Refinancing refers to the process of replacing an existing loan with a new one, typically with better terms and conditions. It is a financial strategy that allows borrowers to obtain a lower interest rate, reduce their monthly payments, or access additional funds. The refinancing market has witnessed significant growth in recent years, driven by various factors such as favorable interest rates, changing economic conditions, and evolving borrower needs.

Meaning

Refinancing is a financial strategy that involves replacing an existing loan or mortgage with a new one, often with more favorable terms and conditions. This process allows borrowers to take advantage of lower interest rates, reduce their monthly payments, or access additional funds for various purposes such as debt consolidation, home improvements, or education expenses. Refinancing can be done for different types of loans, including mortgages, auto loans, student loans, and personal loans.

Executive Summary

The refinancing market has experienced substantial growth in recent years, driven by several key factors. Low-interest rates have been a major driver, as borrowers seek to capitalize on favorable market conditions to secure better loan terms. Additionally, changing economic conditions, such as improved credit scores or increased home equity, have created opportunities for borrowers to refinance their loans at more favorable rates.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Growing Demand for Mortgage Refinancing: The mortgage refinancing segment holds a significant share in the overall refinancing market, driven by the desire of homeowners to take advantage of lower interest rates and reduce their monthly mortgage payments.

Increasing Awareness and Accessibility: The availability of online lending platforms and digital tools has made the refinancing process more accessible to a broader range of borrowers. Additionally, the growing awareness about the benefits of refinancing has contributed to the market’s expansion.

Impact of Interest Rate Fluctuations: The refinancing market is highly sensitive to changes in interest rates. When interest rates are low, borrowers are more likely to refinance their loans to secure better terms. Conversely, rising interest rates can dampen demand for refinancing.

Regulatory Environment: The refinancing market is subject to regulatory oversight to protect consumers and ensure fair lending practices. Compliance with regulations such as the Truth in Lending Act (TILA) and the Home Mortgage Disclosure Act (HMDA) is crucial for lenders operating in this market.

Technological Advancements: The adoption of advanced technologies, such as artificial intelligence and machine learning, has streamlined the refinancing process, making it faster and more efficient for both lenders and borrowers. These technological advancements have also enhanced risk assessment and fraud prevention measures.

Market Drivers

Favorable Interest Rates: Low-interest rates create an incentive for borrowers to refinance their existing loans to secure better terms, leading to increased market activity.

Economic Conditions: Improvements in the overall economy, such as rising incomes, job stability, and increased home equity, provide borrowers with the confidence and financial capacity to pursue refinancing opportunities.

Debt Consolidation: Many borrowers opt for refinancing to consolidate their debts into a single loan, simplifying their financial obligations and potentially reducing their overall interest payments.

Access to Additional Funds: Refinancing allows homeowners to tap into their home equity and access additional funds for various purposes, such as home renovations, education expenses, or investment opportunities.

Evolving Borrower Needs: As borrowers’ financial goals and priorities change over time, refinancing offers flexibility and customization options to align their loan terms with their current requirements.

Market Restraints

Stringent Lending Standards: Lenders may impose stricter eligibility criteria and requirements for refinancing, making it challenging for some borrowers to qualify for better loan terms.

Closing Costs and Fees: Refinancing involves various fees and closing costs, such as appraisal fees, origination fees, and title insurance, which can add significant upfront expenses for borrowers.

Creditworthiness and Risk Assessment: Borrowers with less-than-ideal credit scores or a higher risk profile may face difficulties in obtaining favorable refinancing terms or may be subject to higher interest rates.

Market Volatility: Fluctuations in interest rates, housing market conditions, and economic uncertainties can impact borrower confidence and their willingness to pursue refinancing options.

Prepayment Penalties: Some loan agreements may impose penalties for early loan repayment, discouraging borrowers from refinancing their existing loans.

Market Opportunities

Technology-driven Innovation: The integration of advanced technologies, such as artificial intelligence, machine learning, and automation, presents opportunities to streamline the refinancing process, enhance customer experience, and improve risk assessment.

Targeted Marketing and Outreach: Lenders can leverage data analytics and personalized marketing strategies to identify potential refinancing candidates and offer tailored solutions that meet their specific needs.

