444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The refuse-derived fuel (RDF) market refers to the segment of the waste management industry that focuses on the conversion of non-recyclable waste into fuel for energy generation. RDF is produced by sorting and processing municipal solid waste (MSW) to extract valuable components, such as paper, plastic, and organic materials, which are then transformed into a fuel source. The RDF market has gained significant traction in recent years due to the increasing need for sustainable waste management solutions and the rising demand for renewable energy.

Meaning

Refuse-derived fuel (RDF) is a type of fuel derived from non-recyclable waste materials. It involves the sorting and processing of municipal solid waste (MSW) to remove recyclable materials, such as glass, metals, and paper. The remaining organic and high-calorific value materials are processed further to produce RDF, which can be used as a fuel source in various industries, including power generation, cement kilns, and industrial boilers.

Executive Summary

The RDF market has experienced substantial growth as governments and industries seek sustainable waste management solutions and renewable energy sources. The conversion of non-recyclable waste into RDF offers several advantages, including waste reduction, energy recovery, and reduced greenhouse gas emissions. The market is driven by environmental regulations, increasing landfill costs, and the growing focus on circular economy principles.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The RDF market is influenced by a combination of factors, including regulatory frameworks, waste management practices, energy demand, and public perception. The market dynamics are driven by the need for sustainable waste management solutions, the shift towards renewable energy sources, and the collaboration between waste management companies, energy producers, and government bodies.

Stringent environmental regulations and waste management targets drive the demand for RDF as a renewable energy source. Governments set targets and provide incentives to promote the use of RDF, ensuring compliance with waste reduction and renewable energy generation goals.

The rising landfill costs and limited landfill space create financial incentives for waste management companies and industries to explore alternative waste management options, such as RDF. The utilization of RDF reduces disposal expenses and contributes to a circular economy by maximizing resource recovery.

Public perception and acceptance play a crucial role in the market dynamics of RDF. Awareness campaigns, stakeholder engagement, and transparent communication can address concerns and increase public acceptance of RDF as a sustainable waste management and energy solution.

Collaboration between waste management companies, energy producers, and government bodies is essential for the development of RDF facilities, infrastructure, and technology. Public-private partnerships and research collaborations facilitate the advancement of RDF production and utilization, promoting market growth.

Regional Analysis

The RDF market can be analyzed based on regional segments, including North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. Each region has its waste management regulations, renewable energy targets, and market dynamics.

Competitive Landscape

Leading Companies in the Refuse Derived Fuel Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The RDF market can be segmented based on the following criteria:

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact

The Covid-19 pandemic had a significant impact on the RDF market. The lockdown measures and restrictions led to disruptions in waste collection and processing, affecting RDF production and utilization. Reduced industrial activities and changes in waste composition also impacted the availability of suitable waste materials for RDF production.

However, the pandemic also highlighted the importance of sustainable waste management and renewable energy sources. The focus on building resilient and sustainable economies post-pandemic has increased the interest in RDF as a solution for waste management and energy recovery.

The impact of the pandemic varied across regions, depending on the severity of the outbreak and the level of waste management infrastructure in place. Some regions witnessed delays in RDF facility construction and investments, while others continued to prioritize sustainable waste management practices.

Key Industry Developments

Analyst Suggestions

Future Outlook

The future outlook for the RDF market is positive, driven by the increasing focus on sustainable waste management practices, renewable energy generation, and resource recovery. The rising landfill costs, stringent environmental regulations, and the need to reduce carbon emissions will further propel the demand for RDF as a renewable fuel source.

Technological advancements, research and development initiatives, and collaborations among industry stakeholders will continue to enhance RDF production processes, improve quality standards, and address environmental concerns. The expansion of RDF utilization in power generation, cement production, and industrial processes will contribute to a more sustainable and diversified energy mix.

The RDF market is expected to witness substantial growth globally, with Europe leading the way due to its stringent waste management regulations and renewable energy targets. North America, Asia Pacific, Latin America, and the Middle East and Africa are also expected to experience significant market growth, driven by increasing waste generation, government support, and the adoption of sustainable waste management practices.

Conclusion

In conclusion, the RDF market presents a promising solution for sustainable waste management and renewable energy generation. With the right technological advancements, infrastructure investments, and public engagement, RDF can contribute significantly to a circular economy, reduced landfill waste, and a greener future.

