The radiological detector market is a crucial segment of the global security and defense industry, offering detection and monitoring solutions for radiation threats and hazards. Radiological detectors play a vital role in safeguarding public health, ensuring nuclear safety, and countering radiological terrorism. With the increasing risk of radiological incidents, including nuclear accidents, illicit trafficking of radioactive materials, and nuclear proliferation, the demand for advanced radiological detection technologies continues to rise worldwide.

Meaning

Radiological detectors are specialized instruments designed to detect, measure, and identify ionizing radiation emitted by radioactive materials. These detectors utilize various technologies such as scintillation, semiconductor, gas-filled, and solid-state detectors to detect radiation sources and quantify radiation levels. Radiological detectors are employed in diverse applications including homeland security, border monitoring, customs inspection, environmental monitoring, medical imaging, and nuclear industry safety.

Executive Summary

The radiological detector market is witnessing significant growth driven by increasing security threats, technological advancements, regulatory compliance requirements, and government investments in nuclear security and radiation detection infrastructure. Key market players are focusing on developing innovative detection solutions with enhanced sensitivity, accuracy, portability, and interoperability to address evolving customer needs and emerging threats. Despite challenges such as regulatory constraints, budgetary constraints, and supply chain disruptions, the radiological detector market presents lucrative opportunities for industry participants to capitalize on growing demand for radiation detection and monitoring solutions.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Growing Nuclear Security Concerns: The proliferation of nuclear weapons, nuclear terrorism, and illicit trafficking of radioactive materials pose significant security challenges, driving the demand for advanced radiological detection technologies and border monitoring solutions.

Technological Advancements: Recent advancements in radiological detection technologies, including the development of compact, lightweight, and portable detectors, improved sensitivity, and spectral resolution, are driving market growth and innovation.

Regulatory Compliance Requirements: Stringent regulatory requirements and international standards governing radiation safety, nuclear security, and customs inspection drive the adoption of radiological detection solutions by government agencies, regulatory bodies, and critical infrastructure operators.

Government Investments in Nuclear Security: Governments worldwide are investing in nuclear security programs, border security initiatives, and radiation detection infrastructure to enhance national security, counter nuclear smuggling, and prevent radiological terrorism.

Market Drivers

Security Threats: The increasing risk of radiological terrorism, nuclear proliferation, and nuclear accidents drives the demand for radiological detectors to detect, identify, and mitigate radiation threats and hazards.

Technological Advancements: Continuous advancements in radiological detection technologies, including improved sensitivity, selectivity, and reliability, enhance the effectiveness and efficiency of radiation detection and monitoring systems.

Regulatory Compliance: Stringent regulatory requirements and standards governing radiation safety, nuclear security, and customs inspection mandate the deployment of radiological detection solutions by government agencies, border security forces, and critical infrastructure operators.

Government Initiatives: Government initiatives, funding programs, and international collaborations aimed at enhancing nuclear security, preventing nuclear terrorism, and countering illicit trafficking of radioactive materials drive market growth and innovation in radiological detection technologies.

Market Restraints

Budgetary Constraints: Budgetary constraints and funding limitations pose challenges for governments and organizations seeking to invest in radiological detection infrastructure, procurement of advanced detection systems, and maintenance of existing radiation monitoring networks.

Supply Chain Disruptions: Supply chain disruptions, component shortages, and manufacturing delays caused by global events such as the Covid-19 pandemic and geopolitical tensions impact the availability, affordability, and delivery of radiological detectors.

Complex Regulatory Environment: The complex regulatory environment governing the export, import, and use of radiological detection technologies poses challenges for market players in terms of compliance, licensing, and export control requirements.

Technological Complexity: The complexity of radiological detection technologies, including the need for specialized training, maintenance, and technical support, may deter end-users from adopting advanced detection solutions.

Market Opportunities

Development of Next-Generation Detectors: Opportunities exist for the development of next-generation radiological detectors with improved sensitivity, selectivity, portability, and interoperability to address emerging threats and customer requirements.

Expansion into Emerging Markets: Emerging markets in Asia-Pacific, Latin America, and the Middle East present opportunities for market players to expand their presence, penetrate new verticals, and capitalize on growing demand for radiation detection solutions.

Integration with AI and IoT: Integration with artificial intelligence (AI) algorithms, machine learning (ML) techniques, and Internet of Things (IoT) platforms enables the development of smart, autonomous radiological detection systems for real-time monitoring, data analysis, and threat assessment.

Customized Solutions for End-User Needs: Tailored solutions for specific end-user requirements, including border security, customs inspection, nuclear power plants, and medical facilities, offer opportunities for market players to differentiate themselves and address niche markets.

Market Dynamics

The radiological detector market operates in a dynamic environment influenced by various factors, including technological advancements, security threats, regulatory requirements, and market trends. Key dynamics driving market growth and innovation include:

Technological Innovation: Continuous advancements in radiological detection technologies, including the development of new sensor materials, detection algorithms, and data analytics techniques, drive market innovation and product differentiation.

Security Threat Landscape: Evolving security threats, including radiological terrorism, nuclear smuggling, and nuclear accidents, shape market dynamics and drive demand for advanced radiological detection solutions.

Regulatory Environment: Stringent regulatory requirements governing radiation safety, nuclear security, and customs inspection influence market dynamics, product development strategies, and customer procurement decisions.

Market Consolidation: Market consolidation through mergers, acquisitions, and strategic partnerships enables companies to enhance their product portfolios, expand their market reach, and achieve economies of scale in manufacturing and distribution.

Regional Analysis

The radiological detector market exhibits regional variations in terms of market size, growth trends, and regulatory frameworks. Key regions driving market growth and innovation include:

North America: North America dominates the radiological detector market, driven by robust demand from government agencies, defense forces, nuclear facilities, and critical infrastructure operators for radiation detection and monitoring solutions.

Europe: Europe is a prominent market for radiological detectors, characterized by stringent regulatory requirements, technological innovation, and government investments in nuclear security, border surveillance, and radiation monitoring infrastructure.

Asia-Pacific: Asia-Pacific is a rapidly growing market for radiological detectors, fueled by increasing security threats, nuclear proliferation concerns, and government initiatives to enhance nuclear security, counter terrorism, and prevent illicit trafficking of radioactive materials.

Middle East and Africa: The Middle East and Africa region present opportunities for market players to expand their presence in emerging markets, address growing security concerns, and support government efforts to enhance nuclear safety and security.

Latin America: Latin America offers potential for market growth in radiological detection technologies, driven by increasing investments in border security, customs inspection, and critical infrastructure protection against radiological threats and hazards.

Competitive Landscape

Leading Companies in the Radiological Detector Market:

Canberra Industries, Inc. (a subsidiary of Mirion Technologies, Inc.)

Thermo Fisher Scientific Inc.

FLIR Systems, Inc.

Ludlum Measurements, Inc.

AMETEK, Inc.

Berkeley Nucleonics Corporation

Smiths Detection Inc. (a subsidiary of Smiths Group plc)

Mirion Technologies, Inc.

Landauer, Inc. (a subsidiary of Fortive Corporation)

Leidos Holdings, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

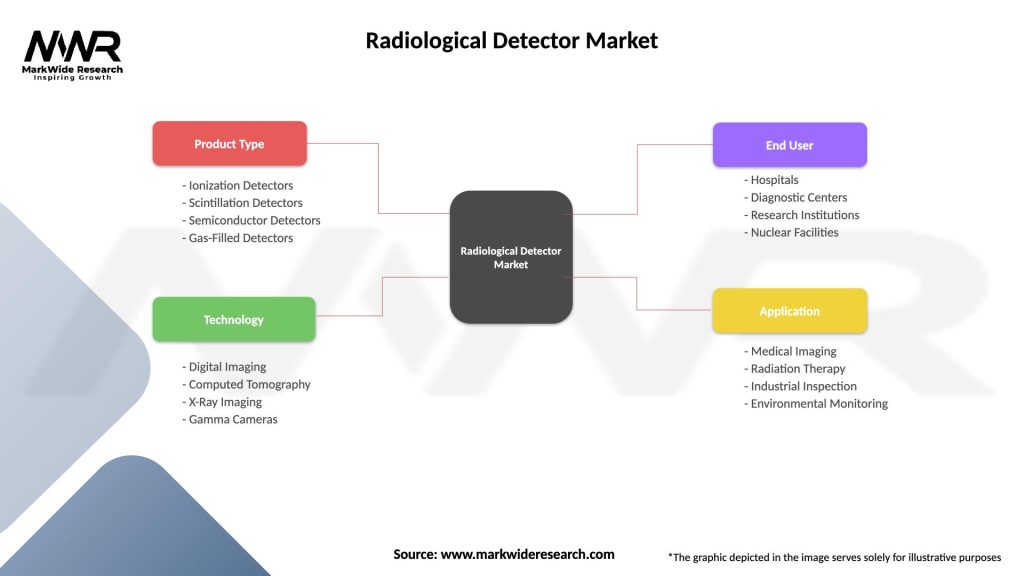

Segmentation

The radiological detector market can be segmented based on various factors such as technology type, application, end-user vertical, and geography. Common segmentation categories include:

Application: Homeland security, border monitoring, customs inspection, environmental monitoring, medical imaging, nuclear industry safety, and research applications.

End-User Vertical: Government agencies, defense forces, law enforcement agencies, border security forces, critical infrastructure operators, nuclear facilities, research institutions, and medical facilities.

Geography: North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America.

Segmentation provides a structured approach to understanding market dynamics, identifying growth opportunities, and targeting specific customer segments with tailored products and solutions.

Category-wise Insights

Scintillation Detectors: Scintillation detectors are widely used for radiation detection and spectroscopy applications in homeland security, nuclear medicine, environmental monitoring, and nuclear research. Key trends include the development of scintillation materials, photodetectors, and readout electronics for improved energy resolution, sensitivity, and timing performance.

Semiconductor Detectors: Semiconductor detectors offer high energy resolution, radiation hardness, and efficiency for gamma-ray spectroscopy, X-ray imaging, and neutron detection applications. Trends include the use of semiconductor materials such as silicon, germanium, and cadmium zinc telluride (CZT) for radiation detection and imaging in security, defense, and medical imaging applications.

Gas-filled Detectors: Gas-filled detectors such as ionization chambers, proportional counters, and Geiger-Mueller (GM) tubes are commonly used for radiation detection and surveying in nuclear facilities, environmental monitoring, and medical diagnostics. Trends include the miniaturization, portability, and automation of gas-filled detectors for field-deployable radiation monitoring systems.

Solid-state Detectors: Solid-state detectors based on silicon, diamond, and other semiconductor materials offer advantages such as compact size, high sensitivity, and low power consumption for radiation detection and imaging applications. Trends include the development of solid-state photodetectors, avalanche photodiodes (APDs), and complementary metal-oxide-semiconductor (CMOS) imagers for medical imaging, security screening, and nuclear physics research.

Key Benefits for Industry Participants and Stakeholders

Enhanced Radiation Detection Capabilities: Radiological detectors enable enhanced detection and identification of radioactive materials, isotopes, and contamination sources for nuclear security, environmental monitoring, and public health protection.

Improved Safety and Security: Radiological detectors contribute to improved safety and security by providing early warning, threat detection, and radiation monitoring capabilities for nuclear facilities, critical infrastructure, and public spaces.

Effective Response to Radiological Incidents: Radiological detectors facilitate effective response to radiological incidents, nuclear accidents, and radiological emergencies by providing real-time data, situational awareness, and decision support for emergency responders and incident commanders.

Compliance with Regulatory Requirements: Radiological detectors help organizations comply with regulatory requirements, international standards, and best practices for radiation safety, nuclear security, and emergency preparedness and response.

Risk Mitigation and Liability Reduction: Radiological detectors assist organizations in mitigating risks, reducing liabilities, and safeguarding assets against radiological threats, hazards, and regulatory non-compliance.

SWOT Analysis

A SWOT analysis provides insights into the strengths, weaknesses, opportunities, and threats facing the radiological detector market:

Strengths:

Advanced detection technologies

Regulatory compliance capabilities

Strategic partnerships and collaborations

Established customer base and market presence

Weaknesses:

Technological complexity

High upfront costs

Dependence on government funding

Supply chain vulnerabilities

Opportunities:

Technological innovation

Market expansion into emerging regions

Integration with AI and IoT

Customized solutions for specific applications

Threats:

Intense competition

Regulatory constraints

Budgetary constraints

Cybersecurity risks

Understanding these factors through a SWOT analysis helps industry participants identify strategic priorities, mitigate risks, and capitalize on opportunities for growth and innovation in the radiological detector market.

Market Key Trends

Integration with AI and Machine Learning: Integration with artificial intelligence (AI) algorithms and machine learning (ML) techniques enables intelligent data analysis, anomaly detection, and predictive modeling for enhanced radiation detection and threat assessment.

Miniaturization and Portability: Trends towards miniaturization and portability drive the development of handheld, wearable, and unmanned radiological detectors for field-deployable radiation monitoring, emergency response, and reconnaissance applications.

Wireless Connectivity and IoT Integration: Wireless connectivity and integration with Internet of Things (IoT) platforms enable remote monitoring, data sharing, and real-time alerts for radiation detection networks, border surveillance systems, and critical infrastructure protection.

Multiparametric Sensing and Fusion: Trends towards multiparametric sensing and data fusion combine multiple detection modalities, such as gamma-ray spectroscopy, neutron detection, and chemical analysis, to enhance the sensitivity, selectivity, and reliability of radiological detectors.

Covid-19 Impact

The Covid-19 pandemic has had a mixed impact on the radiological detector market. While the pandemic has led to disruptions in supply chains, manufacturing operations, and customer demand, it has also highlighted the importance of radiological detection and monitoring for public health, emergency response, and biosafety applications.

Supply Chain Disruptions: The Covid-19 pandemic has caused disruptions in the supply chain, component shortages, and manufacturing delays, impacting the availability, affordability, and delivery of radiological detectors and related equipment.

Increased Demand for Biosafety Applications: The pandemic has increased the demand for radiological detectors and monitoring systems for biosafety applications, including medical imaging, radiation therapy, and laboratory diagnostics, to ensure patient safety and regulatory compliance.

Remote Monitoring and Telemedicine: Trends towards remote monitoring, telemedicine, and virtual healthcare services drive the adoption of radiological detectors with wireless connectivity, remote data access, and cloud-based analytics for remote patient monitoring and diagnostic imaging.

Focus on Emergency Preparedness: The Covid-19 pandemic has underscored the importance of emergency preparedness, disaster response, and public health surveillance, driving investments in radiological detection infrastructure, training, and capacity building for pandemic preparedness and response.

Key Industry Developments

Next-Generation Detectors: Key industry players are investing in the development of next-generation radiological detectors with improved sensitivity, resolution, and reliability for homeland security, border surveillance, and nuclear safety applications.

Smart Detection Systems: Trends towards smart detection systems integrate advanced sensors, data analytics, and AI algorithms to enable real-time monitoring, anomaly detection, and threat assessment for radiation detection networks and critical infrastructure protection.

Modular and Scalable Platforms: Modular and scalable platforms offer flexibility, interoperability, and upgradeability for radiological detection systems, allowing users to customize configurations, expand capabilities, and adapt to evolving threats and requirements.

Cloud-Based Solutions: Cloud-based solutions enable remote data access, centralized management, and real-time collaboration for radiological detection networks, border surveillance systems, and emergency response operations.

Analyst Suggestions

Invest in R&D and Innovation: Industry players should invest in research and development (R&D) to develop innovative detection technologies, improve product performance, and address emerging customer needs and market trends.

Enhance Collaboration and Partnerships: Collaboration with government agencies, research institutions, and industry partners facilitates technology transfer, knowledge exchange, and joint development of advanced radiological detection solutions.

Diversify Product Portfolio: Diversification of product portfolio with a range of detectors, sensors, and integrated systems for different applications and end-user verticals enhances market competitiveness and revenue growth potential.

Address Regulatory Compliance: Compliance with regulatory requirements, international standards, and best practices for radiation safety, nuclear security, and customs inspection is essential to gain customer trust and market acceptance.

Future Outlook

The radiological detector market is expected to witness steady growth and innovation driven by increasing security threats, technological advancements, and regulatory compliance requirements. Key trends shaping the future outlook of the market include:

Technological Innovation: Continuous advancements in detection technologies, including improved sensitivity, resolution, and interoperability, drive market innovation and product differentiation.

Market Expansion: Market expansion into emerging regions, new verticals, and niche applications offers growth opportunities for industry players to diversify revenue streams and capture market share.

Integration with AI and IoT: Integration with artificial intelligence (AI) algorithms and Internet of Things (IoT) platforms enables the development of smart, autonomous detection systems for real-time monitoring, data analysis, and threat assessment.

Customized Solutions: Tailored solutions for specific end-user requirements, regulatory compliance, and emerging threats enable industry players to differentiate themselves and address niche markets effectively.

Conclusion

The radiological detector market plays a critical role in safeguarding public health, ensuring nuclear safety, and countering radiological terrorism. With increasing security threats, technological advancements, and regulatory compliance requirements, the demand for advanced radiological detection technologies continues to rise worldwide. Industry players must focus on innovation, collaboration, and market expansion to capitalize on growing opportunities and address evolving customer needs in the dynamic and competitive radiological detector market.

What is Radiological Detector?

Radiological detectors are devices used to identify and measure ionizing radiation, including alpha, beta, and gamma radiation. They are essential in various applications such as medical imaging, nuclear power plants, and environmental monitoring.

What are the key players in the Radiological Detector Market?

Key players in the Radiological Detector Market include companies like Thermo Fisher Scientific, Siemens Healthineers, and General Electric. These companies are known for their innovative technologies and extensive product offerings in radiation detection.

What are the growth factors driving the Radiological Detector Market?

The growth of the Radiological Detector Market is driven by increasing demand for radiation safety in healthcare, rising nuclear energy production, and the need for environmental monitoring. Additionally, advancements in detection technologies are enhancing the effectiveness of these devices.

What challenges does the Radiological Detector Market face?

The Radiological Detector Market faces challenges such as high costs associated with advanced detection technologies and regulatory compliance issues. Additionally, the need for skilled personnel to operate these devices can limit market growth.

What opportunities exist in the Radiological Detector Market?

Opportunities in the Radiological Detector Market include the development of portable detection devices and the integration of artificial intelligence for improved data analysis. Furthermore, increasing investments in healthcare infrastructure present significant growth potential.

What trends are shaping the Radiological Detector Market?

Trends in the Radiological Detector Market include the shift towards digital detection technologies and the growing emphasis on real-time monitoring solutions. Additionally, there is a rising focus on sustainability and eco-friendly materials in the manufacturing of these detectors.

Leading Companies in the Radiological Detector Market:

Canberra Industries, Inc. (a subsidiary of Mirion Technologies, Inc.)

Thermo Fisher Scientific Inc.

FLIR Systems, Inc.

Ludlum Measurements, Inc.

AMETEK, Inc.

Berkeley Nucleonics Corporation

Smiths Detection Inc. (a subsidiary of Smiths Group plc)

Mirion Technologies, Inc.

Landauer, Inc. (a subsidiary of Fortive Corporation)

Leidos Holdings, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.