Collaborations and Partnerships: Collaboration between fintech companies, traditional lenders, and other industry stakeholders can unlock synergies and create new opportunities for innovation and market expansion.

Education and Awareness Campaigns: Increasing consumer awareness about refinancing benefits, eligibility criteria, and the refinancing process can stimulate market growth by encouraging more borrowers to explore refinancing options.

Emerging Markets: The refinancing market is expanding beyond traditional segments, such as mortgages, into new areas such as student loans, auto loans, and personal loans. This diversification offers opportunities for lenders to tap into underserved markets and cater to a wider range of borrower needs.

Market Dynamics

The refinancing market is dynamic and influenced by various factors, including economic conditions, interest rate fluctuations, regulatory changes, and borrower preferences. Understanding these dynamics is crucial for lenders and industry participants to navigate market trends effectively and seize opportunities for growth.

The market’s growth is driven by favorable interest rates, changing economic conditions, and evolving borrower needs. Low-interest rates create an incentive for borrowers to refinance their loans and secure better terms, leading to increased market activity. Improvements in the overall economy, such as rising incomes and increased home equity, provide borrowers with the confidence and financial capacity to pursue refinancing opportunities.

Technological advancements have also had a significant impact on the market, making the refinancing process more accessible and efficient. The adoption of advanced technologies, such as artificial intelligence and machine learning, has streamlined the loan application and approval processes, reducing the time and effort required for both lenders and borrowers. These technological advancements have also enhanced risk assessment and fraud prevention measures, improving the overall security and efficiency of the refinancing market.

However, the market is not without its challenges. Stricter lending standards, closing costs, and fees can make it difficult for some borrowers to qualify for refinancing or deter them from pursuing the option altogether. Market volatility, including fluctuations in interest rates and economic uncertainties, can also impact borrower confidence and their willingness to pursue refinancing opportunities.

To capitalize on the market’s opportunities, lenders can leverage technology-driven innovation to enhance the refinancing process and improve customer experience. Targeted marketing and outreach efforts, supported by data analytics, can help identify potential refinancing candidates and offer tailored solutions. Collaborations and partnerships between industry stakeholders can unlock synergies and drive innovation. Additionally, education and awareness campaigns can play a crucial role in increasing consumer understanding of refinancing benefits and eligibility criteria, thereby stimulating market growth.

Regional Analysis

The refinancing market exhibits regional variations influenced by economic conditions, regulatory environments, and borrower preferences. While the market’s fundamentals remain similar across regions, specific factors contribute to unique dynamics in each area.

North America: The refinancing market in North America is mature and highly developed. The United States, in particular, accounts for a significant share of the global refinancing market due to the country’s large mortgage market and favorable interest rate environment. In Canada, mortgage refinancing is also a common practice, driven by similar factors such as interest rate fluctuations and changing borrower needs.

Europe: Europe has a diverse refinancing market, with variations across countries. The mortgage refinancing market is prominent in countries such as the United Kingdom, Germany, and France. Regulatory frameworks, including affordability assessments and loan-to-value ratios, shape the market dynamics in these regions.

Asia Pacific: The refinancing market in Asia Pacific is experiencing significant growth due to rising homeownership rates, increasing disposable incomes, and expanding middle-class populations. Countries such as China, India, and Australia have witnessed a surge in mortgage refinancing activities.

Latin America: In Latin America, the refinancing market is influenced by economic conditions, including interest rate fluctuations and inflation rates. Countries like Brazil, Mexico, and Argentina have active refinancing markets, driven by factors such as the desire to reduce debt burdens and access additional funds for investment or education.

Middle East and Africa: The refinancing market in the Middle East and Africa is characterized by unique factors such as expatriate populations, oil-driven economies, and evolving regulatory environments. Countries like the United Arab Emirates, Saudi Arabia, and South Africa have seen growth in mortgage refinancing activities.

Understanding the regional dynamics and tailoring strategies to specific market conditions is essential for industry participants to effectively operate and grow their presence in different regions.