What is Refuse Derived Fuel?

Refuse Derived Fuel (RDF) is a type of fuel produced from various types of waste materials, including municipal solid waste, industrial waste, and commercial waste. It is processed to remove non-combustible materials and is used primarily in energy generation and as a substitute for fossil fuels.

What are the key companies in the Refuse Derived Fuel Market?

Key companies in the Refuse Derived Fuel Market include Veolia, SUEZ, and Covanta, which are involved in waste management and energy recovery. These companies focus on converting waste into energy and developing sustainable waste-to-energy solutions, among others.

What are the drivers of growth in the Refuse Derived Fuel Market?

The growth of the Refuse Derived Fuel Market is driven by increasing waste generation, the need for sustainable waste management solutions, and rising energy demands. Additionally, government regulations promoting renewable energy sources contribute to the market’s expansion.

What challenges does the Refuse Derived Fuel Market face?

The Refuse Derived Fuel Market faces challenges such as fluctuating waste composition, high initial investment costs for processing facilities, and regulatory hurdles. These factors can impact the efficiency and profitability of RDF production and utilization.

What opportunities exist in the Refuse Derived Fuel Market?

Opportunities in the Refuse Derived Fuel Market include advancements in waste processing technologies, increasing investments in renewable energy projects, and growing awareness of environmental sustainability. These factors can enhance the adoption of RDF in various industries.

What trends are shaping the Refuse Derived Fuel Market?

Trends in the Refuse Derived Fuel Market include the integration of circular economy principles, innovations in waste-to-energy technologies, and the development of stricter waste management regulations. These trends are driving the evolution of RDF applications in energy generation and industrial processes.

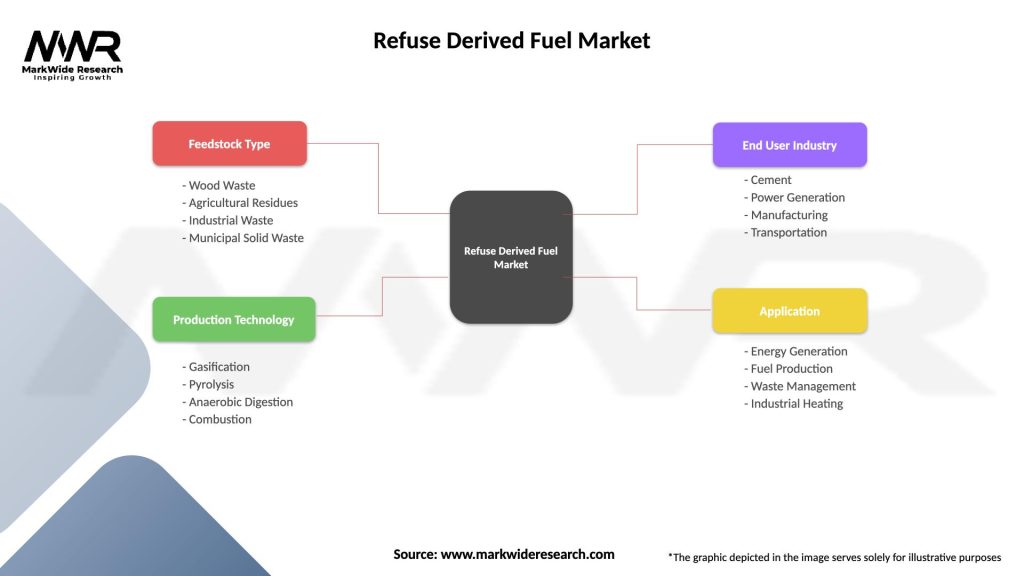

Refuse Derived Fuel Market

| Segmentation Details | Description |

|---|---|

| Feedstock Type | Wood Waste, Agricultural Residues, Industrial Waste, Municipal Solid Waste |

| Production Technology | Gasification, Pyrolysis, Anaerobic Digestion, Combustion |

| End User Industry | Cement, Power Generation, Manufacturing, Transportation |

| Application | Energy Generation, Fuel Production, Waste Management, Industrial Heating |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Refuse Derived Fuel Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA