditional metropolitan areas, as digital infrastructure requirements expand throughout Russia. Early market entry in developing regions can establish competitive advantages and long-term client relationships.

Sustainability credentials development becomes essential as clients increasingly prioritize environmental responsibility and operational cost optimization. Companies should invest in green building expertise, renewable energy integration capabilities, and energy-efficient construction methodologies.

Workforce development initiatives should address skilled labor shortages through training programs, partnerships with educational institutions, and knowledge transfer from experienced professionals. Building internal capabilities reduces dependence on external contractors while improving project quality and timelines.

Technology monitoring and adaptation processes should be established to stay current with rapidly evolving data center technologies and construction methodologies. Regular assessment of emerging trends enables proactive adaptation and competitive positioning.

Market growth prospects remain robust, with the Russia data center construction market expected to maintain strong expansion driven by continued digital transformation and infrastructure modernization requirements. MWR analysis projects sustained growth as organizations increasingly recognize the strategic importance of modern data center infrastructure for business competitiveness and operational efficiency.

Technology evolution will continue reshaping construction practices, with increasing emphasis on automation, artificial intelligence, and sustainable design approaches. Future facilities will incorporate more sophisticated monitoring and management systems while achieving higher levels of energy efficiency and environmental responsibility.

Geographic expansion beyond traditional metropolitan areas will create new market opportunities as digital services penetrate regional markets and government initiatives improve connectivity infrastructure. This expansion will require adapted construction approaches suitable for smaller markets and local conditions.

Edge computing growth will drive demand for distributed infrastructure requiring new construction methodologies emphasizing rapid deployment, standardization, and remote management capabilities. This trend will create opportunities for companies specializing in modular construction and prefabricated solutions.

Sustainability requirements will become increasingly stringent, driving demand for renewable energy integration, advanced cooling technologies, and environmentally responsible construction materials. Companies developing expertise in these areas will gain competitive advantages in the evolving marketplace.

Market consolidation may occur as smaller players seek partnerships or acquisition opportunities to compete effectively with larger, well-resourced competitors. This trend could create opportunities for strategic acquisitions and market share expansion for established companies.

The Russia data center construction market presents substantial opportunities for growth and development, driven by strong domestic demand, government support for digital infrastructure, and increasing adoption of cloud computing and digital services. Despite challenges related to economic uncertainties and technology access, the market demonstrates resilience and adaptation capabilities that position it for continued expansion.

Key success factors for market participants include developing specialized technical expertise, establishing strategic partnerships, and maintaining focus on sustainability and energy efficiency. Companies that can navigate regulatory requirements while delivering innovative, cost-effective solutions will be well-positioned to capitalize on market opportunities.

Future market development will be shaped by technological advancement, regulatory evolution, and changing customer requirements. The emphasis on edge computing, sustainability, and automation will create new opportunities while requiring adaptation of traditional construction approaches. Organizations that proactively address these trends while building strong operational capabilities will achieve sustainable competitive advantages in this dynamic and growing market.

What is Data Center Construction?

Data Center Construction refers to the process of building facilities that house computer systems and associated components, such as telecommunications and storage systems. These centers are crucial for managing data and supporting various IT operations across industries.

What are the key players in the Russia Data Center Construction Market?

Key players in the Russia Data Center Construction Market include companies like DataLine, IXcellerate, and Rostelecom, which are involved in the design, construction, and operation of data centers. These companies focus on providing reliable infrastructure and services to meet the growing demand for data processing and storage, among others.

What are the main drivers of growth in the Russia Data Center Construction Market?

The main drivers of growth in the Russia Data Center Construction Market include the increasing demand for cloud services, the rise of big data analytics, and the expansion of e-commerce. Additionally, the need for enhanced data security and compliance with regulations is pushing companies to invest in new data center facilities.

What challenges does the Russia Data Center Construction Market face?

The Russia Data Center Construction Market faces challenges such as high construction costs, regulatory hurdles, and the need for skilled labor. Additionally, the geopolitical climate can impact investment and operational stability in the region.

What opportunities exist in the Russia Data Center Construction Market?

Opportunities in the Russia Data Center Construction Market include the potential for green data centers that utilize renewable energy sources and energy-efficient technologies. Furthermore, the growing trend of digital transformation across various sectors presents a significant opportunity for new data center projects.

What trends are shaping the Russia Data Center Construction Market?

Trends shaping the Russia Data Center Construction Market include the adoption of modular data center designs, increased focus on sustainability, and the integration of advanced cooling technologies. These trends are driven by the need for efficiency and the growing emphasis on reducing the environmental impact of data center operations.

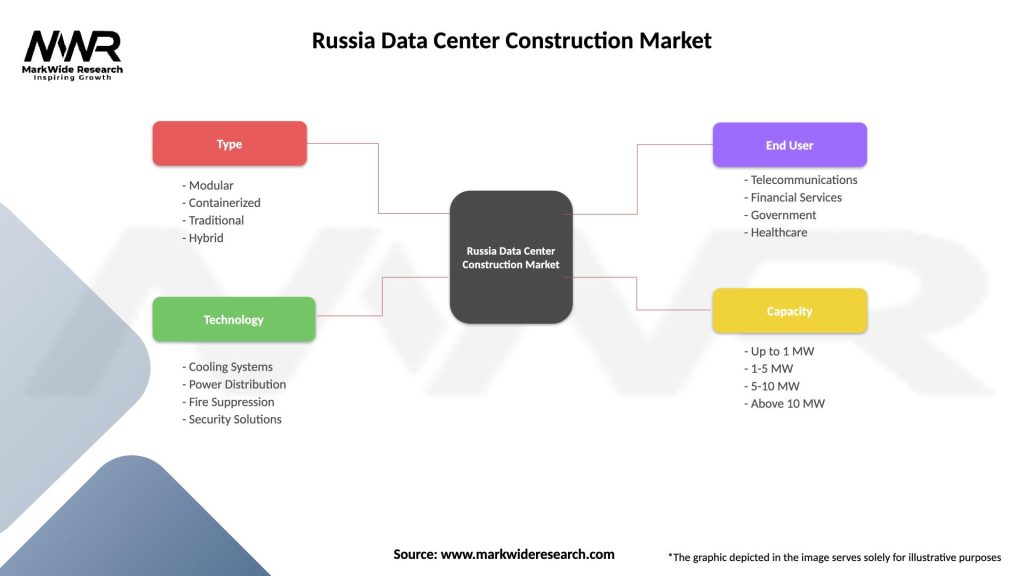

Russia Data Center Construction Market

| Segmentation Details | Description |

|---|---|

| Type | Modular, Containerized, Traditional, Hybrid |

| Technology | Cooling Systems, Power Distribution, Fire Suppression, Security Solutions |

| End User | Telecommunications, Financial Services, Government, Healthcare |

| Capacity | Up to 1 MW, 1-5 MW, 5-10 MW, Above 10 MW |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Russia Data Center Construction Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.