Competitive Landscape

Leading Companies in the Refinancing Market:

Wells Fargo & Company

JPMorgan Chase & Co.

Bank of America Corporation

Quicken Loans, LLC

CitiGroup Inc.

U.S. Bank

PNC Financial Services Group, Inc.

SoFi

LendingTree, Inc.

Better.com

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

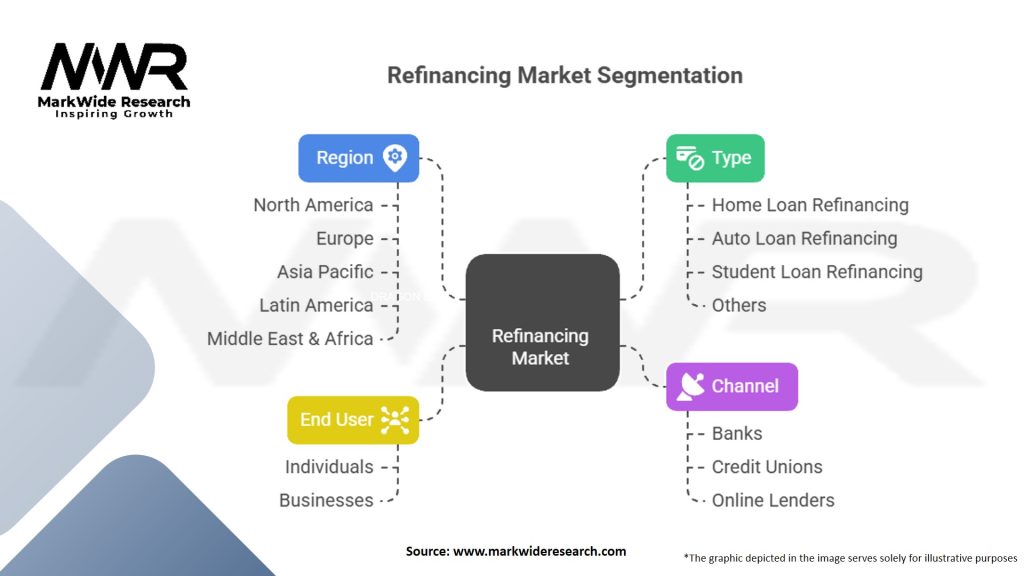

Segmentation

The refinancing market can be segmented based on various factors, including loan type, borrower profile, and industry sector. Common segments include mortgage refinancing, auto loan refinancing, student loan refinancing, and personal loan refinancing.

Mortgage Refinancing: This segment focuses on refinancing residential mortgages. It includes both fixed-rate and adjustable-rate mortgages. Borrowers in this segment typically aim to reduce their monthly mortgage payments, secure a lower interest rate, or access their home equity for other purposes.

Auto Loan Refinancing: Auto loan refinancing involves replacing an existing auto loan with a new one, often with more favorable terms. Borrowers in this segment seek to lower their interest rates, reduce their monthly payments, or extend their loan terms.

Student Loan Refinancing: Student loan refinancing enables borrowers to replace their existing student loans with a new loan that offers better interest rates and repayment terms. This segment targets borrowers looking to lower their monthly payments, save on interest costs, or simplify their loan repayment by consolidating multiple loans into one.

Personal Loan Refinancing: Personal loan refinancing allows borrowers to replace their existing personal loans with new loans that offer better terms and conditions. Borrowers in this segment may aim to reduce their interest rates, extend their repayment periods, or consolidate their debts into a single loan.

Segmentation in the refinancing market helps lenders and industry participants tailor their products and marketing strategies to specific borrower needs and preferences, enhancing their competitiveness and market relevance.

Category-wise Insights

Mortgage Refinancing Insights:

Homeowners often choose to refinance their mortgages to take advantage of lower interest rates, reduce their monthly mortgage payments, or switch from adjustable-rate mortgages to fixed-rate mortgages.

Cash-out refinancing allows homeowners to access their home equity and use the funds for purposes such as home improvements, debt consolidation, or investment opportunities.

Government-backed mortgage refinancing programs, such as the Home Affordable Refinance Program (HARP) in the United States, provide options for borrowers with limited equity or who are underwater on their mortgages.

Auto Loan Refinancing Insights:

Auto loan refinancing offers borrowers the opportunity to obtain a lower interest rate, reduce their monthly payments, or change their loan term to better align with their financial goals.

Refinancing an auto loan can be particularly beneficial for borrowers who have improved their credit scores since the original loan was taken out, as they may qualify for more favorable terms.

Student Loan Refinancing Insights:

Student loan refinancing allows borrowers to combine multiple student loans into a single loan with a lower interest rate and simplified repayment terms.

Refinancing student loans can potentially save borrowers money on interest payments over the life of the loan, reduce their monthly payments, and provide a single monthly payment instead of multiple payments to different lenders.

Personal Loan Refinancing Insights:

Personal loan refinancing offers borrowers the opportunity to secure a lower interest rate, extend their repayment period, or consolidate their debts into a single loan for easier management.

Borrowers may consider refinancing personal loans to reduce their overall debt burden, save on interest costs, or simplify their finances by having a single monthly payment.

Understanding the unique insights and considerations for each category of refinancing can help lenders and industry participants cater to specific borrower needs and optimize their product offerings.

Key Benefits for Industry Participants and Stakeholders

Increased Market Share: By participating in the refinancing market, lenders can expand their customer base and increase their market share. Offering attractive refinancing options can attract borrowers from competitors and foster customer loyalty.

Revenue Generation: The refinancing market presents revenue opportunities for lenders through origination fees, interest income, and other associated fees. The increased volume of refinancing activities can contribute to overall profitability.

Customer Retention: Providing refinancing options allows lenders to retain existing customers who may otherwise seek refinancing opportunities with competitors. Retention of borrowers can lead to long-term customer relationships and potential cross-selling opportunities.

Enhanced Customer Experience: Streamlining the refinancing process, leveraging technology, and providing personalized solutions can improve the customer experience. Positive customer experiences contribute to customer satisfaction, brand reputation, and potential referrals.

Risk Management: Regular refinancing activities provide lenders with an opportunity to assess and manage their risk portfolios. Proper risk assessment and evaluation of borrower eligibility can contribute to maintaining a healthy loan portfolio.

Economic Growth: A vibrant refinancing market contributes to economic growth by providing borrowers with opportunities to reduce their debt burdens, access additional funds for investments or expenses, and stimulate overall consumer spending.

Industry participants and stakeholders can capitalize on these benefits by developing innovative products, adopting advanced technologies, and prioritizing customer-centric approaches.

SWOT Analysis

A SWOT analysis provides an assessment of the strengths, weaknesses, opportunities, and threats related to the refinancing market.

Strengths:

Low-interest rates create an incentive for borrowers to refinance, driving market growth.

Technological advancements streamline the refinancing process and enhance efficiency.

Increasing awareness and accessibility of refinancing options contribute to market expansion.

Diversification into different loan categories offers opportunities for growth and innovation.

Weaknesses:

Stringent lending standards and eligibility criteria may limit refinancing options for some borrowers.

Upfront closing costs and fees can deter borrowers from pursuing refinancing opportunities.

Market volatility and interest rate fluctuations can impact borrower confidence and market demand.

Opportunities:

Technology-driven innovation can streamline processes, enhance customer experience, and improve risk assessment.

Targeted marketing and outreach efforts can identify potential refinancing candidates and offer tailored solutions.

Collaboration and partnerships can unlock synergies and expand product offerings.

Education and awareness campaigns can stimulate market growth by increasing consumer understanding.

Threats:

Economic downturns or recessions can reduce borrower confidence and limit refinancing activities.

Regulatory changes or increased compliance requirements can impact the refinancing market’s operations.

Competition from traditional lenders and emerging fintech companies can pose challenges for market participants.

A comprehensive understanding of the SWOT analysis can assist industry participants in developing strategies to capitalize on strengths, mitigate weaknesses, leverage opportunities, and navigate potential threats in the refinancing market.

Market Key Trends

Digital Transformation: The refinancing market is experiencing a significant shift towards digital platforms and technology-driven solutions. Online lenders and fintech companies are leveraging advanced technologies to streamline processes, enhance customer experience, and expedite loan approvals.

Personalized Solutions: Borrowers are increasingly seeking personalized refinancing solutions tailored to their specific needs and financial goals. Lenders are leveraging data analytics and advanced algorithms to assess borrower profiles and offer customized loan options.

Automation and Efficiency: The adoption of automation in the refinancing process is improving efficiency and reducing turnaround times. Automated underwriting, document processing, and risk assessment are streamlining operations and enhancing the overall borrower experience.

Alternative Data and Credit Scoring: Traditional credit scoring models are being supplemented with alternative data sources, such as utility payments, rental histories, and online financial data. This allows lenders to assess borrower creditworthiness more accurately and offer refinancing options to a broader range of borrowers.

Sustainable and Green Refinancing: The focus on sustainability and environmental responsibility is extending to the refinancing market. Borrowers are increasingly seeking refinancing options that support energy-efficient home improvements or environmentally friendly initiatives.

Keeping abreast of these key trends enables industry participants to adapt their strategies, develop innovative solutions, and stay competitive in the evolving refinancing market.

Covid-19 Impact

The COVID-19 pandemic has had a significant impact on the refinancing market, both in the short term and potentially in the long term.

Short-term Impact:

Interest Rate Fluctuations: The pandemic caused interest rates to plummet to historic lows, creating an opportunity for borrowers to refinance and secure better terms. This led to a surge in refinancing activities, particularly in the mortgage market.

Economic Uncertainty: The pandemic brought economic uncertainty, including job losses and financial instability for many borrowers. This impacted refinancing decisions, as some borrowers prioritized financial stability and focused on maintaining their existing loans rather than pursuing refinancing options.

Market Volatility: Market volatility and changing economic conditions during the pandemic affected lender risk assessments and borrower eligibility criteria. Lenders may have tightened their lending standards, making it more challenging for some borrowers to qualify for refinancing.

Long-term Impact:

Shift in Borrower Priorities: The pandemic may have altered borrower priorities and financial goals. Some borrowers may seek refinancing options to improve cash flow, reduce debt burdens, or adapt to new financial circumstances.

Regulatory Changes: The economic impact of the pandemic may result in regulatory changes aimed at protecting borrowers and maintaining financial stability. These changes could impact the refinancing market’s operations, eligibility criteria, and risk management practices.

Evolving Borrower Needs: The pandemic highlighted the importance of flexibility and adaptability. Borrowers may increasingly seek refinancing options that offer more flexible terms, such as adjustable-rate mortgages or loan modifications.

Technological Acceleration: The pandemic accelerated the adoption of digital solutions and remote processes. This trend may continue in the refinancing market, with increased reliance on digital platforms for loan applications, document submissions, and virtual closings.

As the world recovers from the pandemic, the refinancing market is likely to adapt to the new economic landscape and borrower preferences.

Key Industry Developments

Expansion of Online Lenders: Online lenders and fintech companies have gained significant market share in the refinancing industry. Their user-friendly interfaces, quick approvals, and competitive rates have attracted borrowers seeking convenient refinancing options.

Partnership between Fintech and Traditional Lenders: Collaboration between fintech companies and traditional lenders has become more common. Fintech companies bring technological capabilities and innovative solutions, while traditional lenders offer established customer bases and regulatory expertise.

Increasing Focus on Data Security: With the rising adoption of digital platforms, data security and privacy have become paramount concerns. Industry participants are investing in robust security measures to protect borrower information and maintain trust in the refinancing process.

Regulatory Scrutiny and Compliance: Regulatory bodies are closely monitoring the refinancing market to ensure consumer protection and fair lending practices. Compliance requirements may evolve, impacting the operations and risk management practices of industry participants.

Expansion of Refinancing Offerings: Industry participants are diversifying their refinancing offerings beyond traditional mortgages to include auto loans, student loans, and personal loans. This diversification allows lenders to cater to a wider range of borrower needs and tap into new market segments.

Understanding these key industry developments allows market participants to adapt to changing dynamics, identify potential partnerships, and stay at the forefront of market trends.

Analyst Suggestions

Embrace Technological Innovation: Industry participants should invest in technology-driven solutions to streamline processes, enhance efficiency, and improve the overall borrower experience. Adopting artificial intelligence, machine learning, and automation can lead to faster approvals, more accurate risk assessments, and cost savings.

Enhance Customer Engagement: Developing personalized and customer-centric refinancing solutions is crucial for attracting and retaining borrowers. Investing in data analytics and customer relationship management systems can enable lenders to understand borrower preferences and offer tailored refinancing options.

Collaborate for Growth: Collaboration between lenders, fintech companies, and other industry stakeholders can unlock synergies and drive innovation. Partnerships can expand product offerings, improve technological capabilities, and reach a broader customer base.

Stay Compliant and Adaptable: Regulatory compliance is essential in the refinancing market. Industry participants should stay updated on regulatory changes, ensure adherence to compliance requirements, and have robust risk management practices in place.

Focus on Education and Awareness: Increasing consumer awareness about refinancing benefits, eligibility criteria, and the refinancing process is crucial for market growth. Lenders can invest in educational campaigns, provide clear and transparent information, and offer resources to help borrowers make informed refinancing decisions.

By implementing these suggestions, industry participants can position themselves for success in the competitive refinancing market and better serve borrower needs.

Future Outlook

The refinancing market is expected to continue growing, driven by various factors:

Favorable Interest Rates: Interest rates are expected to remain relatively low, creating incentives for borrowers to refinance their existing loans and secure better terms.

Technological Advancements: Continued advancements in technology will further streamline the refinancing process, making it faster, more efficient, and accessible to a broader range of borrowers.

Market Expansion: The refinancing market is likely to expand beyond traditional mortgage refinancing to include other loan categories, such as auto loans, student loans, and personal loans. This diversification will offer new growth opportunities for industry participants.

Regulatory Environment: Regulatory changes and compliance requirements may shape the refinancing market’s landscape. Lenders need to stay updated on regulatory developments and adapt their operations accordingly.

Economic Recovery: As economies recover from the COVID-19 pandemic, borrowers’ financial situations may improve, leading to increased demand for refinancing options to optimize their financial positions.

Conclusion

The refinancing market plays a vital role in providing borrowers with opportunities to improve their financial situations, access better terms, and manage their debts effectively. Understanding market dynamics, regional variations, and key industry developments is essential for industry participants to thrive in this competitive landscape.

By embracing technological innovations, enhancing customer engagement, and staying compliant with regulatory requirements, lenders can position themselves for growth and offer personalized refinancing solutions to meet borrower needs. Collaboration and partnerships can drive innovation and expand product offerings, while a focus on education and awareness can empower borrowers to make informed refinancing decisions.

What is refinancing?

Refinancing refers to the process of replacing an existing loan with a new one, typically to secure better terms, such as lower interest rates or different repayment schedules. This practice is common in various sectors, including mortgages, auto loans, and student loans.

What are the key players in the refinancing market?

Key players in the refinancing market include major financial institutions such as Quicken Loans, Wells Fargo, and Bank of America, which offer a range of refinancing options for consumers. These companies compete to provide attractive rates and services to borrowers, among others.

What are the main drivers of the refinancing market?

The refinancing market is primarily driven by factors such as fluctuating interest rates, changes in consumer credit scores, and the overall economic environment. Additionally, homeowners seeking to reduce monthly payments or consolidate debt contribute to market growth.

What challenges does the refinancing market face?

Challenges in the refinancing market include regulatory changes that can impact lending practices, rising interest rates that may deter borrowers, and increased competition among lenders. These factors can create uncertainty for both consumers and financial institutions.

What opportunities exist in the refinancing market?

Opportunities in the refinancing market include the potential for innovative financial products tailored to specific consumer needs, such as green refinancing options for energy-efficient homes. Additionally, the rise of digital platforms can enhance accessibility for borrowers.

What trends are shaping the refinancing market?

Current trends in the refinancing market include the growing use of technology to streamline the application process and the increasing popularity of cash-out refinancing. These trends reflect changing consumer preferences and advancements in financial technology.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.